Israel Auto Finance Market Outlook to 2029

By Market Structure, By Lenders, By Vehicle Type, By Loan Tenure, By Consumer Age Group, and By Region

Report Overview

Report Code

TDR0122

Coverage

Middle East

Published

February 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Israel Auto Finance Market Outlook to 2029 - By Market Structure, By Lenders, By Vehicle Type, By Loan Tenure, By Consumer Age Group, and By Region.” provides a comprehensive analysis of the auto finance market in Israel. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer-level profiling, issues and challenges, and comparative landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the Auto Finance Market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Israel Auto Finance Market Outlook to 2029 - By Market Structure, By Lenders, By Vehicle Type, By Loan Tenure, By Consumer Age Group, and By Region.” provides a comprehensive analysis of the auto finance market in Israel. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer-level profiling, issues and challenges, and comparative landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the Auto Finance Market. The report concludes with future market projections based on loan disbursement volume, by market, vehicle types, region, cause and effect relationship, and success case studies highlighting the major opportunities and cautions.

Israel Auto Finance Market Overview and Size

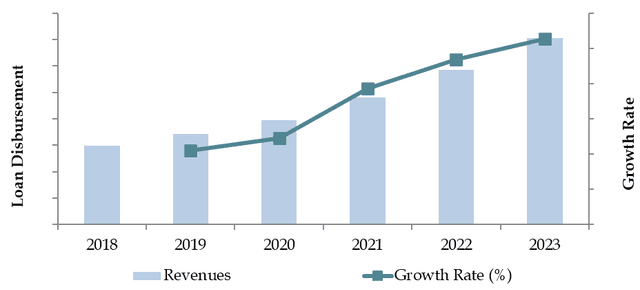

The Israel auto finance market reached a valuation of ILS 30 Billion in 2023, driven by the increasing demand for vehicle ownership, supportive financing schemes, and evolving consumer preferences towards flexible auto loan options. The market is characterized by major players such as Bank Leumi, Bank Hapoalim, Direct Finance, Clal Finance, and Union Bank. These institutions are recognized for their wide range of financing products, competitive interest rates, and customer-centric lending services.

In 2023, Direct Finance introduced a new digital auto loan platform aimed at streamlining the loan application process and enhancing customer experience. This initiative seeks to leverage the growing digital adoption in Israel and provide a more convenient auto financing solution. Tel Aviv and Haifa are key markets due to their high population density and robust automotive market demand.

Market Size for Israel Auto Finance Industry on the Basis of Loan Disbursement Value in USD Billion, 2018-2024

What Factors are Leading to the Growth of Israel Auto Finance Market:

Economic Factors: The steady economic growth and the increasing cost of living have influenced consumer preference for financed vehicle purchases. In 2023, financed auto purchases accounted for approximately 60% of total car sales in Israel, as financing options provide an opportunity for consumers to spread costs over time. This trend is particularly evident among middle-income households aiming to maintain cash flow while acquiring vehicles.

Growing Middle Class: The expanding middle class, with rising disposable incomes, is increasingly turning to auto finance solutions to access better and newer vehicle models. The middle-income population in Israel has grown by 10% in recent years, driving demand for flexible and affordable auto loan products. Auto finance serves as a critical enabler for car ownership among this demographic.

Digitalization: The rise of digital banking and financial services has transformed the auto finance market, improving transparency and accessibility. In 2023, around 35% of auto loan applications in Israel were submitted online, reflecting a growing trend towards digital financial services. Online platforms offer quick loan approvals, personalized interest rates, and a seamless customer experience, significantly boosting market growth by catering to tech-savvy consumers.

Which Industry Challenges Have Impacted the Growth of the Israel Auto Finance Market

Credit Risk and Loan Defaults: Managing credit risk and loan defaults is a significant challenge for the auto finance market in Israel. With economic fluctuations and rising interest rates, financial institutions face increased risks of loan delinquencies. In 2023, approximately 15% of auto loans were reported to be in arrears, highlighting the need for stringent credit assessment processes and risk management strategies.

Regulatory Compliance: Stringent regulations related to consumer lending, interest rate caps, and data privacy have added complexity to the auto finance market. The Bank of Israel’s strict regulatory requirements mandate detailed disclosures and transparent lending practices, which, while protecting consumers, also increase compliance costs for financial institutions. These regulations, if not adhered to, could result in penalties and affect profitability.

Rising Competition from Leasing Alternatives: The growing popularity of vehicle leasing, especially among corporate clients and high-income consumers, poses a challenge to traditional auto finance models. In 2023, vehicle leasing captured approximately 30% of the total automotive financing market in Israel. Leasing offers benefits such as lower upfront costs and maintenance support, making it a preferred option over traditional auto loans for some consumer segments.

What are the Regulations and Initiatives that have Governed the Market:

Interest Rate Regulations: The Bank of Israel enforces regulations that limit the maximum interest rates applicable to auto loans. These rules are designed to protect consumers from predatory lending practices but also restrict the flexibility of lenders in pricing loans according to borrower risk profiles. In 2023, the average interest rate for auto loans was capped at 8%, balancing consumer affordability with lender profitability.

Consumer Protection Policies: Strict consumer protection laws require lenders to provide detailed loan agreements, including full disclosure of interest rates, fees, and repayment schedules. These policies ensure that borrowers have a clear understanding of their financial obligations, which has enhanced market transparency and reduced the risk of disputes. In 2023, compliance with these regulations reached 95% among major financial institutions.

Incentives for Green Vehicle Financing: To support Israel’s sustainability goals, the government has introduced incentives for financing electric and hybrid vehicles. These include reduced interest rates, tax breaks, and subsidies for eco-friendly vehicles. In 2023, green auto loans accounted for 10% of the total auto financing market, showcasing the positive impact of these incentives.

Israel Auto Finance Market Segmentation

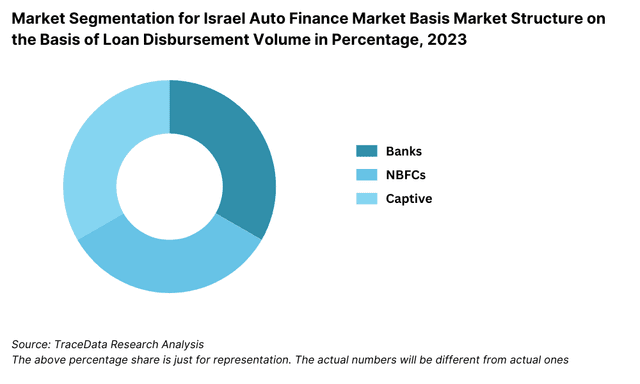

By Market Structure: Traditional banking institutions dominate the market due to their robust financial infrastructure, trustworthiness, and comprehensive product offerings. Banks like Bank Leumi, Bank Hapoalim, and Mizrahi-Tefahot Bank lead this segment by providing competitive interest rates, tailored loan products, and a wide range of financing options. Non-banking financial companies (NBFCs) such as Clal Finance and Direct Finance also hold a significant share due to their quicker loan approval processes, flexible financing options, and focus on niche markets like used vehicle financing. Digital lending platforms are gaining traction, offering convenience, speed, and personalized loan offers through innovative technology solutions.

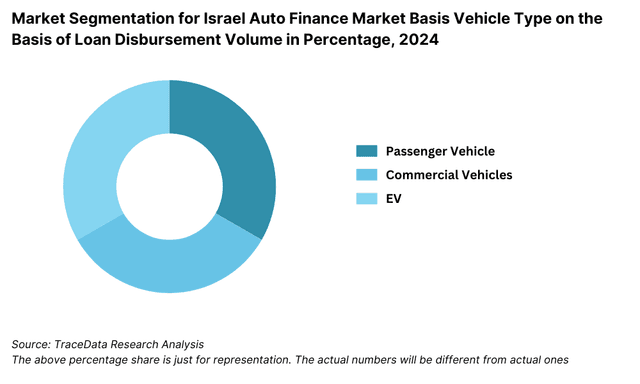

By Vehicle Type: New vehicle financing leads the market due to strong demand for the latest models and attractive financing schemes offered by both banks and NBFCs. This segment benefits from lower interest rates and promotional offers. Used vehicle financing is also growing, particularly among cost-conscious consumers looking for affordable car ownership options. Financial institutions offer tailored loan products for used vehicles, albeit often with higher interest rates due to associated risks.

By Loan Tenure: Medium-term loans (3 to 5 years) dominate the market, offering a balance between affordable monthly payments and reasonable interest costs. Short-term loans (up to 3 years) are preferred by high-income consumers aiming to reduce total interest payments. Long-term loans (above 5 years) attract customers seeking lower monthly installments, often for high-value vehicle purchases.

Competitive Landscape in Israel Auto Finance Market

The Israel auto finance market is moderately concentrated, with major financial institutions leading the space. However, the emergence of non-banking financial companies (NBFCs) and digital lending platforms has diversified the market, offering consumers a wider range of financing options and services. Key players include Bank Leumi, Bank Hapoalim, Direct Finance, Clal Finance, and Union Bank.

Key Players in the Israel Auto Finance Market

Name | Founding Year | Original Headquarters |

|---|---|---|

Leumi Bank (Leumi Car Financing) | 1902 | Tel Aviv, Israel |

Bank Hapoalim (Poalim Auto Loans) | 1921 | Tel Aviv, Israel |

Direct Finance (Mimun Yashir) | 2006 | Petah Tikva, Israel |

CAL Auto Financing (Israel Credit Cards) | 1979 | Givatayim, Israel |

Union Bank of Israel (Auto Financing) | 1951 | Tel Aviv, Israel |

Oto Capital (Shlomo Group) | 1974 | Petah Tikva, Israel |

Menora Mivtachim Finance | 1935 | Tel Aviv, Israel |

Clal Finance (Clal Insurance) | 1987 | Tel Aviv, Israel |

Mizrahi-Tefahot Bank Car Loans | 1923 | Ramat Gan, Israel |

Discount Bank Auto Finance | 1935 | Tel Aviv, Israel |

Recent Competitor Trends and Key Information:

Bank Leumi: As one of the largest and oldest banks in Israel, Bank Leumi reported a 12% increase in auto loan disbursements in 2023, driven by attractive interest rates and flexible repayment options. The bank’s digital loan application platform has improved processing times and customer convenience.

Bank Hapoalim: Known for its strong retail banking presence, Bank Hapoalim experienced a 15% growth in auto finance volumes in 2023. The bank's focus on eco-friendly vehicle financing, offering lower interest rates for electric and hybrid cars, has attracted environmentally conscious consumers.

Direct Finance: Specializing in quick and hassle-free auto financing, Direct Finance saw a 10% increase in loan approvals in urban centers like Tel Aviv and Haifa. The company’s digital-first approach and innovative loan products have resonated well with younger, tech-savvy consumers.

Clal Finance: Clal Finance strengthened its position in the used vehicle financing segment, with a 20% growth in this niche market in 2023. The company’s tailored financing solutions for pre-owned vehicles have made it a preferred choice among budget-conscious buyers.

Union Bank: Focusing on competitive interest rates and customized auto loan packages, Union Bank recorded a 7% increase in market share in 2023. The bank’s strategic partnerships with automotive dealerships have enhanced its reach and accessibility to potential borrowers.

Yallacompare: An emerging digital platform, Yallacompare offers a unique auto loan comparison tool, allowing consumers to compare loan offers from various banks and NBFCs. In 2023, the platform facilitated over ILS 1 billion in auto loan transactions, highlighting the growing demand for digital financial services.

What Lies Ahead for Israel Auto Finance Market?

The Israel auto finance market is expected to witness steady growth by 2029, exhibiting a healthy compound annual growth rate (CAGR) during the forecast period. This growth is anticipated to be driven by favorable economic conditions, increasing vehicle sales, advancements in digital finance solutions, and supportive regulatory frameworks.

Increased Adoption of Electric Vehicle (EV) Financing: As the Israeli government continues to promote green initiatives, there is expected to be a rising demand for electric and hybrid vehicles. Auto finance companies are likely to introduce specialized green loan products with lower interest rates and favorable terms for EV purchases. In 2023, green auto loans accounted for 10% of total auto financing, a figure projected to double by 2029.

Digital Transformation in Auto Finance: The integration of digital technologies such as AI, big data analytics, and automation is expected to streamline loan approval processes, enhance customer experience, and reduce operational costs for financial institutions. Digital lending platforms are likely to capture a larger market share by offering quick and convenient loan services. By 2029, it is estimated that 50% of auto loan applications in Israel will be processed digitally.

Emergence of Subscription-Based Financing Models: The market is witnessing a growing interest in vehicle subscription services as an alternative to traditional loans and leases. These models provide consumers with flexibility, allowing them to switch vehicles or terminate contracts more easily. Financial institutions are expected to develop financing solutions that support these new ownership models, particularly among younger, urban consumers.

Expansion of Used Vehicle Financing: With a growing number of consumers looking for cost-effective vehicle ownership options, used vehicle financing is projected to gain momentum. Financial institutions are expected to offer tailored loan products for pre-owned vehicles, focusing on competitive interest rates and flexible repayment options.

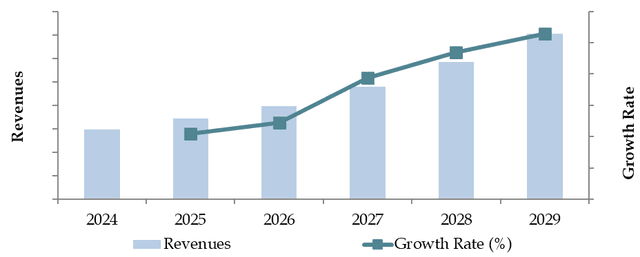

Future Outlook and Projections for Israel Car Finance Market on the Basis of Loan Disbursements in USD Billion, 2024-2029

Israel Auto Finance Market Segmentation

- By Market Structure:

- Banks

- Non-Banking Financial Companies (NBFCs)

- Digital Finance Platforms

- Credit Unions

- Peer-to-Peer (P2P) Lending Platforms

- Captive Finance Companies

- Microfinance Institutions

- By Type of Vehicles Financed:

- Passenger Vehicles

- Commercial Vehicles

- Electric Vehicles (EVs)

- Hybrid Vehicles

- Luxury Vehicles

- Used Vehicles

- By Loan Tenure:

- <3 years

- 3-5 years

- 5-7 years

- 7-9 years

- 9 years

- By Interest Rates:

- Fixed Interest Rate Loans

- Variable Interest Rate Loans

- Zero Interest Loans

- By Region:

- Central Israel (Tel Aviv, Haifa)

- Northern Israel

- Southern Israel

- Jerusalem

- Peripheral Areas

Players Mentioned in the Report (Banks):

- Bank Hapoalim

- Bank Leumi

- Mizrahi-Tefahot Bank

- Israel Discount Bank

- Bank of Jerusalem

- Mercantile Bank

- K.L.S Car Financing Ltd.

- Instaloan

- Lendbuzz

- Toyota Financial Services Israel

- Hyundai Capital Israel

Players Mentioned in the Report (NBFCs):

- K.L.S Car Financing Ltd.

- Instaloan

- Lendbuzz

Players Mentioned in the Report (Captive):

- Toyota Financial Services Israel

- Hyundai Capital Israel

Key Target Audience:

- Auto Finance Providers (Banks, NBFCs, Digital Lenders)

- Automotive Dealerships

- Vehicle Manufacturers (Captive Finance Companies)

- Regulatory Bodies (e.g., Bank of Israel)

- Financial Technology (Fintech) Companies

- Research and Development Institutions

Time Period:

- Historical Period: 2018-2023

- Base Year: 2024

- Forecast Period: 2024-2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-Role of Entities, Stakeholders, and challenges they face.

4.2. Relationship and Engagement Model between Banks-Dealers, NBFCs-Dealers and Captive-Dealers-Commission Sharing Model, Flat Fee Model and Revenue streams

4.3. Supply Decision-Making Process

5.1. New Car and Used Car Sales in Israel by type of vehicle, 2018-2024

8.1. Credit Disbursed, 2018-2024

8.2. Outstanding Loan, 2018-2024

9.1. By Market Structure (Bank-Owned, Multi-Finance, and Captive Companies), 2023-2024P

9.2. By Financing Options (Traditional Loans, Leasing, Multi-Finance Loans), 2023-2024P

9.3. By Cities, 2023-2024P

9.4. By Type of Vehicle (New, Used, Electric), 2023-2024P

9.5. By Average Loan Tenure (0-2 years, 3-5 years, 6-8 years, Above 8 years), 2023-2024P

10.1. Customer Landscape and Cohort Analysis

10.2. Customer Journey and Decision-Making

10.3. Need, Desire, and Pain Point Analysis

10.4. Gap Analysis Framework

11.1. Trends and Developments for Israel Car Finance Market

11.2. Growth Drivers for Israel Car Finance Market

11.3. SWOT Analysis for Israel Car Finance Market

11.4. Issues and Challenges for Israel Car Finance Market

11.5. Government Regulations for Israel Car Finance Market

12.1. Market Size and Future Potential for Online Car Financing Aggregators, 2018-2029

12.2. Business Model and Revenue Streams

12.3. Cross Comparison of Leading Digital Car Finance Companies Based on Company Overview, Revenue Streams, Loan Disbursements/Number of Leads Generated, Operating Cities, Number of Branches, and Other Variables

13.1. Finance Penetration Rate and Average Down Payment for New and Used Cars, 2018-2029

13.2. How Finance Penetration Rates are Changing Over the Years with Reasons

13.3. Type of Car Segment for which Finance Penetration is Higher

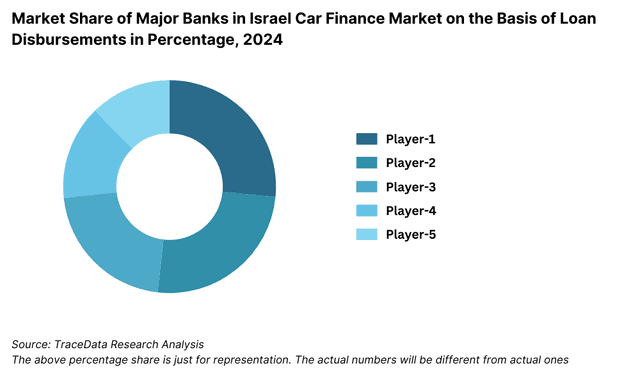

17.1. Market Share of Key Banks in Israel Car Finance Market, 2023

17.2. Market Share of Key NBFCs in Israel Car Finance Market, 2023

17.3. Market Share of Key Captive in Israel Car Finance Market, 2023

17.4. Benchmark of Key Competitors in Israel Car Finance Market, including Variables such as Company Overview, USP, Business Strategies, Strengths, Weaknesses, Business Model, Number of Branches, Product Features, Interest Rate, NPA, Loan Disbursed, Outstanding Loans, Tie-Ups and others

17.5. Strengths and Weaknesses

17.6. Operating Model Analysis Framework

17.7. Gartner Magic Quadrant

17.8. Bowmans Strategic Clock for Competitive Advantage

18.1. Credit Disbursed, 2025-2029

18.2. Outstanding Loan, 2025-2029

19.1. By Market Structure (Bank-Owned, Multi-Finance, and Captive Companies), 2025-2029

19.2. By Financing Options (Traditional Loans, Leasing, Multi-Finance Loans), 2025-2029

19.3. By Region, 2025-2029

19.4. By Type of Vehicle (New, Used, Electric), 2025-2029

19.5. By Average Loan Tenure (0-2 years, 3-5 years, 6-8 years, above 8 years), 2025-2029

19.6. Recommendation

19.7. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities for the Israel Auto Finance Market. Basis this ecosystem, we will shortlist leading 5-6 lenders in the country based on their financial information, loan disbursement volume, and market share.

Sourcing is made through industry reports, multiple secondary sources, and proprietary databases to perform desk research and collate industry-level information.

Step 2: Desk Research

Subsequently, we engage in an exhaustive desk research process by referencing diverse secondary and proprietary databases. This approach enables us to conduct a thorough analysis of the market, aggregating industry-level insights. We delve into aspects like loan disbursement volumes, number of market players, interest rate trends, demand patterns, and other variables.

We supplement this with detailed examinations of company-level data, relying on sources like press releases, annual reports, financial statements, and similar documents. This process aims to construct a foundational understanding of both the market and the entities operating within it.

Step 3: Primary Research

We initiate a series of in-depth interviews with C-level executives and other stakeholders representing various Israel Auto Finance Market companies and end-users. This interview process serves a multi-faceted purpose: to validate market hypotheses, authenticate statistical data, and extract valuable operational and financial insights from these industry representatives. A bottom-to-top approach is undertaken to evaluate loan disbursement volumes for each player, thereby aggregating to the overall market.

As part of our validation strategy, our team executes disguised interviews wherein we approach each company under the guise of potential customers. This approach enables us to validate the operational and financial information shared by company executives, corroborating this data against what is available in secondary databases. These interactions also provide us with a comprehensive understanding of revenue streams, the value chain, processes, pricing, and other factors.

Step 4: Sanity Check

- Bottom-to-top and top-to-bottom analysis, along with market size modeling exercises, is undertaken to assess the sanity check process.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Israel auto finance market is poised for substantial growth, reaching a valuation of ILS 42 Billion by 2029. This growth is driven by factors such as increasing vehicle ownership, rising disposable incomes, and the expansion of digital lending platforms. The market's potential is further bolstered by government incentives for electric vehicle financing and advancements in AI-driven loan processing, making auto financing more accessible and efficient.

The Israel Auto Finance Market features several key players, including Bank Leumi, Bank Hapoalim, Direct Finance, Clal Finance, Union Bank, and Yallacompare. These institutions dominate the market due to their strong financial presence, extensive lending portfolios, and competitive interest rates. Other notable players include emerging fintech firms specializing in digital lending solutions.

The primary growth drivers include economic factors such as increasing demand for vehicle ownership, supportive financing schemes, and evolving consumer preferences. The expanding digital ecosystem in Israel, coupled with the growing trend of electric vehicle adoption, also contributes to the market's growth. Additionally, the rise of digital lending platforms has streamlined the loan application and approval processes, enhancing the overall growth of the Israel Auto Finance Market.

The Israel Auto Finance Market faces several challenges, including rising interest rates, which may impact loan affordability for consumers. Regulatory challenges, such as stringent compliance requirements and consumer protection laws, increase operational costs for lenders. Additionally, competition from alternative financing models, such as vehicle leasing and subscription-based services, poses a significant challenge to traditional auto loans.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0