India Power Tools Market Outlook to 2029

By Technology (Electric, Pneumatic, Hydraulic, Cordless), By Application (Construction, Manufacturing, Automotive, Residential, DIY, Industrial Maintenance) and By Region

Report Overview

Report Code

TDR008

Coverage

Asia

Published

September 2024

Pages

80-100

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “India Power Tools Market Outlook to 2029 - By Market Structure (Domestic and International Brands), By Technology (Electric, Pneumatic, Hydraulic, Cordless), By Application (Construction, Manufacturing, Automotive, Residential, DIY, Industrial Maintenance) and By Region.” provides a comprehensive analysis of the power tools market in India. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the Power Tools Market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “India Power Tools Market Outlook to 2029 - By Market Structure (Domestic and International Brands), By Technology (Electric, Pneumatic, Hydraulic, Cordless), By Application (Construction, Manufacturing, Automotive, Residential, DIY, Industrial Maintenance) and By Region.” provides a comprehensive analysis of the power tools market in India. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the Power Tools Market. The report concludes with future market projections based on sales revenue, by market, product types, region, cause and effect relationship, and success case studies highlighting the major opportunities and cautions.

India Power Tools Market Overview and Size

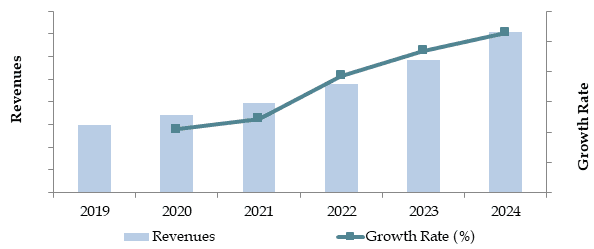

The India power tools market reached a valuation of INR 15 Billion in 2023, driven by the growing demand across construction, manufacturing, and automotive sectors, along with an increasing trend towards DIY (Do-It-Yourself) projects among consumers. The market is characterized by major players such as Bosch, Stanley Black & Decker, Makita, Hilti, and Hitachi. These companies are recognized for their extensive product portfolios, strong distribution networks, and commitment to innovation.

In 2023, Bosch introduced a new series of cordless power tools, specifically designed to cater to the Indian market’s growing preference for portable and efficient tools. This initiative aligns with the increasing industrial activities and infrastructure developments in key regions such as Maharashtra, Gujarat, and Tamil Nadu, which are driving significant demand for power tools.

Market Size for India Power Tools Industry on the Basis of Revenues in USD Million, 2018-2024

Source: TraceData Research Analysis.

What Factors are Leading to the Growth of the India Power Tools Market:

Industrial Growth: The rapid expansion of the construction, manufacturing, and automotive sectors has significantly driven the demand for power tools in India. In 2023, the construction sector alone accounted for approximately 40% of the total power tool sales. This surge is attributed to ongoing infrastructure projects and the increasing adoption of modern tools to enhance efficiency and productivity.

Urbanization and Infrastructure Development: With the continuous urbanization and large-scale infrastructure projects across India, there is a growing need for reliable and durable power tools. The government's focus on smart cities and infrastructure development has further fueled the demand, especially in key regions like Maharashtra, Gujarat, and Tamil Nadu.

Technological Advancements: The shift towards cordless power tools, which offer greater mobility and ease of use, has been a major growth driver. In 2023, cordless tools accounted for approximately 30% of total power tool sales, up from 20% in 2018. Innovations in battery technology, such as longer-lasting lithium-ion batteries, have made cordless tools more popular among professionals and DIY enthusiasts alike.

Which Industry Challenges Have Impacted the Growth of the India Power Tools Market

High Import Dependence: India's heavy reliance on imported power tools, particularly from countries like China, poses significant challenges. In 2023, approximately 60% of the power tools sold in India were imported, making the market vulnerable to supply chain disruptions, fluctuating exchange rates, and import restrictions. This dependence on imports has also led to higher costs for consumers, which can limit market growth.

Lack of Skilled Labor: The shortage of skilled labor capable of efficiently using advanced power tools remains a major challenge. A recent industry survey indicated that about 35% of construction firms face difficulties in adopting modern power tools due to a lack of trained personnel. This skills gap hampers productivity and slows down the adoption of more advanced and efficient tools.

Regulatory Compliance and Safety Standards: Stringent regulations regarding safety standards and quality control for power tools can increase operational costs for manufacturers and importers. Compliance with these standards is crucial, but it can be challenging, especially for smaller players in the market. In 2023, it was reported that around 20% of power tools in the market required additional modifications to meet safety regulations, leading to delays and added costs.

What are the Regulations and Initiatives Governing the India Power Tools Market:

BIS Certification for Power Tools: The Bureau of Indian Standards (BIS) mandates that all power tools sold in India must adhere to specific safety and performance criteria to ensure product quality and consumer safety. As of 2023, approximately 85% of power tools in the market were BIS-certified, reflecting a high level of compliance among manufacturers and importers.

Incentives for Domestic Manufacturing: Under the 'Make in India' initiative, the government has introduced several incentives to promote domestic manufacturing of power tools. These include tax benefits, subsidies, and reduced import duties on raw materials. In 2023, local production of power tools increased by 15%, driven by these government initiatives aimed at reducing import dependence and boosting local industry.

Import Tariffs and Restrictions: The Indian government has imposed import tariffs on certain categories of power tools to encourage domestic production and reduce reliance on imports. As of 2023, these tariffs stood at 10%, which has led to an increase in the prices of imported power tools. Additionally, restrictions on the import of substandard tools have been enforced to maintain quality and safety standards in the market.

India Power Tools Market Segmentation

By Market Structure: In the India Power Tools market, domestic brands are dominant within the market structure, largely due to the price-sensitive nature of the Indian consumer market. While international brands like Bosch and Stanley Black & Decker maintain a significant presence, domestic brands appeal to a broader consumer base with affordable pricing, easy availability of parts, and local manufacturing capabilities. The government's push towards self-reliance under the "Make in India" initiative has also provided a boost to domestic players.

By Type of Technology: Electric power tools lead the market due to their widespread application across industries such as construction, manufacturing, and residential use. Electric tools are popular for their efficiency, affordability, and wide availability in India. However, the demand for cordless tools is rapidly increasing as they offer greater mobility and convenience, particularly in construction and industrial maintenance. While pneumatic and hydraulic tools are used in specific industrial applications, their market share remains smaller compared to electric and cordless tools.

By Application: For application, the construction industry dominates the power tools market. India's expanding infrastructure projects, urbanization, and the construction of new residential and commercial spaces have created high demand for power tools in this segment. Manufacturing and automotive sectors also hold a significant share, as power tools are essential in assembly, maintenance, and repair work. The DIY segment, though smaller, is growing due to increased interest in home improvement activities among urban consumers, driven by the rise of e-commerce platforms

Competitive Landscape in India Power Tools Market

The India power tools market is relatively fragmented, with a mix of global and domestic players competing for market share. Major players like Bosch, Stanley Black & Decker, Makita, and Hilti dominate the space due to their strong brand presence, extensive product offerings, and commitment to innovation. However, the market is also witnessing the entrance of new firms and the growth of local manufacturers, which has diversified the market and provided consumers with more options.

| Name | Founding Year | Original Headquarters |

| Bosch Power Tools India | 1921 | Stuttgart, Germany |

| Makita Power Tools India | 1915 | Anjo, Japan |

| Stanley Black & Decker | 1843 | New Britain, Connecticut, USA |

| Hitachi Koki India (Now HiKOKI) | 1948 | Tokyo, Japan |

| Dewalt (Stanley Black & Decker) | 1924 | Baltimore, Maryland, USA |

| Ralli Wolf | 1958 | Mumbai, India |

| Cumi (Carborundum Universal Ltd.) | 1954 | Chennai, India |

| KPT (Kulkarni Power Tools) | 1976 | Pune, India |

| Powertex India | 1997 | Ahmedabad, India |

| Planet Power Tools | 2006 | Bangalore, India |

| Eastman Cast and Forge Ltd. | 1989 | Ludhiana, India |

Some of the recent competitor trends and key information about competitors include:

Bosch: As a market leader, Bosch continues to expand its product portfolio with the introduction of innovative cordless power tools. In 2023, Bosch recorded a 20% increase in sales of cordless tools, driven by the launch of its new lithium-ion battery technology, which offers extended battery life and faster charging times. The company’s strong after-sales support and extensive dealer network have further solidified its position in the market.

Stanley Black & Decker: Known for its durable and high-performance tools, Stanley Black & Decker saw a 15% growth in its Indian operations in 2023. The company has been focusing on introducing cost-effective power tools targeting small and medium enterprises (SMEs) and expanding its presence in tier 2 and tier 3 cities. Their recent collaboration with local distributors has enhanced their reach in the Indian market.

Makita: Makita, recognized for its innovation and durability, reported a 10% increase in sales of brushless motor technology tools in 2023. These tools are designed to offer higher efficiency and longevity, making them popular among professionals in the construction and manufacturing sectors. Makita’s investment in local manufacturing capabilities has also helped in reducing costs and improving market responsiveness.

Hilti: Hilti’s focus on high-end construction tools and solutions has earned it a strong reputation among professional users. In 2023, Hilti achieved a 12% growth in sales, particularly in urban regions where large infrastructure projects are underway. The company’s emphasis on customer support and specialized training for tool usage has contributed to its success in the competitive Indian market.

Hitachi: Hitachi continues to be a significant player in the power tools market, particularly in the industrial segment. In 2023, the company introduced a new range of heavy-duty power tools aimed at the construction and manufacturing sectors, which has been well-received. Hitachi’s focus on quality and reliability has helped it maintain a steady market share.

DeWalt: DeWalt, known for its rugged and durable power tools, has been expanding its product range to include more cordless and brushless motor tools. The company saw a 13% increase in sales in 2023, driven by its focus on professional-grade tools and strategic partnerships with local distributors. DeWalt’s tools are particularly favored in the automotive and manufacturing industries for their reliability and performance.

What Lies Ahead for the India Power Tools Market?

The India power tools market is projected to grow steadily by 2029, exhibiting a healthy CAGR during the forecast period. This growth is expected to be driven by the expansion of the construction and manufacturing sectors, increasing urbanization, and the rising adoption of advanced technologies in various industries.

Adoption of Cordless and Smart Tools: As the demand for convenience and mobility increases, there will be a significant shift towards cordless power tools. The adoption of smart tools integrated with IoT and AI technologies is also expected to rise, offering advanced features such as predictive maintenance, remote monitoring, and enhanced safety. These tools will be particularly appealing to professional users in construction and manufacturing, driving market growth.

Expansion of Infrastructure Projects: The ongoing and planned infrastructure projects across India, including government initiatives like smart cities, will continue to boost the demand for power tools. This trend will particularly benefit manufacturers of heavy-duty tools designed for large-scale construction and industrial applications.

Growth in DIY and Consumer Segments: The DIY (Do-It-Yourself) culture is gaining traction in India, especially among urban consumers. This trend, coupled with increasing consumer awareness and the availability of affordable power tools, is expected to drive growth in the consumer segment. Online platforms will play a crucial role in making these tools more accessible to a broader audience.

Focus on Sustainable Practices: There is a growing emphasis on sustainability within the power tools market, with manufacturers increasingly focusing on producing energy-efficient tools and reducing the carbon footprint of their products. Initiatives such as the use of recyclable materials in tool manufacturing and eco-friendly packaging are likely to influence buying decisions, especially among environmentally conscious consumers.

Expansion of E-commerce and Online Sales Channels: The rise of e-commerce platforms will continue to be a major growth driver for the power tools market in India. Online sales channels provide consumers with easy access to a wide range of products, competitive pricing, and customer reviews, which are expected to contribute significantly to market expansion, particularly in tier 2 and tier 3 cities.

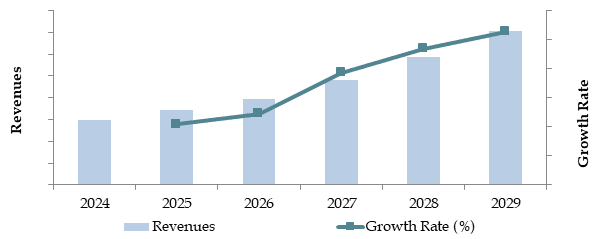

Future Outlook and Projections for India Power Tools Market on the Basis of Revenues in USD Million, 2024-2029

Source: TraceData Research Analysis

India Power Tools Market Segmentation

- By Market Structure:

- International Brands

- Domestic Brands

- By Power Source:

- Electric Tools

- Pneumatic Tools

- Hydraulic Tools

- Cordless Tools

- Manual Tools

- By Application:

- Construction

- Manufacturing

- Automotive

- Residential

- DIY (Do-It-Yourself)

- Industrial Maintenance

- By Region:

- Northern India

- Southern India

- Central India

- Western India

- Eastern India

- By Distribution Channel:

- Dealer Network

- Direct Sales

- Online Sales

Players Mentioned in the Report:

- Bosch Power Tools India

- Makita Power Tools India

- Stanley Black & Decker

- Hitachi Koki India (Now HiKOKI)

- Dewalt (Stanley Black & Decker)

- Ralli Wolf

- Cumi (Carborundum Universal Ltd.)

- KPT (Kulkarni Power Tools)

- Powertex India

- Planet Power Tools

- Eastman Cast and Forge Ltd.

Key Target Audience:

- Power Tool Manufacturers

- Construction Companies

- Automotive Manufacturers

- Online Marketplaces

- B2B Distributors

- Government and Regulatory Bodies (e.g., Bureau of Indian Standards)

- Research and Development Institutions

Time Period:

- Historical Period: 2018-2023

- Base Year: 2024

- Forecast Period: 2024-2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Market Overview and Genesis for India Power Tools Market

4.2. Value Chain Process-Role of Entities, Stakeholders, Gross Margins, Net Margins and Challenges Faced

4.3. Business Model Canvas for India Power Tools Market

7.1. Revenues, 2018-2024

8.1. By Market Structure (International and Domestic Brands), 2023-2024P

8.2. By Type of Technology (Electric, Pneumatic, Hydraulic, Cordless), 2023-2024P

8.3. By Application (Construction, Manufacturing, Automotive, Residential, DIY, Industrial Maintenance), 2023-2024P

8.4. By Region (Northern, Southern, Central, Western, Eastern India), 2023-2024P

8.5. By Distribution Channels (Dealer Network, Direct Sales and Online Sales), 2023-2024P

8.6. By Price Category, 2023-2024P

9.1. Customer Landscape and Cohort Analysis

9.2. Customer Journey and Decision Making

9.3. Need, Desire, and Pain Point Analysis

9.4. Gap Analysis Framework

10.1. Trends and Developments for India Power Tools Market

10.2. Growth Drivers for India Power Tools Market

10.3. SWOT Analysis for India Power Tools Market

10.4. Issues and Challenges for India Power Tools Market

10.5. Government Regulations and Licensing Requirement for India Power Tools Market

13.1. Market Share of Major Players in India Power Tools Market, 2023

13.1.1. By Electric Power Tools, 2023

13.1.2. By Hydraulic Power Tools Market, 2023

13.1.3. By Pneumatic Power Tools Market, 2023

13.2. Benchmark of Key Competitors in India Power Tools Market Basis Operational and Financial Variables

13.3. Product SKUs and Pricing Analysis

13.4. Strengths and Weaknesses

13.5. Operating Model Analysis Framework

13.6. Gartner Magic Quadrant

13.7. Bowmans Strategic Clock for Competitive Advantage

14.1. Revenues, 2025-2029

15.1. By Players (International and Domestic Brands), 2025-2029

15.2. By Type of Technology (Electric, Pneumatic, Hydraulic, Cordless), 2025-2029

15.3. By Application (Construction, Manufacturing, Automotive, Residential, DIY, Industrial Maintenance), 2025-2029

15.4. By Region (Northern, Southern, Central, Western, Eastern India), 2025-2029

15.5. By Distribution Channels (Dealer Network, Direct Sales and Online Sales), 2025-2029

15.6. By Price Category, 2025-2029

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the Ecosystem: We begin by mapping the entire ecosystem of the India Power Tools Market, identifying all key demand-side and supply-side entities. This includes manufacturers, distributors, retailers, end-users, and regulatory bodies. Based on this ecosystem, we shortlist leading 5-6 key manufacturers in the country, using criteria such as financial performance, production capacity, and market share.

Information Sourcing: We source data through industry articles, multiple secondary sources, and proprietary databases to perform desk research. This initial step allows us to gather industry-level information and understand the overall market dynamics.

Step 2: Desk Research

Exhaustive Desk Research: We engage in an in-depth desk research process, referencing diverse secondary and proprietary databases. This comprehensive approach enables us to analyze market trends, sales revenues, the number of market players, pricing levels, and demand patterns. Additionally, we examine company-level data through press releases, annual reports, financial statements, and other relevant documents to construct a solid foundation for understanding the market and its key players.

Step 3: Primary Research

In-Depth Interviews: We conduct a series of in-depth interviews with C-level executives and other key stakeholders from various companies within the India Power Tools Market, as well as with end-users. These interviews serve multiple purposes: validating market hypotheses, authenticating statistical data, and gathering valuable operational and financial insights from industry representatives. A bottom-up approach is employed to evaluate volume sales for each player, which is then aggregated to estimate the overall market size.

Disguised Interviews for Validation: As part of our validation strategy, we execute disguised interviews, where our team approaches companies under the guise of potential customers. This method allows us to cross-verify the operational and financial information provided by company executives against data available in secondary databases. These interactions also help us gain a comprehensive understanding of revenue streams, value chains, processes, pricing, and other critical factors.

Step 4: Sanity Check

- Sanity Check Process: We perform a thorough sanity check process, employing both bottom-up and top-down analysis along with market size modeling exercises. This step ensures that the data collected is accurate, reliable, and consistent with market realities. Any discrepancies are addressed through additional research and validation, thereby reinforcing the credibility of our findings and projections.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The India power tools market is poised for significant growth, projected to reach a valuation of INR 25 Billion by 2029. This growth is driven by the rapid expansion of the construction and manufacturing sectors, increasing urbanization, and a rising trend towards DIY (Do-It-Yourself) activities among consumers. The market's potential is further enhanced by technological advancements and the growing adoption of cordless and smart tools.

The India Power Tools Market features several key players, including Bosch, Stanley Black & Decker, and Makita. These companies dominate the market due to their extensive product portfolios, strong distribution networks, and commitment to innovation. Other notable players include Hilti, Hitachi, and DeWalt, which are recognized for their high-performance tools and strong market presence.

The primary growth drivers include the booming construction and manufacturing sectors, which require efficient and reliable tools for various applications. Additionally, the increasing urbanization and infrastructure development across the country contribute to the demand for power tools. The growing popularity of DIY projects and the shift towards cordless and smart tools are also significant factors driving market growth.

The India Power Tools Market faces several challenges, including high import dependence, which makes the market vulnerable to supply chain disruptions and price fluctuations. The lack of skilled labor capable of using advanced tools efficiently is another significant challenge. Regulatory compliance, particularly with safety and quality standards, can also pose barriers to market entry and expansion. Furthermore, the price sensitivity of consumers, especially in the unorganized sector, can limit the adoption of high-end power tools.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0