India Electronics Manufacturing Market Outlook to 2035

By Product Category, By End-Use Industry, By Manufacturing Model, By Sales & Supply Chain Structure, and By Region

Report Overview

Report Code

TDR0508

Coverage

Asia

Published

January 2026

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “India Electronics Manufacturing Market Outlook to 2035 – By Product Category, By End-Use Industry, By Manufacturing Model, By Sales & Supply Chain Structure, and By Region” provides a comprehensive analysis of the electronics manufacturing ecosystem in India. The report covers an overview and genesis of the market, overall market size in terms of value, detailed market segmentation; trends and developments, policy and regulatory landscape, buyer-level demand profiling, key issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major domestic and international players operating in the Indian electronics manufacturing market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “India Electronics Manufacturing Market Outlook to 2035 – By Product Category, By End-Use Industry, By Manufacturing Model, By Sales & Supply Chain Structure, and By Region” provides a comprehensive analysis of the electronics manufacturing ecosystem in India. The report covers an overview and genesis of the market, overall market size in terms of value, detailed market segmentation; trends and developments, policy and regulatory landscape, buyer-level demand profiling, key issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major domestic and international players operating in the Indian electronics manufacturing market.

The report concludes with future market projections based on domestic consumption growth, export-oriented manufacturing expansion, government-led localization initiatives, supply chain realignment away from single-country dependencies, technology upgrading across EMS operations, and region-wise manufacturing cluster development, along with cause-and-effect relationships and case-based illustrations highlighting the major opportunities and structural risks shaping the market through 2035.

India Electronics Manufacturing Market Overview and Size

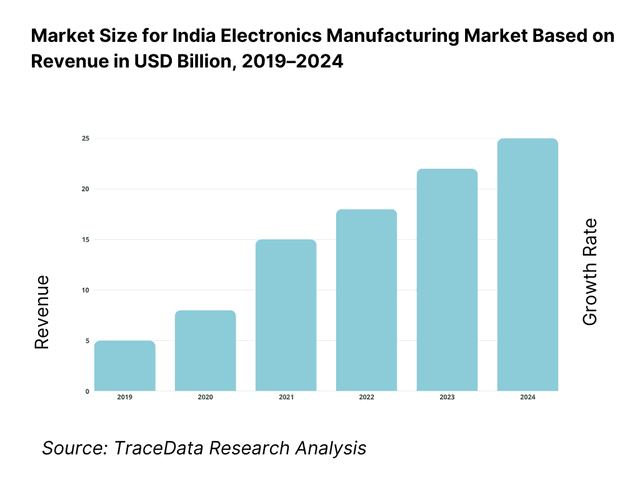

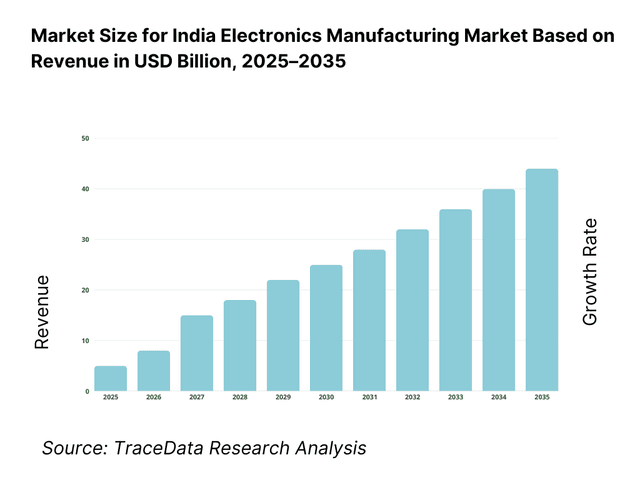

The India electronics manufacturing market is valued at approximately ~USD ~ billion, representing the production and assembly of electronic goods across consumer electronics, mobile devices, IT hardware, industrial electronics, automotive electronics, telecom equipment, and electronic components. The market encompasses original equipment manufacturing (OEM), electronics manufacturing services (EMS), contract manufacturing, and system integration activities, spanning printed circuit board assembly (PCBA), final product assembly, testing, packaging, and increasingly localized component sourcing.

India’s electronics manufacturing sector is anchored by a rapidly expanding domestic consumption base, rising digital penetration, growing smartphone and appliance demand, and sustained investments under policy frameworks such as production-linked incentives and phased manufacturing programs. The sector has evolved from import-dependent assembly operations toward deeper value addition, with increasing localization of enclosures, mechanicals, wiring harnesses, chargers, displays, and select semiconductor-linked components.

Mobile phones and consumer electronics form the backbone of manufacturing volumes, while IT hardware, automotive electronics, and industrial electronics are emerging as higher-value growth segments. The market benefits from India’s large labor pool, expanding industrial infrastructure, improving logistics connectivity, and the strategic push to position India as a global electronics manufacturing hub serving both domestic and export markets.

Regionally, Southern and Northern India dominate electronics manufacturing activity. Southern states lead due to mature electronics clusters, port access, export-oriented facilities, and strong EMS presence. Northern India has gained importance driven by mobile handset assembly, appliance manufacturing, and proximity to large consumption centers. Western India represents a fast-growing hub for automotive electronics, industrial electronics, and design-led manufacturing, supported by industrial corridors and supplier ecosystems. Eastern India remains relatively underpenetrated but is gradually attracting investments through electronics parks, state incentives, and backend manufacturing opportunities.

What Factors are Leading to the Growth of the India Electronics Manufacturing Market:

Rising domestic demand across consumer, industrial, and automotive electronics strengthens manufacturing scale: India’s electronics demand continues to expand due to urbanization, rising disposable incomes, digital adoption, and increasing electrification across sectors. Smartphones, televisions, home appliances, wearable devices, power electronics, and automotive electronics are witnessing sustained volume growth. This expanding consumption base provides manufacturers with scale economics, enabling higher capacity utilization, cost optimization, and gradual movement toward localized component ecosystems. The sheer size of domestic demand reduces dependence on export cycles and supports long-term capacity planning for electronics manufacturers.

Government-led manufacturing incentives and localization policies accelerate capacity creation: Policy initiatives focused on import substitution, export competitiveness, and domestic value addition have significantly reshaped the electronics manufacturing landscape. Incentive structures linked to incremental production, phased localization requirements, and electronics cluster development have encouraged both global and domestic players to establish and expand manufacturing operations in India. These policies reduce entry barriers, improve project viability, and incentivize long-term commitments across EMS, component manufacturing, and sub-assembly operations, thereby deepening the electronics manufacturing value chain.

Supply chain diversification away from single-country concentration benefits India as an alternative hub: Global electronics supply chains are undergoing structural realignment to reduce over-reliance on concentrated manufacturing geographies. India is increasingly positioned as a complementary manufacturing base for global OEMs seeking diversification, resilience, and regional supply capability. This shift has led to incremental relocation of assembly lines, expansion of EMS footprints, and onboarding of Indian suppliers into global vendor ecosystems. While full-spectrum component localization remains gradual, assembly-led manufacturing provides a foundation for progressive value addition over the forecast period.

Which Industry Challenges Have Impacted the Growth of the India Electronics Manufacturing Market:

Dependence on imported components and exposure to global supply chain volatility impacts cost stability and production planning: Despite significant progress in assembly-led manufacturing, India’s electronics manufacturing ecosystem remains dependent on imported semiconductors, displays, camera modules, passive components, and select sub-assemblies. Disruptions in global supply chains—driven by geopolitical tensions, logistics bottlenecks, currency fluctuations, or supplier concentration—can impact input availability, pricing, and delivery schedules. Sudden changes in component lead times or landed costs affect production planning, working capital cycles, and margin stability for manufacturers, particularly for EMS players operating on thin contractual margins and fixed pricing commitments to OEM clients.

Limited depth of domestic component ecosystem constrains value addition and competitiveness: While final assembly and PCBA capabilities have scaled rapidly, the domestic availability of high-value components remains limited. Gaps persist in semiconductor fabrication, advanced packaging, display manufacturing, precision sensors, and specialized electronic materials. This limits India’s ability to move up the value chain beyond assembly-intensive operations and reduces the competitiveness of locally manufactured electronics in export markets where deeper localization improves cost efficiency. Developing component ecosystems requires high capital investment, long gestation periods, and technology transfer, which slows the pace of structural transformation in the electronics manufacturing landscape.

Infrastructure readiness and operational execution challenges vary across manufacturing clusters: Electronics manufacturing requires stable power supply, clean room-ready facilities, water availability, waste management systems, and efficient logistics connectivity. While leading electronics clusters offer improving infrastructure, execution quality varies across regions, particularly in newer industrial parks. Delays in land acquisition, utility provisioning, and regulatory clearances can extend project timelines and increase setup costs. For time-sensitive electronics programs with short product life cycles, such execution risks can affect India’s attractiveness relative to more mature manufacturing hubs with plug-and-play infrastructure.

What are the Regulations and Initiatives which have Governed the Market:

Production-linked incentives and phased manufacturing programs shaping localization and capacity expansion: Government-led incentive frameworks linked to incremental output and domestic value addition have played a central role in scaling electronics manufacturing capacity in India. These initiatives encourage manufacturers to expand production volumes, localize components in phases, and invest in backward integration over time. Eligibility conditions related to investment thresholds, production targets, and localization milestones influence product selection, sourcing strategies, and long-term manufacturing roadmaps for both domestic firms and multinational players operating in India.

Electronics manufacturing cluster development and state-level incentive policies supporting ecosystem creation: Dedicated electronics manufacturing clusters, supported by central and state governments, provide shared infrastructure, fiscal incentives, and regulatory facilitation to reduce setup costs and improve operational efficiency. State-level policies covering capital subsidies, power tariff support, stamp duty exemptions, and employment-linked incentives play a critical role in influencing location decisions. Variations in policy implementation, approval timelines, and post-investment support across states impact the pace and success of cluster-led manufacturing development.

Import duties, customs structures, and trade policy measures influencing sourcing and cost structures: Customs duty structures on finished goods and components are used as policy tools to promote domestic manufacturing and discourage direct imports. Differential duties across components, sub-assemblies, and finished products affect sourcing decisions, bill-of-material optimization, and supplier onboarding strategies. While such measures support localization objectives, frequent revisions or complexity in duty structures can create short-term uncertainty for manufacturers managing global supply chains and multi-country sourcing arrangements.

India Electronics Manufacturing Market Segmentation

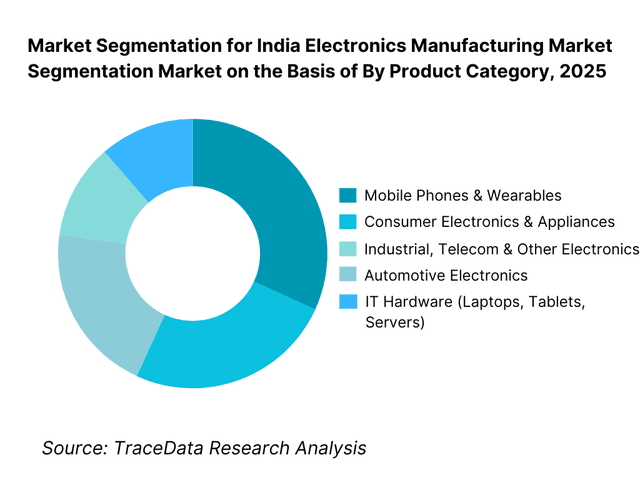

By Product Category: Mobile phones and consumer electronics hold dominance. This is because smartphones, feature phones, televisions, home appliances, and personal electronics account for the largest share of manufacturing volumes in India. High domestic consumption, short replacement cycles, and large-scale assembly programs by global and domestic brands drive capacity utilization and investment in this segment. Mobile phone manufacturing, in particular, benefits from standardized platforms, modular assembly processes, and strong policy support, making it the anchor segment for India’s electronics manufacturing ecosystem. While IT hardware, automotive electronics, and industrial electronics are expanding rapidly in value terms, consumer electronics continue to dominate in volume-driven manufacturing output.

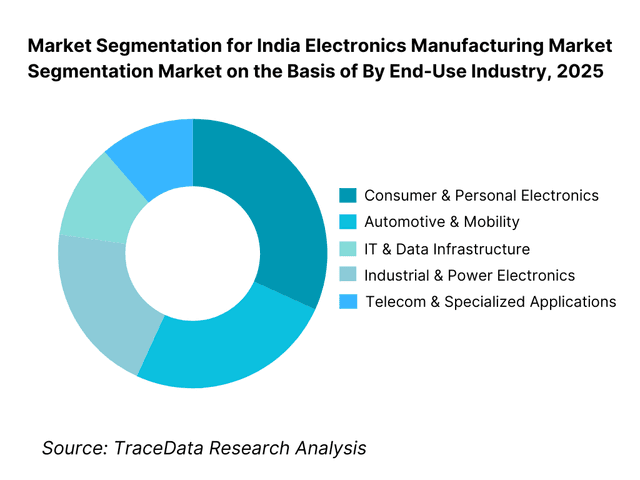

By End-Use Industry: Consumer and mobility-led demand dominates the market. Consumer-oriented end-use industries drive the majority of electronics manufacturing demand in India due to population scale, rising incomes, and digital adoption. Mobility-related electronics—including smartphones, wearables, and in-vehicle electronics—benefit from frequent product refresh cycles and expanding feature integration. Industrial, automotive, and telecom end-uses are growing faster in value terms, supported by electrification, automation, and connected infrastructure, but continue to trail consumer segments in overall manufacturing volumes.

Competitive Landscape in India Electronics Manufacturing Market

The India electronics manufacturing market exhibits moderate-to-high fragmentation, characterized by a mix of large multinational EMS providers, domestic contract manufacturers, and OEM-led captive manufacturing units. Market leadership is driven by scale of operations, ability to support high-volume programs, cost efficiency, quality compliance, and long-term relationships with global and domestic brands.

Global EMS players dominate large-scale smartphone and consumer electronics assembly, supported by strong balance sheets, advanced process capabilities, and established global customer relationships. Domestic manufacturers are increasingly competitive in select segments such as appliances, industrial electronics, chargers, and sub-assemblies, leveraging cost advantages, local sourcing, and policy incentives. Competition remains intense on margins, execution reliability, and ability to meet localization and compliance requirements.

Name | Founding Year | Original Headquarters |

Foxconn | 1974 | New Taipei City, Taiwan |

Pegatron | 2008 | Taipei, Taiwan |

Wistron | 2001 | Taipei, Taiwan |

Dixon Technologies | 1993 | Noida, India |

Tata Electronics | 2020 | Bengaluru, India |

Flex | 1969 | Singapore |

Sanmina | 1980 | San Jose, California, USA |

Jabil | 1966 | St. Petersburg, Florida, USA |

Sahasra Electronics | 2000 | Noida, India |

Some of the Recent Competitor Trends and Key Information About Competitors Include:

Foxconn: Foxconn remains the largest electronics manufacturing presence in India by scale, with a strong focus on mobile device assembly and export-oriented production. The company’s competitive strength lies in its ability to execute high-volume programs, manage complex global supply chains, and align closely with anchor OEM clients. Foxconn’s India strategy increasingly emphasizes capacity expansion, supplier ecosystem development, and gradual movement toward higher-value components.

Dixon Technologies: Dixon has emerged as a leading domestic EMS player with a diversified portfolio across consumer electronics, home appliances, lighting, and mobile devices. The company benefits from strong relationships with Indian and global brands, policy-driven localization opportunities, and expanding backward integration into components. Dixon’s positioning is particularly strong in high-volume, cost-sensitive product categories.

Tata Electronics: Tata Electronics represents India’s strategic push toward deeper electronics value chain participation, including precision manufacturing and semiconductor-linked activities. Backed by a large industrial group, the company focuses on long-term ecosystem creation, advanced manufacturing capabilities, and integration with global supply chains, positioning it as a critical player in India’s electronics manufacturing evolution.

Pegatron and Wistron: These Taiwan-headquartered EMS players have played a pivotal role in scaling India’s mobile device manufacturing capacity. Their competitive advantage lies in process discipline, quality consistency, and rapid replication of global manufacturing models. Continued investment decisions are closely tied to policy stability, scale economics, and export competitiveness.

Flex and Jabil: Global EMS majors such as Flex and Jabil maintain a strong presence in industrial, automotive, healthcare, and high-reliability electronics segments. Their India operations focus on complex assemblies, lifecycle management, and value-added manufacturing, supporting multinational clients seeking diversified production bases beyond consumer electronics.

What Lies Ahead for India Electronics Manufacturing Market?

The India electronics manufacturing market is expected to expand strongly through 2035, supported by sustained domestic consumption growth, export-oriented manufacturing expansion, and continued policy-led localization initiatives. Rising demand across smartphones, consumer appliances, automotive electronics, industrial electronics, and digital infrastructure equipment will underpin long-term manufacturing momentum. As global supply chains diversify and OEMs seek scalable alternatives to single-country concentration, India is positioned to strengthen its role as a strategic electronics manufacturing hub serving both domestic and international markets.

Transition Toward Higher Value Addition and Deeper Localization Across the Electronics Value Chain: The next phase of growth will increasingly focus on moving beyond assembly-led manufacturing toward higher value addition. This includes localization of printed circuit boards, mechanicals, enclosures, chargers, power modules, and select semiconductor-linked activities such as packaging, testing, and advanced materials. As production volumes scale and supplier ecosystems mature, manufacturers will seek to improve margins and competitiveness by reducing import dependence and increasing domestic sourcing depth. Players that successfully integrate backward into components and sub-assemblies will be better positioned to capture long-term value and withstand global supply volatility.

Growing Importance of Export-Oriented Manufacturing and Global OEM Integration: While domestic demand remains the anchor, export-oriented electronics manufacturing will become a more important growth lever through 2035. India is increasingly being integrated into global OEM supply chains for smartphones, IT hardware, automotive electronics, and industrial electronics. Export competitiveness will depend on consistency of policy frameworks, cost structures, quality compliance, and logistics efficiency. Manufacturers aligned with global quality standards, multi-country sourcing strategies, and long-term OEM programs will benefit disproportionately from this shift.

Expansion of EMS and Platform-Based Manufacturing Models to Support Scale and Flexibility: Electronics Manufacturing Services (EMS) players will continue to play a central role in scaling India’s electronics output. OEMs are expected to increasingly rely on EMS partners to manage high-volume programs, frequent product refresh cycles, and multi-SKU complexity. Platform-based manufacturing models that allow rapid product switching, modular assembly, and standardized testing will support faster time-to-market and improved asset utilization. EMS providers with strong balance sheets, automation capabilities, and supply chain integration will consolidate their competitive position.

Rising Adoption of Automation, Digital Manufacturing, and Quality Systems: As manufacturing complexity increases and labor cost advantages gradually narrow, electronics manufacturers will invest more aggressively in automation, digital process control, and advanced quality systems. Surface-mount technology optimization, automated testing, real-time yield monitoring, and predictive maintenance will become increasingly important for maintaining competitiveness. Digitalization across planning, production, and quality assurance will help manufacturers improve consistency, reduce rework, and meet export-grade reliability requirements.

India Electronics Manufacturing Market Segmentation

By Product Category

• Mobile Phones & Wearables

• Consumer Electronics & Home Appliances

• IT Hardware (Laptops, Tablets, Servers)

• Automotive Electronics

• Industrial, Telecom & Other Electronics

By Manufacturing Model

• Electronics Manufacturing Services (EMS) / Contract Manufacturing

• OEM In-House Manufacturing

• ODM / Design-Led Manufacturing

• Hybrid and Platform-Based Manufacturing Models

By End-Use Industry

• Consumer & Personal Electronics

• Automotive & Mobility

• IT & Data Infrastructure

• Industrial & Power Electronics

• Telecom & Specialized Applications

By Sales & Supply Chain Structure

• Domestic Brand-Oriented Manufacturing

• Export-Oriented Manufacturing for Global OEMs

• Mixed Domestic–Export Manufacturing Programs

• Aftermarket and Replacement Electronics Manufacturing

By Region

• South India

• North India

• West India

• East India

Players Mentioned in the Report:

• Global EMS providers and contract manufacturers operating in India

• Domestic electronics manufacturing companies

• Multinational OEM captive manufacturing units

• Component manufacturers and subsystem suppliers

• Emerging semiconductor-linked manufacturing players

Key Target Audience

• Electronics manufacturers and EMS providers

• Global and domestic OEMs

• Component and materials suppliers

• Industrial park and electronics cluster developers

• Policy makers and government agencies

• Logistics and supply chain service providers

• Private equity, strategic investors, and infrastructure funds

Time Period:

Historical Period: 2019–2024

Base Year: 2025

Forecast Period: 2025–2035

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4. 1 Manufacturing Model Analysis for Electronics Manufacturing including OEM captive manufacturing, EMS/contract manufacturing, ODM models, and hybrid manufacturing setups with margins, preferences, strengths, and weaknesses

4. 2 Revenue Streams for Electronics Manufacturing Market including assembly revenues, contract manufacturing fees, value-added services, component manufacturing revenues, and export-oriented manufacturing income

4. 3 Business Model Canvas for Electronics Manufacturing Market covering OEMs, EMS providers, component suppliers, tooling and automation vendors, logistics partners, testing and certification agencies, and industrial park developers

5. 1 Global Electronics Manufacturers vs Regional and Domestic Players including multinational EMS providers, global OEM captive units, Indian contract manufacturers, and local assemblers

5. 2 Investment Model in Electronics Manufacturing Market including greenfield manufacturing plants, brownfield expansions, joint ventures, and government-incentivized investments

5. 3 Comparative Analysis of Electronics Manufacturing Supply Models by Domestic-Oriented Production and Export-Oriented Manufacturing Programs including global OEM sourcing strategies

5. 4 Electronics Spend Allocation comparing consumer electronics, automotive electronics, industrial electronics, and IT hardware with average manufacturing value contribution

8. 1 Revenues from historical to present period

8. 2 Growth Analysis by product category and by manufacturing model

8. 3 Key Market Developments and Milestones including policy initiatives, major capacity expansions, export program launches, and entry of global players

9. 1 By Market Structure including global EMS players, domestic manufacturers, and OEM captive units

9. 2 By Product Category including mobile phones, consumer electronics, IT hardware, automotive electronics, and industrial electronics

9. 3 By Manufacturing Model including EMS/contract manufacturing, OEM in-house manufacturing, and ODM models

9. 4 By End-Use Industry including consumer, automotive, industrial, telecom, and IT infrastructure

9. 5 By Value Chain Stage including PCBA, final assembly, testing, packaging, and component manufacturing

9. 6 By Export Orientation including domestic-focused manufacturing and export-oriented manufacturing

9. 7 By Client Type including global OEMs, domestic brands, and aftermarket players

9. 8 By Region including North, South, West, East, and Central India

10. 1 OEM Demand Landscape and Program Analysis highlighting anchor OEMs and volume-driven programs

10. 2 Supplier Selection and Manufacturing Location Decision Making influenced by cost, incentives, infrastructure, and ecosystem depth

10. 3 Capacity Utilization and ROI Analysis measuring plant utilization, scale economics, and margin dynamics

10. 4 Gap Analysis Framework addressing localization gaps, skill constraints, infrastructure readiness, and policy execution

11. 1 Trends and Developments including export-led manufacturing, automation adoption, and component localization

11. 2 Growth Drivers including domestic consumption growth, supply chain diversification, and policy-led incentives

11. 3 SWOT Analysis comparing India’s scale advantage versus component ecosystem limitations and execution risks

11. 4 Issues and Challenges including import dependence, infrastructure variability, skill gaps, and cost pressures

11. 5 Government Regulations covering manufacturing incentives, customs duties, quality standards, and compliance frameworks in India

12. Snapshot on Semiconductor and Component Manufacturing Ecosystem in India

12. 1 Market Size and Future Potential of electronic components, PCB manufacturing, and semiconductor-linked activities

12. 2 Business Models including component manufacturing, packaging and testing, and import-substitution models

12. 3 Delivery Models and Type of Solutions including local sourcing, global supplier integration, and technology partnerships

15. 1 Market Share of Key Players by manufacturing output and by client programs

15. 2 Benchmark of 15 Key Competitors including global EMS providers, domestic manufacturers, and OEM captive units operating in India

15. 3 Operating Model Analysis Framework comparing global EMS-led models, domestic contract manufacturing models, and OEM captive manufacturing

15. 4 Gartner Magic Quadrant positioning global leaders and emerging challengers in electronics manufacturing

15. 5 Bowman’s Strategic Clock analyzing competitive advantage through scale efficiency, differentiation, and cost leadership

16. 1 Revenues with projections

17. 1 By Market Structure including global EMS players, domestic manufacturers, and OEM captive units

17. 2 By Product Category including mobile devices, consumer electronics, IT hardware, automotive electronics, and industrial electronics

17. 3 By Manufacturing Model including EMS, OEM in-house, and ODM models

17. 4 By End-Use Industry including consumer, automotive, industrial, and telecom

17. 5 By Value Chain Stage including assembly, testing, and component manufacturing

17. 6 By Export Orientation including domestic and export-focused production

17. 7 By Client Type including global OEMs and domestic brands

17. 8 By Region including North, South, West, East, and Central India

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

We begin by mapping the complete ecosystem of the India Electronics Manufacturing Market across demand-side and supply-side participants. On the demand side, entities include domestic and global OEMs across mobile devices, consumer electronics, IT hardware, automotive electronics, industrial electronics, and telecom equipment. Demand is further segmented by end-use application (consumer, automotive, industrial, telecom), manufacturing intent (domestic market supply vs export-oriented production), and program maturity (new program launch, scale-up, or replacement cycle).

On the supply side, the ecosystem includes global and domestic electronics manufacturing services (EMS) providers, contract manufacturers, OEM captive manufacturing units, printed circuit board assembly players, component and sub-assembly suppliers, tooling and automation vendors, testing and certification agencies, logistics partners, industrial park developers, and state and central regulatory bodies. From this mapped ecosystem, we shortlist 8–12 key EMS providers and domestic manufacturers based on production scale, client portfolio, product category focus, geographic footprint, and alignment with high-volume electronics programs. This step establishes how value is created and captured across sourcing, assembly, testing, packaging, logistics, and after-sales support within the electronics manufacturing value chain.

Step 2: Desk Research

An exhaustive desk research process is undertaken to analyze the structure, evolution, and demand dynamics of the India electronics manufacturing market. This includes review of domestic electronics consumption trends, export-oriented manufacturing programs, OEM sourcing strategies, policy-driven localization initiatives, and electronics cluster development activity across key states. We analyze product-level demand patterns, manufacturing model preferences, and sourcing depth across components and sub-assemblies.

Company-level analysis includes assessment of EMS and OEM manufacturing footprints, capacity expansion plans, client concentration, backward integration initiatives, and quality and compliance capabilities. We also review regulatory frameworks, incentive structures, customs duty regimes, and certification requirements influencing manufacturing economics. The outcome of this stage is a robust industry foundation that defines segmentation logic and establishes the base assumptions required for market sizing, segmentation splits, and forward-looking scenario development.

Step 3: Primary Research

We conduct structured interviews with EMS providers, contract manufacturers, OEM sourcing teams, component suppliers, industrial park operators, logistics partners, and industry experts. The objectives are threefold: (a) validate assumptions around demand concentration by product category and end-use industry, (b) authenticate segmentation splits across manufacturing models, regions, and supply chain structures, and (c) gather qualitative insights on pricing models, capacity utilization, lead times, localization challenges, quality benchmarks, and buyer expectations.

A bottom-to-top approach is applied by estimating production volumes and average manufacturing value across key product categories and end-use segments, which are aggregated to derive the overall market view. In selected cases, discreet buyer-style interactions are conducted with EMS players and suppliers to validate field-level realities such as program onboarding timelines, scale-up constraints, supplier qualification processes, and execution risks.

Step 4: Sanity Check

The final stage integrates bottom-to-top and top-to-down approaches to cross-validate market size estimates, segmentation splits, and forecast assumptions. Demand projections are reconciled with macro indicators such as electronics consumption growth, export trends, manufacturing investment announcements, and policy-driven localization targets. Assumptions related to component availability, cost structures, labor productivity, and infrastructure readiness are stress-tested to assess their impact on manufacturing scalability.

Sensitivity analysis is conducted across key variables including export demand growth, localization pace, policy continuity, and technology adoption intensity. Market models are refined until alignment is achieved between supplier capacity, OEM sourcing requirements, and ecosystem readiness, ensuring internal consistency and robust directional forecasting through 2035.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The India electronics manufacturing market holds strong long-term potential, supported by expanding domestic demand, increasing export-oriented manufacturing programs, and sustained government focus on localization and supply chain resilience. India’s scale of consumption, improving manufacturing infrastructure, and integration into global OEM supply chains position it as a key growth market through 2035. As value addition deepens beyond assembly, the sector is expected to capture higher economic and strategic value over the forecast period.

The market features a combination of global EMS providers, domestic contract manufacturers, and OEM captive manufacturing units. Competition is shaped by production scale, cost efficiency, quality compliance, ability to support high-volume programs, and long-term OEM relationships. EMS players play a central role in execution, while domestic manufacturers are increasingly expanding capabilities across components and sub-assemblies.

Key growth drivers include rising consumer electronics demand, mobile device penetration, automotive electrification, expansion of digital infrastructure, and policy-led manufacturing incentives. Additional momentum comes from global supply chain diversification and increasing preference for India as a secondary or alternative manufacturing base for multinational OEMs. Scale economics and export integration continue to reinforce long-term growth prospects.

Challenges include dependence on imported components, limited depth of domestic component ecosystems, infrastructure variability across manufacturing clusters, and skill gaps in advanced manufacturing processes. Policy consistency, cost competitiveness, and execution reliability will remain critical factors influencing India’s ability to scale and move up the electronics manufacturing value chain through 2035.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0