Indonesia Automotive Aftermarket Service Market Outlook to 2029

By Service Providers, By Types of Services, By Vehicle Age, By Consumer Age, and By Region

Report Overview

Report Code

TDR0014

Coverage

Asia

Published

September 2024

Pages

80-100

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled "Indonesia Automotive Aftermarket Service Market Outlook to 2029 - By Market Structure, By Service Providers, By Types of Services, By Vehicle Age, By Consumer Age, and By Region" provides a comprehensive analysis of the automotive aftermarket service market in Indonesia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled "Indonesia Automotive Aftermarket Service Market Outlook to 2029 - By Market Structure, By Service Providers, By Types of Services, By Vehicle Age, By Consumer Age, and By Region" provides a comprehensive analysis of the automotive aftermarket service market in Indonesia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the market. The report concludes with future market projections based on service revenue, by market, service types, region, cause and effect relationship, and success case studies highlighting the major opportunities and cautions.

Indonesia Automotive Aftermarket Service Market Overview and Size

The Indonesia automotive aftermarket service market grew at a value of IDR 85 Trillion in 2023, driven by increasing road vehicles, a greater consciousness toward vehicle maintenance, and the increasing availability of both preventive and corrective services. The market is highly concentrated, with the major players being Auto2000, Shop&Drive, CARfix, Astra Otoparts, and independent garages, which are known for their huge networks, diverse portfolios, and customer-centric solutions.

Auto2000 introduces new service packages in the coming year, 2023, to improve customers' experience; the services have been channeled to preventive maintenance services. The main markets would still be Jakarta and Surabaya due to the high ownership rates in those cities and proper automotive infrastructure.

Market Size for Indonesia Automotive Aftermarket Service Industry on the Basis of Revenue in IDR Billion, 2018-2024

What Factors are Leading to the Growth of Indonesia Automotive Aftermarket Service Market:

Economic Factors: Economic growth in Indonesia has strengthened demand for automotive aftermarket services. Vehicle ownership tends to be on the rise, and a high contribution from the middle class in 2023 also contributed notably to the growth of this sector, as most vehicle owners reached out for cheaper ways of maintaining and repairing their vehicles. Many consumers prefer extending the life of their vehicles through aftermarket services instead of purchasing new ones.

Increasing Vehicle Population: The overall increase of vehicles in Indonesia's roads due to the growing middle-income population and urbanization drives the aftermarket service market. With increasing vehicle ownership, regular maintenance and repairs are on the rise, and even upgrades have broadened their horizons in major cities like Jakarta, Surabaya, and Bandung.

Digitalization: Digitalization is about the development of digital platforms that have shaped the outlook of the Indonesian aftermarket service by making it very easy for consumers to access these services. In 2023 alone, 30% of all bookings made in the aftermarket service were booked through digital platforms, implying a modern trend of convenience through online ways. These platforms make it possible for customers to compare prices of services, read customer reviews, and schedule an appointment with an auto technician, therefore providing transparency and comfort, and driving market growth.

Which Industry Challenges Have Impacted the Growth for Indonesia Automotive Aftermarket Service Market:

Quality and Trust Issues: Quality and trust issues remain one of the biggest concerns in Indonesia regarding the quality of aftermarket services, counterfeit, or low-quality parts being used. Indeed, in a recent industry survey, 45% of consumers claimed not to use independent garages for fear of low-quality repairs using non-genuine parts. A trust issue is affecting customer retention and could well deter a considerable segment of possible users.

Challenges from Regulations: Major challenges include stern regulations regarding vehicle emissions and safety standards. In 2023, about 18% of vehicles failed to meet the minimum regulatory requirement for maintenance services, mainly older models. These are very costly for service providers to provide support for, hence making it difficult for certain kinds of vehicles and adding to the compliance overhead.

Shortage of Skilled Labor: The lack of skilled technicians has adversely impacted the growth in Indonesia's automotive aftermarket service industry. Almost 40% of the service providers reported that hiring qualified personnel was difficult, affecting their capacity to offer advanced repairs and maintenance services, especially for newer vehicle models that need specialized expertise.

What are the Regulations and Initiatives which have Governed the Indonesia Automotive Aftermarket Service Market:

Vehicle Inspection Regulations: The Indonesian government requires periodic vehicle inspections to be carried out to ensure that vehicles meet minimum requisite safety and environmental standards. The inspections involve brakes, tires, and emissions, among other things. In 2023, about 70% of the vehicles passed during the first attempt, which indicates a relatively high level of compliance by the vehicles in the market.

Regulations on Replacement Parts: The government has set up regulations requiring the use of certified replacement parts for repairs and maintenance, especially in critical systems such as brakes and airbags. These are intended to improve safety and reduce the use of counterfeit or substandard parts. In 2023, the enforcement of these rules raised demand for certified parts, guaranteeing better quality control across the industry.

Government Incentives for Electric Vehicle Services: At a time when there is an ongoing rush towards electric vehicle adoption in Indonesia, the country's government is initiating various programs on the ground such as subsidies to promote the setting-up of EV service centers and reductions in taxes related to parts which are exclusively applicable in the maintenance of EVs. In 2023, this segment accounted for around 2% in the revenue created in the after-sale services, but this is estimated to increase soon with these given incentives.

Indonesia Automotive Aftermarket Service Market Segmentation

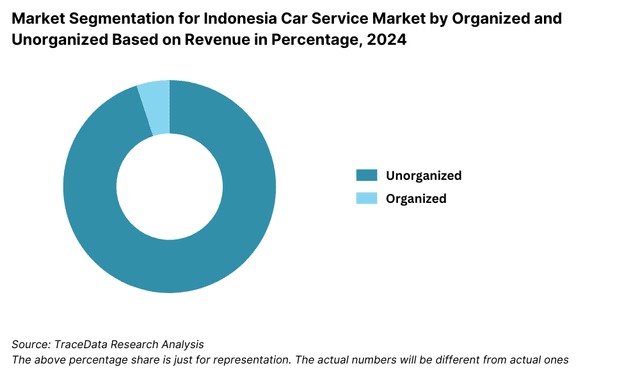

By Market Structure: Organized service centres dominate the market. They have large service networks helped by certified technicians and original spare parts. The centre, therefore, would attract customers seeking reliable and good quality of services at an assurance of warranty covers. Simultaneously, independent garages have taken a major chunk of the market for two reasons: their competitiveness in prices, especially in suburban and rural areas where big service centers are usually not available. Local garages are also preferred for their personalized service and flexible payment options, which appeal to cost-conscious customers.

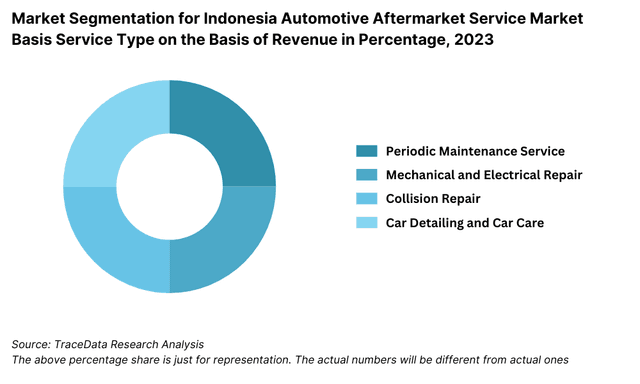

By Type of Services: Pre-service maintenance oil changes and rotations top the list since more consumers maintain their vehicles running longer by lengthening the lifespan of their cars. Corrective repairs also contribute to a great extent to the business, including brake repairs or engine overhauls, for which older ones are more in demand. Car accessories and upgrades comprise much of this market, but primarily from the younger consumers who wish to personalize their own vehicles.

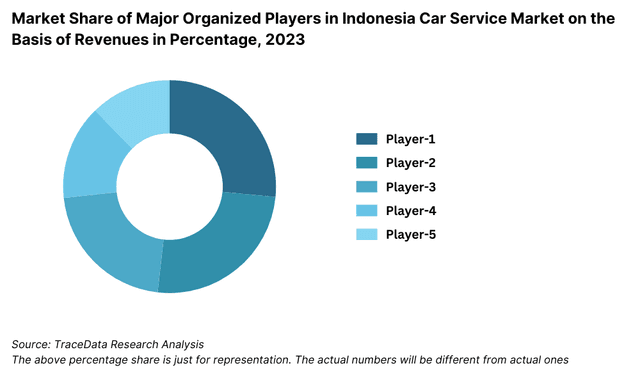

By Service Providers: Auto2000 leads the market with its great reputation in full-service packages, wide service networks, and very high customer satisfaction. Astra Otoparts and Shop&Drive are also major competitors as they have taken the quality of service seriously while offering a vast array of products. CARfix is an emerging player that specializes in competitive pricing and speedy service delivery, especially in cities.

Competitive Landscape in Indonesia Automotive Aftermarket Service Market

The Indonesia automotive aftermarket service market is highly fragmented, with several established players leading the space. However, the entry of new digital platforms and the proliferation of independent garages have diversified the market, offering consumers a wider array of choices and services. Major players include Auto2000, Shop&Drive, CARfix, and Astra Otoparts, which dominate the organized sector, while smaller independent garages thrive in the unorganized sector.

| Name | Founding Year | Headquarters |

| Auto2000 | 1975 | Jakarta, Indonesia |

| Shop&Drive | 1998 | Jakarta, Indonesia |

| Bosch Car Service Indonesia | 1921 | Jakarta, Indonesia |

| Supercar.id | 2014 | Jakarta, Indonesia |

| Doctor Mobil | 2014 | Tangerang, Indonesia |

| MekaCarCare | 2015 | Jakarta, Indonesia |

| Mobil88 | 1988 | Jakarta, Indonesia |

| Otoklix | 2019 | Jakarta, Indonesia |

| Carfix | 2017 | Semarang, Central Java |

| Ahass (Honda Authorized Service Station) | 1971 | Jakarta, Indonesia |

Some recent competitor trends and key information about competitors include:

Auto2000: With a wide network of service centers and customer-focused service packages, Auto2000 has been able to maintain its strong position in the market. In 2023, preventive maintenance service bookings increased by 12% due to efforts to promote regular vehicle upkeep. Their focus on integrating digital tools into the service booking process has also improved customer convenience.

Shop&Drive: Shop&Drive is one of the market leaders in the automotive services sector. Revenues for this company have grown 20% over the year 2023, a fact that majorly contributed due to their well-calculated expansion plan to suburban territories and new offerings like on-the-spot vehicle servicing, where the speed and reliability of their services have started attracting more of the urban dwellers.

CARfix: As the services of CARfix are cheaper compared to others with faster service. Customer flow within the company experienced a 15% increase within 2023, especially during metropolitan cities, in terms of Jakarta and Semarang. By this method, CARfix targeted budget-buyers and already obtained a marvelous market share at the capital of metropolitan areas.

Astra Otoparts: One of the biggest distributors of automotive parts and services in the country, Astra Otoparts has spread its service bouquet through new lines of products along with a larger national network of its services. By the end of 2023, Astra Otoparts had seen an increase of 10% in premium parts and service revenue due to better demand for quality repairs, authentic OEM parts.

What Lies Ahead for Indonesia Automotive Aftermarket Service Market?

The Indonesia automotive aftermarket service market is expected to witness steady growth with a healthy CAGR throughout the forecast period, up to 2029. Growth will be driven by increasing vehicle ownership, consumer awareness of regular vehicle maintenance, and advancements in digital service platforms.

- Shift to Electric Vehicles: While the Indonesian government is still encouraging electric mobility, there should be a gradual ramp-up in demand for specialized EV maintenance and repair services. This will be further helped through incentives offered by the government for electric vehicles and building of more EV-related infrastructure such as charging stations and service centers capable of handling EV-specific repairs.

Technology Integration: Advanced technologies like AI, IoT, and big data analytics will transform the aftermarket service industry in diagnostics, maintenance, and customer service. Improved diagnostics, efficient servicing, and increased transparency towards customers will result in more trust and loyalty among consumers.

Organized Service Centers: The market is shifting more towards organized service centers that offer both certified parts and skilled technicians for warranty-backed services. Organized service centers have seen a greater demand in urban markets where quality and reliability are looked upon by the consumers. Certified pre-owned vehicle programs will also accelerate growth in the organized service center because it gives the customers assurance of quality and after-sales service.

Focus on Sustainable Practices: The Indonesia Automotive Aftermarket Service Market is going on to add a sustainable note as service providers increasingly adopt environmentally friendly practices: using recycled materials for repairs, using energy-efficient service processes, and reducing wastes. As environmental awareness among consumers continues to increase, service centers will likely have a competitive advantage if they highlight sustainability practices.

Future Outlook and Projections for Indonesia Multi Brand Car Service Market on the Basis of Revenues in USD Million, 2024-2029

Indonesia Automotive Aftermarket Service Market Segmentation

By Market Structure:

Auction Companies

C2C

Local Dealers

Multi-brand Non-franchise Dealerships

OEM Certified Dealers

Organized Sector

Unorganized Sector

Commercial Vehicles

By Manufacturer:

Honda

Toyota

Daihatsu

Mitsubishi

Nissan

Hyundai

BMW

Mercedes-Benz

By Type of Services:

Preventive Maintenance

Corrective Repairs

Accessories

By Age of Vehicle:

5 years

1-2 years

3-5 years

By Age of Consumer:

18-34

35-54

55+

By Region:

Northern

Southern

Central

Western

Eastern

Players Mentioned in the Report:

Auto2000

Shop&Drive

Bosch Car Service Indonesia

Supercar.id

Doctor Mobil

MekaCarCare

Mobil88

Otoklix

Carfix

Ahass (Honda Authorized Service Station)

Key Target Audience:

Automotive Service Providers

Vehicle Owners

Digital Service Platforms

Regulatory Bodies

Research and Development Institutions

Time Period:

Historical Period: 2018-2023

Base Year: 2024

Forecast Period: 2024-2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1 Delivery Model Analysis for Automotive Aftermarket Services including authorized service centers, independent garages, multi-brand service chains, mobile service units, and digital aggregator platforms with margins, preferences, strengths, and weaknesses

4.2 Revenue Streams for Automotive Aftermarket Service Market including periodic maintenance services, mechanical repairs, body and paint services, diagnostics, spare parts sales, and value-added services

4.3 Business Model Canvas for Automotive Aftermarket Service Market covering OEMs, authorized dealers, independent workshops, spare parts distributors, digital platforms, and fleet service partners5.1 Authorized OEM Service Centers vs Independent and Multi-brand Workshops including Astra-authorized networks, Toyota and Honda dealers, versus independent garages and national service chains

5.2 Investment Model in Automotive Aftermarket Service Market including franchise-led expansion, company-owned workshops, asset-light digital platforms, and hybrid models

5.3 Comparative Analysis of Automotive Aftermarket Service Delivery by Walk-in Customers, Fleet Contracts, and Digital or App-based Booking Channels

5.4 Vehicle Ownership and Maintenance Budget Allocation comparing routine servicing, repairs, and discretionary upgrades with average annual spend per vehicle8.1 Revenues from historical to present period

8.2 Growth Analysis by service type and by vehicle segment

8.3 Key Market Developments and Milestones including expansion of multi-brand service chains, digitization of bookings, and EV servicing readiness initiatives9.1 By Market Structure including authorized service centers, independent garages, and organized multi-brand chains

9.2 By Service Type including routine maintenance, mechanical repairs, body and paint, diagnostics, and value-added services

9.3 By Vehicle Type including passenger cars, two-wheelers, light commercial vehicles, and heavy commercial vehicles

9.4 By Customer Segment including individual vehicle owners, fleet operators, ride-hailing vehicles, and corporate customers

9.5 By Vehicle Age including new vehicles under warranty, mid-life vehicles, and aging vehicles

9.6 By Service Mode including workshop-based servicing, doorstep or mobile servicing, and accident repair centers

9.7 By Pricing Tier including economy, mid-range, and premium service offerings

9.8 By Region including Java, Sumatra, Kalimantan, Sulawesi, and Eastern Indonesia10.1 Vehicle Owner Landscape and Cohort Analysis highlighting two-wheeler dominance and growing passenger car base

10.2 Service Provider Selection and Purchase Decision Making influenced by trust, price transparency, warranty, proximity, and digital convenience

10.3 Service Effectiveness and ROI Analysis measuring vehicle uptime, maintenance cost savings, and resale value impact

10.4 Gap Analysis Framework addressing skill shortages, counterfeit spare parts risk, uneven service quality, and digital adoption gaps11.1 Trends and Developments including growth of multi-brand service chains, digital aggregators, predictive maintenance, and EV service capability development

11.2 Growth Drivers including rising vehicle parc, aging vehicles, urban mobility demand, and expansion of ride-hailing fleets

11.3 SWOT Analysis comparing authorized service networks versus independent workshops on cost, quality, and reach

11.4 Issues and Challenges including price competition, informal sector dominance, technician availability, and spare parts authenticity

11.5 Government Regulations covering vehicle service standards, emissions compliance, safety inspections, and consumer protection norms in Indonesia12.1 Market Size and Future Potential of online service aggregators, digital bookings, and connected vehicle diagnostics

12.2 Business Models including marketplace-led platforms, subscription-based maintenance plans, and fleet service contracts

12.3 Delivery Models and Type of Solutions including app-based booking, doorstep servicing, telematics-enabled diagnostics, and loyalty programs15.1 Market Share of Key Players by revenues and by service network size

15.2 Benchmark of 15 Key Competitors including authorized OEM dealer networks, Astra Otoparts service chains, Planet Ban, Shop & Drive, independent garage networks, digital service aggregators, and regional workshop groups

15.3 Operating Model Analysis Framework comparing authorized dealership models, independent workshops, franchise chains, and digital-first platforms

15.4 Gartner Magic Quadrant positioning organized service chains and digital platforms versus traditional workshop operators

15.5 Bowman’s Strategic Clock analyzing competitive advantage through service differentiation versus low-cost positioning16.1 Revenues with projections

17.1 By Market Structure including authorized service centers, organized multi-brand chains, and independent workshops

17.2 By Service Type including maintenance, repairs, body and paint, and diagnostics

17.3 By Vehicle Type including passenger cars, two-wheelers, and commercial vehicles

17.4 By Customer Segment including individual owners and fleet operators

17.5 By Vehicle Age including new, mid-life, and aging vehicles

17.6 By Service Mode including workshop-based and doorstep servicing

17.7 By Pricing Tier including economy, mid-range, and premium services

17.8 By Region including Java, Sumatra, Kalimantan, Sulawesi, and Eastern Indonesia

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities for the Indonesia Automotive Aftermarket Service Market. Based on this ecosystem, we will shortlist the leading 5-6 service providers in the country using their financial performance, service capacity, and market presence as criteria.

Information sourcing is conducted through industry reports, secondary research articles, and proprietary databases to gather comprehensive industry-level insights.

Step 2: Desk Research

We engage in an extensive desk research process by reviewing diverse secondary and proprietary databases. This enables us to analyze the market thoroughly, examining aspects such as revenue trends, the number of market players, pricing dynamics, and service demand. The research also includes detailed reviews of company-level data, derived from annual reports, press releases, financial statements, and other official documents, aimed at building a strong understanding of the market landscape and its key entities.

Step 3: Primary Research

We conduct in-depth interviews with senior executives and other stakeholders representing various companies and end-users in the Indonesia Automotive Aftermarket Service Market. These interviews serve to validate market assumptions, verify statistical data, and uncover valuable operational and financial insights. We take a bottom-up approach to estimate volume sales for each service provider and aggregate these findings to calculate the overall market size.

As part of our validation process, we conduct disguised interviews, approaching companies as potential customers to verify the operational and financial information shared by executives. This helps cross-check secondary data and gives us a deeper understanding of revenue streams, pricing, value chains, and other factors shaping the market.

Step 4: Sanity Check

- We undertake both top-down and bottom-up market size modeling to validate the accuracy of our findings. This includes cross-referencing different data points and performing sanity checks to ensure consistency in our analysis.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Indonesia Automotive Aftermarket Service Market is set for significant growth, driven by the rising vehicle population, increasing consumer awareness of regular maintenance, and expanding digital platforms. The market is projected to grow steadily, reflecting increasing demand for both preventive and corrective services.

The key players in the market include Auto2000, Shop&Drive, Astra Otoparts, and CARfix. These companies lead the market due to their wide service networks, strong brand recognition, and comprehensive service offerings.

Key growth drivers include the rising number of vehicles on the road, increased consumer focus on vehicle maintenance, and the integration of digital platforms for service bookings. Government initiatives promoting electric vehicles and sustainability practices are also expected to contribute to market expansion.

The market faces challenges such as quality concerns related to the use of counterfeit parts, regulatory compliance with emissions and safety standards, and a shortage of skilled technicians. These issues can impact both service quality and availability, posing barriers to market growth.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0