Argentina Logistics and warehousing Market Outlook to 2029

By Service Mix (Freight Forwarding, Warehousing, and Value-Added Services), By End User (Retail, Automotive, FMCG, Healthcare, Others), By Mode of Freight (Road, Rail, Air, Sea), and By Region

Report Overview

Report Code

TDR0252

Coverage

Central and South America

Published

September 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Argentina Logistics and Warehousing Market Outlook to 2029 – By Service Mix (Freight Forwarding, Warehousing, and Value-Added Services), By End User (Retail, Automotive, FMCG, Healthcare, Others), By Mode of Freight (Road, Rail, Air, Sea), and By Region.” provides a comprehensive analysis of the logistics and warehousing industry in Argentina. The report covers the market's overview and genesis, overall market size by revenue, segmentation by services and end users, trends and developments, regulatory environment, customer profiles, challenges, and a comparative competitive landscape.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Argentina Logistics and Warehousing Market Outlook to 2029 – By Service Mix (Freight Forwarding, Warehousing, and Value-Added Services), By End User (Retail, Automotive, FMCG, Healthcare, Others), By Mode of Freight (Road, Rail, Air, Sea), and By Region.” provides a comprehensive analysis of the logistics and warehousing industry in Argentina. The report covers the market's overview and genesis, overall market size by revenue, segmentation by services and end users, trends and developments, regulatory environment, customer profiles, challenges, and a comparative competitive landscape. It concludes with future market projections by service line, region, and industry verticals, and includes success case studies and key insights into opportunities and constraints.

Argentina Logistics and Warehousing Market Overview and Size

The Argentina logistics and warehousing market was valued at ARS 4.28 trillion in 2023, supported by recovering trade volumes, domestic consumption, and rising e-commerce penetration. The sector is primarily driven by key players such as Andreani, Ocasa, DHL, and OCA Logística, offering integrated logistics and warehousing solutions across the country.

The government’s National Logistics Plan 2030 has introduced multiple infrastructure upgrades, including freight rail improvements and development of inland logistics hubs to reduce dependency on Buenos Aires. The provinces of Córdoba and Santa Fe have emerged as critical nodes due to their central geographic position and agro-industrial significance.

In 2023, DHL Supply Chain announced a USD 20 million investment to expand its warehousing footprint in Buenos Aires province, aimed at catering to high-growth sectors such as healthcare and electronics.

%252C%25202019-2024.png&w=640&q=75)

What Factors are Leading to the Growth of Argentina Logistics and Warehousing Market

E-commerce Expansion: The surge in e-commerce activity, growing at a CAGR of 25% (2020–2023), has amplified demand for last-mile delivery and fulfillment centers. More than 10 million active e-shoppers in 2023 fueled the need for faster, reliable logistics, prompting investments in micro-fulfillment centers across metro cities.

Agribusiness and Commodities Trade: Argentina’s agricultural exports—mainly soy, maize, and beef—have generated substantial demand for storage, cold chain logistics, and efficient port infrastructure. Rosario Port handled over 75% of agricultural bulk exports in 2023, pushing the need for upstream logistics efficiency.

Road and Rail Infrastructure Development: Government-led initiatives under PPP models, especially in freight corridors connecting the interior provinces to Buenos Aires port, have improved transit times and reduced transportation costs by 12% in select corridors.

Which Industry Challenges Have Impacted the Growth for Argentina Logistics and Warehousing Market

Macroeconomic Instability: Argentina’s chronic inflation and currency depreciation have significantly increased operational costs for logistics providers. In 2023, inflation surged past 120%, leading to a 30–40% rise in fuel, labor, and maintenance costs. This unpredictability in cost structure hampers long-term planning and deters foreign investment in the sector.

Infrastructure Bottlenecks: Although the government has initiated upgrades, much of Argentina’s road and rail infrastructure remains outdated or poorly maintained. According to the Ministry of Transport, nearly 40% of national roads used for freight were in “poor” or “very poor” condition in 2023, contributing to higher vehicle wear and prolonged delivery timelines.

Fragmented Market Structure: The market is dominated by small and medium-sized players with limited technological adoption and asset scale. Over 70% of logistics companies in Argentina operate with fewer than 10 trucks and minimal warehousing space, leading to inefficiencies and inconsistent service quality.

What are the Regulations and Initiatives which have Governed the Market

National Logistics Plan 2030: Launched by the Ministry of Transport, this plan includes strategic infrastructure investments across freight corridors, logistics nodes, and intermodal terminals. As of 2023, over 120 projects were underway with a combined investment target of USD 2.5 billion aimed at reducing logistics costs by up to 15% by 2029.

Tax Incentives for Warehousing Zones: The Argentine government has introduced regional tax breaks and subsidies to promote the development of logistics parks, particularly in provinces like Córdoba, Tucumán, and Mendoza. In 2023, five new logistics parks received development licenses with support from public-private partnerships.

Import-Export Facilitation Policies: The government has introduced digital customs clearance systems (SIMPES) and simplified documentation processes to reduce cargo clearance times. In 2023, implementation of paperless clearance reduced average customs processing time by 22% at the Port of Rosario.

Argentina Logistics and Warehousing Market Segmentation

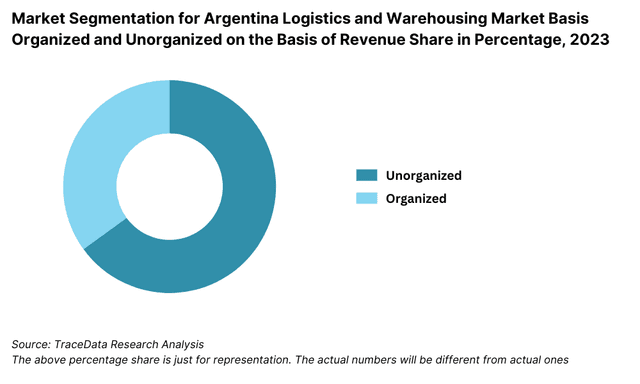

By Market Structure: Unorganized players dominate the market due to their wide regional presence, cost-effective operations, and flexibility in services. These operators typically focus on short-haul freight, small-scale warehousing, and localized logistics needs, catering mainly to SMEs and rural supply chains. Organized players, on the other hand, are steadily growing their presence by offering integrated services, advanced tracking systems, and adherence to compliance standards. Companies like Andreani, DHL, and Ocasa are gaining market share by serving large enterprises, implementing automation, and expanding cold chain and high-tech warehousing capacity.

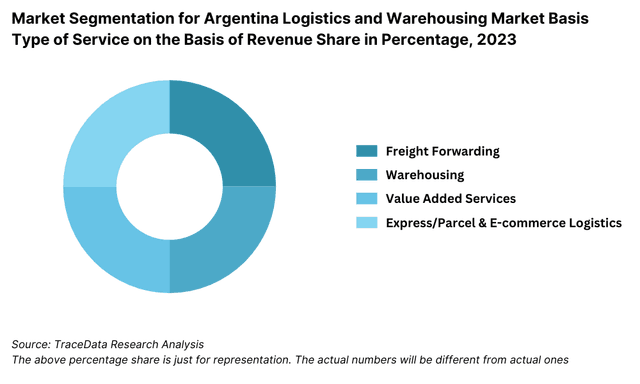

By Service Type: Freight forwarding is the largest contributor to the logistics market in Argentina, owing to the country’s strong agriculture export base, demand from manufacturing, and over-reliance on road transport. Warehousing services are expanding rapidly, particularly in urban hubs such as Buenos Aires, Córdoba, and Rosario, as demand grows for modern inventory storage, e-commerce fulfillment, and cold chain infrastructure. Value-added services such as packing, labelling, customs brokerage, and last-mile delivery are also witnessing traction as clients seek end-to-end solutions from logistics partners.

By End-User Industry: Retail and FMCG players form the largest user base in the logistics and warehousing industry, driven by increasing demand for shelf availability, warehouse consolidation, and reverse logistics solutions. Agriculture and agro-processing sectors follow due to Argentina’s dominant role in global commodity exports, requiring bulk handling and port logistics. Healthcare and pharmaceuticals are fast emerging as high-value clients, pushing the need for temperature-controlled storage and regulatory compliance in distribution processes.

Competitive Landscape in Argentina Logistics and Warehousing Market

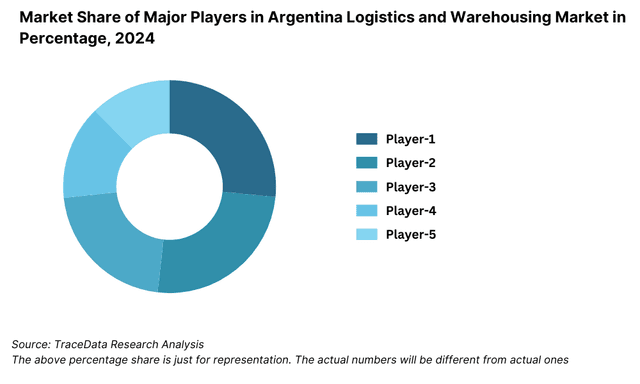

The Argentina logistics and warehousing market is moderately consolidated, with a mix of long-established domestic companies and global third-party logistics (3PL) providers. Leading players include Andreani, Ocasa, OCA Logística, DHL Supply Chain, and Grupo Logístico Andreani. The recent expansion of e-commerce and emphasis on supply chain optimization has led to digital transformation across logistics service providers, introducing more value-added and integrated service offerings.

Company | Establishment Year | Headquarters |

Andreani | 1945 | Buenos Aires, Argentina |

Ocasa | 1983 | Buenos Aires, Argentina |

OCA Logística | 1957 | Buenos Aires, Argentina |

DHL Supply Chain | 1969 (global) | Bonn, Germany / Argentina Office in Buenos Aires |

Grupo Logístico Cruz del Sur | 1959 | Buenos Aires, Argentina |

Some of the recent competitor trends and key information about competitors include:

Andreani: A market leader in logistics and warehousing, Andreani invested over USD 50 million in automation and warehouse expansion in 2023. The company launched a new fulfillment center in Tigre, enhancing last-mile delivery capacity, particularly for e-commerce and healthcare sectors.

Ocasa: Specializing in high-compliance logistics, Ocasa grew its pharma and healthcare client base by 22% in 2023. Its cold chain infrastructure and ISO certifications have positioned it as a preferred partner for regulated industries. The company also expanded operations to serve regional markets including Chile and Uruguay.

OCA Logística: A legacy logistics provider with a strong courier network, OCA handled over 100 million shipments in 2023. The company launched “OCA Express” for B2C deliveries and partnered with retail chains to create in-store pick-up hubs.

DHL Supply Chain: With a focus on contract logistics and supply chain automation, DHL increased its warehousing footprint by 30% in Argentina in 2023. The firm introduced AI-based warehouse management tools to improve inventory visibility and efficiency across sectors including automotive, retail, and electronics.

Grupo Logístico Cruz del Sur: Known for its extensive southern regional network, Cruz del Sur upgraded its fleet in 2023 with GPS-enabled tracking systems and eco-efficient trucks. The company also rolled out a specialized logistics service for Patagonia-based industrial clients.

What Lies Ahead for Argentina Logistics and Warehousing Market?

The Argentina logistics and warehousing market is projected to grow steadily by 2029, demonstrating a healthy CAGR driven by rising domestic consumption, infrastructure development, and digital transformation across the supply chain ecosystem.

Expansion of E-commerce Fulfillment and Last-Mile Logistics: With Argentina’s e-commerce user base expected to exceed 20 million by 2026, demand for urban warehousing and last-mile delivery solutions will intensify. Logistics providers are anticipated to invest in micro-fulfillment centers, route optimization tools, and click-and-collect delivery formats to meet customer expectations for speed and flexibility.

Increased Investments in Cold Chain Infrastructure: The growing demand for temperature-sensitive goods, particularly in pharmaceuticals, perishable food, and biotech, will drive robust expansion of cold storage facilities. Companies will focus on energy-efficient refrigeration systems, real-time temperature monitoring, and compliance with international safety standards to cater to high-growth sectors.

Digitalization and Automation of Warehousing: The integration of warehouse management systems (WMS), automated guided vehicles (AGVs), and AI-powered inventory management tools will become more mainstream among organized logistics players. These technologies are expected to improve storage efficiency, reduce operational errors, and enhance throughput across key logistics hubs.

Regional Development and Intermodal Logistics Hubs: The government’s push under the National Logistics Plan 2030 will continue to foster the development of multi-modal transport corridors and regional logistics parks in provinces such as Córdoba, Salta, and Mendoza. These hubs will reduce transport bottlenecks and promote better connectivity between inland producers and export gateways.

%252C%25202024-2030.png&w=640&q=75)

Argentina Logistics and Warehousing Market Segmentation

• By Market Structure:

o Organized Sector

o Unorganized Sector

o Domestic Logistics Providers

o Global 3PLs

o Government-operated Freight Services

• By Type of Services:

o Freight Forwarding

o Warehousing

o Value-Added Services (VAS)

o Cold Chain Logistics

o Last-Mile Delivery

o Reverse Logistics

• By Mode of Transportation:

o Road Transport

o Rail Transport

o Air Freight

o Sea Freight

o Intermodal Transport

• By End-User Industry:

o Retail and FMCG

o Automotive and Industrial Goods

o Agriculture and Commodities

o Healthcare and Pharmaceuticals

o E-commerce

o Electronics and Technology

o Oil & Gas and Chemicals

• By Ownership of Assets:

o Asset-Light 3PL Providers

o Asset-Heavy Logistics Firms

• By Region:

o Buenos Aires Province

o Córdoba

o Santa Fe

o Mendoza

o Patagonia

o Northwestern Argentina

o Northeastern Argentina

Players Mentioned in the Report:

• Andreani

• Ocasa

• OCA Logística

• DHL Supply Chain

• Grupo Logístico Cruz del Sur

• Loginter

• Blue Express

• Kuehne + Nagel Argentina

Key Target Audience:

• Logistics and Warehousing Companies

• E-commerce Retailers

• Manufacturing and Export Firms

• Agricultural Exporters

• Cold Chain and Pharma Distributors

• Government Transport and Infrastructure Departments

• Third-Party Logistics Providers

• Technology and Automation Vendors

• Industry Associations and Trade Bodies

Time Period:

• Historical Period: 2018–2023

• Base Year: 2024

• Forecast Period: 2024–2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-“ Role of Entities, Stakeholders, and Challenges They Face

4.2. Revenue Streams for Argentina Logistics and Warehousing Market

4.3. Business Model Canvas for Argentina Logistics and Warehousing Market

4.4. Service Decision-Making Process

4.5. Logistics Partner Selection Criteria

5.1. Logistics Spend as a % of GDP in Argentina, 2018-“2024

5.2. Organized vs Unorganized Logistics Share, 2018-“2024

5.3. Number of Warehousing and Logistics Firms by Province

5.4. Cargo Volume Handled by Mode of Transport, 2018-“2024

8.1. Revenue, 2018-“2024

8.2. Freight Volume and Warehousing Capacity, 2018-“2024

9.1. By Market Structure (Organized and Unorganized), 2023-“2024P

9.2. By Type of Service (Freight Forwarding, Warehousing, VAS), 2023-“2024P

9.3. By Mode of Transport (Road, Rail, Air, Sea), 2023-“2024P

9.4. By End-User Industry (Retail, FMCG, Pharma, Agriculture, etc.), 2023-“2024P

9.5. By Region (Buenos Aires, Córdoba, Santa Fe, etc.), 2023-“2024P

10.1. Customer Landscape and Industry Use Cases

10.2. Logistics Partner Selection and Outsourcing Preferences

10.3. Pricing Expectations and Contract Structures

10.4. Need, Desire, and Pain Point Analysis

10.5. Gap Analysis Framework

11.1. Trends and Developments for Argentina Logistics and Warehousing Market

11.2. Growth Drivers for Argentina Logistics and Warehousing Market

11.3. SWOT Analysis

11.4. Issues and Challenges

11.5. Government Regulations and Infrastructure Initiatives

12.1. Market Size and Growth Potential, 2018-“2029

12.2. Business Models and Fulfillment Strategies

12.3. Cross-Comparison of E-commerce Logistics Providers

13.1. Temperature-Controlled Warehousing and Fleet Capacity

13.2. Cold Chain Demand from Pharma, Dairy, Meat, and Seafood

13.3. Key Cold Chain Players and Business Models

16.1. Benchmark of Key Competitors Including Overview, USP, Strategy, Network, Clients, Revenue, and Warehousing Capacity

16.2. Strength and Weakness

16.3. Operating Model Analysis Framework

16.4. Gartner Magic Quadrant (Adapted)

16.5. Bowmans Strategic Clock for Competitive Advantage

17.1. Revenue, 2025-“2029

17.2. Freight and Warehouse Volume, 2025-“2029

18.1. By Market Structure (Organized and Unorganized), 2025-“2029

18.2. By Type of Service, 2025-“2029

18.3. By Mode of Transport, 2025-“2029

18.4. By Region, 2025-“2029

18.5. By End-User Industry, 2025-“2029

18.6. By Ownership Model (Asset-Light vs Asset-Heavy), 2025-“2029

18.7. Recommendation

18.8. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand side and supply side entities for Argentina Logistics and Warehousing Market. Basis this ecosystem, we will shortlist leading 5–6 logistics service providers in the country based upon their financial information, warehousing capacity, freight volume, and client portfolio.

Sourcing is made through industry articles, multiple secondary, and proprietary databases to perform desk research around the market to collate industry-level information.

Step 2: Desk Research

Subsequently, we engage in an exhaustive desk research process by referencing diverse secondary and proprietary databases. This approach enables us to conduct a thorough analysis of the market, aggregating industry-level insights. We delve into aspects like total logistics revenue, warehousing capacity, number of players, freight volumes, mode-wise transport share, regional penetration, and service offerings.

We supplement this with detailed examinations of company-level data, relying on sources like press releases, annual reports, financial statements, investor presentations, and public tenders. This process aims to construct a foundational understanding of both the market and the entities operating within it.

Step 3: Primary Research

We initiate a series of in-depth interviews with C-level executives, logistics heads, warehouse managers, and other stakeholders representing various Argentina Logistics and Warehousing companies, 3PL players, clients from retail, e-commerce, pharma, and agriculture. This interview process serves a multi-faceted purpose: to validate market hypotheses, authenticate statistical data, and extract valuable operational and financial insights from these industry representatives. Bottom to top approach is undertaken to evaluate service volume and revenue for each player, thereby aggregating to the overall market.

As part of our validation strategy, our team executes disguised interviews wherein we approach each company under the guise of potential clients or service users. This enables us to validate the operational information shared by company executives and corroborate data against secondary databases. These interactions also provide us with a comprehensive understanding of service pricing, value chain dynamics, client contracts, and capacity utilization.

Step 4: Sanity Check

- Bottom to top and top to bottom analysis along with market size modeling exercises is undertaken to assess sanity check process. Multiple triangulation techniques are used across sources to ensure the accuracy and consistency of findings.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Argentina logistics and warehousing market holds strong potential, reaching a valuation of ARS 4.28 trillion in 2023. This growth is supported by increased domestic consumption, rising e-commerce penetration, and ongoing infrastructure development under the National Logistics Plan 2030. With growing investments in cold chain, automation, and regional logistics hubs, the market is poised for robust expansion through 2029.

The Argentina Logistics and Warehousing Market is led by key players such as Andreani, Ocasa, OCA Logística, DHL Supply Chain, and Grupo Logístico Cruz del Sur. These companies dominate due to their extensive logistics networks, diversified service offerings, investment in automation, and strong client bases across retail, pharma, and agriculture sectors.

Major growth drivers include the rapid expansion of e-commerce, which is driving demand for last-mile delivery and fulfillment services; increased focus on cold chain infrastructure for pharma and perishables; and public-private investments in multimodal logistics and digitalization. Rising export activity in agriculture and industry is also fueling demand for efficient freight and warehousing solutions.

The market faces challenges such as macroeconomic instability, high inflation impacting operational costs, and outdated road and rail infrastructure. Other issues include market fragmentation with many small-scale operators lacking digital capabilities, port congestion, and a shortage of skilled logistics labor. These barriers can restrict efficiency and service quality, especially outside major urban centers.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0