Colombia Logistics and warehousing Market Outlook to 2029

By Market Structure, By Type of Services, By End Users, By Mode of Transport, By Ownership, and By Region

Report Overview

Report Code

TDR0263

Coverage

Central and South America

Published

September 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Colombia Logistics and Warehousing Market Outlook to 2029 – By Market Structure, By Type of Services, By End Users, By Mode of Transport, By Ownership, and By Region” provides a comprehensive analysis of the logistics and warehousing market in Colombia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer-level profiling, issues and challenges, and comparative landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the logistics and warehousing industry.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Colombia Logistics and Warehousing Market Outlook to 2029 – By Market Structure, By Type of Services, By End Users, By Mode of Transport, By Ownership, and By Region” provides a comprehensive analysis of the logistics and warehousing market in Colombia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer-level profiling, issues and challenges, and comparative landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the logistics and warehousing industry. The report concludes with future market projections based on revenue, by segment, transport modes, regional dynamics, cause-and-effect relationships, and success case studies highlighting key opportunities and strategic cautions.

Colombia Logistics and Warehousing Market Overview and Size

The Colombia logistics and warehousing market reached a valuation of COP 38 Trillion in 2023, driven by increasing e-commerce penetration, growing demand for efficient last-mile delivery, and infrastructure improvements across major cities. The industry is characterized by leading players such as Servientrega, Coordinadora, DHL, TCC, and Kuehne + Nagel, which offer integrated logistics, freight forwarding, warehousing, and express delivery services.

In 2023, Coordinadora invested in expanding its distribution center capacity in Bogotá and Medellín to handle increasing parcel volumes, especially from the booming e-commerce sector. Bogotá, Medellín, and Cali are the primary logistics hubs, owing to their dense urban population and growing industrial activity.

%252C%25202019-2024.png&w=640&q=75)

What Factors are Leading to the Growth of the Colombia Logistics and Warehousing Market:

Infrastructure Development: Significant investment in highway and port infrastructure under Colombia’s 4G and 5G infrastructure programs has enhanced regional connectivity. Over COP 75 trillion has been allocated to logistics corridors, improving freight efficiency and reducing turnaround time.

E-commerce Boom: Colombia’s e-commerce market grew at a CAGR of 25% from 2020 to 2023. This growth has created massive demand for logistics services, especially last-mile delivery, fulfillment centers, and temperature-controlled logistics.

Trade Agreements and Nearshoring: Colombia's strategic location and multiple trade agreements (e.g., Pacific Alliance, Andean Community) have made it a hub for regional distribution. The global shift toward nearshoring has also attracted warehousing and distribution operations from North American companies.

Which Industry Challenges Have Impacted the Growth for Colombia Logistics and Warehousing Market

Inadequate Infrastructure in Remote Areas: While major cities have seen infrastructure upgrades, rural and remote regions still suffer from poor road quality, limited connectivity, and lack of multimodal transport options. According to the Colombian Logistics Observatory, approximately 30% of logistics delays in 2023 were caused by underdeveloped infrastructure in secondary and tertiary routes, hindering national supply chain efficiency.

Security and Cargo Theft: Cargo theft remains a serious issue, especially along key highways connecting Bogotá, Barranquilla, and Buenaventura. Industry reports indicate that 1 in every 100 shipments faced some form of theft or tampering in 2023, particularly affecting high-value goods such as electronics and pharmaceuticals. This raises insurance costs and deters foreign logistics operators.

Bureaucratic Bottlenecks and Customs Delays: Despite trade liberalization efforts, customs clearance remains slow and cumbersome at ports and borders. In 2023, average customs processing time at the Port of Buenaventura was 72 hours—almost double that of regional benchmarks like Panama. These delays negatively impact international trade flow and increase demurrage charges.

What are the Regulations and Initiatives which have Governed the Market

National Logistics Policy (PNLogística): The Colombian government launched the PNLogística to modernize the country’s logistics framework by 2030. It focuses on digitizing logistics operations, developing intermodal corridors, and improving customs clearance systems. As of 2023, 6 out of 11 strategic logistics corridors were under active development.

4G and 5G Infrastructure Programs: These nationwide programs aim to enhance logistics connectivity through public-private partnerships. Over USD 25 billion has been allocated to road expansions, tunnel construction, and port modernization. In 2023, three major 4G highway projects were completed, significantly reducing freight time between Bogotá and Medellín by up to 30%.

Free Trade Zones and Tax Incentives: Colombia offers over 110 free trade zones with customs and tax benefits to promote warehousing and distribution activities. In 2023, warehousing space in FTZs grew by 18%, supported by government-led investment promotion and tax reliefs for logistics operators.

Colombia Logistics and Warehousing Market Segmentation

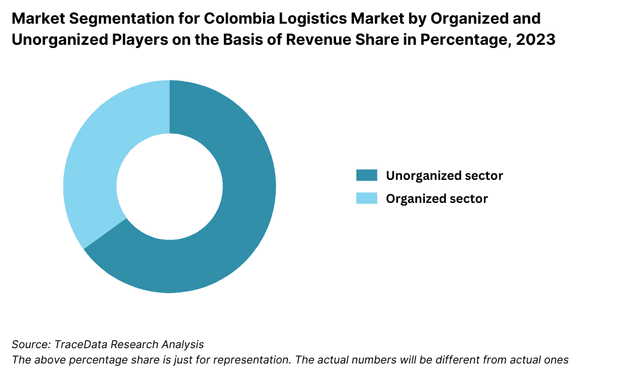

By Market Structure: The logistics market in Colombia is primarily fragmented with a large share held by unorganized and small regional players, particularly in last-mile delivery and intra-city freight. These firms are popular in tier-2 and tier-3 cities due to their localized reach, flexible operations, and cost competitiveness. On the other hand, organized players like DHL, Coordinadora, and Kuehne + Nagel dominate high-value segments such as international freight forwarding, e-commerce fulfillment, and industrial warehousing, especially in urban and port-connected areas. Their technological capabilities, integrated supply chain offerings, and compliance with international standards attract large corporates and exporters.

By Type of Services: Transportation services account for the largest share of the logistics sector, driven by Colombia’s growing domestic trade and road-reliant freight system. Warehousing services have expanded rapidly in response to rising e-commerce, pharmaceuticals, and FMCG demand, particularly around Bogotá and Medellín. Value-added services (e.g., packaging, labeling, reverse logistics) are gaining momentum among retailers and D2C brands looking to outsource complex operations.

%2520on%2520the%2520Basis%2520of%2520Revenue%2520Share%2520in%2520Percentage%252C%25202023.png&w=640&q=75)

By End User Industry: E-commerce and retail are the dominant end-use segments, fueled by Colombia’s growing digital economy and consumer demand for fast delivery. FMCG and pharmaceuticals also contribute significantly due to their time-sensitive and high-volume logistics requirements. Manufacturing, including automotive and electronics, relies on 3PL and 4PL services for nationwide distribution.

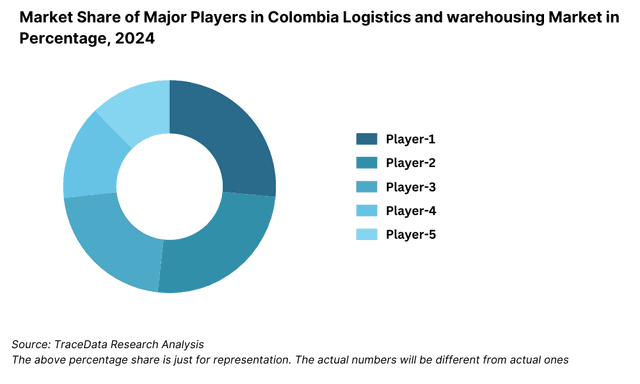

Competitive Landscape in Colombia Logistics and Warehousing Market

The Colombia logistics and warehousing market is moderately consolidated, with a mix of international players and strong domestic logistics providers. The entry of digital-first logistics firms and e-commerce-focused delivery platforms has added dynamism to the market, giving businesses and consumers broader options in terms of services, pricing, and delivery timelines.

Company | Establishment Year | Headquarters |

Servientrega | 1982 | Bogotá, Colombia |

Coordinadora | 1982 | Medellín, Colombia |

TCC (Transportadora) | 1968 | Medellín, Colombia |

DHL Colombia | 1970 | Bogotá, Colombia |

Kuehne + Nagel | 1890 (Global) | Bogotá, Colombia |

Envía (Grupo Redex) | 2004 | Bogotá, Colombia |

Rappi Logistics | 2015 | Bogotá, Colombia |

Deprisa (Avianca) | 1995 | Bogotá, Colombia |

Some of the recent competitor trends and key information about competitors include:

Servientrega: As one of Colombia’s largest logistics firms, Servientrega handled over 120 million shipments in 2023, supported by a network of 6,000 service points across the country. Their expansion into real-time tracking and micro-fulfillment centers has improved service speed, especially in urban areas.

Coordinadora: With an extensive footprint across Colombia, Coordinadora reported a 19% year-on-year revenue growth in 2023, largely driven by increasing demand from retail and e-commerce clients. Their investments in cold chain logistics and automated warehousing have strengthened their B2B service offerings.

TCC: TCC is a trusted name for integrated logistics solutions including last-mile delivery, warehousing, and returns management. In 2023, they launched a new tech-driven logistics platform to centralize fleet and inventory tracking, improving efficiency across regional routes.

DHL Colombia: Operating both domestically and internationally, DHL has been a preferred partner for large enterprises. The company has expanded its warehousing capacity in Bogotá Free Trade Zone by 25% in 2023, focusing on high-value verticals such as healthcare and electronics.

Kuehne + Nagel: Known for its end-to-end international freight and warehousing services, Kuehne + Nagel introduced AI-powered demand forecasting for Colombian retail clients in 2023. This has helped reduce lead times and improve inventory accuracy.

Envía: With a strong emphasis on SME clients, Envía witnessed a 22% increase in deliveries in 2023, especially in tier-2 and tier-3 cities. The company’s affordable pricing and decentralized delivery model are key competitive advantages.

Rappi Logistics: Rappi has emerged as a major player in on-demand delivery logistics. In 2023, they launched a specialized warehousing and fulfillment service for D2C brands, targeting small businesses seeking to scale quickly with same-day delivery options.

Deprisa: A division of Avianca, Deprisa combines air freight and ground logistics, making it a leader in time-critical deliveries. In 2023, they expanded their aviation-linked delivery services to new cities, optimizing rapid parcel movement.

What Lies Ahead for Colombia Logistics and Warehousing Market?

The Colombia logistics and warehousing market is projected to grow steadily through 2029, with an anticipated CAGR of around 7–9% during the forecast period. This growth will be supported by rising domestic consumption, the expansion of digital retail, infrastructure upgrades, and Colombia's emergence as a regional logistics hub.

Expansion of E-commerce Logistics: The e-commerce sector is expected to continue driving demand for advanced logistics services such as rapid fulfillment, returns management, and last-mile delivery. Companies are likely to invest in hyperlocal warehouses and delivery optimization technologies to cater to rising customer expectations for speed and flexibility.

Rise of Multimodal and Intermodal Transport: With government efforts to improve rail and inland waterway infrastructure, Colombia is poised to shift a portion of cargo from road to more cost-efficient modes. The integration of multimodal transport will reduce logistics costs and carbon emissions, especially for heavy and bulk cargo over long distances.

Digital Logistics Ecosystem: Digital transformation will play a critical role in reshaping logistics operations. Widespread adoption of Transport Management Systems (TMS), Warehouse Management Systems (WMS), and real-time tracking tools will improve visibility, operational efficiency, and customer satisfaction across the supply chain.

Growth in Cold Chain and Specialized Warehousing: With increasing demand from sectors like pharmaceuticals, agri-exports, and food & beverage, Colombia is set to witness a surge in demand for temperature-controlled and specialized warehousing solutions. Investment in cold chain logistics is expected to grow by over 10% annually through 2029.

%252C%25202024-2030.png&w=640&q=75)

Colombia Logistics and Warehousing Market Segmentation

- By Market Structure:

o Organized Logistics Providers

o Unorganized & Regional Players

o Third-Party Logistics (3PL)

o Fourth-Party Logistics (4PL)

o Freight Forwarders

o Courier, Express & Parcel (CEP) Operators

o E-commerce Logistics Companies - By Type of Services:

o Transportation Services

o Warehousing Services

o Inventory Management

o Freight Forwarding

o Cold Chain Logistics

o Value-added Services (packaging, labeling, returns management) - By End User Industry:

o E-commerce

o FMCG

o Pharmaceuticals

o Retail

o Automotive

o Agriculture & Perishables

o Industrial & Manufacturing - By Mode of Transport:

o Road Freight

o Air Cargo

o Rail Freight

o Maritime Shipping - By Ownership of Warehousing:

o Owned Warehouses

o Leased Warehouses

o 3PL-Managed Warehousing - By Region:

o Bogotá Capital Region

o Antioquia (Medellín and surroundings)

o Valle del Cauca (Cali and surroundings)

o Caribbean Coast (Barranquilla, Cartagena, Santa Marta)

o Eastern Region

o Central Region

Players Mentioned in the Report:

- Servientrega

- Coordinadora

- TCC (Transportadora)

- DHL Colombia

- Kuehne + Nagel

- Envía (Grupo Redex)

- Rappi Logistics

- Deprisa (Avianca)

Key Target Audience:

- Logistics and Warehousing Companies

- E-commerce Companies

- Freight Forwarding and Transportation Firms

- Government and Regulatory Bodies (e.g., Ministry of Transport, DIAN)

- Investment and Infrastructure Development Agencies

- Industrial Park and Free Trade Zone Developers

- Cold Chain Solution Providers

- Research & Consulting Firms

Time Period:

- Historical Period: 2018–2023

- Base Year: 2024

- Forecast Period: 2024–2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-“ Role of Entities, Stakeholders, and Challenges They Face

4.2. Revenue Streams for Colombia Logistics and Warehousing Market

4.3. Business Model Canvas for Colombia Logistics Market

4.4. Demand Decision-Making Process

4.5. Supply Chain Planning and Execution

5.1. Logistics Spend in Colombia, 2018-“2024

5.2. Organized vs. Unorganized Logistics Providers, 2018-“2024

5.3. Intermodal Transport and Infrastructure Investments, 2024

5.4. Distribution of Warehousing Providers by Region

8.1. Revenues, 2018-“2024

8.2. Shipment Volume, 2018-“2024

9.1. By Market Structure (Organized and Unorganized), 2023-“2024P

9.2. By Type of Service (Transportation, Warehousing, Value-Added), 2023-“2024P

9.3. By End-User Industry (Retail, FMCG, Pharma, etc.), 2023-“2024P

9.4. By Mode of Transport (Road, Air, Rail, Sea), 2023-“2024P

9.5. By Ownership of Warehousing (Owned, Leased, 3PL Managed), 2023-“2024P

9.6. By Region (Bogotá, Antioquia, Valle del Cauca, etc.), 2023-“2024P

10.1. Client Segmentation and Usage Patterns

10.2. Customer Journey and Service Expectations

10.3. Logistics Requirements by Sector

10.4. Gap Analysis Framework

11.1. Trends and Developments in Colombia Logistics Market

11.2. Growth Drivers for Colombia Logistics and Warehousing Market

11.3. SWOT Analysis for Colombia Logistics Market

11.4. Challenges in the Colombia Logistics and Warehousing Ecosystem

11.5. Government Regulations and Incentives

12.1. Market Size and Growth in E-commerce Logistics, 2018-“2029

12.2. Role of Tech Platforms in Fulfillment and Delivery

12.3. Comparison of Key E-commerce Logistics Players in Colombia

13.1. Warehouse Stock Availability and Utilization Trends

13.2. Demand for Cold Chain Services Across Segments

13.3. Warehouse Classification (Grade A, B, C) and Vacancy Trends

13.4. Future Supply Pipeline and Investments

16.1. Benchmark of Key Players-“ Overview, Strategy, Strengths, Limitations, Network, Services, Technology Stack

16.2. Strengths and Weaknesses of Key Operators

16.3. Logistics Operating Model Analysis

16.4. Gartner Magic Quadrant View

16.5. Bowmans Strategic Clock for Positioning

17.1. Revenues, 2025-“2029

17.2. Shipment Volume, 2025-“2029

18.1. By Market Structure (Organized and Unorganized), 2025-“2029

18.2. By Type of Service (Transportation, Warehousing, etc.), 2025-“2029

18.3. By End-User Industry, 2025-“2029

18.4. By Region, 2025-“2029

18.5. By Mode of Transport, 2025-“2029

18.6. By Ownership Type, 2025-“2029

18.7. Recommendation

18.8. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities for the Colombia Logistics and Warehousing Market. Based on this ecosystem, we shortlist 5–6 leading logistics providers in the country, using metrics such as annual revenue, warehousing capacity, geographic coverage, and service portfolios.

Sourcing is done through industry articles, logistics association reports, proprietary databases, and government portals to perform initial desk research and collect high-level industry data.

Step 2: Desk Research

We then conduct exhaustive desk research leveraging both public and proprietary sources. This includes reviewing logistics industry white papers, government trade and infrastructure reports, port authority statistics, market databases, and trade publications.

Company-specific insights such as market share, fleet size, warehouse capacity, technology adoption, and revenue are gathered using annual reports, investor presentations, regulatory filings, and press releases. This allows us to build a baseline understanding of the market dynamics and the strategic positioning of key players.

Step 3: Primary Research

A structured primary research process is initiated via interviews with key stakeholders, including CXOs and senior managers of logistics companies, 3PL/4PL providers, warehousing operators, port authorities, industry experts, and large end-user companies (e.g., e-commerce, FMCG, manufacturing).

These interactions help validate hypotheses around market size, service demand, pricing, operating models, and infrastructure trends. We also conduct bottom-up volume estimations by aggregating data from regional logistics providers and clients.

Additionally, disguised interviews are conducted by approaching companies as potential clients. This technique helps verify operational claims, pricing structures, capacity availability, and service lead times in a more neutral setting.

Step 4: Sanity Check

- Sanity checks are performed using both top-down (macro-level logistics GDP share, trade flows, infrastructure spend) and bottom-up (provider-level volume and revenue aggregation) models to validate the robustness of estimates. This ensures that the final market sizing and forecasting align with real-world patterns and practical business conditions in Colombia.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Colombia logistics and warehousing market holds significant growth potential, with the sector valued at COP 38 Trillion in 2023 and projected to grow steadily through 2029. Key drivers include infrastructure development, rapid e-commerce growth, trade facilitation reforms, and Colombia’s strategic position for regional distribution. The expansion of urban consumption, improved digital connectivity, and public-private infrastructure investments further reinforce the market's long-term potential.

Major players in the Colombia market include Servientrega, Coordinadora, TCC, DHL Colombia, and Kuehne + Nagel. These companies lead due to their national and international networks, diversified service offerings (transportation, warehousing, last-mile delivery), and strong logistics infrastructure. Emerging players like Rappi Logistics and Envía are also disrupting the market through tech-enabled logistics and e-commerce partnerships.

Growth is driven by increasing e-commerce penetration, government investment in the 4G/5G infrastructure programs, the rise of consumer-centric logistics, and the adoption of advanced technologies like real-time tracking, warehouse automation, and digital fleet management. Additionally, Colombia’s growing trade agreements and nearshoring trends are positioning the country as a logistics gateway to Latin America.

The market faces challenges such as poor infrastructure in remote areas, high logistics costs (13–15% of product value), customs inefficiencies, and cargo security issues. Many logistics firms also operate with low technological penetration, particularly in the unorganized segment, limiting their scalability and efficiency. Addressing these challenges is crucial to unlocking the market’s full potential.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0