Bangladesh Cold Chain Market Outlook to 2029

By Market Structure, By End-User Industry, By Type of Products Stored, By Mode of Transportation, By Type of Refrigeration, and By Region

Report Overview

Report Code

TDR0183

Coverage

Asia

Published

May 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Bangladesh Cold Chain Market Outlook to 2029 – By Market Structure, By End-User Industry, By Type of Products Stored, By Mode of Transportation, By Type of Refrigeration, and By Region” provides a comprehensive analysis of the cold chain industry in Bangladesh. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer-level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the Cold Chain Market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Bangladesh Cold Chain Market Outlook to 2029 – By Market Structure, By End-User Industry, By Type of Products Stored, By Mode of Transportation, By Type of Refrigeration, and By Region” provides a comprehensive analysis of the cold chain industry in Bangladesh. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer-level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the Cold Chain Market. The report concludes with future market projections based on revenue, by product category, end-user industry, region, cause-and-effect relationships, and success case studies highlighting major opportunities and cautions.

Bangladesh Cold Chain Market Overview and Size

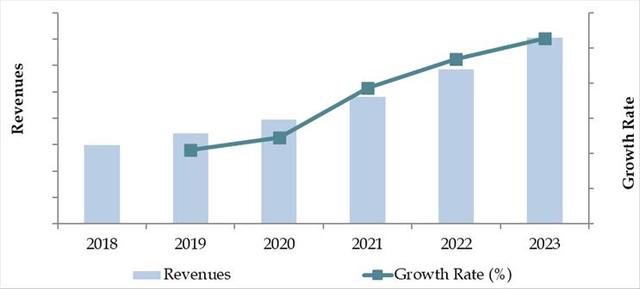

The Bangladesh cold chain market was valued at BDT 16.5 Billion in 2023, driven by increasing demand for temperature-sensitive pharmaceuticals, perishable food items, and agricultural produce. Rapid urbanization, rising health awareness, and the expansion of modern retail and e-commerce channels are key contributors to growth. The market is dominated by players such as Golden Harvest, PRAN-RFL Group, Bengal Meat, ACI Logistics (Shwapno), and Abdul Monem Limited, known for their strong logistics networks and integrated cold storage and distribution services.

In 2023, Golden Harvest Cold Chain Logistics expanded its refrigerated warehousing capacity in Dhaka and Chattogram to cater to rising demand from pharmaceutical and food processing clients. These cities, with their strategic port access and dense consumer bases, serve as key operational hubs for cold chain activities in the country.

Market Size for Bangladesh Cold Chain Industry on the Basis of Revenues in USD Million, 2018-2024

What Factors are Leading to the Growth of Bangladesh Cold Chain Market:

Food Security and Agricultural Preservation: Bangladesh experiences high post-harvest losses (30–40%) due to lack of cold storage. The government’s push for food security, coupled with rising agricultural productivity, has increased the need for efficient cold storage and transport facilities.

Healthcare and Pharmaceuticals: The demand for temperature-controlled logistics has surged due to the rise in vaccine distribution, biopharmaceuticals, and diagnostic kits. In 2023, over BDT 3.5 Billion worth of pharmaceutical products required cold chain logistics, with growth driven by both domestic consumption and exports.

Rising Organized Retail and E-commerce: Supermarkets and online grocery platforms are expanding rapidly, particularly in Dhaka and Chattogram. These retailers require robust cold chain support for storing and delivering fresh produce, frozen food, and dairy.

Which Industry Challenges Have Impacted the Growth for Bangladesh Cold Chain Market

Infrastructure Deficiencies: One of the primary challenges facing the cold chain sector in Bangladesh is inadequate cold storage infrastructure. According to a recent industry assessment, nearly 40% of perishable goods in Bangladesh are exposed to spoilage due to the absence of proper temperature-controlled storage and transportation facilities. This has particularly impacted rural producers and small-scale exporters who lack access to modern logistics support.

High Operating Costs: Cold chain operations in Bangladesh are burdened by high energy and maintenance costs. Diesel-powered generators, which are often used due to inconsistent electricity supply, can increase operating costs by over 25%. This reduces the profitability for operators and creates a pricing challenge for service affordability across the supply chain.

Limited Technical Expertise: The industry faces a scarcity of trained personnel in cold chain management and operations. A 2023 survey highlighted that over 55% of cold storage units are managed without specialized staff, leading to frequent system breakdowns and inefficient temperature monitoring. This not only affects product quality but also customer confidence in the reliability of services.

What are the Regulations and Initiatives which have Governed the Market

Cold Storage Licensing and Compliance: The Bangladesh government requires all commercial cold storages to obtain licenses from the Department of Agricultural Marketing (DAM). These facilities must adhere to technical standards related to insulation, temperature range, and safety protocols. In 2023, approximately 68% of cold storage facilities were found compliant during government audits, marking an improvement over previous years.

Import Duties on Refrigerated Equipment: High import tariffs on refrigerated vehicles and specialized equipment continue to hinder expansion of the cold logistics network. As of 2024, import duties for cold chain equipment such as blast freezers and reefer trucks range from 15% to 25%, increasing initial capital costs for new entrants and deterring small investors.

Government Schemes for Agro-Supply Chains: The Ministry of Agriculture and Ministry of Commerce have jointly introduced incentive schemes such as subsidized loans and grants for setting up cold storage units in agri-centric regions. Under the 2023 Agro-Logistics Enhancement Program, over 20 new facilities received partial funding support, boosting capacity for post-harvest storage in northern and western districts.

Bangladesh Cold Chain Market Segmentation

By Market Structure: The unorganized segment currently dominates the cold chain market in Bangladesh, primarily consisting of small-scale cold storage operators and informal logistics providers. These players often lack standardized temperature monitoring systems but offer localized services, making them more accessible to rural farmers and small businesses. The organized segment, although smaller in share, is growing rapidly with investments from corporate players and multinational logistics firms. These companies provide end-to-end cold chain solutions with advanced refrigeration systems, GPS tracking, and compliance with global standards, attracting large-scale exporters, pharma companies, and food retail chains.

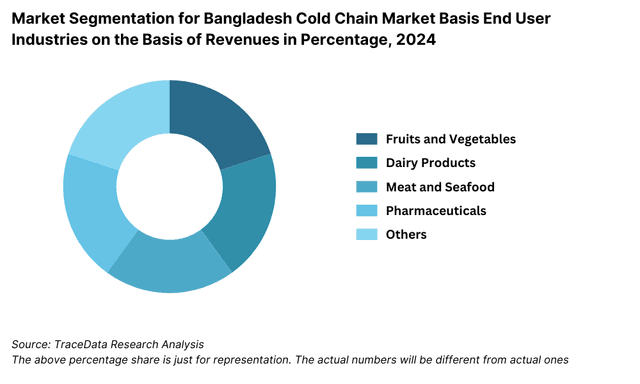

By End-User Industry: The agriculture and horticulture sector holds the largest share due to the country's dependence on fresh produce and seasonal vegetables. Poor post-harvest management has driven demand for cold storage to reduce wastage. The pharmaceutical industry is the second-largest user, driven by stringent temperature requirements for vaccines, biologics, and diagnostics. Meat, poultry, and seafood sectors are also key contributors, especially for frozen export products to the Middle East and Europe. Growth in e-commerce grocery delivery has further increased demand for reliable last-mile refrigerated logistics.

By Temperature Type: The cold chain market is segmented into chilled (0°C to 10°C) and frozen (-18°C and below) categories. Chilled logistics account for a larger share due to the dominance of fresh fruit, vegetables, and dairy. Frozen storage demand is increasing in processed food and seafood exports, particularly in Dhaka and Chattogram regions.

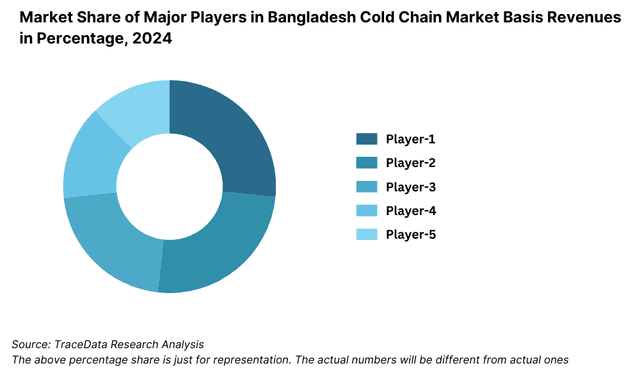

Competitive Landscape in Bangladesh Cold Chain Market

The Bangladesh cold chain market is moderately fragmented, with a mix of established players and emerging companies operating across different segments such as cold storage, refrigerated transport, and integrated cold logistics. The increasing demand for food safety, pharmaceutical compliance, and export-quality preservation has encouraged both local and international firms to expand operations in the country.

| Company Name | Founding Year | Original Headquarters |

| ACI Logistics Ltd. (Shwapno Cold Chain) | 2008 | Dhaka, Bangladesh |

| PRAN-RFL Group (Cold Chain Division) | 1981 | Dhaka, Bangladesh |

| Golden Harvest Logistics Ltd. | 2001 | Dhaka, Bangladesh |

| BRAC Cold Chain (Agri & Dairy Projects) | 1972 | Dhaka, Bangladesh |

| Bangas Ltd. (Cold Storage & Logistics) | 1980 | Dhaka, Bangladesh |

| Gemcon Group (Meena Cold Storage) | 1979 | Dhaka, Bangladesh |

| Paragon Group (Agri Cold Chain) | 1993 | Dhaka, Bangladesh |

| EON Group (Cold Chain Services) | 1991 | Dhaka, Bangladesh |

| Akij Group (Food Cold Chain Division) | 1940 | Dhaka, Bangladesh |

| City Group (Cold Storage Division) | 1972 | Dhaka, Bangladesh |

| Rahimafrooz Cold Chain | 1954 | Dhaka, Bangladesh |

| Maersk Bangladesh (Cold Chain Solutions) | 1904 (BD: ~2000s) | Copenhagen, Denmark |

| DHL Global Forwarding Bangladesh (Temperature-Controlled Logistics) | 1969 (BD: ~1980s) | Bonn, Germany |

| DB Schenker Bangladesh (Cold Chain Division) | 1872 (BD: ~2000s) | Essen, Germany |

| Kuehne + Nagel Bangladesh (Perishables and Pharma Logistics) | 1890 (BD: ~2000s) | Schindellegi, Switzerland |

Some of the recent competitor trends and key information about competitors include:

Golden Harvest Ice Cream Ltd: A key player in the frozen food segment, the company operates its own cold storage facilities and temperature-controlled distribution network. In 2023, the company expanded its capacity by 25% to support growing demand for frozen processed food.

Aftab Bahumukhi Farms Ltd: A pioneer in poultry and meat cold logistics, Aftab has invested in modern blast freezing and refrigerated transport units. The company’s cold chain division grew 18% in 2023, driven by rising domestic meat consumption and demand for hygienic packaging.

PRAN-RFL Group: One of the largest FMCG companies in Bangladesh, PRAN operates an extensive cold storage network for beverages, dairy, and agri-products. In 2023, the company launched a regional cold storage hub in Bogura to reduce transit losses for fresh produce.

Bengal Meat: Specialized in export-oriented meat processing, Bengal Meat operates integrated cold chain systems from slaughterhouses to export terminals. In 2023, the firm reported a 30% increase in exports, driven by demand from Gulf countries and institutional buyers.

BRAC Cold Chain Solutions: A social enterprise focusing on rural access to cold storage for agri-products and vaccines. BRAC’s micro-cold storage units deployed in northern districts helped reduce post-harvest loss by 20% for over 15,000 smallholder farmers in 2023.

What Lies Ahead for Bangladesh Cold Chain Market?

The Bangladesh cold chain market is projected to witness significant expansion by 2029, driven by rising demand for quality food preservation, pharmaceutical compliance, and export-grade logistics infrastructure. The sector is expected to grow at a healthy CAGR during the forecast period, supported by public-private partnerships, digital innovation, and increasing private sector participation.

Expansion of Pharmaceutical Cold Chain: With Bangladesh becoming a major exporter of generic pharmaceuticals, demand for highly controlled temperature logistics for vaccines, biologics, and insulin is projected to grow rapidly. Investments in WHO-GDP compliant cold storage and transport solutions will become a major focus area.

Digitization and IoT Adoption: The cold chain sector is expected to see increased integration of IoT-enabled temperature sensors, real-time tracking systems, and cloud-based inventory platforms. These technologies will improve traceability, reduce spoilage, and enhance supply chain visibility for logistics operators and end-users alike.

Government Incentives and Infrastructure Push: Upcoming government-backed infrastructure programs and policy incentives—particularly under the National Agricultural Policy and Export Policy—are expected to boost private investments in cold storages, reefer trucks, and solar-powered preservation units, especially in agri-dominant regions like Rangpur, Rajshahi, and Mymensingh.

Growth of Integrated Cold Chain Logistics Providers: The market is likely to see a shift from standalone cold storage units to fully integrated cold chain service providers offering end-to-end solutions from first mile to last mile. This consolidation is expected to improve service quality, reduce inefficiencies, and provide scalability for food and pharma exporters.

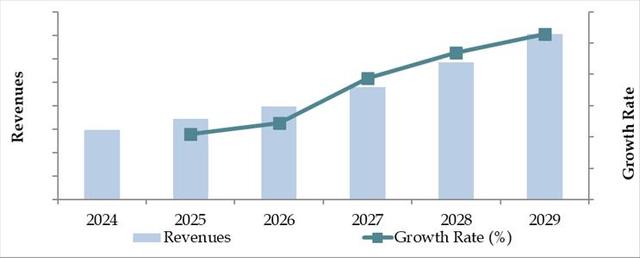

Future Outlook and Projections for Bangladesh Cold Chain Market on the Basis of Revenues in USD Million, 2024-2029

Bangladesh Cold Chain Market Segmentation

• By Market Structure:

o Integrated Cold Chain Solution Providers

o Standalone Cold Storage Facilities

o Refrigerated Transport Operators

o Third-Party Logistics (3PL) Providers

o Organized Sector

o Unorganized Sector

• By End-User Industry:

o Agriculture & Horticulture

o Dairy Products

o Meat & Seafood

o Pharmaceuticals

o Processed Food

o E-commerce Grocery Delivery

• By Temperature Type:

o Chilled (0°C to 10°C)

o Frozen (-18°C and below)

• By Storage Capacity:

o <500 MT

o 500–1000 MT

o 1000–5000 MT

o >5000 MT

• By Type of Refrigerated Transport:

o Reefer Vans

o Refrigerated Trucks

o Insulated Containers

• By Region:

o Dhaka

o Chattogram

o Rajshahi

o Khulna

o Barisal

o Sylhet

Players Mentioned in the Report:

· Cold Chain Bangladesh Limited (CCBL)

· Transmove

· Dreamco Express

· Golden Harvest Express

· Yusen Logistics Bangladesh

· A.H. Khan & Co. Ltd.

· 3i Logistics Group

· MGH Group

· Younus Group of Industries

· AK Khan & Company

Key Target Audience:

• Cold Storage Operators

• Refrigerated Transport Companies

• Agri Exporters and Cooperatives

• Pharmaceutical Distributors

• Government Agencies (e.g., Ministry of Agriculture, Export Promotion Bureau)

• Logistics and Infrastructure Investors

• International Development Organizations

• R&D and Innovation Institutes

Time Period:

• Historical Period: 2018–2023

• Base Year: 2024

• Forecast Period: 2024–2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

6.1. Revenues, 2018-2024P

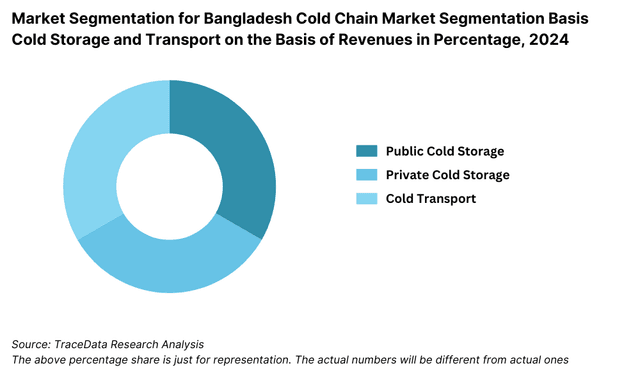

7.1. By Cold Storage and Cold Transport, 2023-2024P

7.2. By End-User Application (Dairy Products, Meat and Seafood, Pharmaceuticals, Fruits and Vegetables and Others), 2023-2024P

7.3. By Ownership (Owned and 3PL Cold Chain Facilities), 2023-2024P

10.1. Bangladesh Cold Storage Market Size

10.1.1. By Revenue, 2018-2024P

10.1.2. By Number of Pallets, 2018-2024P

10.2. Bangladesh Cold Storage Market Segmentation

10.2.1. By Temperature Range (Ambient, Chilled and Frozen), 2023-2024P

10.2.2. By End-User Application (Dairy Products, Meat and Seafood, Pharmaceuticals, Fruits and Vegetables and Others), 2023-2024P

10.2.3. By Major Cities, 2023-2024P

10.3. Bangladesh Cold Storage Market Future Outlook and Projections, 2025-2029

10.3.1. By Temperature Range (Ambient, Chilled and Frozen), 2025-2029

10.3.2. By Major Cities (Manila, Quezon, Cebu and others), 2025-2029

11.1. Bangladesh Cold Transport Market Size (By Revenue and Number of Reefer Trucks), 2018-2024P

11.2. Bangladesh Cold Transport Market Segmentation

11.2.1. By Mode of Transportation (Land, Sea and Air), 2023-2024P

11.2.2. By Location (Domestic and International), 2023-2024P

11.3. Bangladesh Cold Transport Market Future Outlook and Projections, 2025-2029

11.3.1. By Mode of Transport (Land, Sea and Air), 2025-2029

11.3.2. By Location (Domestic and International), 2025-2029

12.1. Trends and Developments in Bangladesh Cold Chain Market

12.2. Issues and Challenges in Bangladesh Cold Chain Market

12.3. Decision Making Parameters for End Users in Bangladesh Cold Chain Market

12.4. SWOT Analysis of Bangladesh Cold Chain Industry

12.5. Government Regulations and Associations in Bangladesh Cold Chain Market

12.6. Macroeconomic Factors Impacting Bangladesh Cold Chain Market

13.1. Parameters to be covered for Each End Users to Determine Business Potential:

13.1.1. Production Clusters

13.1.2. Market Demand, Major Products Stored, Cold Storage Companies in Guwahati catering to End Users

13.1.3. Location Preference for Each End User and their Production Plants, Preferences for Outsourcing and Captive Facility, Services Required, Facility Preferences, Decision Making Parameters

13.1.4. Cross comparison of leading end users/companies based on Headquarters, Manufacturing Plants, Products Stored, Major Products, Total Production, Cold Chain Partner, Facility Outsourced/Captive, Pallets Owned/Hired, Contact Person, Address and others

16.1. Competitive Landscape in Bangladesh Cold Chain Market

16.2. Competition Scenario in Bangladesh Cold Chain Market (Competition Stage, Major Players, Competing Parameters)

16.3. Key Metrics (Temperature Range, Pallet Position, Prices Charged, Occupancy Rate, Revenue (2023) and Employee Base) for Major Players in Bangladesh Cold Chain Market

16.4. Company Profiles of Major Companies in Bangladesh Cold Chain Market (Year of Establishment, Company Overview, Service Offered, USP, Warehousing Facilities, Warehousing Price, Cold Storage by location, Occupancy Rate, Major Clientele, Industries Catered, Employee Base, Temperature Range, Topline OPEX*, Revenue, Recent Developments, Future Strategies)

16.5. Strength and Weakness

16.6. Operating Model Analysis Framework

16.7. Gartner Magic Quadrant

16.8. Bowmans Strategic Clock for Competitive Advantage

17.1. Revenues, 2025-2029

18.1. By Cold Storage and Cold Transport, 2025-2029

18.2. By End-User Application (Dairy Products, Meat and Seafood, Pharmaceuticals, Fruits and Vegetables and Others), 2025-2029

18.3. By Ownership (Owned and 3PL Cold Chain Facilities), 2025-2029

18.4. Recommendation

18.5. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities within the Bangladesh Cold Chain Market. Based on this mapping, we shortlist 5–6 key companies across cold storage, refrigerated transport, and integrated logistics services based on criteria such as revenue, facility capacity, and regional footprint.

Sourcing is conducted through industry reports, government publications, and multiple secondary and proprietary databases to perform structured desk research and gather baseline industry information.

Step 2: Desk Research

An exhaustive secondary research process is then undertaken using public domain sources, industry white papers, policy documents, market databases, and commercial research platforms. This step includes analyzing market-level variables such as cold storage capacity, logistics infrastructure, usage by sector, and investment flows.

Detailed company-level assessments are performed by reviewing financial filings, press releases, partnership announcements, and expansion projects to evaluate market share, operational scale, and geographical coverage of key players in Bangladesh.

Step 3: Primary Research

A series of in-depth interviews are conducted with top management, logistics heads, cold chain engineers, and other key stakeholders from across cold chain companies, agribusiness exporters, pharmaceutical distributors, and government-linked agencies.

This step is designed to validate hypotheses formed during desk research, authenticate statistical data, and gain deep insights into operational challenges, pricing models, process bottlenecks, and infrastructure readiness.

As part of data validation, our team also conducts disguised interviews with cold chain providers posing as prospective clients. This enables cross-verification of service pricing, asset capacity, refrigeration technology, and service coverage claims.

Step 4: Sanity Check

- A combination of bottom-up (individual company volume aggregation) and top-down (industry benchmarking and macro analysis) modeling exercises is undertaken to perform a market sizing sanity check. The goal is to ensure consistency and accuracy of insights across both primary and secondary data sources.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Bangladesh cold chain market is poised for strong growth, driven by increasing demand in agriculture, pharmaceuticals, and food processing sectors. With rising export volumes, stricter food safety standards, and a growing domestic need for temperature-controlled logistics, the market is expected to expand steadily and reach multi-billion BDT valuation by 2029. Government incentives and foreign investment are further enhancing the market’s long-term potential.

Key players in the Bangladesh cold chain market include Golden Harvest Ice Cream Ltd, Aftab Bahumukhi Farms Ltd, PRAN-RFL Group, Bengal Meat, and BRAC Cold Chain Solutions. These companies operate across various segments such as cold storage, refrigerated transportation, and integrated logistics, serving both domestic and export-focused industries.

The main growth drivers include increasing demand for food preservation in agriculture, expanding pharmaceutical exports requiring cold logistics, government support for agro-logistics infrastructure, and technological advancements in temperature monitoring. Rising consumer awareness of food safety and reduction in post-harvest losses are also accelerating demand for cold chain solutions.

Major challenges include inadequate cold storage infrastructure, high operational and energy costs, limited availability of skilled workforce, and regulatory bottlenecks around equipment imports. Additionally, the fragmented nature of the market and the dominance of unorganized players restrict efficiency and scalability.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0