Australia Organic Farming Market Outlook to 2029

By Market Structure, By Crop Type, By Farming Practices, By Distribution Channels, By Consumer Demographics, and By Region

Report Overview

Report Code

TDR0118

Coverage

Asia

Published

February 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Australia Organic Farming Market Outlook to 2029 - By Market Structure, By Crop Type, By Farming Practices, By Distribution Channels, By Consumer Demographics, and By Region.” provides a comprehensive analysis of the organic farming market in Australia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the Organic Farming Market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Australia Organic Farming Market Outlook to 2029 - By Market Structure, By Crop Type, By Farming Practices, By Distribution Channels, By Consumer Demographics, and By Region.” provides a comprehensive analysis of the organic farming market in Australia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the Organic Farming Market. The report concludes with future market projections based on sales revenue, by market, crop types, region, cause and effect relationship, and success case studies highlighting the major opportunities and cautions.

Australia Organic Farming Market Overview and Size

The Australia organic farming market reached a valuation of AUD 2.5 billion in 2023, driven by rising consumer awareness regarding health and sustainability, government support for organic certification, and growing export opportunities. The market is characterized by major players such as Australian Organic, Bellamy’s Organic, BioGro Australia, and Organic Farmers Australia. These companies are recognized for their adherence to strict organic standards, wide distribution networks, and diverse crop offerings.

In 2023, Australian Organic launched new initiatives to certify small-scale farmers, aiming to increase the share of organic-certified farms across the country. New South Wales and Victoria are key markets due to their favorable climatic conditions, established supply chains, and high consumer demand for organic products.

Market Size for Australia Organic Farming Industry on the Basis of Revenues, 2018-2024

What Factors are Leading to the Growth of Australia Organic Farming Market:

Health and Environmental Awareness: The increasing demand for chemical-free and environmentally sustainable produce has fueled the organic farming market. In 2023, nearly 70% of Australian households reported purchasing organic products at least once a month, indicating a significant shift toward healthier consumption patterns.

Government Support: Federal and state-level incentives for organic certification and sustainable farming practices have encouraged farmers to adopt organic methods. In 2023, the government allocated AUD 150 million to support organic research and infrastructure development, further boosting market growth.

Export Demand: Australia’s reputation for producing high-quality organic goods has made it a preferred supplier for international markets, particularly in Asia and Europe. Organic product exports grew by 20% in 2023, with top categories including grains, dairy, and fresh produce.

Which Industry Challenges Have Impacted the Growth for Australia Organic Farming Market

High Costs of Transition to Organic Farming: The shift from conventional to organic farming requires significant investment in terms of certification, infrastructure, and adapting to new farming practices. In 2023, around 40% of farmers cited high initial costs as a major barrier to adopting organic methods. These expenses often deter small-scale farmers, limiting the market's overall growth.

Climate-Related Challenges: Unpredictable weather patterns, such as droughts and floods, have disrupted organic farming operations, particularly in regions like Queensland and New South Wales. In 2023, approximately 25% of organic farmers reported losses due to extreme weather events, highlighting the vulnerability of the industry to climate change.

Limited Consumer Awareness in Rural Areas: While urban consumers increasingly demand organic products, rural areas lag in awareness and willingness to pay premium prices. According to a recent survey, only 30% of rural households expressed interest in purchasing organic products, compared to 65% in urban regions. This disparity affects market penetration and revenue potential.

What are the Regulations and Initiatives which have Governed the Market:

National Organic Certification Standards: The Australian government mandates strict certification processes for organic farming to ensure product authenticity and quality. Certification bodies such as Australian Organic follow stringent guidelines, including the prohibition of synthetic chemicals and genetically modified organisms (GMOs). In 2023, nearly 85% of organic farmers in Australia complied with these standards, boosting consumer trust in organic products.

Subsidies and Grants for Organic Farmers: Government initiatives such as the "The reports cover Australia Organic Farming Market Segmentation, Report, Opportunities, Statistics, Challenges, and Market Forecast Trends shaping the Market through 2029." offer financial support to farmers transitioning to organic methods. In 2023, the program allocated AUD 100 million in grants, benefiting over 1,500 farmers and encouraging wider adoption of organic farming.

Export Facilitation Policies: The Australian government actively promotes organic exports through trade agreements and reduced tariffs. In 2023, the organic export sector saw a 15% growth, supported by government-backed promotional campaigns in key markets like China, Japan, and the European Union.

Australia Organic Farming Market Segmentation

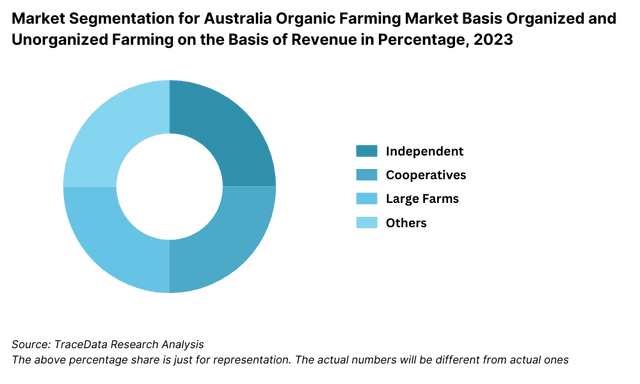

By Market Structure: Independent organic farmers dominate the market due to their localized approach, strong ties to community-supported agriculture (CSA) programs, and ability to cater to niche consumer preferences. They often provide direct-to-consumer services, including farmers' markets and subscription-based organic produce deliveries. Certified organic cooperatives and larger farming groups hold a significant share because they ensure consistent supply, higher production volumes, and adherence to certification standards, which appeals to major retailers and export markets.

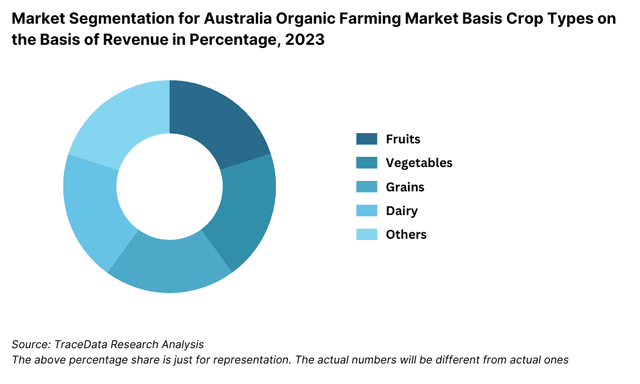

By Crop Type: Organic fruits and vegetables are the leading segments, driven by high consumer demand for fresh, chemical-free produce. They are followed by organic grains and cereals, which are essential for both direct consumption and as inputs for organic food manufacturing. The growing popularity of organic dairy and meat products also contributes significantly, especially in export markets where such products command a premium.

By Farming Practices: Mixed organic farming, which combines crops and livestock, holds the largest share due to its efficiency in resource utilization and soil health management. This is followed by pure organic cropping systems that focus on high-value crops such as fruits and specialty herbs. Agroforestry-based organic farming is an emerging trend, blending tree cultivation with organic farming to enhance biodiversity and provide additional income sources for farmers.

Competitive Landscape in Australia Organic Farming Market

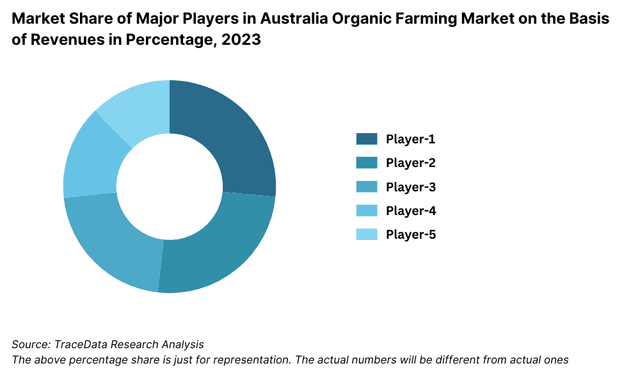

The Australia organic farming market is moderately fragmented, with a mix of independent farmers, cooperatives, and larger corporate players dominating the space. Additionally, the emergence of specialized organic product brands and online marketplaces has diversified the market, offering consumers more choices and streamlined distribution.

Company Name | Establishment Year | Headquarters |

|---|---|---|

Bellamy's Organic | 2004 | Launceston, Tasmania |

Barambah Organics | 2002 | Brisbane, Queensland |

Manna Farms | 1980s | Colignan, Victoria |

Cleaver's Organic | 2006 | Sydney, New South Wales |

Australian Organic Food Co. | 2014 | Braeside, Victoria |

Organic Farming Systems | 2002 | Perth, Western Australia |

Junee Licorice and Chocolate | 1998 | Junee, New South Wales |

Meredith Dairy | 1991 | Meredith, Victoria |

Kinross Station Lamb | 2010s | Cootamundra, New South Wales |

Mungalli Creek Dairy | 2000 | Millaa Millaa, Queensland |

Some of the recent competitor trends and key information about competitors include:

Australian Organic: As the leading certifier of organic products in Australia, Australian Organic recorded a 30% increase in organic certifications in 2023, reflecting the growing interest in sustainable farming practices. The organization’s focus on promoting certified organic standards has solidified its position as a key player in the industry.

Bellamy’s Organic: A major producer of organic baby food, Bellamy’s reported a 25% growth in revenue in 2023, driven by strong domestic demand and expanding export markets in Asia. The company's emphasis on product innovation and premium-quality ingredients has bolstered consumer trust and brand loyalty.

BioGro Australia: Known for its expertise in organic fertilizers and soil enhancers, BioGro experienced a 20% rise in product sales in 2023. The company’s collaborations with organic farming cooperatives have significantly contributed to its growth by improving productivity and sustainability for farmers.

Organic Farmers Australia: Specializing in fresh organic produce, Organic Farmers Australia reported a 15% increase in domestic sales in 2023. Their focus on direct-to-consumer models, including farmers’ markets and subscription boxes, has enhanced consumer accessibility and trust in organic products.

Eco-Farms Organic Wholesalers: As one of Australia’s largest organic wholesalers, Eco-Farms saw a 12% increase in sales in 2023, primarily driven by expanding distribution networks in urban and regional areas. The company’s partnerships with major retail chains and online platforms have played a crucial role in increasing the availability of organic products nationwide.

What Lies Ahead for Australia Organic Farming Market?

The Australia organic farming market is projected to grow significantly by 2029, exhibiting a strong CAGR during the forecast period. This growth is expected to be driven by rising consumer awareness about health and sustainability, government support, and increasing export opportunities for organic products.

Expansion of Export Markets: As global demand for organic products continues to rise, Australia is well-positioned to capitalize on its reputation for high-quality organic goods. Key export destinations such as China, Japan, and the EU are expected to drive growth, with organic grains, dairy, and meat products leading the charge.

Adoption of Advanced Farming Technologies: The integration of precision agriculture, biofertilizers, and advanced irrigation systems in organic farming is anticipated to enhance productivity and reduce costs. These technological advancements will make organic farming more accessible, particularly for small and medium-scale farmers, driving growth across the sector.

Growth in Direct-to-Consumer Channels: The rising popularity of farmers’ markets, organic subscription boxes, and online platforms is expected to strengthen direct-to-consumer sales. These channels not only provide farmers with better margins but also enhance consumer trust and loyalty by creating a closer connection between producers and buyers.

Increased Focus on Climate-Resilient Farming Practices: With climate change posing challenges such as droughts and extreme weather, farmers are expected to adopt more resilient farming practices. These include agroforestry, crop diversification, and sustainable water management, which will ensure the long-term viability of organic farming in Australia.

Future Outlook and Projections for Australia Organic Farming Market on the Basis of Revenues in USD Billion, 2024-2029

Australia Organic Farming Market Segmentation

- By Market Structure:

- Independent Organic Farmers

- Organic Farming Cooperatives

- Large-Scale Corporate Organic Farms

- Contract Farming Operations

- Community-Supported Agriculture (CSA) Programs

- By Crop Type:

- Fruits and Vegetables

- Grains and Cereals

- Dairy and Livestock

- Specialty Herbs and Spices

- Organic Processed Foods

- By Farming Practices:

- Mixed Organic Farming

- Pure Organic Cropping Systems

- Agroforestry-Based Organic Farming

- Permaculture

- By Distribution Channels:

- Supermarkets and Hypermarkets

- Online Marketplaces

- Farmers’ Markets

- Subscription-Based Delivery Services

- Specialty Organic Retailers

- By Consumer Demographics:

- Health-Conscious Consumers

- Environmentally Conscious Consumers

- Households with Children

- High-Income Households

- By Region:

- New South Wales

- Victoria

- Queensland

- South Australia

- Western Australia

- By Farming Type:

- Integrated Organic Farming

- Pure Organic Farming

Players Mentioned in the Report:

- Bellamy's Organic

- Barambah Organics

- Manna Farms

- Cleaver's Organic

- Australian Organic Food Co.

- Organic Farming Systems

- Junee Licorice and Chocolate

- Meredith Dairy

- Kinross Station Lamb

- Mungalli Creek Dairy

Key Target Audience:

- Organic Farmers and Cooperatives

- Organic Product Distributors and Retailers

- Certification Bodies and Regulatory Authorities

- Agricultural Technology Providers

- Research and Development Institutions

Time Period:

- Historical Period: 2018-2023

- Base Year: 2024

- Forecast Period: 2024-2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-Role of Entities, Stakeholders, and Challenges They Face

4.2. Revenue Streams for Australia Organic Farming Market

4.3. Business Model Canvas for Australia Organic Farming Market

4.4. Organic Produce Buying Decision Process

4.5. Organic Farming Supply Decision Process

5.1. Organic Farming Land Area in Australia, 2018-2024

5.2. Growth in Organic vs. Conventional Farming, 2018-2024

5.3. Organic Food Retail Spend in Australia, 2024

5.4. Number of Organic Farms by Region in Australia, 2023

8.1. Revenue, 2018-2024

8.2. Production Volume, 2018-2024

8.3. Export Volume for Organic Farming, 2018-2024

9.1. By Market Structure (Independent, Cooperatives, Large Farms), 2023-2024P

9.2. By Crop Type (Fruits, Vegetables, Grains, Dairy, and Others), 2023-2024P

9.3. By Farming Practices (Mixed, Pure Cropping, Agroforestry and others), 2023-2024P

9.4. By Distribution Channels (Supermarkets, Farmers Markets, Online Platforms), 2023-2024P

9.5. By Region (NSW, Victoria, Queensland, WA, SA), 2023-2024P

9.6. By Farming Type (Integrated Organic Farming and Pure Organic Farming), 2023-2024P

10.1. Consumer Landscape and Cohort Analysis

10.2. Customer Journey and Buying Decision Process

10.3. Need, Desire, and Pain Point Analysis

10.4. Gap Analysis Framework

11.1. Trends and Developments for Australia Organic Farming Market

11.2. Growth Drivers for Australia Organic Farming Market

11.3. SWOT Analysis for Australia Organic Farming Market

11.4. Issues and Challenges for Australia Organic Farming Market

11.5. Government Regulations for Australia Organic Farming Market

16.1. Market Share of Major Players in Australia Organic Farming Market Basis Revenues, 2023

16.1. Benchmark of Key Competitors in Australia Organic Farming Market Basis Operational and Financial Variables

16.2. Strengths and Weaknesses

16.3. Operating Model Analysis Framework

16.4. Gartner Magic Quadrant

16.5. Bowmans Strategic Clock for Competitive Advantage

17.1. Revenue, 2025-2029

17.2. Production Volume, 2025-2029

18.1. By Market Structure (Independent, Cooperatives, Large Farms), 2025-2029

18.2. By Crop Type (Fruits, Vegetables, Grains, Dairy, and Others), 2025-2029

18.3. By Farming Practices (Mixed, Pure Cropping, Agroforestry), 2025-2029

18.4. By Distribution Channels (Supermarkets, Farmers Markets, Online Platforms), 2025-2029

18.5. By Region (NSW, Victoria, Queensland, WA, SA), 2025-2029

18.6. By Farming Type (Integrated Organic Farming and Pure Organic Farming), 2025-2029

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities for the Australia Organic Farming Market. Based on this ecosystem, we will shortlist leading 5-6 players in the country using criteria such as financial performance, production capacity, and market presence.

Source data through industry articles, government reports, and multiple secondary and proprietary databases to perform desk research around the market and gather macro- and micro-level insights.

Step 2: Desk Research

Engage in an exhaustive desk research process, leveraging secondary and proprietary databases to conduct a thorough market analysis. This step involves studying sales revenue, production volumes, market trends, and industry dynamics.

Supplement this research with detailed company-level data from annual reports, press releases, financial statements, and other publicly available documents. This process forms the foundation for understanding the market and its key players.

Step 3: Primary Research

Conduct in-depth interviews with C-level executives, organic farmers, cooperative representatives, and other stakeholders in the Australia Organic Farming Market. These interviews aim to validate market hypotheses, verify statistical data, and extract actionable insights regarding operations, financials, and industry trends.

Adopt a bottom-up approach to assess production volumes for each player, aggregating this data to estimate the overall market size. Disguised interviews are also conducted to cross-verify operational and financial data obtained during desk research.

Gather comprehensive insights into revenue streams, pricing strategies, distribution channels, and other critical market aspects.

Step 4: Sanity Check

- Undertake top-down and bottom-up market size modeling exercises to validate findings and ensure consistency. Perform a thorough sanity check to ensure the accuracy and reliability of the data and insights compiled.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Australia Organic Farming Market is poised for substantial growth, projected to reach a valuation of AUD 4.5 billion by 2029. This growth is driven by increasing consumer demand for sustainable and chemical-free produce, government incentives for organic farming, and the expansion of export opportunities for high-value organic products.

Key players include Australian Organic, Bellamy’s Organic, BioGro Australia, and Organic Farmers Australia. These companies dominate the market due to their strong focus on quality certification, extensive distribution networks, and innovative farming practices. Other notable players include Eco-Farms Organic Wholesalers and several cooperatives supporting small-scale organic farmers.

Primary growth drivers include rising consumer awareness about health and sustainability, government support for certification programs, and technological advancements in organic farming. Additionally, the increasing popularity of organic exports, particularly in Asia and Europe, significantly contributes to market expansion.

The market faces challenges such as high transition costs for farmers shifting to organic methods, climate-related risks like droughts and floods, and limited consumer awareness in rural areas. Supply chain inefficiencies, including inadequate cold storage and transportation infrastructure, also present significant barriers to market growth.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0