Chile Cold Chain Market Outlook to 2029

By Type (Cold Storage and Cold Transport), By Application (Dairy, Fruits & Vegetables, Meat & Seafood, Pharmaceuticals), By Temperature Type (Chilled and Frozen), By Region (Northern, Central, and Southern Chile)

Report Overview

Report Code

TDR0261

Coverage

Central and South America

Published

September 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Chile Cold Chain Market Outlook to 2029 – By Type (Cold Storage and Cold Transport), By Application (Dairy, Fruits & Vegetables, Meat & Seafood, Pharmaceuticals), By Temperature Type (Chilled and Frozen), By Region (Northern, Central, and Southern Chile)” provides a comprehensive analysis of the cold chain industry in Chile. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation, trends and developments, regulatory framework, customer-level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the...

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Chile Cold Chain Market Outlook to 2029 – By Type (Cold Storage and Cold Transport), By Application (Dairy, Fruits & Vegetables, Meat & Seafood, Pharmaceuticals), By Temperature Type (Chilled and Frozen), By Region (Northern, Central, and Southern Chile)” provides a comprehensive analysis of the cold chain industry in Chile. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation, trends and developments, regulatory framework, customer-level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the Cold Chain Market. The report concludes with future market projections based on revenue, by service type, application, temperature, region, and success case studies highlighting the major opportunities and key risk factors.

Chile Cold Chain Market Overview and Size

The Chile cold chain market reached a valuation of USD 2.5 billion in 2023, driven by growing demand for fresh and frozen food, increasing exports of perishables, and rising pharmaceutical logistics needs. Major players include Frigorífico Simunovic, Emergent Cold LatAm, Friosan, and Transportes Flores. These companies have built robust infrastructure in warehousing and temperature-controlled transport services across the country.

In 2023, Emergent Cold LatAm announced expansion in Santiago, adding new cold storage facilities to meet rising demand in the Central region. Southern Chile, with its strong seafood export base, is emerging as a key logistics hub.

%252C%25202019-2024.png&w=640&q=75)

What Factors are Leading to the Growth of Chile Cold Chain Market:

Export-Oriented Economy: Chile is one of the top exporters of seafood, fruits, and vegetables, requiring robust cold chain infrastructure. In 2023, fresh fruit exports alone crossed USD 5.8 billion, contributing significantly to cold logistics demand. Exporters rely on temperature-controlled facilities to preserve quality and comply with international standards.

Rising Urban Consumption of Perishables: With increased urbanization and shifting dietary preferences toward fresh and ready-to-cook meals, demand for cold chain services has surged in urban centers such as Santiago, Valparaíso, and Concepción. Chilean retail and e-grocery channels are expanding their cold chain needs, especially in chilled dairy and meat categories.

Pharma and Vaccine Logistics: The pharmaceutical sector, including vaccine distribution, has emerged as a key segment post-COVID-19. In 2023, pharma logistics contributed over 12% to the overall cold chain market, driven by regulatory compliance and rising healthcare needs in remote regions.

Which Industry Challenges Have Impacted the Growth for Chile Cold Chain Market

Infrastructure Gaps in Remote Regions: Despite advancements in urban areas, cold chain infrastructure in remote and southern regions of Chile remains underdeveloped. According to TraceData estimates, nearly 30% of perishable goods transported to rural zones face spoilage risks due to lack of temperature-controlled last-mile facilities. This weak infrastructure continues to hinder efficient distribution and increases post-harvest losses.

High Operational Costs: The cost of energy, refrigeration equipment, and skilled labor significantly elevates operating expenses in Chile’s cold chain market. In 2023, energy consumption for cold storage contributed nearly 20% to total operating costs, pushing smaller operators to the brink of unviability. These high costs are a critical constraint on scalability, particularly for SMEs and regional players.

Skilled Workforce Shortage: The industry faces a talent gap in skilled refrigeration technicians, warehouse operators, and compliance managers. A national logistics workforce survey revealed that 42% of cold chain companies in Chile struggle to fill key technical roles, impacting service quality and uptime of refrigerated systems.

What are the Regulations and Initiatives which have Governed the Market:

Sanitary and Quality Control Regulations (SAG): The Chilean Agriculture and Livestock Service (SAG) imposes strict quality control for exportable perishables, requiring specific temperature handling protocols and HACCP certifications. In 2023, over 85% of fresh fruit exporters were certified under SAG’s cold chain compliance framework, ensuring global competitiveness and reduced rejection rates.

Cold Chain Standards for Pharma Logistics: The Ministry of Health mandates GDP (Good Distribution Practices) for temperature-sensitive pharmaceuticals, including vaccines and biologics. All pharmaceutical distributors must use validated cold chain equipment and maintain detailed temperature logs. By end-2023, nearly 70% of licensed pharma transporters were GDP-compliant.

Port Logistics Modernization Programs: The Chilean government has invested in modernizing cold storage infrastructure at major ports like San Antonio and Valparaíso. In 2023, a USD 40 million public-private partnership expanded reefer container capacity by 18%, significantly reducing bottlenecks for perishable exports.

Chile Cold Chain Market Segmentation

By Type of Service: Cold storage facilities account for a major share of the market due to Chile’s strong export dependency on perishable goods like fruits and seafood, which require long-term storage before shipping. These warehouses are often located near ports such as San Antonio and Valparaíso. Cold transportation services are also growing, driven by rising demand for last-mile refrigerated logistics, especially for pharma and dairy products. Fleet modernization with reefer trucks and containers is helping to boost reliability and market share.

%2520on%2520the%2520Basis%2520of%2520Revenue%2520Share%2520in%2520Percentage%252C%25202023.png&w=640&q=75)

By Application: Fruits and vegetables lead the application segment due to Chile’s prominent position as a global exporter, especially of grapes, apples, and cherries. Meat and seafood follow, supported by strong aquaculture and livestock production in the southern region. Pharmaceutical logistics is a rapidly emerging segment, with growth driven by vaccine distribution and rising regulatory standards for temperature-sensitive medications.

%2520on%2520the%2520Basis%2520of%2520Revenue%2520Share%2520in%2520Percentage%252C%25202023.png&w=640&q=75)

By Temperature Type: Frozen storage and transportation dominate the market, especially in the meat and seafood category, which require sub-zero preservation. Chilled segment usage is prominent for dairy, fruits, vegetables, and pharma products that need 2°C to 8°C storage. With growing consumption of fresh food and pharma regulations, the chilled segment is expected to witness faster growth over the next few years.

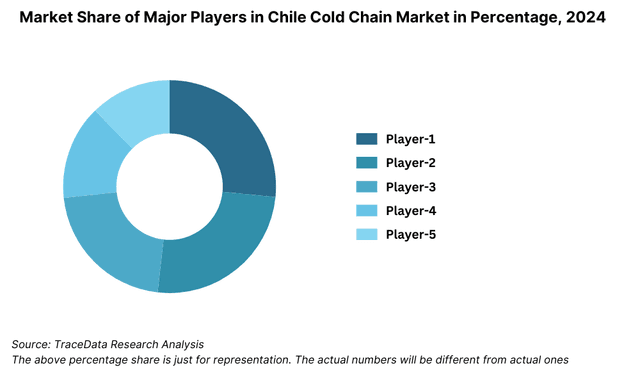

Competitive Landscape in Chile Cold Chain Market

The Chile cold chain market is moderately concentrated, with a mix of established logistics providers and emerging regional players. Major players such as Emergent Cold LatAm, Frigorífico Simunovic, Friosan, Transportes Flores, and Andes Logistics dominate due to their strong infrastructure, strategic locations near ports, and compliance with international cold chain standards. However, local and specialized firms are gaining traction by focusing on niche segments such as pharmaceutical distribution and seafood logistics.

Company | Establishment Year | Headquarters |

Emergent Cold LatAm | 2021 | Santiago, Chile |

Frigorífico Simunovic | 1960 | Punta Arenas, Chile |

Friosan | 1994 | Santiago, Chile |

Transportes Flores | 1988 | Valparaíso, Chile |

Andes Logistics | 2005 | Santiago, Chile |

Some of the recent competitor trends and key information about competitors include:

Emergent Cold LatAm: A major player in the Latin American cold storage sector, Emergent Cold expanded its Chilean footprint in 2023 by adding 12,000 pallet positions in a new cold facility in Santiago. The company focuses on integrated cold storage and transport solutions, especially for exports via Valparaíso and San Antonio ports.

Frigorífico Simunovic: With a stronghold in southern Chile, this company specializes in seafood storage and processing. In 2023, it handled over 20% of frozen fish logistics volume in the Magallanes region, reinforcing its dominance in the seafood cold chain.

Friosan: A key mid-sized player, Friosan operates temperature-controlled warehouses in the Central region. In 2023, the company introduced an advanced temperature monitoring system that reduced spoilage rates by 18% for fruits and vegetables.

Transportes Flores: Known for its nationwide cold transport fleet, the company reported a 22% increase in demand from pharmaceutical clients in 2023. The company recently partnered with a Santiago-based vaccine distributor to enhance its pharma cold chain coverage.

Andes Logistics: Focused on multimodal logistics for perishable exports, Andes Logistics reported a 30% YoY growth in refrigerated container services. Their strategic alliances with port authorities and exporters have positioned them as a preferred partner for fruit exporters.

What Lies Ahead for Chile Cold Chain Market?

The Chile cold chain market is projected to experience steady growth through 2029, driven by rising demand for perishable exports, expanding urban cold storage infrastructure, and stricter regulatory compliance for pharmaceuticals and food safety. The market is expected to register a healthy CAGR, supported by both domestic consumption trends and international trade demands.

Expansion of Export-Oriented Cold Storage: With continued growth in agricultural and seafood exports, there will be a significant rise in investment toward modern cold storage facilities near Chile’s major ports and agricultural hubs. The Central and Southern regions are likely to witness substantial infrastructure expansion to cater to seasonal surges in export volumes, especially for fruits and frozen fish.

Growth in Pharmaceutical Cold Chain: As healthcare standards evolve and access to specialty medicines and vaccines improves, the pharmaceutical segment of the cold chain will expand. By 2029, pharma logistics is expected to account for over 15% of total cold chain revenue in Chile, supported by the enforcement of Good Distribution Practices (GDP) and temperature-sensitive product regulations.

Digitalization and Real-Time Monitoring: Cold chain players are expected to increasingly integrate technologies such as IoT sensors, blockchain for traceability, and AI-based temperature optimization tools. These technologies will enhance product integrity, reduce losses, and increase operational transparency—key factors for exporters and pharma distributors alike.

Sustainability and Energy Efficiency Initiatives: With rising energy costs and environmental concerns, the Chilean cold chain industry is moving toward greener practices. The use of solar-powered refrigeration units, energy-efficient warehouses, and hybrid transport fleets is projected to rise. By 2029, nearly 25% of new cold storage capacity is expected to incorporate sustainable design standards and green certifications.

%252C%25202024-2030.png&w=640&q=75)

Chile Cold Chain Market Segmentation

By Type of Service:

Cold Storage

Cold Transportation

Integrated Cold Chain Solutions

By Application:

Fruits & Vegetables

Meat & Seafood

Dairy Products

Pharmaceuticals

Processed Foods

By Temperature Type:

Chilled (2°C to 8°C)

Frozen (Below 0°C)

By Type of Transport Mode:

Reefer Trucks

Refrigerated Containers (Reefer Containers)

Air Freight Cold Chain

Rail-Based Cold Logistics

By Type of Storage Facility:

Public Cold Storage

Private Warehouses

Contract Warehousing

By Ownership Type:

Third-Party Logistics (3PL) Providers

In-House Logistics Providers

By Region:

Northern Chile

Central Chile (including Santiago Metropolitan Region)

Southern Chile (including Biobío, Los Lagos, Magallanes)

Players Mentioned in the Report:

Emergent Cold LatAm

Frigorífico Simunovic

Friosan

Transportes Flores

Andes Logistics

Logística FríoSur

Friofort

Key Target Audience:

Cold Storage Providers

Refrigerated Transport Operators

Food Exporters and Agro-Processors

Pharmaceutical Distributors

Government Regulatory Bodies (e.g., SAG, Ministry of Health)

Port Authorities and Trade Bodies

Technology Providers for Cold Chain Monitoring

Investors and Infrastructure Funds

Time Period:

Historical Period: 2018–2023

Base Year: 2024

Forecast Period: 2024–2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-“ Role of Entities, Stakeholders, and Challenges They Face

4.2. Revenue Streams for Chile Cold Chain Market

4.3. Business Model Canvas for Chile Cold Chain Market

4.4. Product Flow and Cold Chain Integration in Export Supply Chain

4.5. Logistics Partner Selection Process

5.1. Cold Storage Capacity in Chile, 2018-“2024

5.2. Cold Transport Fleet Size and Utilization, 2018-“2024

5.3. Cold Chain Dependency by Sector (Fruits, Seafood, Pharma, etc.)

5.4. Distribution of Cold Chain Warehouses by Region

8.1. Revenues, 2018-“2024

8.2. Cold Storage Volume (in pallet positions), 2018-“2024

8.3. Cold Transport Volume (in MT/km), 2018-“2024

9.1. By Type of Service (Cold Storage, Cold Transport), 2023-“2024P

9.2. By Application (Fruits & Vegetables, Meat & Seafood, Dairy, Pharma), 2023-“2024P

9.3. By Temperature Type (Frozen and Chilled), 2023-“2024P

9.4. By Type of Transport (Truck, Rail, Reefer Container, Air), 2023-“2024P

9.5. By Ownership Model (3PL vs. In-house), 2023-“2024P

9.6. By Region (Northern, Central, Southern Chile), 2023-“2024P

10.1. Customer Segments and Use Cases

10.2. Buyer Journey and Procurement Decision Process

10.3. Pain Points and Unmet Needs

10.4. Gap Analysis Framework

11.1. Trends and Developments in Chile Cold Chain Market

11.2. Growth Drivers for Chile Cold Chain Market

11.3. SWOT Analysis for Chile Cold Chain Market

11.4. Issues and Challenges in the Chile Cold Chain Ecosystem

11.5. Government Regulations and Compliance Requirements

12.1. Cold Chain in Fruit and Seafood Exports (Volume, Dependency, Losses)

12.2. Business Model and Integration in Export Value Chain

12.3. Port Infrastructure and Reefer Container Usage by Port

13.1. Pharma Cold Chain Requirements and Compliance (GDP Standards)

13.2. Market Size and Dependency by Region

13.3. Key Challenges and Innovations in Pharma Logistics

16.1. Benchmark of Key Competitors-“ Company Overview, USP, Services Offered, Revenue, Fleet, Storage, Expansion Plans

16.2. Strengths and Weaknesses

16.3. Operating Model Analysis Framework

16.4. Bowmans Strategic Clock for Competitive Advantage

17.1. Revenues, 2025-“2029

17.2. Cold Storage Capacity and Utilization Forecast, 2025-“2029

17.3. Cold Transport Volume and Fleet Forecast, 2025-“2029

18.1. By Type of Service (Cold Storage and Transport), 2025-“2029

18.2. By Application, 2025-“2029

18.3. By Temperature Type, 2025-“2029

18.4. By Transport Mode, 2025-“2029

18.5. By Region, 2025-“2029

18.6. By Ownership Model, 2025-“2029

18.7. Recommendation

18.8. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities for the Chile Cold Chain Market. Based on this ecosystem, we shortlist 5–6 leading service providers in the country using parameters such as storage capacity, fleet size, service coverage, and financial strength.

Sourcing is carried out through government databases, port authority data, industry articles, company websites, and proprietary research databases to perform desk research and build a comprehensive industry-level understanding.

Step 2: Desk Research

We conduct extensive secondary research referencing public and proprietary databases. This step includes analysis of logistics infrastructure, cold storage and transport capacity, service distribution by region, and key sectoral applications such as food exports, seafood, dairy, and pharmaceuticals.

Data points such as cold storage capacity (in cubic meters/pallet positions), refrigerated truck numbers, regional market shares, and export cold chain dependency are analyzed. We supplement this with company-level data such as press releases, annual reports, expansion announcements, and infrastructure investments.

Step 3: Primary Research

In-depth interviews are conducted with key stakeholders across the Chile cold chain ecosystem, including senior executives from cold storage companies, refrigerated transport providers, food exporters, pharmaceutical distributors, and port authorities.

These interviews help validate our desk findings, authenticate market size estimates, and extract insights on operational models, pricing strategies, challenges, and upcoming investments.

A bottom-up approach is adopted to calculate storage and transport capacity utilization, which is then aggregated to estimate total market size and service segmentation.

Disguised interviews are also carried out with logistics firms and freight forwarders under the pretense of being potential customers, to validate utilization rates, pricing benchmarks, value-added service offerings, and client servicing models.

Step 4: Sanity Check

- Both top-down and bottom-up methodologies are applied to triangulate the findings. Cold storage capacity by region, refrigerated transport volume, and segment-wise demand (e.g., fruits, seafood, pharma) are modeled to validate final market sizing. Final estimates are corroborated through independent validations with export data, Ministry of Health compliance statistics, and SAG (Servicio Agrícola y Ganadero) reports on cold chain certifications.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Chile cold chain market holds significant growth potential, reaching a valuation of USD 2.5 billion in 2023. This growth is driven by rising exports of perishables such as fruits, seafood, and dairy, along with expanding demand for temperature-controlled pharmaceutical logistics. The market is further supported by infrastructure investments, government regulatory support, and the adoption of digital cold chain technologies.

Key players in the Chile Cold Chain Market include Emergent Cold LatAm, Frigorífico Simunovic, Friosan, Transportes Flores, and Andes Logistics. These companies dominate the market due to their strong infrastructure, strategic port-based facilities, and expertise in cold storage and refrigerated transportation. Emerging regional players are also gaining ground through service specialization in pharma and fresh produce.

The primary growth drivers include Chile’s strong position as a global exporter of fresh produce and seafood, rising urban consumption of perishable foods, and growing demand for pharmaceutical cold logistics. In addition, government investment in port and logistics infrastructure, and the shift toward sustainable and tech-enabled cold chain solutions, are fueling market expansion.

Key challenges include infrastructure gaps in rural and remote areas, high operational and energy costs, and a shortage of skilled labor for cold chain operations. Additionally, compliance with stringent food safety and pharma regulations requires significant investment in technology and monitoring systems, which can be a barrier for smaller operators.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0