Cambodia Cold Chain Market Outlook to 2029

By Market Structure (Cold Storage and Cold Transport), By End-Users (Fruits & Vegetables, Meat & Seafood, Dairy Products, Pharmaceuticals), By Temperature Type, By Region, and By Ownership Model

Report Overview

Report Code

TDR0260

Coverage

Asia

Published

September 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Cambodia Cold Chain Market Outlook to 2029 – By Market Structure (Cold Storage and Cold Transport), By End-Users (Fruits & Vegetables, Meat & Seafood, Dairy Products, Pharmaceuticals), By Temperature Type, By Region, and By Ownership Model” provides a comprehensive analysis of the cold chain market in Cambodia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the cold...

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Cambodia Cold Chain Market Outlook to 2029 – By Market Structure (Cold Storage and Cold Transport), By End-Users (Fruits & Vegetables, Meat & Seafood, Dairy Products, Pharmaceuticals), By Temperature Type, By Region, and By Ownership Model” provides a comprehensive analysis of the cold chain market in Cambodia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the cold chain market. The report concludes with future market projections based on revenue, by segment, end-user category, and region, along with success case studies and key insights.

Cambodia Cold Chain Market Overview and Size

The Cambodia cold chain market reached a valuation of USD 210 Million in 2023, driven by rising demand for perishable food safety, increasing urbanization, and the expansion of the country's retail and pharmaceutical sectors. Major players in the market include Cambodia Cold Chain Logistics, Phnom Penh Cold Storage, Linfox, Mekong Express, and DHL Cambodia, known for their network connectivity, compliance with international storage standards, and service diversification.

In 2023, Phnom Penh Cold Storage introduced new temperature-controlled warehouse units in the Kandal region to meet increasing demand from agribusiness exporters and pharmaceutical distributors. Key demand centers include Phnom Penh, Siem Reap, and Sihanoukville, given their port access, population density, and food distribution networks.

%252C%25202019-2024.png&w=640&q=75)

What Factors are Leading to the Growth of Cambodia Cold Chain Market:

Agricultural Export Push: Cambodia has been aggressively expanding its export of perishable goods, particularly tropical fruits (mangoes, bananas, and longans), seafood, and vegetables. In 2023, agricultural exports contributed over 20% to total national exports, requiring temperature-sensitive supply chains to preserve freshness and meet international standards.

Rise in Organized Retail and E-commerce: Growth in supermarkets (Aeon, Lucky Supermarket) and online grocery platforms has driven the need for cold storage and delivery logistics. In 2023, organized retail outlets accounted for 27% of food sales, up from 18% in 2020, creating a downstream push for integrated cold chain systems.

Pharmaceutical Sector Expansion: The post-pandemic rise in vaccine and biologics demand, coupled with increased government investment in healthcare infrastructure, has elevated the importance of GDP-compliant cold chain systems. Vaccine imports and distribution now constitute 9–11% of cold chain volume usage in the country.

Which Industry Challenges Have Impacted the Growth for Cambodia Cold Chain Market

High Energy and Operating Costs: Operating cold storage and transport facilities in Cambodia is expensive due to high electricity tariffs and reliance on diesel-powered backup systems. According to recent industry data, around 38% of operational costs in cold chain logistics are attributed to energy expenses. These high costs discourage new entrants and limit scalability for existing players, especially in rural areas.

Fragmented Cold Chain Infrastructure: The cold chain network in Cambodia is still in a nascent stage, with uneven distribution of facilities across regions. In 2023, over 60% of cold storage capacity was concentrated in Phnom Penh and Sihanoukville, leading to inefficiencies in supply chain flow from northern and central provinces. This fragmentation creates bottlenecks, especially during peak harvest and export seasons.

Shortage of Skilled Manpower: There is a noticeable lack of trained professionals for cold chain operations including temperature-sensitive handling, monitoring, and compliance with international standards. As per logistics industry surveys, close to 45% of cold chain firms in Cambodia reported difficulty in finding skilled technicians and warehouse managers, impacting service quality and operational consistency.

What are the Regulations and Initiatives which have Governed the Market:

Cold Chain Standards for Agri Exports: The Cambodian Ministry of Commerce has enforced new export compliance requirements for agri-produce that mandate cold chain handling for high-value perishables such as mangoes and bananas. In 2023, about 70% of certified exporters adopted basic temperature tracking systems to meet destination market protocols in China and Korea.

Investment Incentives for Logistics: To attract foreign and private investment in cold logistics, the Cambodian government offers 5–7 year tax holidays, import duty exemptions for cold chain equipment, and special investment zones. These incentives led to an 8% YoY increase in cold chain FDI in 2023, primarily in Phnom Penh and Kandal provinces.

Public-Private Partnerships for Rural Access: Agencies such as USAID and FAO have partnered with local municipalities to install solar-powered micro cold storages in rural areas. In 2023, over 20 pilot units were operational, benefiting smallholder farmers in Kampong Cham and Prey Veng by reducing post-harvest losses by up to 15%.

Cambodia Cold Chain Market Segmentation

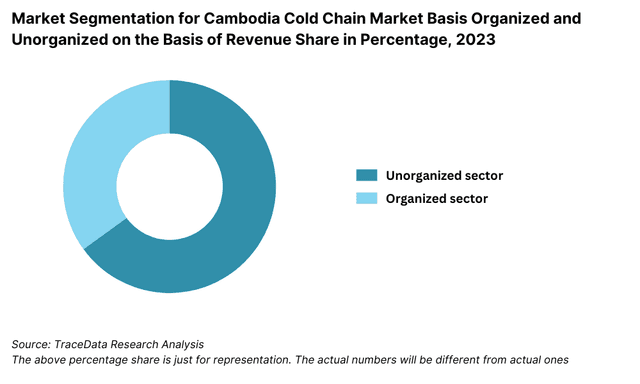

By Market Structure: The unorganized sector continues to dominate the market due to the widespread presence of small-scale operators, basic infrastructure, and cost competitiveness. These players often operate in regional clusters with limited compliance and serve domestic demand with basic refrigeration units. The organized segment, although smaller, is growing steadily due to the entry of international logistics firms and growing compliance needs from exporters and pharmaceutical companies. These players provide integrated cold storage and transportation services, real-time monitoring, and regulatory certifications.

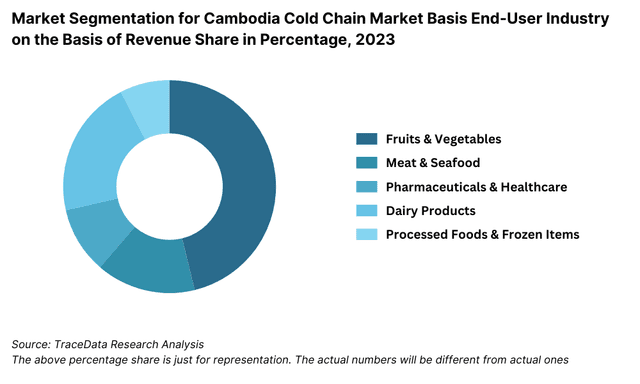

By End-User Industry: Fruits and vegetables lead the demand in the cold chain market, largely driven by Cambodia’s export of mangoes, bananas, and longans. These products require temperature-controlled handling from farms to export terminals. Meat and seafood follow due to high domestic consumption and exports to neighboring countries. Pharmaceutical products, including vaccines and biologics, are a fast-growing segment due to the rising healthcare demand and government emphasis on quality logistics. Dairy products are also gaining share with the rise in demand for processed and fresh dairy in urban regions.

By Temperature Type: The chilled segment dominates the market, primarily catering to fresh produce, dairy, and certain pharmaceutical items. Chilled storage and transport offer short- to medium-term preservation at temperatures between 0°C and 5°C. The frozen segment is used for seafood, meat, and long-term storage pharmaceuticals and operates below -18°C. Both segments are critical for Cambodia’s export supply chain and are being increasingly adopted across organized logistics networks.

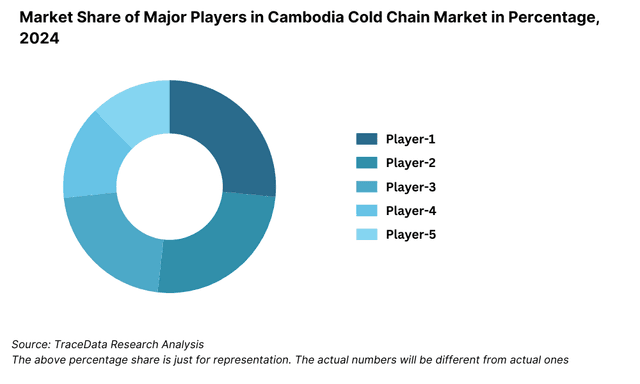

Competitive Landscape in Cambodia Cold Chain Market

The Cambodia cold chain market is moderately concentrated, with a mix of regional operators and multinational logistics companies. The entry of foreign players and development-focused PPPs have expanded the market, providing integrated services in storage, handling, and transport. Key players include Phnom Penh Cold Storage, Cambodia Cold Chain Logistics, Linfox, DHL Cambodia, Mekong Express, and VIBRA Cold Chain Services.

Company | Establishment Year | Headquarters |

Phnom Penh Cold Storage | 2008 | Phnom Penh, Cambodia |

Cambodia Cold Chain Logistics | 2014 | Phnom Penh, Cambodia |

Linfox | 1956 | Melbourne, Australia |

DHL Cambodia | 2002 | Phnom Penh, Cambodia |

Mekong Express | 2001 | Phnom Penh, Cambodia |

VIBRA Cold Chain Services | 2019 | Phnom Penh, Cambodia |

Some of the recent competitor trends and key information about competitors include:

Phnom Penh Cold Storage: One of the earliest dedicated cold storage providers in Cambodia, Phnom Penh Cold Storage expanded its warehouse capacity by 20% in 2023. It now offers advanced temperature monitoring and HACCP-certified services, serving clients in the agriculture, seafood, and pharmaceutical sectors.

Cambodia Cold Chain Logistics: A domestic logistics provider focused on the food and beverage sector, the company introduced hybrid cold transport vehicles in 2023 to reduce energy consumption. It has increased its service coverage to Battambang and Siem Reap.

Linfox: A major regional logistics player, Linfox invested in building a new 10,000-pallet cold storage facility in Phnom Penh in 2023. The company services multinational clients and adheres to international compliance protocols, making it a preferred partner for pharma and FMCG firms.

DHL Cambodia: Specializing in temperature-sensitive logistics, DHL introduced GDP-compliant packaging and tracking solutions in Cambodia in 2023. The company supports vaccine imports and pharmaceutical distribution across 10 provinces, contributing to over 12% of organized cold chain volume.

Mekong Express: Traditionally a passenger transport firm, Mekong Express diversified into perishable freight in 2022. Its adoption of refrigerated vans for fresh food delivery to supermarkets and hotels has helped it capture urban market share in Phnom Penh and Siem Reap.

VIBRA Cold Chain Services: A newer entrant, VIBRA focuses on end-to-end cold logistics for agricultural cooperatives and exporters. In 2023, it launched a solar-powered mini-cold storage pilot project in Prey Veng to reduce post-harvest losses and improve rural cold chain access.

What Lies Ahead for Cambodia Cold Chain Market?

The Cambodia cold chain market is projected to grow steadily by 2029, exhibiting a strong CAGR during the forecast period. This growth will be driven by rising exports of perishables, healthcare sector modernization, infrastructure investment, and rising private-public partnerships in rural logistics.

Expansion of Agri-Export-Oriented Infrastructure: Cambodia is expected to see increased investment in cold chain infrastructure to support its export of fruits and vegetables to China, Korea, and the EU. As more agribusinesses seek certifications and compliance, there will be greater demand for cold storage and temperature-controlled logistics, especially in provinces such as Battambang, Kampong Thom, and Siem Reap.

Pharma and Vaccine Distribution Growth: With growing healthcare investments and rising demand for biologics and vaccines, the pharmaceutical cold chain segment will expand significantly. This includes the adoption of Good Distribution Practice (GDP) compliance and real-time temperature tracking technologies, particularly for vaccine distribution across rural clinics and health centers.

Adoption of Technology and Automation: The integration of IoT-enabled temperature monitoring, warehouse automation, and route optimization software will become more widespread. These technologies are expected to reduce spoilage, enhance operational efficiency, and support compliance with international export standards, particularly important for perishable goods exporters.

Rural Cold Chain Penetration via Solar Solutions: Driven by support from development agencies and international donors, the market will witness the scaling up of solar-powered micro cold storages in remote farming communities. These solutions are cost-effective and help reduce post-harvest losses, supporting inclusive growth across the agricultural value chain.

%252C%25202024-2030.png&w=640&q=75)

Cambodia Cold Chain Market Segmentation

• By Market Structure:

o Cold Storage

o Cold Transportation

o Integrated Cold Chain Services

o Organized Sector

o Unorganized Sector

• By End-User Industry:

o Fruits & Vegetables

o Meat & Seafood

o Dairy Products

o Pharmaceuticals

o Processed Foods

o Quick Service Restaurants (QSRs)

• By Temperature Type:

o Chilled (0°C to 5°C)

o Frozen (Below -18°C)

o Ambient Controlled

• By Ownership Model:

o 3PL Cold Chain Operators

o Captive In-house Cold Chain

o Government/PPP Operated Facilities

• By Region:

o Phnom Penh

o Sihanoukville

o Siem Reap

o Battambang

o Kampong Cham

o Others (Takeo, Kampong Thom, Prey Veng)

Players Mentioned in the Report:

• Phnom Penh Cold Storage

• Cambodia Cold Chain Logistics

• Linfox

• DHL Cambodia

• Mekong Express

• VIBRA Cold Chain Services

• Khmer Cold Logistics

• Cambodian Fresh Supply Chain Alliance

Key Target Audience:

• Cold Storage Operators

• Cold Chain Logistics and Transportation Firms

• Agribusiness Exporters

• Pharmaceutical and Biologics Distributors

• Retail Chains and Supermarkets

• Government Agencies and Regulatory Bodies (e.g., Ministry of Commerce, MAFF, Ministry of Health)

• International Donor and Development Organizations (e.g., USAID, ADB, GIZ)

• Investors and Infrastructure Developers

Time Period:

• Historical Period: 2018-2023

• Base Year: 2024

• Forecast Period: 2024-2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-“ Role of Entities, Stakeholders, and Challenges They Face

4.2. Revenue Streams for Cambodia Cold Chain Market

4.3. Business Model Canvas for Cambodia Cold Chain Market

4.4. Cold Chain Service Decision-Making Process (End-User Perspective)

4.5. Supply Decision-Making Process (Service Provider Perspective)

5.1. Cold Chain Infrastructure Overview in Cambodia (Storage & Transport)

5.2. Organized vs. Unorganized Breakdown of Cold Chain Providers, 2023

5.3. Reefer Transport Availability by Province

5.4. Investment Trends in Cold Chain Infrastructure, 2018-“2024

8.1. Revenues, 2018-“2024

8.2. Cold Storage vs. Cold Transport Revenue Split, 2018-“2024

9.1. By Market Structure (Organized and Unorganized Market), 2023-“2024P

9.2. By End-User Industry (Fruits & Vegetables, Meat, Dairy, Pharma), 2023-“2024P

9.3. By Temperature Type (Chilled, Frozen), 2023-“2024P

9.4. By Ownership Model (3PL, Captive, PPP), 2023-“2024P

9.5. By Region (Phnom Penh, Sihanoukville, Siem Reap, Others), 2023-“2024P

10.1. Customer Landscape and Sector-Wise Requirements

10.2. Export-Driven Cold Chain Demand

10.3. Pain Points, Expectations, and Service Gaps

10.4. Gap Analysis Framework

11.1. Trends and Developments for Cambodia Cold Chain Market

11.2. Growth Drivers for Cambodia Cold Chain Market

11.3. SWOT Analysis for Cambodia Cold Chain Market

11.4. Issues and Challenges for Cambodia Cold Chain Market

11.5. Government Regulations for Cambodia Cold Chain Market

12.1. Micro Cold Storage Projects and Impact

12.2. Public-Private Partnership (PPP) Models

12.3. Development Agency Interventions (USAID, GIZ, ADB)

13.1. Funding Trends in Cold Chain Infrastructure, 2018-“2024

13.2. Tax Incentives, FDI Trends, and Government Subsidies

13.3. Cost Structure Benchmarking

16.1. Benchmark of Key Competitors in Cambodia Cold Chain Market Including Variables such as Company Overview, USP, Business Strategies, Strength, Weakness, Business Model, Market Coverage, Certifications, Cold Storage Capacity, Cold Transport Fleet Size

16.2. Strength and Weakness

16.3. Operating Model Analysis Framework

16.4. Gartner Magic Quadrant

16.5. Bowmans Strategic Clock for Competitive Advantage

17.1. Revenues, 2025-“2029

17.2. Cold Storage vs. Cold Transport Revenue Split, 2025-“2029

18.1. By Market Structure (Organized and Unorganized Market), 2025-“2029

18.2. By End-User Industry (Fruits & Vegetables, Meat, Dairy, Pharma), 2025-“2029

18.3. By Temperature Type (Chilled, Frozen), 2025-“2029

18.4. By Ownership Model (3PL, Captive, PPP), 2025-“2029

18.5. By Region (Phnom Penh, Sihanoukville, Siem Reap, Others), 2025-“2029

18.6. Recommendation

18.7. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand side and supply side entities for Cambodia Cold Chain Market. Basis this ecosystem, we will shortlist leading 5–6 players in the country based on their storage/transport capacity, service coverage, sectoral focus (e.g., pharma, agri-export), and financial or operational scale.

Sourcing is made through industry articles, government documents, association reports, and proprietary databases to perform desk research around the market to collate industry-level information.

Step 2: Desk Research

Subsequently, we engage in an exhaustive desk research process by referencing diverse secondary and proprietary databases. This approach enables us to conduct a thorough analysis of the market, aggregating industry-level insights. We delve into aspects like revenue by segment (storage vs. transport), regional infrastructure availability, demand drivers across end-user industries, and service pricing benchmarks.

This is supplemented with detailed examinations of company-level data, relying on sources like press releases, government tenders, logistics trade reports, NGO impact assessments, and media coverage. This process helps build a baseline understanding of the industry’s evolution, capacity, and competitive positioning.

Step 3: Primary Research

We initiate a series of in-depth interviews with C-level executives and operations heads from Cambodia-based cold chain logistics firms, exporters, agribusiness leaders, pharmaceutical distributors, and government officials. The interview process is aimed at validating our hypotheses, authenticating macro- and micro-level data, and extracting strategic insights related to capacity utilization, infrastructure gaps, cost structures, and compliance levels.

As part of our validation strategy, our team executes disguised interviews wherein we approach select companies as prospective clients or partners. This allows us to validate the service offerings, pricing models, certifications, and operational workflows shared during expert interviews. These interactions also help uncover informal trends and ground-level operational challenges.

Step 4: Sanity Check

- Bottom to top and top to bottom analysis along with cold chain revenue modeling exercises is undertaken to assess sanity check process. We align demand estimates from end-user sectors (agriculture, pharma, dairy, etc.) with existing infrastructure and transport availability to ensure logical alignment of forecasts and current capacity.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Cambodia cold chain market is expected to witness robust growth, reaching a valuation of USD 210 Million in 2023. This growth is fueled by the increasing demand for temperature-sensitive logistics, especially in the agriculture, pharmaceutical, and food processing sectors. The market's potential is further enhanced by export-driven opportunities, rising urbanization, and international investments in infrastructure and capacity development.

The Cambodia Cold Chain Market features several key players including Phnom Penh Cold Storage, Cambodia Cold Chain Logistics, and Linfox. These companies dominate the organized sector due to their reliable service networks, compliance capabilities, and established client base. Other notable players include DHL Cambodia, Mekong Express, and VIBRA Cold Chain Services.

Key growth drivers include increasing demand for agri-exports (mangoes, bananas, seafood), expanding healthcare and vaccine distribution needs, and the emergence of organized retail and e-commerce. Government policies, FDI incentives, and the deployment of solar-powered rural cold storages have also played a major role in market development.

The Cambodia Cold Chain Market faces several challenges including high energy costs, limited skilled workforce, and poor last-mile connectivity in rural areas. Infrastructure fragmentation and a largely unorganized service provider base contribute to inefficiencies. Additionally, a lack of standardization and compliance among small players remains a key barrier to scaling up quality cold chain services.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0