Cambodia Alcoholic Drinks Market Outlook to 2029

By Market Structure, By Product Types (Beer, Wine, Spirits, Others), By Consumer Demographics, By Distribution Channels (On-trade, Off-trade), and By Region

Report Overview

Report Code

TDR0046

Coverage

Asia

Published

October 2024

Pages

80-100

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled "Cambodia Alcoholic Drinks Market Outlook to 2029 - By Market Structure, By Product Types (Beer, Wine, Spirits, Others), By Consumer Demographics, By Distribution Channels (On-trade, Off-trade), and By Region " provides a comprehensive analysis of the alcoholic drinks market in Cambodia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities, bottlenecks, and profiling of major players in the Cambodian Alcoholic Drinks Market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled "Cambodia Alcoholic Drinks Market Outlook to 2029 - By Market Structure, By Product Types (Beer, Wine, Spirits, Others), By Consumer Demographics, By Distribution Channels (On-trade, Off-trade), and By Region " provides a comprehensive analysis of the alcoholic drinks market in Cambodia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities, bottlenecks, and profiling of major players in the Cambodian Alcoholic Drinks Market. The report concludes with future market projections based on sales revenue by product type, distribution channel, consumer demographics, and region, along with key success factors and case studies highlighting major opportunities and challenges.

Cambodia Alcoholic Drinks Market Overview and Size

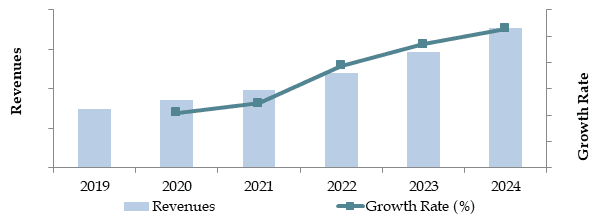

The Cambodian alcoholic drinks market reached a valuation of USD 900 million in 2023, driven by rising disposable incomes, a growing tourism sector, and shifting consumer preferences toward premium beverages. The market is characterized by major players such as Cambrew, Khmer Brewery, Heineken Cambodia, and Singha. These companies are known for their diverse portfolios, ranging from beer to spirits and wines, catering to the increasing demand from both locals and international tourists.

In 2023, Khmer Brewery expanded its product line to include premium craft beers, targeting the younger, more affluent demographic. Phnom Penh and Siem Reap are key markets due to their high population density and robust tourism industry.

Market Size for Cambodia Alcoholic Beverage Industry on the Basis of Revenue in USD Billion, 2018-2024

Source: TraceData Research Analysis

What Factors are Leading to the Growth of Cambodia Alcoholic Drinks Market:

Rising Disposable Income: Cambodia's expanding middle class and increasing disposable income have led to higher spending on premium alcoholic beverages. In 2023, alcoholic drinks sales increased by 15% as more consumers opted for higher-quality brands, especially in urban areas like Phnom Penh and Siem Reap, where incomes are higher.

Growing Tourism Industry: Cambodia’s booming tourism sector has significantly driven demand for alcoholic beverages, particularly beer and spirits, in popular tourist hubs. In 2023, tourist arrivals increased by 18%, contributing to higher alcohol consumption in bars, restaurants, and hotels. International tourists, especially from countries with strong drinking cultures, have pushed up the demand for a wider variety of alcoholic beverages.

Expanding Retail Infrastructure: The rapid growth of modern retail channels, including supermarkets, hypermarkets, and convenience stores, has made alcoholic beverages more accessible to consumers. In 2023, modern retail channels accounted for 45% of alcoholic drink sales, as they provide a more diverse product selection and improved purchasing convenience.

Which Industry Challenges Have Impacted the Growth for Cambodia Alcoholic Drinks Market:

Quality and Safety Concerns: Concerns about the quality and safety of locally produced alcoholic drinks pose significant challenges. Approximately 40% of Cambodian consumers have expressed hesitancy in purchasing local spirits due to fears of adulteration and poor-quality control. This lack of confidence in domestic production has led to a preference for imported beverages, affecting the market share of local brands.

Regulatory Hurdles: Stringent government regulations on alcohol advertising and sales restrictions have limited the market's growth potential. In 2023, regulations mandating higher taxes on alcohol and restrictions on sales in certain public spaces have led to a decline in consumption, especially in rural areas where these restrictions are more heavily enforced.

Limited Distribution Networks in Rural Areas: Access to alcoholic beverages in rural regions of Cambodia is limited due to underdeveloped distribution networks. Approximately 35% of rural consumers reported difficulties in finding a diverse range of alcoholic drinks, which hampers the growth potential of the market outside urban centers.

What are the Regulations and Initiatives which have Governed the Market:

Alcohol Advertising Restrictions: The Cambodian government enforces strict regulations on alcohol advertising to curb excessive consumption, especially among youth. Alcohol advertisements are banned on national television and restricted across various media platforms. In 2023, this regulation led to a 10% decline in alcohol marketing expenditures, forcing companies to find alternative ways to promote their products.

Excise Taxes on Alcoholic Beverages: The Cambodian government has imposed high excise taxes on alcoholic beverages to discourage excessive consumption and raise revenue. In 2023, the excise tax on spirits was increased by 12%, which has directly impacted the retail prices of both imported and locally produced drinks, limiting consumption growth, particularly in lower-income segments.

Regulations on Alcohol Sales: The sale of alcohol is regulated in terms of hours of operation and permitted outlets. For instance, alcohol sales are restricted after 11 PM in some regions, and licenses are required for retailers to sell alcohol. In 2022, 15% of retailers faced penalties for non-compliance, demonstrating the government's active enforcement of these regulations.

Cambodia Alcoholic Drinks Market Segmentation

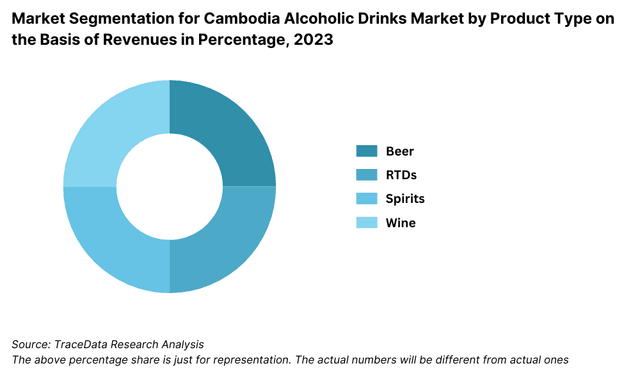

By Product Type: Beer dominates the alcoholic drinks market in Cambodia due to its affordability and cultural acceptance as a common social beverage. In 2023, beer accounted for approximately 60% of total alcoholic drink sales, driven by both domestic brands like Angkor Beer and international brands. Spirits hold a significant share as well, particularly among older consumers and tourists, with whiskey and rum being the most popular. Wine has seen growing demand, especially in urban areas, where it is increasingly associated with premium dining experiences.

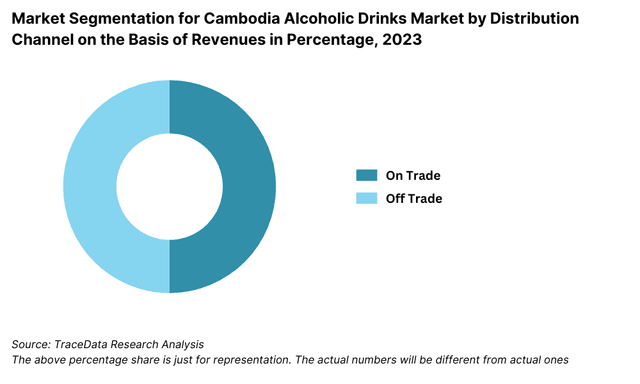

By Distribution Channel: On-trade channels such as bars, restaurants, and nightclubs account for a significant portion of alcoholic drink sales in Cambodia, particularly in major cities like Phnom Penh and Siem Reap. Off-trade channels, including supermarkets, convenience stores, and local shops, contribute heavily to retail sales, especially for beer and lower-priced spirits. In 2023, off-trade channels made up around 55% of total sales due to their convenience and affordability.

By Consumer Demographics: The 25-40 age group is the largest consumer segment for alcoholic drinks in Cambodia, driven by their socializing habits and rising disposable incomes. This demographic is particularly inclined toward premium beer and craft beverages. The 18-24 age group shows increasing consumption, especially in urban areas, where trends like cocktail culture are gaining popularity.

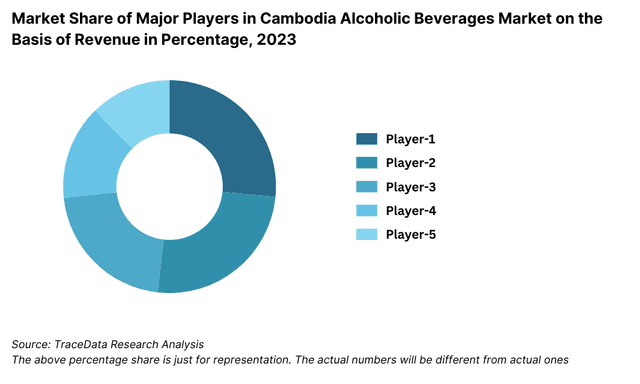

Competitive Landscape in Cambodia Alcoholic Drinks Market

The Cambodian alcoholic drinks market is moderately concentrated, with a few major players leading the industry. However, the emergence of new local breweries and the increasing presence of international brands have diversified the market. Key players include Cambrew, Khmer Brewery, Heineken Cambodia, and Singha, all of which dominate the beer segment. Meanwhile, smaller craft breweries and spirits producers are gaining traction, particularly in urban markets like Phnom Penh and Siem Reap.

Company Name | Establishment Year | Headquarters |

|---|---|---|

Heineken Cambodia | 1864 | Amsterdam, Netherlands |

Cambrew Ltd. (Angkor Beer) | 1991 | Sihanoukville, Cambodia |

Carlsberg Group | 1847 | Copenhagen, Denmark |

Diageo | 1997 | London, United Kingdom |

Pernod Ricard | 1975 | Paris, France |

Bacardi | 1862 | Hamilton, Bermuda |

Asia Pacific Breweries | 1931 | Singapore |

| Brown-Forman | 1870 | Louisville, Kentucky, USA |

| Cambodia Brewery Ltd. (Tiger Beer) | 1992 | Phnom Penh, Cambodia |

AB InBev | 2008 | Leuven, Belgium |

Some of the recent competitor trends and key information about competitors include:

Cambrew: As one of the leading beer producers in Cambodia, Cambrew saw a 15% growth in beer sales in 2023, driven by its flagship brand, Angkor Beer. The company's strong distribution network and strategic marketing initiatives, especially in tourist-heavy areas, have cemented its dominance in the local market.

Khmer Brewery: Known for its Cambodia Beer brand, Khmer Brewery recorded a 20% increase in sales in 2023, owing to its aggressive marketing campaigns targeting younger consumers. The brewery also expanded its portfolio to include premium and craft beer options to cater to evolving consumer preferences.

Heineken Cambodia: Heineken's Cambodian operations reported a 12% growth in beer sales in 2023, primarily due to the increasing popularity of its global brands, including Heineken and Tiger Beer. The company continues to invest in localizing its marketing efforts to capture the growing middle-class consumer base.

Singha (via Carlsberg): Singha, in partnership with Carlsberg, has made significant strides in Cambodia’s premium beer segment, recording a 10% growth in 2023. The brand’s focus on high-end venues and premium product positioning has helped it capture the urban consumer market.

What Lies Ahead for Cambodia Alcoholic Drinks Market?

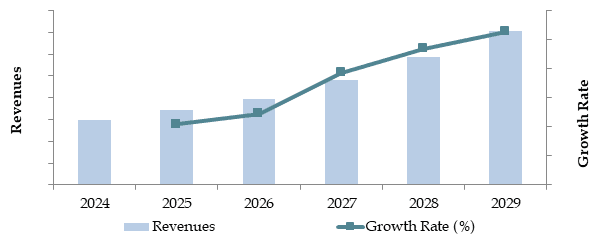

The Cambodian alcoholic drinks market is projected to grow steadily by 2029, driven by rising disposable incomes, increasing tourism, and changing consumer preferences. The market is expected to exhibit a strong CAGR during the forecast period, fueled by the growing popularity of premium alcoholic beverages and the expansion of modern retail channels.

Shift Towards Premiumization: As Cambodian consumers become more affluent, there is a noticeable shift toward premium alcoholic beverages, especially in urban areas. Beer, wine, and craft spirits are expected to see increased demand as consumers seek higher-quality drinks for social and leisure occasions. This trend will be particularly strong among younger consumers in Phnom Penh and Siem Reap.

Growth in Craft Beer and Local Production: Cambodia is experiencing a boom in the craft beer industry, with new microbreweries emerging in the market. Local brewers are capitalizing on the growing preference for unique, locally sourced products. This segment is expected to grow significantly as Cambodian consumers become more adventurous in their beverage choices.

Expansion of Distribution Channels: The continued expansion of modern retail outlets, such as supermarkets, hypermarkets, and convenience stores, will make alcoholic beverages more accessible to a wider consumer base. Additionally, e-commerce platforms are likely to play a more significant role in alcohol distribution, catering to the growing demand for online shopping and delivery services.

Focus on Sustainability: The increasing awareness of environmental sustainability is expected to influence the Cambodian alcoholic drinks market. Major players are adopting sustainable practices in production, packaging, and distribution, including the use of eco-friendly packaging materials and initiatives to reduce carbon emissions. These efforts are expected to resonate with environmentally conscious consumers and drive further growth in the premium segment.

Future Outlook and Projections for Cambodia Alcoholic Beverages Market on the Basis of Revenues in USD Billion, 2024-2029

Source: TraceData Research Analysis

Cambodia Alcoholic Drinks Market Segmentation

- By Alcohol Type:

- Beer

- Spirits (Whiskey, Vodka, Rum)

- Wine (Red, White, Sparkling)

- Cider

- Ready-to-Drink (RTD) Cocktails

- By Beer

- Lager

- Dark Beer and others

- By Beer

- Craft

- Standard Beer

- By RTDs

- Malt based RTDs

- Spirit Based RTDs

- Wine Based RTDs

- Non-Alcoholic RTDs and others

- By Spirits

- Brandy

- Dark Rum

- White Rum

- Whiskies

- Gin

- Vodka and others

- By Vodka

- Flavoured

- Non-Flavoured Vodka

- By Wine

- Fortified Wine

- Champagne

- Other Sparkling Wine

- Red Wine

- White Wine and others

- By Distribution Channel:

- On-Trade (Bars, Restaurants, Hotels)

- Off-Trade (Supermarkets, Hypermarkets, Convenience Stores)

- By Price Segment:

- Economy

- Mid-Range

- Premium

- Super Premium

- By Consumer Age:

- 18-24

- 25-34

- 35-54

- 55+

- By Region:

- Phnom Penh

- Siem Reap

- Sihanoukville

- Battambang

- Kampong Cham

Players Mentioned in the Report:

- Cambodia Brewery Ltd. (Heineken)

- Khmer Brewery (Producers of Cambodia Beer)

- Carlsberg Group

- Diageo PLC

- Pernod Ricard

- Heineken N.V.

- Thai Beverage Public Co. Ltd

Key Target Audience:

- Alcoholic Beverage Producers

- Retailers and Distributors

- Hospitality Industry

- Tourism and Travel Operators

- Regulatory Bodies (e.g., Ministry of Commerce, Ministry of Tourism)

- Research and Development Institutions

Time Period:

- Historical Period: 2018-2023

- Base Year: 2024

- Forecast Period: 2024-2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-Role of Entities, Stakeholders, Gross Margins, and Challenges they Face

4.2. Business Model Canvas for Cambodia Alcoholic Drinks Market

4.3. Consumer Buying Decision Process

5.1. Market Overview and Genesis

5.2. Number of Breweries and Microbreweries, as on Date

8.1. Revenues, 2018-2024

8.2. Sales Volume, 2018-2024

9.1. By Type (Beer, Cider, RTDs, Spirits and Wine), 2018-2023

9.1.1. By Beer (Lager, Dark Beer and others), 2018-2023

9.1.1.1. By Lager (Domestic Premium and Imported Premium), 2018-2023

9.1.1.2. By Craft and Standard Beer, 2018-2023

9.1.1.3. By Price (Super Premium, Premium, Standard and Economy), 2018-2023

9.1.2. By RTDs (Malt based RTDs, Spirit Based RTDs, Wine Based RTDs, Non-Alcoholic RTDs and others), 2018-2023

9.1.2.1. By Price (Super Premium, Premium, Standard and Economy), 2018-2023

9.1.3. By Spirits (Brandy, Dark Rum, White Rum, Whiskies, Gin, Vodka and others), 2018-2023

9.1.3.1. By Price (Super Premium, Premium, Standard and Economy), 2018-2023

9.1.3.2. By Flavoured and Non-Flavoured Vodka, 2018-2023

9.1.4. By Wine (Fortified Wine, Champagne, Other Sparkling Wine, Red Wine, White Wine and others), 2018-2023

9.1.4.1. By Price (Super Premium, Premium, Standard and Economy), 2018-2023

9.2. By Off Trade and On Trade for Each Type of Alcoholic Beverages, 2023

9.2.1. By Distribution Channel for Off Trade, 2023

9.3. By States, 2023-2024P

10.1. Customer Landscape and Segment Analysis

10.2. Customer Journey and Decision-Making Process

10.3. Consumer Needs, Preferences, and Pain Points

10.4. Gap Analysis Framework

11.1. Trends and Developments in Cambodia Alcoholic Drinks Market

11.2. Growth Drivers for Cambodia Alcoholic Drinks Market

11.3. SWOT Analysis for Cambodia Alcoholic Drinks Market

11.4. Issues and Challenges for Cambodia Alcoholic Drinks Market

11.5. Government Regulations for Cambodia Alcoholic Drinks Market

14.1. Market Share of Key Players in Alcoholic Beverages Market, 2023

14.2. Market Share of Key Players in Beer Market, 2023

14.3. Market Share of Key Players in Wine Market, 2023

14.4. Market Share of Key Players in Spirits Market, 2023

14.5. Market Share of Key Players in RTDs Market, 2023

14.6. Benchmark of Key Competitors in Cambodia Alcoholic Drinks Market Basis 15-20 Operational and Financial Parameters

14.7. Strength and Weakness of Key Competitors

14.8. Operating Model Analysis Framework

14.9. Gartner Magic Quadrant for Market Positioning

14.10. Bowmans Strategic Clock for Competitive Advantage

15.1. Revenues, 2025-2029

15.2. Sales Volume, 2025-2029

16.1. By Type (Beer, Cider, RTDs, Spirits and Wine), 2025-2029

16.1.1. By Beer (Lager, Dark Beer and others), 2025-2029

16.1.1.1. By Lager (Domestic Premium and Imported Premium), 2025-2029

16.1.1.2. By Craft and Standard Beer, 2025-2029

16.1.1.3. By Price (Super Premium, Premium, Standard and Economy), 2025-2029

16.1.2. By RTDs (Malt based RTDs, Spirit Based RTDs, Wine Based RTDs, Non-Alcoholic RTDs and others), 2025-2029

16.1.2.1. By Price (Super Premium, Premium, Standard and Economy), 2025-2029

16.1.3. By Spirits (Brandy, Dark Rum, White Rum, Whiskies, Gin, Vodka and others), 2025-2029

16.1.3.1. By Price (Super Premium, Premium, Standard and Economy), 2025-2029

16.1.3.2. By Flavoured and Non-Flavoured Vodka, 2025-2029

16.1.4. By Wine (Fortified Wine, Champagne, Other Sparkling Wine, Red Wine, White Wine and others), 2025-2029

16.1.4.1. By Price (Super Premium, Premium, Standard and Economy), 2025-2029

16.2. By Off Trade and On Trade for Each Type of Alcoholic Beverages, 2025-2029

16.2.1. By Distribution Channel for Off Trade, 2025-2029

16.3. By States, 2025-2029

17.1. Strategic Recommendations

17.2. Opportunity Identification

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities for the Cambodia Alcoholic Drinks Market. Based on this ecosystem, we will shortlist leading 5-6 producers in the country by analyzing their financial information, production capacity/volume.

Sourcing is done through industry articles, multiple secondary, and proprietary databases to perform desk research around the market and gather industry-level information.

Step 2: Desk Research

Subsequently, we engage in an exhaustive desk research process by referencing a diverse range of secondary and proprietary databases. This approach enables us to conduct a thorough analysis of the market, aggregating industry-level insights. We examine aspects such as sales revenues, number of market players, price levels, and demand trends. We supplement this with detailed examinations of company-level data, relying on sources like press releases, annual reports, and financial statements. This process helps build a foundational understanding of both the market and the entities operating within it.

Step 3: Primary Research

We initiate a series of in-depth interviews with C-level executives and other stakeholders representing various Cambodia Alcoholic Drinks Market companies and end-users. These interviews serve multiple purposes: to validate market hypotheses, authenticate statistical data, and extract valuable operational and financial insights from these industry representatives. A bottom-to-top approach is undertaken to evaluate volume sales for each player, thereby aggregating data to assess the overall market.

As part of our validation strategy, our team conducts disguised interviews where we approach each company as potential customers. This approach allows us to verify operational and financial information shared by company executives and cross-reference it with secondary databases. These interactions also provide a deeper understanding of revenue streams, value chains, processes, pricing, and other relevant factors.

Step 4: Sanity Check

- Bottom-to-top and top-to-bottom analysis, along with market size modeling exercises, are conducted to ensure the accuracy and reliability of the collected data. This step ensures a thorough sanity check process before concluding the findings.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Cambodia alcoholic drinks market is expected to experience steady growth, reaching a valuation of USD 1.2 Billion by 2029. This growth is driven by factors such as rising disposable incomes, increased tourism, and shifting consumer preferences toward premium alcoholic beverages. The market's potential is further enhanced by the expansion of modern retail channels and the growing popularity of craft and local brews.

The Cambodian alcoholic drinks market features several key players, including Cambrew, Khmer Brewery, Heineken Cambodia, and Singha (via Carlsberg). These companies dominate the market with their strong brand presence, extensive distribution networks, and diverse product portfolios. Additionally, new local craft breweries are emerging, adding to the market’s diversity.

The primary growth drivers include increased disposable incomes, which allow consumers to spend more on premium drinks, and Cambodia’s flourishing tourism sector, which significantly boosts demand for alcoholic beverages. Additionally, the expansion of modern retail outlets and online sales channels has made alcoholic beverages more accessible, enhancing market growth.

Cambodian alcoholic drinks market faces several challenges, including strict government regulations on advertising and sales, high taxation on imported beverages, and quality concerns with some local products. Additionally, limited distribution networks in rural areas and price sensitivity among consumers pose significant barriers to growth, particularly for premium and imported alcoholic beverages.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0