Bahrain Logistics and Warehousing Market Outlook to 2029

By Mode of Transport, By End Users (Retail, E-commerce, FMCG, Healthcare, Automotive), By Service Mix (Freight Forwarding, Warehousing, and Value-Added Services), and By Region

Report Overview

Report Code

TDR0253

Coverage

Middle East

Published

September 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Bahrain Logistics and Warehousing Market Outlook to 2029 – By Mode of Transport, By End Users (Retail, E-commerce, FMCG, Healthcare, Automotive), By Service Mix (Freight Forwarding, Warehousing, and Value-Added Services), and By Region” provides a comprehensive analysis of the logistics and warehousing industry in Bahrain. The report covers an overview and genesis of the industry, market size in terms of revenue, segmentation across service lines and user verticals; key trends and developments, regulatory landscape, demand drivers, challenges, and competitive landscape including major logistics players, growth opportunities and bottlenecks.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Bahrain Logistics and Warehousing Market Outlook to 2029 – By Mode of Transport, By End Users (Retail, E-commerce, FMCG, Healthcare, Automotive), By Service Mix (Freight Forwarding, Warehousing, and Value-Added Services), and By Region” provides a comprehensive analysis of the logistics and warehousing industry in Bahrain. The report covers an overview and genesis of the industry, market size in terms of revenue, segmentation across service lines and user verticals; key trends and developments, regulatory landscape, demand drivers, challenges, and competitive landscape including major logistics players, growth opportunities and bottlenecks. The report concludes with future market projections based on service lines, industry verticals, and regions, including success case studies highlighting opportunities and strategic insights.

Bahrain Logistics and Warehousing Market Overview and Size

The Bahrain logistics and warehousing market reached a valuation of BHD 1.007 billion in 2023, driven by the country’s strategic location as a GCC gateway, strong government support through infrastructure projects, and growing trade volumes. Bahrain's logistics sector benefits from its close proximity to Saudi Arabia, world-class ports such as Khalifa Bin Salman Port, and the Bahrain International Airport. The market is marked by the presence of local and international players like Agility, DHL, GAC Bahrain, Almoayed Wilhelmsen, and APM Terminals.

In 2023, the government’s focus on economic diversification under Bahrain Vision 2030 led to continued investments in the logistics sector including upgrades in Bahrain Logistics Zone (BLZ) and the new causeway project linking Bahrain with Saudi Arabia. Manama, Hidd, and Al Muharraq remain key logistics hubs due to port connectivity, customs efficiency, and industrial clustering.

%252C%25202019-2024.png&w=640&q=75)

What Factors are Leading to the Growth of Bahrain Logistics and Warehousing Market:

Strategic Location and Trade Access: Bahrain’s geographical positioning between major regional markets such as KSA, UAE, and Qatar enables it to function as a cost-effective regional distribution center. In 2023, over 65% of logistics throughput was related to re-export activity, affirming its role in intra-GCC trade facilitation.

Infrastructure Development: Ongoing development of the Bahrain International Investment Park, logistics zones, and improved port facilities has led to higher logistics throughput. The expansion of Khalifa Bin Salman Port increased container handling capacity by 20% in 2023.

Rise in E-commerce: The growth of online shopping and retail platforms has fueled demand for last-mile delivery, cold storage, and fulfillment centers. In 2023, the e-commerce sector contributed to 15% of warehousing demand, primarily driven by consumer electronics and fashion.

Which Industry Challenges Have Impacted the Growth of Bahrain Logistics and Warehousing Market

Limited Domestic Market Size: Bahrain’s relatively small population and industrial base restrict the scale of domestic logistics demand. In 2023, over 55% of logistics volume was related to transshipment or regional distribution rather than internal consumption.

High Operating Costs: Rising fuel prices and warehouse rental costs in urban regions such as Manama have impacted margins. Average warehouse rents increased by 11% in 2023, leading to cost pressures especially for small and mid-size logistics firms.

Talent Shortage in Supply Chain Management: There is a notable shortage of skilled logistics professionals in Bahrain, particularly in digital supply chain, cold chain, and last-mile logistics. A recent survey noted that 42% of logistics companies face difficulty in hiring trained staff.

What are the Regulations and Initiatives which have Governed the Market

Customs Reforms and E-Clearance: Bahrain Customs Affairs has introduced Electronic Data Interchange (EDI) and pre-arrival processing to reduce clearance times. In 2023, 65% of shipments were processed digitally, reducing average customs clearance by 22%.

National Logistics Strategy: Bahrain launched its National Logistics Strategy in 2021, aiming to triple the sector’s contribution to GDP by 2030. The strategy prioritizes investments in air cargo facilities, cold chains, and bonded logistics parks.

Warehouse Standardization Regulations: The government has implemented compliance protocols for fire safety, digital inventory systems, and hygiene standards in logistics parks. In 2023, 87% of Grade A warehouses were certified under new regulatory norms.

Bahrain Logistics and Warehousing Market Segmentation

By Market Structure: Third-Party Logistics (3PL) Providers dominate Bahrain’s logistics landscape. These firms, including DHL, GAC Bahrain, and Agility, benefit from global networks, advanced infrastructure, and service integration. They offer comprehensive solutions including freight forwarding, customs clearance, warehousing, and distribution. Local Logistics Firms and SMEs also hold a substantial market share, especially in last-mile delivery and niche warehousing services. Their flexibility, lower cost base, and knowledge of local regulations allow them to serve smaller businesses efficiently.

%252C%25202023.png&w=640&q=75)

By Type of Service: Freight Forwarding is the largest service segment, driven by Bahrain’s strategic seaport (Khalifa Bin Salman Port) and its role as a re-export hub in the GCC. It includes sea, air, and land transport coordination. Warehousing services are growing rapidly due to increased demand from FMCG, e-commerce, and pharmaceutical sectors. Modern storage solutions including temperature-controlled and bonded warehouses are gaining traction. E-Commerce Logistics is an emerging segment with significant growth, spurred by rising online shopping, demand for faster delivery, and entry of regional e-retailers. Express Logistics is growing due to increasing B2C deliveries and international courier services. Companies like Aramex, FedEx, and UPS are key players in this segment.

%252C%25202023.png&w=640&q=75)

By Mode of Transport: Road Transport dominates, enabled by Bahrain’s integrated road network and its causeway connection to Saudi Arabia. Most domestic and regional cargo movements occur via road. Sea Freight is crucial for imports, exports, and re-exports, with the Khalifa Bin Salman Port serving as a key maritime logistics hub. Air Freight handles time-sensitive and high-value shipments. Bahrain International Airport offers dedicated cargo services and is expanding its cargo terminal capacity.

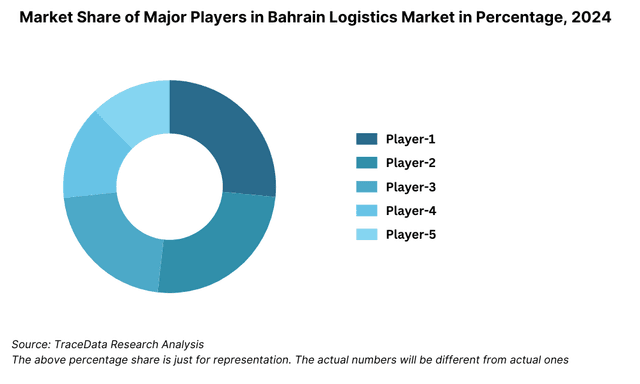

Competitive Landscape in Bahrain Logistics and Warehousing Market

The Bahrain logistics and warehousing market is moderately concentrated, with a combination of global logistics providers and strong regional players operating across segments. While established multinational firms dominate freight forwarding and express logistics, local companies are carving a niche in warehousing, last-mile delivery, and specialized logistics services. Digitalization, customer-centric solutions, and infrastructure investments are key themes driving competitive strategies.

Company | Establishment Year | Headquarters |

DHL Bahrain | 1979 | Manama, Bahrain |

Agility Logistics | 1979 | Kuwait (Regional Ops: Bahrain) |

GAC Bahrain | 1956 | Manama, Bahrain |

Aramex | 1982 | UAE (Bahrain Branch) |

Almoayyed Logistics | 1982 | Manama, Bahrain |

FedEx Express | 1971 | USA (Bahrain Operations) |

Some of the recent competitor trends and key information about competitors include:

DHL Bahrain: As one of the earliest international players in Bahrain, DHL continues to lead the express and cross-border logistics segment. In 2023, the company expanded its fleet and digital parcel tracking capabilities, handling over 4 million shipments, reflecting a 12% year-on-year increase in volume.

Agility Logistics: Leveraging its regional strength, Agility Bahrain focuses on integrated freight, warehousing, and contract logistics. In 2023, it opened a new 28,000 sqm logistics park near Hidd Industrial Area to cater to FMCG and industrial goods.

GAC Bahrain: Known for its strong presence in maritime and contract logistics, GAC expanded its port-side warehousing capacity in 2023 by 15%, supporting the increase in sea freight and oil & gas equipment movement.

Aramex: Specializing in e-commerce delivery and B2C logistics, Aramex Bahrain recorded a 20% rise in last-mile deliveries in 2023, driven by rising online shopping. The company launched same-day delivery services in key urban zones.

Almoayyed Logistics: A trusted local provider offering freight, warehousing, and cold chain services. In 2023, Almoayyed Logistics was selected by a leading pharma distributor to manage its temperature-sensitive supply chain, strengthening its foothold in healthcare logistics.

FedEx Express: With strong capabilities in air cargo and express delivery, FedEx reported a 10% growth in international shipments in 2023. The company also introduced AI-based route optimization in Bahrain to enhance delivery speed and reduce fuel costs.

What Lies Ahead for Bahrain Logistics and Warehousing Market?

The Bahrain logistics and warehousing market is expected to witness steady growth through 2029, supported by infrastructure development, regional trade integration, and expansion of non-oil sectors. The market is projected to grow at a CAGR of approximately 6.8% during the forecast period, with increasing demand for digital logistics, smart warehousing, and specialized services across various industries.

Integration with Saudi Arabia and GCC Trade Corridors: Bahrain’s logistics sector will continue to benefit from its strategic proximity to Saudi Arabia and its role in regional re-exports. Enhanced connectivity via the King Fahd Causeway and future projects like the GCC Railway will strengthen Bahrain’s position as a regional transit and logistics hub.

Digital Transformation and Smart Logistics: Adoption of digital platforms for real-time tracking, inventory management, and AI-driven route optimization will accelerate. Companies are expected to invest in Warehouse Management Systems (WMS), IoT sensors, and automated handling to enhance efficiency and reduce turnaround times.

Expansion in E-Commerce and Last-Mile Delivery: With online shopping on the rise, demand for efficient last-mile delivery solutions will grow. Logistics providers are likely to collaborate with e-commerce platforms to offer faster, more flexible delivery services in urban and remote areas.

Development of Cold Chain and Pharma Logistics: As Bahrain positions itself as a regional center for pharmaceutical re-exports and healthcare logistics, there will be increased investments in cold chain warehousing and temperature-controlled transportation. This is especially relevant for vaccine distribution and high-value medical shipments.

%252C%25202024-2030.png&w=640&q=75)

Bahrain Logistics and Warehousing Market Segmentation

• By Market Structure:

Global 3PL Providers

Local Logistics and Transportation Companies

Contract Logistics Operators

Integrated Freight & Warehousing Firms

Government and Semi-Government Logistics Bodies

Courier and Express Delivery Services

Independent Cold Chain Logistics Firms

• By Type of Service:

Freight Forwarding

Warehousing and Storage

E-Commerce Logistics

Express and Courier Services

Cold Chain Logistics

Value-Added Logistics (Labelling, Packaging, Kitting)

• By Mode of Transport:

Road Transport

Sea Freight

Air Freight

Multimodal Logistics

• By End-User Industry:

Oil & Gas

FMCG

Automotive

Pharmaceuticals & Healthcare

Retail & E-Commerce

Construction & Industrial Goods

Food and Beverage

• By Region:

Manama

Hidd

Muharraq

Southern Governorate

Northern Governorate

Central Region (incl. Sitra, Isa Town)

Players Mentioned in the Report:

DHL Bahrain

Agility Logistics

GAC Bahrain

Aramex

Almoayyed Logistics

FedEx Express

APM Terminals Bahrain

Al Jazeera Shipping

FreightLink Logistics

Key Target Audience:

Logistics Service Providers (3PL, FTL, LTL, Express)

Warehousing Operators and Infrastructure Developers

Freight Forwarding Companies

E-Commerce and Retail Brands

Industrial and Manufacturing Companies

Government Trade and Customs Authorities

Investors and PE Firms in Logistics Infrastructure

Market Research and Policy Advisory Firms

Time Period:

Historical Period: 2018–2023

Base Year: 2024

Forecast Period: 2024–2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-“ Role of Entities, Stakeholders, and Challenges they Face

4.2. Revenue Streams for Bahrain Logistics and Warehousing Market

4.3. Business Model Canvas for Bahrain Logistics Sector

4.4. Logistics Decision Making Process by End Users

4.5. Supply Chain Partner Selection Process

5.1. Trade Volume Handled via Logistics in Bahrain, 2018-“2024

5.2. Logistics Spend as % of GDP in Bahrain, 2018-“2024

5.3. Imports and Exports Volume via Sea, Air, and Road in Bahrain, 2024

5.4. Number of Logistics and Warehousing Companies in Bahrain by Region

8.1. Revenues, 2018-“2024

8.2. Volume Handled, 2018-“2024

9.1. By Market Structure (Organized and Unorganized), 2023-“2024P

9.2. By Type of Logistics Service (Freight Forwarding, Warehousing, Express, Cold Chain), 2023-“2024P

9.3. By Mode of Transport (Road, Sea, Air), 2023-“2024P

9.4. By Region (Manama, Hidd, Muharraq, Southern, Northern), 2023-“2024P

9.5. By End-User Industry (Oil & Gas, FMCG, Retail, Automotive, Pharmaceuticals, Industrial), 2023-“2024P

9.6. By Warehouse Type (Dry Storage, Cold Storage, Bonded, Open Yard), 2023-“2024P

10.1. Customer Landscape and Industry Preferences

10.2. Logistics Partner Selection Criteria

10.3. Customer Expectations, Needs, and Challenges

10.4. Gap Analysis and Service Expectations

11.1. Trends and Developments in Bahrain Logistics Market

11.2. Growth Drivers for Bahrain Logistics and Warehousing Market

11.3. SWOT Analysis for Bahrain Logistics Market

11.4. Issues and Challenges for Bahrain Logistics Sector

11.5. Government Regulations and Initiatives

12.1. Market Size and Future Potential for B2C and B2B Logistics, 2018-“2029

12.2. Business Model and Revenue Streams

12.3. Cross Comparison of Leading Logistics Players by Services, Network, Fleet Size, Automation, Technology Integration

13.1. Logistics Credit Access, Working Capital Needs and LTV, 2018-“2029

13.2. Bank vs NBFC Penetration for Fleet and Infrastructure Financing

13.3. Lease vs Owned Warehouse Trends

13.4. Logistics Investment and PE Activity in Bahrain

16.1. Benchmark of Key Players including Company Overview, Services, Strategy, Fleet/Warehouse Capacity, Technology Use, Network, Cities Covered, and Expansion Plans

16.2. Strength and Weakness

16.3. Operating Model and Revenue Stream Analysis

16.4. Gartner Magic Quadrant Adaptation

16.5. Bowmans Strategic Clock for Competitive Advantage

17.1. Revenues, 2025-“2029

17.2. Volume Handled, 2025-“2029

18.1. By Market Structure (Organized and Unorganized), 2025-“2029

18.2. By Type of Logistics Service, 2025-“2029

18.3. By Mode of Transport, 2025-“2029

18.4. By Region, 2025-“2029

18.5. By End-User Industry, 2025-“2029

18.6. By Warehouse Type, 2025-“2029

18.7. Recommendation

18.8. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Mapped the ecosystem and identified all key demand-side and supply-side entities within the Bahrain Logistics and Warehousing Market. This included global and local 3PL providers, warehousing companies, freight forwarders, industrial end-users (e.g., oil & gas, FMCG, pharma), and regulatory authorities such as the Bahrain Logistics Zone and Ministry of Transportation and Telecommunications.

Shortlisted 6–8 major logistics and warehousing providers based on market presence, fleet size, infrastructure capabilities (e.g., square footage of warehousing, cold storage), and financial strength.

Sourcing was conducted through industry associations, logistics trade reports, government publications, and proprietary databases to ensure a comprehensive mapping of the sector.

Step 2: Desk Research

Conducted detailed secondary research across credible public and proprietary data sources. This included market reports, government and customs data, publications from Bahrain EDB (Economic Development Board), GCC trade bodies, company websites, press releases, and annual reports.

Analyzed historical and current data regarding service-wise revenue contributions, market shares, warehousing space availability, shipment volume, port capacity, and express delivery trends.

Collected data on key market drivers including trade volumes, non-oil sector growth, infrastructure investments, and regulatory changes impacting logistics operations.

Step 3: Primary Research

Conducted qualitative and quantitative interviews with logistics heads, supply chain managers, and key decision-makers at major logistics companies operating in Bahrain, as well as import-export businesses using these services.

Interviews aimed to validate hypotheses around pricing trends, service preferences, sector-specific logistics needs (e.g., pharma, FMCG), technology adoption, and capacity utilization levels.

Employed a bottom-to-top approach to estimate annual freight and warehouse volume handled by each player and aggregated these to arrive at overall market size estimates.

Disguised interviews with sales executives were also conducted by posing as prospective B2B clients, to cross-check pricing models, service capabilities, and turnaround times.

Step 4: Sanity Check

Market sizing and segmentation models were tested using both bottom-up and top-down triangulation methods to ensure robustness.

Compared primary findings with secondary market sizing estimates and industry benchmarks across the GCC to validate consistency and plausibility.

- Adjustments were made wherever large variances were detected to ensure the model reflected Bahrain-specific operating conditions and infrastructure capacities.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Bahrain logistics and warehousing market is poised for substantial growth, reaching a valuation of BHD 1.007 billion in 2023. This growth is driven by factors such as its strategic location in the Gulf, increasing non-oil trade, and rising demand from sectors like FMCG, pharmaceuticals, and e-commerce. The market’s potential is further bolstered by government-led infrastructure initiatives and logistics zone development aimed at strengthening Bahrain’s position as a regional logistics hub.

The Bahrain Logistics and Warehousing Market features several key players, including DHL Bahrain, Agility Logistics, and GAC Bahrain. These companies dominate the market due to their strong operational capabilities, extensive regional networks, and integrated service offerings. Other notable players include Aramex, FedEx Express, and Almoayyed Logistics.

The primary growth drivers include Bahrain’s strategic location, its connectivity to Saudi Arabia via the King Fahd Causeway, and the growth of re-export trade. The expanding non-oil economy, combined with rising digital adoption in logistics and increasing investment in warehousing infrastructure, also contributes to market growth. Additionally, the rise of e-commerce and demand for cold chain and pharma logistics are creating new growth opportunities.

The Bahrain Logistics and Warehousing Market faces several challenges, including limited space for large-scale warehousing expansion and high operational costs in specialized logistics segments. Regulatory compliance and customs processes, although improving, can still create delays. Additionally, competition from larger regional logistics hubs and the need for skilled workforce in digital logistics present significant challenges to sustained market growth.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0