Greece Cold Chain Market Outlook to 2029

By Type of Temperature-Controlled Storage and Transport, By End-User Industry (Pharmaceuticals, Food and Beverage, Retail), By Type of Products, By Region, and By Ownership Type

Report Overview

Report Code

TDR0276

Coverage

Asia

Published

September 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Greece Cold Chain Market Outlook to 2029 - By Type of Temperature-Controlled Storage and Transport, By End-User Industry (Pharmaceuticals, Food and Beverage, Retail), By Type of Products, By Region, and By Ownership Type.” provides a comprehensive analysis of the cold chain industry in Greece. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; key trends and developments, regulatory framework, customer profiling, challenges, and comparative landscape including competitive scenario, cross comparisons, opportunities, and pain points.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Greece Cold Chain Market Outlook to 2029 - By Type of Temperature-Controlled Storage and Transport, By End-User Industry (Pharmaceuticals, Food and Beverage, Retail), By Type of Products, By Region, and By Ownership Type.” provides a comprehensive analysis of the cold chain industry in Greece. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; key trends and developments, regulatory framework, customer profiling, challenges, and comparative landscape including competitive scenario, cross comparisons, opportunities, and pain points. The report concludes with future market projections based on revenue, broken down by cold chain services, end-users, temperature ranges, ownership, and a success case study showcasing major market opportunities and critical pitfalls.

Greece Cold Chain Market Overview and Size

The Greece cold chain market reached a valuation of EUR 480 million in 2023, driven by rising demand for temperature-sensitive goods, rapid expansion in organized retail and e-commerce, and stringent EU regulations on pharmaceutical and food storage. The market includes major players such as Frigoglass, Theoni Logistics, SEEMS Logistics, and Metron Logistics, which offer comprehensive storage and distribution services for refrigerated and frozen products across the country.

In 2023, Frigoglass expanded its logistics footprint in Thessaloniki with a new cold warehouse facility to cater to the increasing demand from Northern Greece and Balkan exports. Athens and Thessaloniki remain the key hubs owing to their proximity to ports, infrastructure development, and concentration of pharmaceutical and food processing clusters.

%252C%25202019-2024.png&w=640&q=75)

What Factors are Leading to the Growth of Greece Cold Chain Market:

Regulatory Compliance and EU Standards: The European Union mandates strict guidelines for storage and transportation of perishable goods, especially in pharma and food sectors. Compliance with Good Distribution Practices (GDP) and HACCP standards has significantly boosted investments in modern cold chain infrastructure in Greece. In 2023, over 75% of pharma logistics providers upgraded to GDP-compliant warehouses.

Rise in E-commerce and Frozen Foods: Changing consumer preferences have accelerated demand for frozen ready-to-eat meals, dairy, seafood, and gourmet products, driven by convenience and lifestyle changes. The online food delivery sector in Greece grew by 18% CAGR from 2020–2023, boosting demand for last-mile refrigerated transport.

Growing Pharmaceutical Logistics Market: The pharmaceutical sector remains one of the highest contributors to cold chain demand. With over EUR 1.2 billion in pharma exports in 2023, Greece continues to serve as a regional hub for temperature-sensitive medical products. Growth in biologics and vaccines post-COVID-19 has led to specialized investments in 2–8°C and deep freeze infrastructure.

Which Industry Challenges Have Impacted the Growth of the Greece Cold Chain Market

High Operating Costs: One of the major challenges in Greece’s cold chain sector is the high cost associated with electricity, fuel, and maintenance of temperature-controlled facilities. In 2023, operational expenses accounted for nearly 35–40% of total logistics costs for cold chain operators. The volatility in energy prices has made it difficult for smaller logistics firms to sustain operations, thereby limiting market competitiveness and scalability.

Infrastructure Gaps in Secondary Cities: While cities like Athens and Thessaloniki have well-developed cold storage and distribution networks, infrastructure in Tier-2 and rural areas remains underdeveloped. This gap significantly restricts efficient cold chain coverage for inland agricultural zones, especially in Central and Western Greece. As a result, up to 25% of perishable goods are either delayed or lost due to inadequate cold handling systems in these regions.

Fragmented Market and Low Technology Penetration: The Greece cold chain market remains fragmented, with several small to mid-sized players lacking integrated systems and digital capabilities. In 2023, only 32% of logistics providers adopted real-time temperature tracking and fleet monitoring technologies. This leads to reduced traceability, poor visibility in supply chains, and increased spoilage risks, especially for sensitive cargo like vaccines and seafood.

What are the Regulations and Initiatives which have Governed the Market:

EU Compliance Standards for Perishables and Pharmaceuticals: Cold chain operators in Greece are mandated to comply with European Union GDP (Good Distribution Practices) and HACCP guidelines for food and pharma products. These regulations govern temperature control, hygiene, documentation, and product handling. In 2023, over 80% of pharmaceutical logistics players in Greece were audited for GDP compliance, and 68% passed in the first round.

National Food Safety Regulations: The Hellenic Food Authority (EFET) oversees the transport and storage of perishable goods in Greece. Cold chain companies must comply with regulations for temperature monitoring, product labeling, and food traceability. In 2023, EFET conducted over 2,500 inspections and issued 120 penalties related to improper cold storage conditions.

Port and Logistics Modernization Initiatives: As part of the Greece 2.0 Recovery and Resilience Plan, the government has allocated funding for logistics modernization, including cold storage upgrades in Piraeus and Thessaloniki ports. In 2023, a EUR 40 million investment was approved to develop temperature-controlled terminals to support growing trade in seafood, dairy, and fresh produce.

Greece Cold Chain Market Segmentation

By Type of Market Structure: The Greece cold chain industry is predominantly led by unorganized and mid-scale logistics players, especially in regional and rural markets where infrastructure investment remains limited. These companies handle distribution for local food producers and operate with limited automation and traceability. However, the organized sector, which includes established firms such as Frigoglass, Theoni Logistics, and SEEMS Logistics, has been gaining market share due to their ability to offer end-to-end cold chain solutions, real-time temperature monitoring, GDP-compliant warehousing, and efficient last-mile connectivity—especially in urban centers and for pharmaceutical clients.

%252C%25202023%2520(1).png&w=640&q=75)

By End-User Industry: The pharmaceutical sector accounts for a significant portion of the cold chain demand, driven by the need for precise temperature control, product safety, and EU regulatory compliance. Food and beverage follow as a key segment—particularly frozen seafood, dairy, fresh produce, and bakery items. The retail and e-commerce segment has seen strong growth in recent years, especially with the surge in online grocery delivery and meal kits that require controlled temperatures during last-mile delivery.

%252C%25202023.png&w=640&q=75)

By Type of Temperature Control:Chilled storage (2–8°C) holds the largest share, catering to pharmaceuticals, dairy, and fruits. Frozen storage (-18°C and below) is primarily used for seafood, meat, and ice cream. The demand for ultra-low temperature storage (e.g., for biologics and vaccines) is niche but growing rapidly post-pandemic, with significant investments expected over the next few years to meet demand in the healthcare sector.

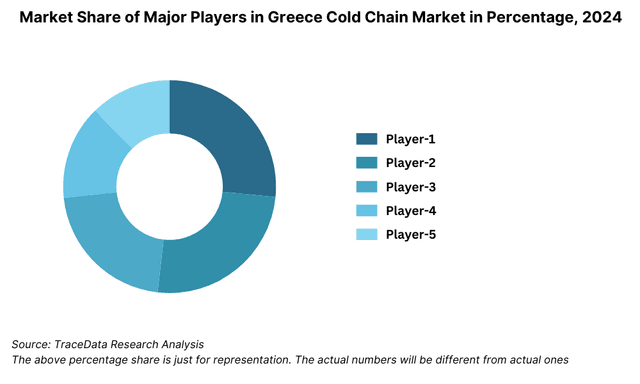

Competitive Landscape in Greece Cold Chain Market

The Greece cold chain market is moderately consolidated, with a mix of large logistics providers and specialized cold chain companies. The presence of regional players, alongside international logistics firms expanding operations in Greece, has diversified the service landscape. Notable companies include Frigoglass, SEEMS Logistics, Theoni Logistics, Metron Logistics, and Express Hellas, each offering varying degrees of cold storage, refrigerated transport, and value-added services.

Company | Establishment Year | Headquarters |

Frigoglass | 1996 | Kato Achaia, Greece |

SEEMS Logistics | 2008 | Athens, Greece |

Theoni Logistics | 2011 | Thessaloniki, Greece |

Metron Logistics | 1999 | Aspropyrgos, Greece |

Express Hellas | 1995 | Piraeus, Greece |

Some of the recent competitor trends and key information about competitors include:

Frigoglass: A leading name in refrigeration and cold logistics, Frigoglass expanded its storage capacity in 2023 with a new cold warehouse in Thessaloniki. The facility focuses on dairy and seafood, aiming to improve cross-border trade with the Balkans. The company also adopted solar power at two key sites to reduce operational energy costs by 18%.

SEEMS Logistics: Focused on pharmaceutical and medical cold chain distribution, SEEMS reported a 22% growth in 2–8°C temperature-controlled shipments in 2023. Its compliance with GDP standards and investments in real-time temperature tracking systems have made it a preferred partner for pharma companies.

Theoni Logistics: Serving Northern Greece and Balkan export routes, Theoni Logistics operates a fleet of over 120 refrigerated trucks. In 2023, the company introduced AI-based route optimization software, improving delivery efficiency by 14% and reducing spoilage in long-distance shipments.

Metron Logistics: Known for its integrated cold chain services, Metron has invested in automation and smart inventory systems. The company reported handling over 65,000 pallets of frozen goods in 2023, with clients in the retail, foodservice, and bakery segments.

Express Hellas: With strong operations in the Attica and Peloponnese regions, Express Hellas has grown its cold transport vertical by 17% year-over-year. Its partnership with Greek food cooperatives has enabled direct farm-to-retail delivery, helping reduce waste and extend shelf life for perishables.

What Lies Ahead for Greece Cold Chain Market?

The Greece cold chain market is projected to experience sustained growth through 2029, backed by increasing demand in the pharmaceutical, food export, and e-commerce sectors. The market is expected to register a CAGR of around 7–9% during the forecast period, driven by regulatory compliance pressures, supply chain modernization, and growing consumer demand for safe and quality perishables.

Expansion of Biopharma and Vaccine Logistics: As Greece strengthens its role as a regional pharmaceutical logistics hub, especially for Southeastern Europe, demand for ultra-cold storage and validated pharma transportation will rise. Cold chain providers are expected to invest in -20°C and -80°C infrastructure to support biologics, gene therapies, and vaccine distribution, especially under EU cross-border health initiatives.

Growth in E-commerce and Omnichannel Food Retail: The rise of online grocery platforms and direct-to-consumer frozen food brands is set to transform last-mile delivery. Cold chain operators will need to develop urban micro-fulfillment centers and enhance last-mile refrigerated transport in densely populated areas like Athens and Thessaloniki to meet increasing delivery expectations.

Digitalization and Smart Cold Chain Monitoring: Digital transformation will play a major role in the future. The adoption of IoT sensors, RFID tags, and real-time tracking systems will become the norm, allowing stakeholders to monitor temperature deviations, ensure traceability, and reduce spoilage. AI-based demand forecasting and route optimization tools are also expected to enhance efficiency and reduce energy consumption.

Infrastructure Development in Secondary Cities: With government and EU support, new cold chain infrastructure is likely to be developed in underpenetrated regions such as Western Macedonia, Peloponnese, and Crete, helping to reduce post-harvest losses and improve linkages between agri-clusters and export ports.

%252C%25202024-2030.png&w=640&q=75)

Greece Cold Chain Market Segmentation

• By Market Structure:

o Independent Cold Chain Logistics Providers

o Integrated 3PL/4PL Cold Chain Companies

o Temperature-Controlled Warehouse Operators

o Cold Transport Fleet Operators

o Organized Sector

o Unorganized Sector

• By End-User Industry:

o Pharmaceuticals and Biotechnology

o Food and Beverage (Dairy, Meat, Seafood, Ready Meals)

o Fresh Produce and Horticulture

o Retail and Supermarkets

o Hospitality and Foodservice

o E-commerce and Online Grocery

• By Temperature Range:

o Chilled (2–8°C)

o Frozen (-18°C and below)

o Ambient (15–25°C)

o Ultra-low Temperature (-80°C and below)

• By Type of Services:

o Cold Storage Warehousing

o Reefer Trucking and Cold Transport

o Cross-Docking and Transshipment

o Last-Mile Cold Delivery

o Value-Added Services (Packaging, Labelling, Inventory Management)

• By Region:

o Attica (Athens)

o Central Macedonia (Thessaloniki)

o Western Greece

o Crete

o Peloponnese

o Eastern Macedonia and Thrace

Players Mentioned in the Report:

• Frigoglass

• SEEMS Logistics

• Theoni Logistics

• Metron Logistics

• Express Hellas

• Kuehne+Nagel Hellas

• Sarantis Cold Logistics

• Havi Logistics Greece

Key Target Audience:

• Cold Chain Logistics Providers

• Pharmaceutical and Food Manufacturers

• E-commerce and Retail Supply Chains

• Ministry of Rural Development and Food

• Hellenic Food Authority (EFET)

• Logistics Infrastructure Investors

• Regulatory and Trade Compliance Agencies

• Research & Policy Institutions

Time Period:

• Historical Period: 2018–2023

• Base Year: 2024

• Forecast Period: 2024–2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-“ Role of Entities, Stakeholders, and challenges that they face

4.2. Revenue Streams for Greece Cold Chain Market

4.3. Business Model Canvas for Greece Cold Chain Market

4.4. Buying Decision Making Process

4.5. Supply Decision Making Process

5.1. Cold Chain Logistics Infrastructure in Greece, 2018-2024

5.2. Cold Storage and Transport Coverage Ratio by Region, 2018-2024

5.3. Investment in Cold Chain Infrastructure in Greece, 2024

5.4. Number of Cold Chain Operators by Type (Storage vs. Transport)

8.1. Revenues, 2018-2024

8.2. Volume Handled (MT / CBM), 2018-2024

9.1. By Market Structure (Organized and Unorganized Market), 2023-2024P

9.2. By Temperature Range (Chilled, Frozen, Ambient, Ultra-Low), 2023-2024P

9.3. By Type of Service (Storage, Transport, Last Mile, Value-Added), 2023-2024P

9.4. By Region, 2023-2024P

9.5. By End-User Industry (Pharmaceuticals, F&B, Retail, Agriculture), 2023-2024P

9.6. By Facility Ownership (Owned, Leased, 3PL), 2023-2024P

10.1. Customer Landscape and Cohort Analysis

10.2. Customer Journey and Decision Making

10.3. Need, Desire, and Pain Point Analysis

10.4. Gap Analysis Framework

11.1. Trends and Developments for Greece Cold Chain Market

11.2. Growth Drivers for Greece Cold Chain Market

11.3. SWOT Analysis for Greece Cold Chain Market

11.4. Issues and Challenges for Greece Cold Chain Market

11.5. Government Regulations for Greece Cold Chain Market

12.1. Market Size and Future Potential of Tech-Enabled Cold Chain Solutions, 2018-2029

12.2. Business Model and Revenue Streams of Smart Cold Chain

12.3. Cross Comparison of Leading Players Based on Facility Type, Temperature Zones, Fleet Size, Sustainability Initiatives

13.1. Credit Penetration and Capital Support for Cold Chain Projects, 2018-2029

13.2. Financial Assistance and Subsidies by EU and National Government

13.3. Breakdown of Finance Availability for SMEs vs Large Cold Chain Operators

13.4. Role of Development Banks and Private Equity in Cold Chain Expansion

13.5. Case Studies on Infrastructure Financing

16.1. Benchmark of Key Competitors in Greece Cold Chain Market including variables such as Company Overview, USP, Business Strategies, Strength, Weakness, Business Model, Technology Adoption, Temperature Coverage, Number of Warehouses and Trucks, Recent Developments

16.2. Strength and Weakness

16.3. Operating Model Analysis Framework

16.4. Gartner Magic Quadrant

16.5. Bowmans Strategic Clock for Competitive Advantage

17.1. Revenues, 2025-2029

17.2. Volume Handled (MT / CBM), 2025-2029

18.1. By Market Structure (Organized and Unorganized Market), 2025-2029

18.2. By Temperature Range (Chilled, Frozen, Ambient, Ultra-Low), 2025-2029

18.3. By Type of Service (Storage, Transport, Last Mile, Value-Added), 2025-2029

18.4. By Region, 2025-2029

18.5. By End-User Industry (Pharmaceuticals, F&B, Retail, Agriculture), 2025-2029

18.6. By Facility Ownership (Owned, Leased, 3PL), 2025-2029

18.7. Recommendation

18.8. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand side and supply side entities for Greece Cold Chain Market. Basis this ecosystem, we will shortlist leading 5-6 players in the country based upon their facility footprint, temperature compliance (GDP, HACCP), and service capabilities including warehousing and transportation.

Sourcing is made through industry articles, multiple secondary, and proprietary databases to perform desk research around the market to collate industry-level information.

Step 2: Desk Research

Subsequently, we engage in an exhaustive desk research process by referencing diverse secondary and proprietary databases. This approach enables us to conduct a thorough analysis of the market, aggregating industry-level insights. We delve into aspects like the warehousing capacity, transport fleet size, number of market players, pricing benchmarks, demand segmentation, and other variables. We supplement this with detailed examinations of company-level data, relying on sources like press releases, annual reports, financial statements, and similar documents. This process aims to construct a foundational understanding of both the market and the entities operating within it.

Step 3: Primary Research

We initiate a series of in-depth interviews with C-level executives and other stakeholders representing various Greece Cold Chain Market companies and end-users. This interview process serves a multi-faceted purpose: to validate market hypotheses, authenticate statistical data, and extract valuable operational and financial insights from these industry representatives. Bottom to top approach is undertaken to evaluate volume handled for each player thereby aggregating to the overall market.

As part of our validation strategy, our team executes disguised interviews wherein we approach each company under the guise of potential customers. This approach enables us to validate the operational and financial information shared by company executives, corroborating this data against what is available in secondary databases. These interactions also provide us with a comprehensive understanding of revenue streams, value chain, process, pricing, and other factors.

Step 4: Sanity Check

- Bottom to top and top to bottom analysis along with market size modeling exercises is undertaken to assess sanity check process.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Greece cold chain market is poised for steady growth, reaching an estimated valuation of EUR 480 Million in 2023. This growth is driven by the rising demand for temperature-sensitive products in the pharmaceutical, food, and e-commerce sectors. Increasing regulatory compliance with EU standards, government-led infrastructure upgrades, and the modernization of retail and food supply chains further enhance the market’s long-term potential.

The Greece Cold Chain Market includes several key players such as Frigoglass, SEEMS Logistics, and Theoni Logistics. These companies have strong capabilities in cold storage, refrigerated transport, and last-mile delivery. Other notable players include Metron Logistics, Express Hellas, and Kuehne+Nagel Hellas, who provide integrated cold chain solutions across various temperature ranges.

Primary growth drivers include the expansion of pharmaceutical logistics, increasing frozen and chilled food consumption, and the surge in e-commerce and home delivery services. Compliance with Good Distribution Practices (GDP) and food safety standards, along with EU-backed funding for cold infrastructure, are also key contributors. The digital transformation of logistics with real-time temperature tracking and route optimization is further accelerating market efficiency.

The Greece Cold Chain Market faces several challenges including high energy and operational costs, limited cold chain coverage in rural and secondary cities, and fragmented service providers with low adoption of technology. Infrastructure constraints at regional levels and underinvestment in ultra-low temperature storage also pose hurdles to comprehensive service delivery. Additionally, maintaining compliance with evolving EU and local regulatory standards remains a persistent challenge for smaller operators.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0