Greece Logistics and warehousing Market Outlook to 2029

By Type of Service (Freight Forwarding, Warehousing, Cold Chain, Last-Mile Delivery), By End Users (Retail, Automotive, Pharmaceuticals, FMCG), By Transport Mode (Road, Sea, Rail, Air), and By Region

Report Overview

Report Code

TDR0277

Coverage

Asia

Published

September 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Greece Logistics and Warehousing Market Outlook to 2029 – By Type of Service (Freight Forwarding, Warehousing, Cold Chain, Last-Mile Delivery), By End Users (Retail, Automotive, Pharmaceuticals, FMCG), By Transport Mode (Road, Sea, Rail, Air), and By Region” provides a comprehensive analysis of the logistics and warehousing industry in Greece. The report covers the market’s genesis and evolution, overall market size in terms of revenue, detailed segmentation, emerging trends and developments, regulatory framework, customer profiling, major issues and challenges, competitive landscape, and company profiling of key logistics players.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Greece Logistics and Warehousing Market Outlook to 2029 – By Type of Service (Freight Forwarding, Warehousing, Cold Chain, Last-Mile Delivery), By End Users (Retail, Automotive, Pharmaceuticals, FMCG), By Transport Mode (Road, Sea, Rail, Air), and By Region” provides a comprehensive analysis of the logistics and warehousing industry in Greece. The report covers the market’s genesis and evolution, overall market size in terms of revenue, detailed segmentation, emerging trends and developments, regulatory framework, customer profiling, major issues and challenges, competitive landscape, and company profiling of key logistics players. The report concludes with future projections based on market performance, demand drivers, infrastructure investments, and case studies highlighting key growth enablers and caution areas.

Greece Logistics and Warehousing Market Overview and Size

The Greece logistics and warehousing market was valued at EUR 9.2 Billion in 2023, supported by Greece’s strategic geographic position as a gateway to Europe, Asia, and Africa, coupled with expanding port infrastructure, trade routes via Piraeus port, and robust growth in e-commerce and retail sectors. The market is driven by both local players and international logistics firms, including Goldair Cargo, ACS Courier, DHL Greece, and Kuehne + Nagel.

In 2023, the Port of Piraeus handled over 5.2 million TEUs, making it one of the largest ports in Europe. Investments in intermodal connectivity and the Trans-European Transport Network (TEN-T) have significantly boosted demand for warehousing and integrated logistics services. Athens, Thessaloniki, and Patras are emerging as key regional hubs due to their infrastructure, population density, and access to rail and maritime routes.

%252C%25202019-2024_B9Jk1Dn.png&w=640&q=75)

What Factors are Leading to the Growth of the Greece Logistics and Warehousing Market:

Strategic Geographic Location: Greece acts as a natural logistics hub for Europe, with the Port of Piraeus serving as a key transshipment point. Its integration into the China-Europe shipping route via the Belt and Road Initiative has attracted investment and increased container traffic by over 8% annually since 2020.

E-Commerce and Retail Expansion: The surge in online shopping, especially post-pandemic, has accelerated demand for last-mile delivery and urban warehousing. In 2023, e-commerce penetration in Greece reached 53%, driving the need for agile supply chains and smart warehouse solutions.

Government and EU Infrastructure Funding: Projects under Greece 2.0 and the EU’s Recovery and Resilience Facility (RRF) are fueling logistics modernization, including digitization of customs, port infrastructure upgrades, and smart transport systems. Over EUR 1.2 billion has been earmarked for logistics infrastructure through 2026.

Which Industry Challenges Have Impacted the Growth for Greece Logistics and Warehousing Market

Fragmented Infrastructure Outside Major Hubs: While ports like Piraeus and Thessaloniki are well-developed, logistics infrastructure in secondary cities and rural areas remains underdeveloped. According to a 2023 industry analysis, over 40% of logistics firms cited poor road and rail connectivity outside Athens and Thessaloniki as a major bottleneck, increasing lead times and operational costs by up to 18%.

Bureaucracy and Regulatory Complexity: Greece’s logistics sector continues to face complex customs procedures, licensing delays, and inconsistent local regulations. In a recent World Bank Logistics Performance Index survey, Greece ranked below the EU average in customs efficiency. On average, logistics providers report up to 2–3 weeks for licensing and permit approvals, slowing down operations and discouraging new entrants.

High Operating and Energy Costs: Rising fuel prices, electricity rates, and warehouse rental costs have significantly impacted profitability in the logistics sector. In 2023, energy and fuel costs constituted approximately 34% of total logistics operating expenses in Greece, compared to the EU average of 26%. This cost burden especially affects SMEs and cold chain operators, reducing competitiveness.

What are the Regulations and Initiatives which have Governed the Market:

EU and National Transport Policies: Greece adheres to the EU Mobility Package and TEN-T regulations, focusing on seamless cross-border freight movement, green logistics, and driver work conditions. In 2022, the Greek Ministry of Infrastructure aligned domestic trucking laws with EU road freight norms, simplifying rules for fleet owners and reducing compliance penalties by 15% year-over-year.

Logistics Parks and Strategic Warehousing Zones: The Greek government has prioritized the development of logistics parks in Attica and Northern Greece. In 2023, over EUR 280 million was invested in the Thriasio Pedio Logistics Center near Athens, aimed at consolidating warehousing, customs, and freight forwarding services under one roof. These initiatives are expected to reduce handling times by 20% once operational.

Tax Incentives and EU Grants for Green Logistics: Under Greece’s Recovery and Resilience Plan, logistics companies investing in electric fleets, energy-efficient warehouses, and digitalization can avail tax deductions and EU subsidies covering up to 50% of capital expenditure. In 2023 alone, over 110 logistics companies received grants under this scheme, promoting ESG-aligned growth.

Greece Logistics and Warehousing Market Segmentation

By Market Structure: The Greek logistics market is primarily dominated by domestic players that have established deep-rooted relationships with retail, FMCG, and manufacturing clients. These local firms often offer flexible pricing models, better regional route knowledge, and tailored services, especially in warehousing and last-mile delivery. However, multinational 3PL and 4PL providers such as DHL, DB Schenker, and Kuehne + Nagel have captured significant market share in freight forwarding and cold chain services by leveraging advanced technology, global networks, and compliance capabilities. Their dominance is particularly evident in high-value, regulated segments such as pharmaceuticals and electronics.

%2520on%2520the%2520Basis%2520of%2520Revenue%2520Share%2520in%2520Percentage%252C%25202023.png&w=640&q=75)

By Mode of Transport: Road freight remains the backbone of the logistics market in Greece, accounting for a major portion of domestic transportation. This is due to the country's mountainous terrain and the lack of widespread rail connectivity. However, sea freight is increasingly vital, particularly due to the strategic role of the Port of Piraeus and its position in global shipping routes. Rail freight is gradually gaining traction, especially for intermodal shipments linking Piraeus with Central Europe, supported by EU funding and private operator interest.

%2520on%2520the%2520Basis%2520of%2520Revenue%2520Share%2520in%2520Percentage%252C%25202023_yWG8BzB.png&w=640&q=75)

By End User Industry: Retail and e-commerce represent the largest end-user segment, driven by the explosive growth in online shopping and the need for responsive, last-mile logistics solutions. The FMCG sector follows, with growing demand for timely delivery and warehousing across Greece's urban and semi-urban areas. Pharmaceuticals and healthcare are rapidly expanding end-use segments due to increasing requirements for GDP-compliant cold storage and temperature-sensitive deliveries, especially in export-linked operations. Automotive logistics, while smaller, remains a steady contributor due to vehicle imports and component warehousing needs.

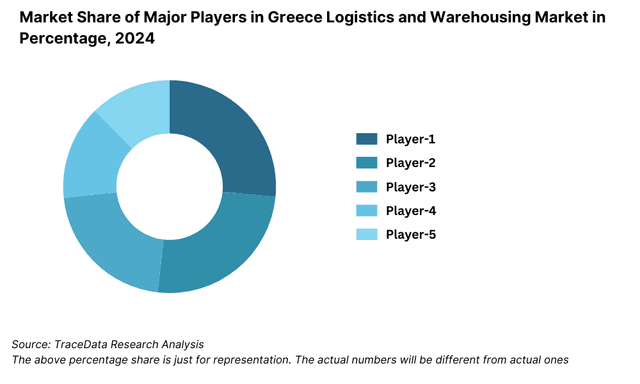

Competitive Landscape in Greece Logistics and Warehousing Market

The Greece logistics and warehousing market is moderately consolidated, with a mix of large global logistics providers and established domestic players. Over the past few years, the sector has experienced digital transformation and infrastructure-driven consolidation, particularly around major trade corridors like Piraeus-Athens-Thessaloniki. Key players include Goldair Cargo, ACS Courier, DHL Greece, Kuehne + Nagel, and Med Frigo, all offering diverse services from freight forwarding to last-mile and cold chain solutions.

Company | Establishment Year | Headquarters |

Goldair Cargo | 1992 | Athens, Greece |

ACS Courier | 1981 | Athens, Greece |

DHL Greece | 1980 (local ops) | Athens, Greece |

Kuehne + Nagel | 1890 (global) | Thessaloniki, Greece |

Med Frigo | 1991 | Patras, Greece |

Some of the recent competitor trends and key information about competitors include:

Goldair Cargo: One of Greece’s largest logistics companies, Goldair Cargo expanded its intermodal services in 2023 by integrating its rail and sea freight networks for Central European routes. The company also launched a new warehousing facility in Thessaloniki, increasing its capacity by 25%, especially for bonded storage and pharmaceuticals.

ACS Courier: A leader in courier and last-mile delivery services, ACS Courier handled over 70 million parcels in 2023, reflecting a 17% YoY growth driven by e-commerce. The company introduced route optimization algorithms and electric delivery vans in Athens, enhancing delivery efficiency and ESG compliance.

DHL Greece: DHL continued its dominance in the international freight forwarding and express logistics segment, registering over 12% revenue growth in 2023. The firm invested in a new temperature-controlled hub near the Athens International Airport to serve its pharma and perishable goods clients.

Kuehne + Nagel Greece: This global player operates key warehouses and inland container depots in Thessaloniki and Piraeus. In 2023, the company introduced blockchain-based tracking solutions for its clients in the retail and FMCG sectors, helping improve shipment visibility and reduce transit time disputes.

Med Frigo: A specialist in cold chain logistics, Med Frigo grew its fleet of temperature-controlled vehicles by 20% in 2023. It expanded operations to cover cross-border routes with Italy and France for food and pharmaceutical shipments. Its investments in telematics and real-time temperature monitoring have strengthened its compliance with EU GDP norms.

What Lies Ahead for Greece Logistics and Warehousing Market?

The Greece logistics and warehousing market is projected to witness steady growth through 2029, driven by infrastructure modernization, rising international trade flows, and increasing demand from the e-commerce, pharmaceutical, and FMCG sectors. With continued EU funding and private investments, the market is expected to record a healthy CAGR over the forecast period.

Expansion of Multimodal and Intermodal Infrastructure: The development of intermodal hubs connecting sea, road, and rail—especially around the Piraeus-Thessaloniki corridor—is expected to significantly reduce transit times and enhance supply chain efficiency. Projects under the Trans-European Transport Network (TEN-T) and Greece 2.0 are likely to make the country a preferred gateway for Europe-bound freight from Asia and Africa.

Digitalization and Smart Logistics: Wider adoption of digital platforms for warehouse management, route optimization, freight visibility, and real-time tracking will drive efficiency. The integration of AI and IoT in cold chain and inventory control is expected to increase operational transparency and reduce spoilage, particularly in pharma and perishables.

Green and Sustainable Warehousing: Sustainability will play a major role in shaping future logistics infrastructure. The adoption of solar-powered warehouses, electric vehicle (EV) fleets, and energy-efficient storage systems is expected to rise, in line with EU’s Green Deal targets. By 2029, it is estimated that over 40% of new logistics facilities in Greece will adopt green building certifications.

Growth in Third-Party Logistics (3PL) and Fourth-Party Logistics (4PL): With rising supply chain complexity, especially in omnichannel retail and cross-border trade, more companies are expected to outsource to 3PL and 4PL providers. This shift will increase demand for value-added services such as inventory optimization, returns management, and customs brokerage.

%252C%25202024-2030_rsSQnBh.png&w=640&q=75)

Greece Logistics and Warehousing Market Segmentation

• By Market Structure:

o Organized Sector

o Unorganized Sector

o Domestic Logistics Providers

o International 3PL & 4PL Companies

o E-commerce-focused Logistics Firms

o Cold Chain Specialists

o Courier and Last-Mile Delivery Companies

• By Mode of Transport:

o Road Freight

o Sea Freight

o Rail Freight

o Air Freight

• By End User Industry:

o Retail & E-commerce

o FMCG

o Pharmaceuticals

o Automotive

o Industrial Manufacturing

o Agriculture & Perishables

• By Region:

o Attica (Athens and surroundings)

o Central Macedonia (Thessaloniki)

o Western Greece (Patras and surroundings)

o Crete

o Eastern Macedonia & Thrace

• By Type of Services:

o Freight Forwarding

o Warehousing

o Cold Chain Logistics

o Express and Last-Mile Delivery

o Value-Added Services (packaging, inventory management, customs clearance)

Players Mentioned in the Report:

• Goldair Cargo

• ACS Courier

• DHL Greece

• Kuehne + Nagel

• Med Frigo

• Speedex

• Transcombi Express

• FDL Group

• Sarmed

• TNT Express Greece

Key Target Audience:

• Third-Party Logistics (3PL) Providers

• Freight Forwarding Companies

• Cold Chain Operators

• E-commerce and Retail Firms

• Manufacturing and Pharmaceutical Companies

• Government and Regulatory Authorities (e.g., Ministry of Infrastructure and Transport)

• Real Estate Developers (Logistics Parks, Warehousing)

• Investment Funds and Infrastructure Investors

• Trade and Transport Policy Makers

• Research and Consulting Firms

Time Period:

• Historical Period: 2018–2023

• Base Year: 2024

• Forecast Period: 2024–2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-“ Role of Entities, Stakeholders, and Challenges They Face

4.2. Revenue Streams for Greece Logistics and Warehousing Market

4.3. Business Model Canvas for Greece Logistics Providers

4.4. Logistics Partner Selection and Outsourcing Decision Process

4.5. Supply Chain Strategy Decision Process

5.1. Overview of Freight Movements by Mode in Greece, 2018-“2024

5.2. Import-Export Volume and Trade Balance, 2018-“2024

5.3. Greece Logistics Cost as % of GDP and Comparison with EU, 2024

5.4. Number of Logistics Companies in Greece by Region

8.1. Revenues, 2018-“2024

8.2. Volume Handled (Tonnage, TEUs), 2018-“2024

9.1. By Market Structure (Organized vs. Unorganized), 2023-“2024P

9.2. By Mode of Transport (Road, Sea, Rail, Air), 2023-“2024P

9.3. By End-User Industry (Retail, FMCG, Pharma, Automotive, Industrial), 2023-“2024P

9.4. By Region (Attica, Central Macedonia, Crete, etc.), 2023-“2024P

9.5. By Type of Services (Freight Forwarding, Warehousing, Cold Chain, Last-Mile Delivery), 2023-“2024P

10.1. Customer Segmentation and Cohort Analysis

10.2. Partner Evaluation Criteria and Outsourcing Decision Factors

10.3. Pain Points in Logistics Operations and Gaps in Service Delivery

10.4. Gap Analysis Framework

11.1. Trends and Developments for Greece Logistics Market

11.2. Growth Drivers for Greece Logistics and Warehousing Market

11.3. SWOT Analysis for Greece Logistics Market

11.4. Issues and Challenges in the Sector

11.5. Regulatory Landscape and EU Policy Impact

12.1. Market Size and Future Potential for Urban Logistics, 2018-“2029

12.2. Business Models of Last-Mile Operators

12.3. Cross Comparison of Key Last-Mile Players-“ Service, Reach, Tech Stack, Partnerships

13.1. Market Size and Growth in Cold Chain Infrastructure, 2018-“2029

13.2. Growth in Pharma and Perishable Goods Logistics

13.3. Cold Storage Capacity by Region

13.4. Adoption of IoT and Compliance with EU GDP Norms

16.1. Benchmarking of Key Players (Company Overview, USP, Service Lines, Clients, Fleet/Warehouse Size)

16.2. Strengths and Weaknesses

16.3. Operating Model and Value Chain Positioning

16.4. Gartner Magic Quadrant (Adapted for Logistics Providers)

16.5. Bowmans Strategic Clock-“ Positioning of Key Players

17.1. Revenues, 2025-“2029

17.2. Volume Handled (Tonnage, TEUs), 2025-“2029

18.1. By Market Structure (Organized and Unorganized), 2025-“2029

18.2. By Mode of Transport (Road, Sea, Rail, Air), 2025-“2029

18.3. By End-User Industry, 2025-“2029

18.4. By Region, 2025-“2029

18.5. By Type of Service, 2025-“2029

18.6. Recommendation

18.7. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities for the Greece Logistics and Warehousing Market. This includes 3PL & 4PL providers, warehousing operators, cold chain specialists, freight forwarders, e-commerce enablers, and end-user industries like retail, pharma, and manufacturing. Based on this ecosystem, we shortlist the leading 5–6 logistics service providers in the country based on operational coverage, fleet strength, warehouse footprint, and financials.

Sourcing is done through industry associations (e.g., Hellenic Logistics Company), logistics trade reports, government publications, EU portals, and multiple secondary and proprietary databases to gather initial industry-level insights.

Step 2: Desk Research

An extensive desk research exercise is conducted using a combination of open-source data, proprietary databases, and government reports (Ministry of Infrastructure & Transport, ELSTAT, Eurostat, etc.). This includes analysis of market revenue, number of logistics and warehousing companies, warehouse capacity, freight volumes by mode (road, rail, sea, air), regional distribution centers, and trade dynamics.

Company-level data such as revenue trends, client sectors, operational investments, and strategic partnerships are gathered from financial statements, news articles, press releases, investor presentations, and company websites to build a detailed profile of the leading players.

Step 3: Primary Research

We conduct in-depth interviews with CXOs, logistics managers, warehouse operators, fleet managers, port authorities, and customs brokers. These interviews validate secondary data findings, provide granular operational and pricing insights, and help us understand demand-side requirements from industries like retail, FMCG, and pharmaceuticals.

Disguised interviews are also conducted with logistics service providers under the guise of potential clients to obtain firsthand information on pricing models, service capabilities, pain points, technology integration, and warehouse offerings. These interviews help triangulate data gathered from published sources and reveal practical market challenges and strategies.

Step 4: Sanity Check

- A combination of bottom-up (aggregating revenue and volume data from key players) and top-down (validating with macroeconomic indicators, trade flow, infrastructure investments) approaches is used to estimate and validate the overall market size. Market modeling tools are then applied to derive growth projections and perform a final sanity check on the calculated figures.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Greece logistics and warehousing market holds significant growth potential, with the sector reaching a valuation of EUR 9.2 Billion in 2023. This growth is underpinned by Greece’s strategic geographic location as a gateway to Europe, Asia, and Africa, combined with rising international trade, increased investments in transport infrastructure, and the rapid growth of e-commerce and cold chain segments.

Key players in the Greece logistics market include Goldair Cargo, ACS Courier, DHL Greece, Kuehne + Nagel, and Med Frigo. These companies dominate due to their strong infrastructure footprint, diversified service offerings across freight and warehousing, and strong partnerships with retail, pharma, and manufacturing sectors. Other emerging players include Sarmed, Speedex, and FDL Group.

Major growth drivers include the expansion of Greece’s port infrastructure (especially Port of Piraeus), EU-backed infrastructure funding, the shift to digital and green logistics solutions, and growing demand from industries such as retail, pharmaceuticals, and food & beverages. The increasing adoption of last-mile and temperature-controlled logistics is also accelerating market expansion.

The industry faces challenges such as fragmented logistics infrastructure outside urban hubs, high energy and operational costs, and bureaucratic hurdles in regulatory approvals and customs. Additionally, a shortage of skilled logistics professionals and limited penetration of automation and smart warehousing technologies constrain the sector’s efficiency and scalability.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0