Algeria Auto Finance Market Outlook to 2029

By Market Structure, By Lender Type, By Vehicle Type (New vs. Used), By Tenure, By Consumer Age Group and By Region

Report Overview

Report Code

TDR0156

Coverage

North America

Published

April 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Algeria Auto Finance Market Outlook to 2029 - By Market Structure, By Lender Type, By Vehicle Type (New vs. Used), By Tenure, By Consumer Age Group and By Region” provides a comprehensive analysis of the auto finance market in Algeria. The report includes an overview and evolution of the industry, overall market size in terms of disbursed loans, market segmentation, trends and developments, regulatory framework, customer-level behavior, challenges, and competitive landscape with cross-comparison, market opportunities and constraints, and profiling of major lending institutions in the Algerian auto finance market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Algeria Auto Finance Market Outlook to 2029 - By Market Structure, By Lender Type, By Vehicle Type (New vs. Used), By Tenure, By Consumer Age Group and By Region” provides a comprehensive analysis of the auto finance market in Algeria. The report includes an overview and evolution of the industry, overall market size in terms of disbursed loans, market segmentation, trends and developments, regulatory framework, customer-level behavior, challenges, and competitive landscape with cross-comparison, market opportunities and constraints, and profiling of major lending institutions in the Algerian auto finance market. The report concludes with future market projections based on disbursal value, lender type, vehicle category, region, and consumer segments, including cause-effect analysis and success stories to highlight potential growth strategies and key concerns.

Algeria Auto Finance Market Overview and Size

The Algeria auto finance market reached a valuation of DZD 320 Billion in 2023, driven by rising vehicle demand, limited public transport options in secondary cities, and an increasing reliance on installment-based vehicle purchases. Key financial institutions include Banque Nationale d’Algérie (BNA), Société Générale Algérie, Al Salam Bank, and BNP Paribas El Djazaïr, alongside a growing role of automotive captives linked with local dealerships and importers.

In 2023, Al Salam Bank launched a tailored Shariah-compliant auto finance program targeting young professionals and first-time buyers. This initiative aims to address unmet demand within a largely unbanked population, boosting penetration rates in cities like Algiers, Oran, and Constantine.

Market Size for Algeria Auto Finance Industry on the Basis of Credit Disbursed in USD Billion, 2018-2023

What Factors are Leading to the Growth of Algeria Auto Finance Market:

Limited Public Transportation Infrastructure: The underdeveloped public transport network in Tier 2 and Tier 3 cities has led to increased private vehicle ownership, which in turn has boosted demand for auto financing. Approximately 62% of new car buyers in 2023 opted for financing, up from 51% in 2020.

Islamic Finance Penetration: Shariah-compliant auto finance products are witnessing strong adoption, particularly among younger demographics. In 2023, Islamic finance accounted for 28% of all auto loans disbursed, driven by offerings from Al Baraka Bank and Al Salam Bank.

Regulatory Support and Import Relaxation: Recent government reforms allowing selective vehicle imports have increased vehicle supply and reduced wait times. These regulatory changes have improved the lending environment and created a more favorable auto finance ecosystem.

Which Industry Challenges Have Impacted the Growth for Algeria Auto Finance Market

Limited Credit Penetration and Financial Inclusion: A significant portion of Algeria’s population remains unbanked or underbanked, which limits their access to formal credit and auto loans. As of 2023, only around 33% of adults in Algeria held a bank account, and less than 18% had access to any form of consumer credit, making it difficult for lenders to scale. This low financial penetration remains one of the most critical bottlenecks for auto finance expansion, especially in rural and semi-urban markets.

High Interest Rates and Inflation Volatility: Elevated interest rates and persistent inflation have increased the cost of borrowing. In 2023, average lending rates for auto loans ranged between 10% and 13%, compared to 6-8% in peer North African markets. This deters consumers from taking vehicle loans, especially for non-essential or used vehicles, resulting in delayed purchases and increased preference for cash transactions.

Regulatory Uncertainty and Import Controls: Frequent changes in vehicle import policies and registration norms have disrupted vehicle supply chains and impacted loan disbursements. For example, a moratorium on new vehicle imports between 2020 and 2022 led to a backlog in financing applications and artificially inflated vehicle prices, directly impacting lending volumes.

What are the Regulations and Initiatives which have Governed the Market

Consumer Credit Law and Islamic Finance Integration: Algeria's Central Bank has introduced several updates to the consumer credit framework to encourage transparent lending practices and compliance with Islamic finance principles. In 2023, over 25% of all auto loans were Shariah-compliant, supported by regulatory mandates for profit-sharing structures and ethical lending practices.

Import Licensing and Vehicle Quotas: The government maintains strict quotas on vehicle imports, especially for new vehicles, and mandates licensing for importers. While the 2023 reforms allowed limited reopening of imports through certified dealers, only models that meet Euro 4 emissions standards and are less than 3 years old were approved. This regulation indirectly affects the auto finance market, as limited vehicle availability impacts loan demand.

Digitization Push and Central Credit Registry: The establishment of a central credit bureau (Bureau de Crédit Algérien) is helping reduce credit risk through better borrower profiling. By 2024, more than 70 financial institutions were integrated into the registry, enabling faster KYC and underwriting for auto finance. This is expected to gradually improve approval rates and support responsible lending.

Algeria Auto Finance Market Segmentation

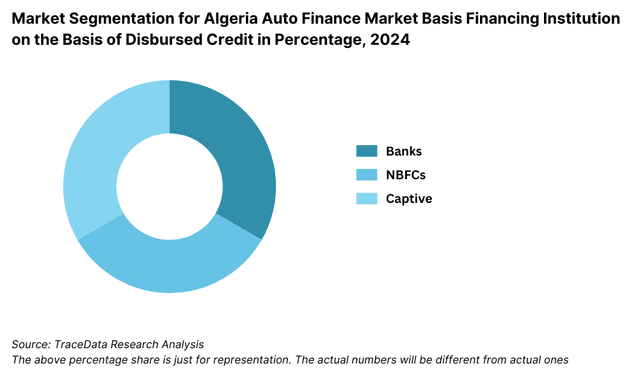

By Market Structure: The auto finance landscape in Algeria is primarily dominated by bank-led financing, given the dominance of public sector banks like Banque Nationale d’Algérie (BNA) and Banque Extérieure d’Algérie (BEA), which offer structured loan products. These institutions benefit from their large branch networks, government-backed lending programs, and consumer trust. Captive financing, though emerging, is mostly offered through partnerships between importers and foreign automotive brands such as Renault and Hyundai. Islamic finance institutions are gaining ground due to increasing demand for Shariah-compliant financial products, especially among younger and religious consumers.

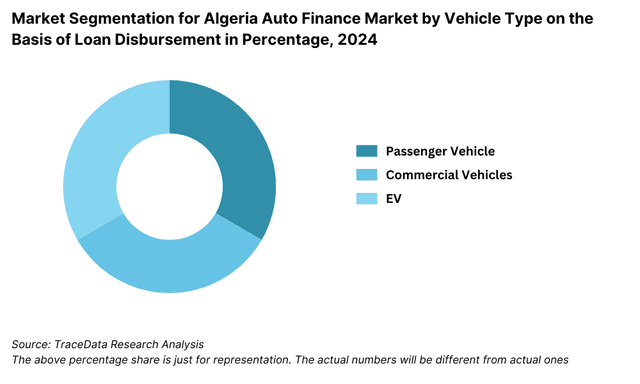

By Vehicle Type: Financing for new vehicles continues to dominate the market due to favorable bank partnerships with new car dealerships, fixed-rate financing, and warranty assurances, making them more appealing to both lenders and borrowers. However, used car financing is steadily growing as vehicle affordability declines and more organized used car channels emerge, especially in urban centers like Algiers and Oran.

By Tenure: The most preferred loan tenures are 36 to 60 months, striking a balance between monthly affordability and total interest payout. Shorter tenures (under 24 months) are rare due to high upfront EMI burdens, while tenures beyond 60 months are limited due to asset depreciation and credit risk concerns.

Competitive Landscape in Algeria Auto Finance Market

The Algeria auto finance market is moderately fragmented, with major public sector banks dominating the lending ecosystem. However, recent years have witnessed increased activity from Islamic banks, international joint-venture banks, and captive finance arms of global automotive brands. New digital lending platforms are also beginning to emerge, particularly in urban regions, providing alternative financing channels to underserved customer segments.

| Company Name | Founding Year | Original Headquarters |

| RCI Services Algeria | 2006 | Boulogne-Billancourt, France |

| Bank ABC Algeria | 1998 | Manama, Bahrain |

| CNEP-Banque | 1964 | Algiers, Algeria |

| ALD Automotive Algeria | 2007 | Rueil-Malmaison, France |

| Al Salam Bank Algeria | 2008 | Manama, Bahrain |

| Sofinance SPA | 2001 | Algiers, Algeria |

Some of the recent competitor trends and key information about major players include:

Banque Nationale d’Algérie (BNA): As the country’s leading state-owned bank, BNA continues to be a key financier for both new and used vehicles. In 2023, the bank disbursed over DZD 100 Billion in auto loans, supported by its extensive branch network and collaborations with leading dealerships across Algeria.

Société Générale Algérie: The bank has focused on expanding digital loan processing capabilities. In 2023, over 40% of auto loan applications were processed digitally, reducing average loan disbursal time from 7 days to 3 days. It has also partnered with European car brands like Peugeot and Citroën for special financing offers.

Al Salam Bank Algeria: This Islamic bank has emerged as a strong player in Shariah-compliant vehicle financing, particularly targeting young professionals. It reported a 32% year-on-year increase in auto loan disbursals in 2023, driven by flexible payment structures and minimal documentation requirements.

BNP Paribas El Djazaïr: A joint-venture subsidiary of the global BNP Paribas Group, it offers competitive fixed-rate auto loans for imported vehicles. In 2023, the bank expanded its footprint in Oran and Constantine, introducing bilingual loan advisory services and customized tenure options.

Baraka Bank Algeria: Another Shariah-compliant lender, Baraka Bank saw a growing preference among salaried and first-time buyers. The bank introduced a deferred installment feature in 2023, allowing customers to postpone payments for the first 3 months—attracting over 5,000 new loan customers.

Renault Algérie Captive Finance: Established to support vehicle sales of Renault, Dacia, and other affiliated brands, the captive unit facilitated over 8,500 vehicle loans in 2023. It is working closely with showrooms to offer on-site instant approvals, which helped boost Renault’s new vehicle sales in a challenging economic environment.

What Lies Ahead for Algeria Auto Finance Market?

The Algeria auto finance market is expected to witness steady growth through 2029, supported by a growing middle class, expanding vehicle ownership, and improving access to formal credit. The market is projected to register a healthy CAGR between 2024 and 2029, driven by financial innovation, policy liberalization, and the emergence of digital lending ecosystems.

Expansion of Islamic Auto Finance: Shariah-compliant financing is poised for significant growth, as demand increases among younger and religious consumers. With more Islamic banks introducing flexible, interest-free vehicle financing solutions, the segment is expected to account for over 35% of new disbursals by 2029. Tailored offerings, reduced paperwork, and ethical lending principles will drive consumer preference.

Digitalization and Fintech Penetration: The adoption of digital lending platforms is set to accelerate, particularly in urban centers like Algiers, Oran, and Constantine. Fintech players are expected to disrupt traditional banking by offering instant loan approvals, AI-powered risk assessments, and mobile-first onboarding. By 2029, over 50% of first-time vehicle buyers are likely to explore digital finance options.

Used Vehicle Financing Growth: With new vehicle prices remaining high due to inflation and import constraints, the used car segment is projected to grow. Financing institutions are expected to expand offerings for vehicles under 5 years old, especially through dealer partnerships. This shift will make auto ownership more affordable, expanding financing penetration in semi-urban regions.

Increased Public-Private Partnerships (PPP): The government is expected to collaborate with financial institutions to promote credit access among underbanked populations. This could include interest rate subsidies, vehicle loan guarantees, or micro-credit schemes targeting youth, women, and rural populations—catalyzing broader vehicle affordability and mobility.

Future Outlook and Projections for Algeria Car Finance Market Size on the Basis of Loan Disbursements in USD Billion, 2024-2029

Algeria Auto Finance Market Segmentation

- By Market Structure:

o Public Sector Banks

o Private Banks

o Islamic Finance Institutions

o Captive Financing Arms

o Fintech Lenders

o Dealer-Led Financing Programs

o Informal Lending Channels - By Lender Type:

o Banque Nationale d’Algérie (BNA)

o Société Générale Algérie

o BNP Paribas El Djazaïr

o Al Salam Bank

o Baraka Bank

o Renault Algérie Captive Finance

o Fintech Startups - By Vehicle Type:

o New Passenger Cars

o Used Passenger Cars

o Commercial Vehicles (LCVs, Pickups)

o Electric/Hybrid Vehicles - By Loan Tenure:

o Less than 24 Months

o 24–36 Months

o 36–60 Months

o More than 60 Months - By Age of Vehicle (for Used Car Financing):

o Less than 2 Years

o 2–5 Years

o More than 5 Years - By Age of Consumer:

o 18–25 Years

o 26–40 Years

o 41–55 Years

o 56+ Years - By Region:

o Northern (Algiers, Tizi Ouzou)

o Western (Oran, Tlemcen)

o Central (Blida, Médéa)

o Eastern (Constantine, Annaba)

o Southern (Ghardaïa, Tamanrasset)

Players Mentioned in the Report (Banks):

- Banque Nationale d’Algérie (BNA)

- Banque Extérieure d’Algérie (BEA)

- Banque de l’Agriculture et du Développement Rural (BADR)

- Banque de Développement Local (BDL)

- Crédit Populaire d’Algérie (CPA)

- Caisse Nationale d’Épargne et de Prévoyance (CNEP Banque)

- Banque Al Baraka Algérie

- Arab Banking Corporation (ABC) Algérie

- Société Générale Algérie

- BNP Paribas El Djazaïr

- Trust Bank Algérie

- Gulf Bank Algeria

- Fransabank El Djazaïr

- HSBC Algeria

- Natixis Banque Algérie

- Arab Bank Algeria

- Calyon Algérie

Players Mentioned in the Report (NBFCs):

- Wafasalaf

- Eqdom

- Sogelease

- Taslif

- Saham Finances

- Salafin

- BMCI Leasing Auto

Players Mentioned in the Report (Captive):

- Toyota Financial Services Algeria

- Volkswagen Financial Services Algeria

- Mercedes-Benz Financial Services Algeria

- BMW Financial Services Algeria

- Stellantis Financial Services Algeria

Key Target Audience:

- Commercial and Retail Banks

- Automotive Finance Companies

- Captive Finance Arms

- Vehicle Dealerships (New & Used)

- Fintech & Digital Lending Startups

- Government and Regulatory Bodies (e.g., Bank of Algeria, Ministry of Finance)

- Market Research and Strategy Consultants

Time Period:

- Historical Period: 2018–2023

- Base Year: 2024

- Forecast Period: 2024–2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-Role of Entities, Stakeholders, and challenges they face.

4.2. Relationship and Engagement Model between Banks-Dealers, NBFCs-Dealers and Captive-Dealers-Commission Sharing Model, Flat Fee Model and Revenue streams

5.1. New Car and Used Car Sales in Algeria by type of vehicle, 2018-2024

8.1. Credit Disbursed, 2018-2024

8.2. Outstanding Loan, 2018-2024

9.1. By Market Structure (Bank-Owned, Multi-Finance, and Captive Companies), 2023-2024

9.2. By Vehicle Type (Passenger, Commercial and EV), 2023-2024

9.3. By Region, 2023-2024

9.4. By Type of Vehicle (New and Used), 2023-2024

9.5. By Average Loan Tenure (0-2 years, 3-5 years, 6-8 years, above 8 years), 2023-2024

10.1. Customer Landscape and Cohort Analysis

10.2. Customer Journey and Decision-Making

10.3. Need, Desire, and Pain Point Analysis

10.4. Gap Analysis Framework

11.1. Trends and Developments for Algeria Car Finance Market

11.2. Growth Drivers for Algeria Car Finance Market

11.3. SWOT Analysis for Algeria Car Finance Market

11.4. Issues and Challenges for Algeria Car Finance Market

11.5. Government Regulations for Algeria Car Finance Market

12.1. Market Size and Future Potential for Online Car Financing Aggregators, 2018-2029

12.2. Business Model and Revenue Streams

12.3. Cross Comparison of Leading Digital Car Finance Companies Based on Company Overview, Revenue Streams, Loan Disbursements/Number of Leads Generated, Operating Cities, Number of Branches, and Other Variables

13.1. Finance Penetration Rate and Average Down Payment for New and Used Cars, 2018-2029

13.2. How Finance Penetration Rates are Changing Over the Years with Reasons

13.3. Type of Car Segment for which Finance Penetration is Higher

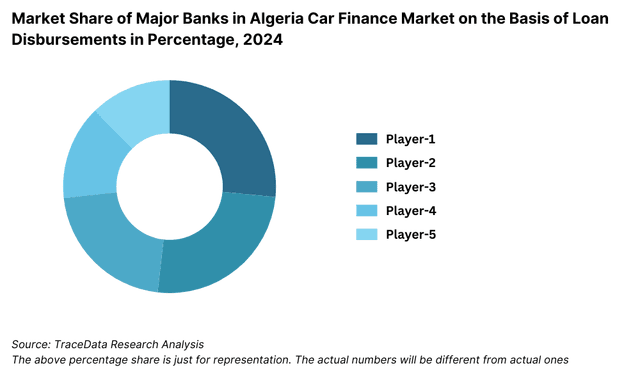

17.1. Market Share of Key Banks in Algeria Car Finance Market, 2024

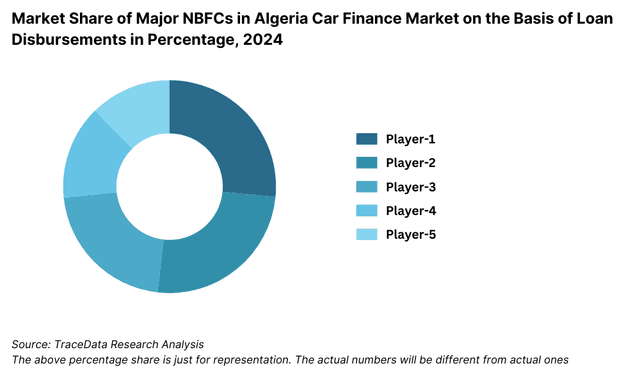

17.2. Market Share of Key NBFCs in Algeria Car Finance Market, 2024

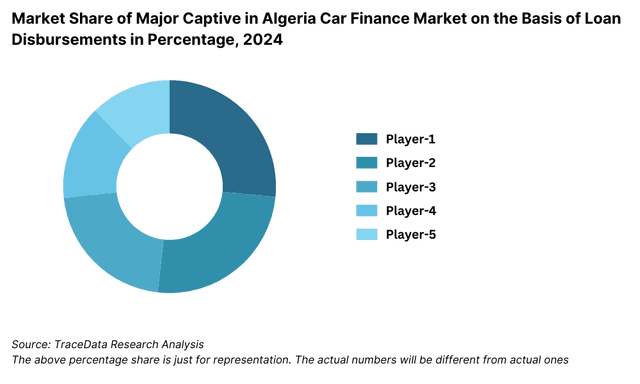

17.3. Market Share of Key Captive in Algeria Car Finance Market, 2024

17.4. Benchmark of Key Competitors in Algeria Car Finance Market, including Variables such as Company Overview, USP, Business Strategies, Strengths, Weaknesses, Business Model, Number of Branches, Product Features, Interest Rate, NPA, Loan Disbursed, Outstanding Loans, Tie-Ups and others

17.5. Strengths and Weaknesses

17.6. Operating Model Analysis Framework

17.7. Gartner Magic Quadrant

17.8. Bowmans Strategic Clock for Competitive Advantage

18.1. Credit Disbursed, 2025-2029

18.2. Outstanding Loan, 2025-2029

19.1. By Market Structure (Bank-Owned, Multi-Finance, and Captive Companies), 2025-2029

19.2. By Vehicle Type (Passenger, Commercial and EV), 2025-2029

19.3. By Region, 2025-2029

19.4. By Type of Vehicle (New and Used), 2025-2029

19.5. By Average Loan Tenure (0-2 years, 3-5 years, 6-8 years, above 8 years), 2025-2029

19.6. Recommendations

19.7. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all key demand-side and supply-side stakeholders across the Algeria Auto Finance Market. This includes public sector banks, private banks, Islamic finance institutions, captive finance arms, fintech lenders, vehicle dealerships, and end-consumers.

Sourcing is done through industry journals, regulatory publications, company websites, and proprietary databases to construct a landscape of key participants and financing models in the Algerian market.

Step 2: Desk Research

A comprehensive desk research process is undertaken, leveraging secondary and proprietary data sources such as government reports, bank financial disclosures, automotive sales databases, and trade publications.

This includes gathering data on loan disbursal values, lender market share, penetration rates, interest rate structures, vehicle import trends, and consumer credit metrics.

Key company-level information is obtained through annual reports, press releases, investor presentations, and public filings to understand financial health, lending strategy, and distribution network reach.

Step 3: Primary Research

In-depth interviews are conducted with senior executives and mid-level managers from auto finance institutions (banks, captives, fintechs), dealerships, and loan agents.

The objective is to validate secondary findings, verify disbursal volumes, understand tenure preferences, default rates, approval times, and competitive dynamics in the market.

Bottom-up analysis is undertaken by collecting lender-level loan disbursal volumes and aggregating them to estimate the overall market size.

To ensure robust validation, disguised interviews are carried out with dealerships and finance agents, posing as potential buyers, to cross-verify information on commissions, documentation processes, approval criteria, and financing terms.

Step 4: Sanity Check

Market triangulation is conducted using both top-down and bottom-up methodologies to ensure consistency and reliability of insights.

- Forecasting models are developed to assess future market growth scenarios under various macroeconomic and policy environments, followed by sensitivity testing of key variables such as interest rates, vehicle prices, and loan default rates.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Algeria Auto Finance Market holds significant potential for growth, reaching an estimated valuation of DZD 320 Billion in 2023. Key growth enablers include rising vehicle ownership, increasing demand for credit-based purchases, and a growing young population entering the workforce. The market is also expected to benefit from digitalization, regulatory liberalization, and the expanding reach of Islamic and captive financing solutions, particularly in underserved regions.

The Algeria Auto Finance Market features a mix of public sector banks, private banks, Islamic finance institutions, and emerging fintechs. Prominent players include Banque Nationale d’Algérie (BNA), Société Générale Algérie, Al Salam Bank, BNP Paribas El Djazaïr, and Renault Algérie Captive Finance. These institutions are recognized for their extensive networks, specialized auto loan products, and partnerships with vehicle dealers.

Major growth drivers include the underpenetrated credit ecosystem, growing demand for vehicles due to limited public transport in secondary cities, and increased acceptance of Islamic finance products. The market is also being fueled by favorable demographics, improved digital lending infrastructure, and government-backed initiatives to promote vehicle ownership among first-time buyers and low-income households.

The market faces multiple challenges including low financial inclusion, high interest rates, and inflationary pressures that affect affordability. Regulatory uncertainty around vehicle imports and financing norms also impedes consistent lending growth. Additionally, limited penetration of used vehicle financing and insufficient fintech scalability in rural areas pose further obstacles to market expansion.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0