Japan Car Rental and Leasing Market Outlook to 2035

By Service Type, By Vehicle Category, By Customer Segment, By Contract Model, and By Region

Report Overview

Report Code

TDR0506

Coverage

Asia

Published

January 2026

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Japan Car Rental and Leasing Market Outlook to 2035 – By Service Type, By Vehicle Category, By Customer Segment, By Contract Model, and By Region” provides a comprehensive analysis of the car rental and leasing industry in Japan. The report covers an overview and genesis of the market, overall market size in terms of value, detailed market segmentation; trends and developments, regulatory and tax landscape, customer-level demand profiling, key issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the Japan car rental and leasing market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Japan Car Rental and Leasing Market Outlook to 2035 – By Service Type, By Vehicle Category, By Customer Segment, By Contract Model, and By Region” provides a comprehensive analysis of the car rental and leasing industry in Japan. The report covers an overview and genesis of the market, overall market size in terms of value, detailed market segmentation; trends and developments, regulatory and tax landscape, customer-level demand profiling, key issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the Japan car rental and leasing market. The report concludes with future market projections based on mobility behavior shifts, inbound tourism recovery, corporate fleet optimization trends, electrification policies, urban transport integration, regional demand drivers, cause-and-effect relationships, and case-based illustrations highlighting the major opportunities and cautions shaping the market through 2035.

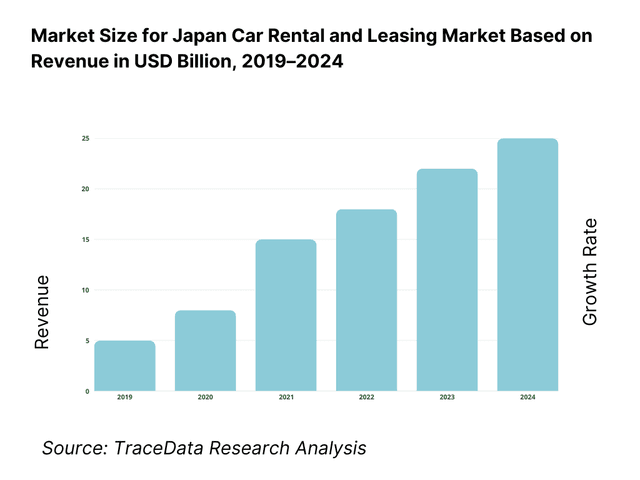

Japan Car Rental and Leasing Market Overview and Size

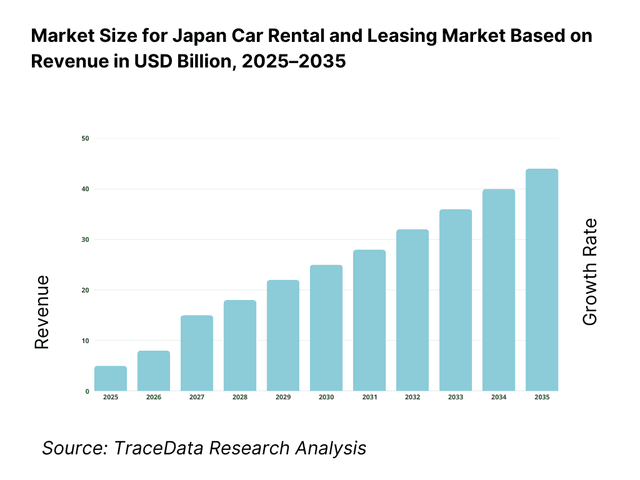

The Japan car rental and leasing market is valued at approximately ~USD ~ billion, representing the demand for short-term rentals, long-term operating leases, and corporate fleet leasing services across passenger cars, vans, and light commercial vehicles. The market supports diverse mobility needs ranging from domestic and inbound tourism, corporate and government fleets, replacement vehicles, and flexible mobility solutions for urban users who prefer access over ownership.

The market is structurally supported by Japan’s mature automotive ecosystem, high urban density, well-developed road infrastructure, and a strong culture of corporate leasing. Long-term leasing is deeply embedded in Japanese corporate procurement practices, particularly among large enterprises and SMEs that prefer off-balance-sheet fleet solutions, bundled maintenance, insurance, and predictable monthly costs. Short-term rentals are closely linked to tourism flows, airport and railway hub traffic, and domestic travel, with strong penetration of compact and kei cars suited to urban driving.

Japan’s car rental and leasing market is also shaped by demographic and behavioral factors, including an aging population, declining private car ownership among younger urban residents, and increasing acceptance of shared and flexible mobility models. Leasing and rental services provide a practical alternative by reducing upfront costs, maintenance responsibility, and resale risk, while aligning with evolving preferences for convenience and flexibility.

From a regional perspective, the Kanto region represents the largest demand center due to the concentration of corporate headquarters, business travel, and international gateways around Tokyo and its surrounding prefectures. Kansai follows, supported by tourism, manufacturing clusters, and strong SME leasing demand. Chubu shows stable demand driven by industrial activity and supplier ecosystems. Hokkaido and Okinawa exhibit disproportionately high short-term rental intensity due to seasonal and leisure tourism, while regional cities see steady leasing demand linked to local enterprises, municipal fleets, and service industries.

What Factors are Leading to the Growth of the Japan Car Rental and Leasing Market:

Recovery and structural growth in inbound and domestic tourism strengthens short-term rental demand: Japan’s tourism recovery and long-term policy focus on inbound travel are reinforcing demand for car rentals, particularly in regions with limited last-mile public transport connectivity. Tourists increasingly prefer rental cars for flexibility in regional travel, rural sightseeing, and multi-stop itineraries. Compact cars, hybrids, and kei vehicles are especially popular due to fuel efficiency and ease of driving. Airports, Shinkansen stations, and regional transport hubs continue to be critical access points for rental demand, supporting fleet expansion and service standardization among operators.

Corporate preference for operating leases and fleet outsourcing drives long-term market stability: Japanese corporations increasingly favor operating leases over vehicle ownership to improve capital efficiency, reduce administrative burden, and ensure predictable fleet costs. Leasing contracts typically bundle vehicle procurement, maintenance, inspections, insurance, and replacement cycles, making them attractive across sectors such as manufacturing, services, pharmaceuticals, utilities, and public administration. This structural reliance on leasing creates stable, recurring demand and long contract tenures, insulating the market from short-term economic volatility.

Urban mobility shifts and declining private ownership support access-based vehicle usage: In major cities, rising parking costs, congestion, and changing lifestyle preferences—especially among younger consumers—are reducing the appeal of private car ownership. Rental and flexible lease models provide access to vehicles when needed without long-term ownership commitments. This trend supports demand for short-term rentals, monthly leases, and subscription-style offerings, particularly for urban households, freelancers, and small businesses seeking mobility without asset ownership.

Which Industry Challenges Have Impacted the Growth of the Japan Car Rental and Leasing Market:

High operating costs and margin pressure due to vehicle depreciation, compliance, and maintenance standards impact profitability: Japan’s car rental and leasing operators face structurally high operating costs driven by strict vehicle inspection regimes (shaken), insurance requirements, parking regulations, and high-quality maintenance expectations. Vehicles must be regularly inspected, maintained, and replaced to comply with safety and environmental standards, leading to relatively short fleet replacement cycles. While these practices support service quality and safety, they increase capital intensity and depreciation pressure, particularly for rental fleets with high utilization. Margin management becomes challenging during periods of demand softness, as operators must continue bearing fixed fleet and compliance costs irrespective of utilization levels.

Seasonality and demand concentration create fleet utilization imbalances across regions: Demand for car rentals in Japan is highly seasonal and region-specific, with sharp peaks during holiday periods, cherry blossom and autumn travel seasons, and summer tourism in destinations such as Hokkaido and Okinawa. Outside peak periods, fleet utilization drops significantly in certain regions, leading to idle assets and lower return on invested capital. Balancing fleet allocation across regions and seasons remains operationally complex, especially given logistical costs, vehicle registration constraints, and the need to maintain service availability at key transport hubs year-round.

Urban constraints, parking limitations, and congestion reduce operational flexibility in major cities: In large metropolitan areas such as Tokyo and Osaka, limited parking availability, high land costs, and congestion increase the complexity and cost of operating rental branches and managing leased fleets. Vehicle storage, customer pick-up and drop-off logistics, and last-mile delivery of replacement vehicles require careful planning and often involve higher real estate and labor expenses. These urban constraints can limit rapid fleet scaling and reduce the attractiveness of expanding physical branch networks, particularly for smaller or newer operators.

What are the Regulations and Initiatives which have Governed the Market:

Vehicle inspection, safety, and environmental regulations governing fleet lifecycle and compliance: Japan’s regulatory framework places strong emphasis on vehicle safety, emissions control, and roadworthiness through mandatory inspection systems and environmental standards. These regulations directly influence fleet age, replacement frequency, and maintenance practices for rental and leasing companies. While compliance ensures high safety and environmental performance, it also increases total cost of ownership and accelerates fleet turnover, shaping pricing strategies and contract structures across both short-term rentals and long-term leases.

Taxation, accounting treatment, and leasing frameworks influencing corporate adoption: Leasing structures in Japan are shaped by tax treatment, accounting rules, and corporate procurement norms that favor operating leases with bundled services. Favorable treatment of lease payments as operating expenses, combined with the ability to outsource fleet management, has historically supported strong corporate leasing demand. Changes in accounting standards or tax interpretations can influence contract structures, lease tenures, and the relative attractiveness of leasing versus ownership, particularly for SMEs and public-sector entities.

Government initiatives promoting low-emission vehicles and fleet electrification: National and local government initiatives aimed at reducing emissions and promoting next-generation vehicles are increasingly relevant to the car rental and leasing market. Incentives for hybrid and electric vehicles, support for charging infrastructure, and emissions targets for fleets encourage operators to introduce cleaner vehicles. While these initiatives create long-term growth opportunities, they also require upfront investment, careful residual value management, and operational adjustments, making leasing companies key intermediaries in Japan’s gradual transition toward lower-emission mobility solutions.

Japan Car Rental and Leasing Market Segmentation

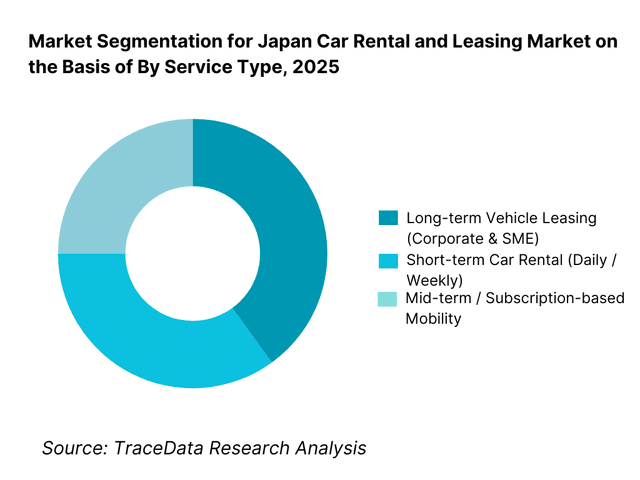

By Service Type: The long-term leasing segment holds dominance in the Japan car rental and leasing market. This is because corporate leasing is deeply embedded in Japanese business practices, where companies prefer operating leases that bundle vehicle procurement, maintenance, insurance, inspections, and replacement cycles into predictable monthly payments. Leasing reduces administrative burden, improves capital efficiency, and supports compliance with strict vehicle inspection and safety norms. While short-term rentals are growing with tourism recovery, leasing continues to account for the majority of market value due to longer contract tenures and stable fleet utilization.

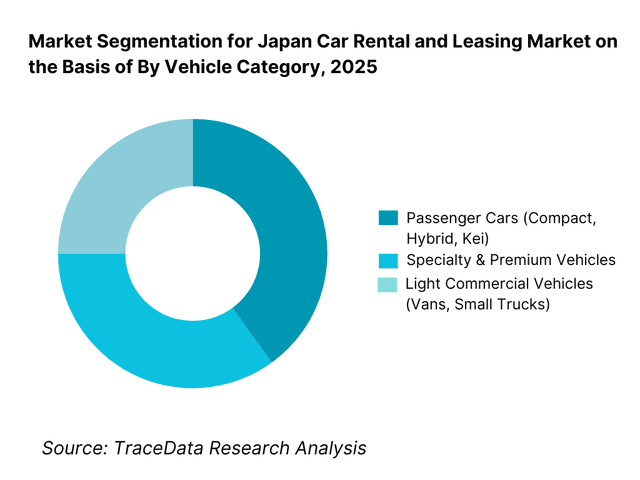

By Vehicle Category: Passenger cars dominate fleet composition due to their suitability for both corporate use and tourism-driven rentals. Compact cars, hybrids, and kei vehicles are particularly favored for urban mobility, fuel efficiency, and ease of driving. Light commercial vehicles play a supporting role, mainly in leasing contracts for service companies, logistics, utilities, and municipal operations.

Competitive Landscape in Japan Car Rental and Leasing Market

The Japan car rental and leasing market exhibits moderate-to-high concentration, led by a few large, well-established players with nationwide branch networks, strong OEM relationships, and deep corporate client penetration. Competitive differentiation is driven by fleet scale, service reliability, geographic coverage, bundled offerings, digital reservation platforms, and the ability to manage compliance-heavy operations efficiently. While national players dominate airports, major cities, and corporate accounts, regional operators remain competitive in local markets by leveraging proximity, customer familiarity, and niche fleet offerings.

Name | Founding Year | Original Headquarters |

Toyota Rent a Car | 1966 | Nagoya, Japan |

Nippon Rent-A-Car | 1969 | Tokyo, Japan |

Times Car Rental | 1965 | Tokyo, Japan |

ORIX Auto | 1973 | Tokyo, Japan |

Mitsubishi Auto Lease | 1972 | Tokyo, Japan |

Sumitomo Mitsui Auto Service | 1981 | Tokyo, Japan |

Nissan Rent a Car | 1966 | Yokohama, Japan |

Budget Rent a Car Japan | 1970s | Tokyo, Japan |

Some of the Recent Competitor Trends and Key Information About Competitors Include:

Toyota Rent a Car: Backed by the Toyota Group ecosystem, the company benefits from strong vehicle sourcing, high fleet quality, and nationwide coverage. Its competitive advantage lies in reliability, dense branch presence near stations and airports, and the ability to rapidly refresh fleets with fuel-efficient and hybrid models.

Nippon Rent-A-Car: Nippon Rent-A-Car maintains a strong position in both business and leisure rentals, with a focus on service consistency and broad regional reach. The company is well positioned in airport and railway hub locations, benefiting from steady domestic and inbound travel demand.

Times Car Rental: Leveraging its broader mobility and parking ecosystem, Times differentiates through integrated urban mobility solutions. Its linkage with parking infrastructure supports convenient pick-up and drop-off models, strengthening competitiveness in dense metropolitan areas.

ORIX Auto: ORIX Auto is a leading force in long-term vehicle leasing, particularly for corporate and SME clients. Its strength lies in comprehensive fleet management services, strong financial backing, and the ability to structure flexible contracts aligned with client operational needs.

Mitsubishi Auto Lease & Sumitomo Mitsui Auto Service: These players are deeply entrenched in corporate and institutional leasing, benefiting from strong banking and financial group affiliations. Their competitive positioning emphasizes long-term contracts, large fleet volumes, and growing involvement in electrification and low-emission fleet transitions.

What Lies Ahead for Japan Car Rental and Leasing Market?

The Japan car rental and leasing market is expected to expand steadily by 2035, supported by sustained corporate leasing penetration, the normalization of inbound tourism, and a broader shift toward flexible, access-based mobility—especially in major urban centers. Growth momentum is further enhanced by fleet renewal cycles driven by safety and inspection requirements, gradual electrification of mobility, and rising demand for outsourced fleet management among SMEs and institutional buyers. As customers increasingly prioritize predictable monthly costs, convenience, and bundled services (maintenance, insurance, roadside support), rental and leasing models will remain a core mobility solution across both business and leisure use cases.

Transition Toward EV/Hybrid-Heavy Fleets and “Low-Carbon Mobility” Positioning: The market’s next phase will see a gradual but persistent move toward higher shares of hybrids and EVs in rental and lease fleets. Leasing companies are expected to play a central role in reducing technology and residual value risk for customers by offering structured replacement cycles and bundled charging/maintenance support. Rental operators will increasingly position “eco fleets” as a differentiator for tourists and corporates, especially in city-heavy travel patterns where fuel efficiency and emissions narratives influence buyer choices and corporate procurement policies.

Rising Preference for Bundled Fleet Management and Outsourced Corporate Mobility Programs: Corporate Japan will continue shifting from self-managed fleets to outsourced fleet programs that combine procurement, servicing, compliance management (inspection scheduling, insurance, documentation), and replacement planning under a single provider. This trend supports long-tenure leasing contracts, predictable revenues for operators, and deeper client stickiness. Through 2035, providers that offer data-enabled fleet optimization (utilization, routing efficiency, cost-per-km) and standardized service SLAs across regions will gain share in large enterprise and multi-branch SME accounts.

Expansion of Subscription and Mid-Term Rental Models for Urban Consumers and Flexible Work Patterns: Monthly subscription-style mobility and mid-term rentals are expected to expand as work patterns evolve and urban users seek flexibility without ownership. These models will be particularly relevant for younger consumers, expatriates, gig workers, and households needing a second car on a temporary basis. Operators that provide app-first onboarding, flexible cancellation, transparent pricing, and doorstep delivery/pickup will be better positioned to capture incremental demand beyond traditional daily rentals and multi-year leases.

Increased Use of Digital Platforms, Dynamic Pricing, and Seamless Reservation-to-Return Journeys: Digitalization will accelerate across the value chain, with stronger reliance on app-based reservations, self-service kiosks, automated identity verification, and smarter fleet allocation systems. Dynamic pricing, demand forecasting, and real-time fleet utilization management will become more important as operators aim to reduce seasonality-driven inefficiencies and improve ROI on vehicles. Companies that integrate digital booking with airport/rail hub partnerships and frictionless return workflows will improve customer satisfaction and operational throughput.

Regional Growth Beyond Megacities Through Tourism Corridors and Rural Mobility Needs:

While Kanto and Kansai will remain the largest demand hubs, incremental growth will increasingly come from tourism corridors and regional destinations where public transport does not fully cover last-mile mobility. Regions such as Hokkaido, Kyushu, Okinawa, and parts of Chubu are expected to see higher rental intensity as inbound tourists diversify itineraries beyond Tokyo-Osaka routes. In parallel, leasing demand in regional cities will remain steady due to SME fleets, municipal usage, and service-industry mobility needs.

Japan Car Rental and Leasing Market Segmentation

By Service Type

- Short-term Car Rental (Daily / Weekly)

- Mid-term Rental (Monthly / Multi-week)

- Long-term Vehicle Leasing (Corporate & SME)

- Subscription-based Mobility Plans

By Vehicle Category

- Kei Cars

- Compact / Sedan Passenger Cars

- SUVs / Minivans

- Light Commercial Vehicles (Vans, Small Trucks)

- Premium / Specialty Vehicles

By Customer Segment

- Corporate / SME Fleets

- Government / Municipal / Institutional

- Individual Consumers (Urban Users)

- Domestic Tourists

- Inbound Tourists

By Contract Model

- Operating Lease (Bundled Services)

- Finance Lease

- Maintenance Lease / Full-Service Lease

- Pay-per-use / Flexible Subscription Contracts

By Region

- Kanto

- Kansai

- Chubu

- Kyushu

- Hokkaido

- Tohoku

- Chugoku

- Shikoku

- Okinawa

Players Mentioned in the Report:

- Toyota Rent a Car

- Nippon Rent-A-Car

- Times Car Rental

- Nissan Rent a Car

- ORIX Auto

- Mitsubishi Auto Lease

- Sumitomo Mitsui Auto Service

- Regional rental operators, franchise networks, corporate fleet management providers, and emerging subscription-mobility platforms

Key Target Audience

- Car rental operators and franchise networks

- Vehicle leasing and fleet management companies

- OEMs and dealer groups supporting fleet sales

- Corporate procurement and fleet administrators (large enterprises and SMEs)

- Airports, railway hub operators, and tourism ecosystem partners

- EV charging infrastructure providers and mobility service integrators

- Travel platforms, OTAs, and digital mobility aggregators

- Private equity and mobility-focused investors

Time Period:

Historical Period: 2019–2024

Base Year: 2025

Forecast Period: 2025–2035

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4. 1 Delivery Model Analysis for Car Rental and Leasing including short-term rentals, mid-term rentals, long-term operating leases, corporate fleet management models, and subscription-based mobility with margins, preferences, strengths, and weaknesses

4. 2 Revenue Streams for Car Rental and Leasing Market including daily and weekly rental revenues, long-term lease rentals, fleet management fees, insurance add-ons, and ancillary service revenues

4. 3 Business Model Canvas for Car Rental and Leasing Market covering vehicle OEMs, leasing companies, rental operators, fleet management providers, insurance partners, financing institutions, and digital booking platforms

5. 1 Global Car Rental and Leasing Companies vs Domestic and Regional Players including Japanese rental brands, global mobility companies, and local fleet operators

5. 2 Investment Model in Car Rental and Leasing Market including fleet ownership models, operating lease investments, subscription fleet investments, and digital platform investments

5. 3 Comparative Analysis of Car Rental and Leasing Distribution by Direct-to-Customer and Corporate or Travel-Channel Partnerships including airport counters, railway hubs, online platforms, and corporate contracts

5. 4 Consumer Mobility Budget Allocation comparing car rental and leasing spend versus private vehicle ownership, public transport, taxis, and ride-hailing with average spend per user per month

8. 1 Revenues from historical to present period

8. 2 Growth Analysis by service type and by vehicle category

8. 3 Key Market Developments and Milestones including tourism recovery, corporate fleet outsourcing trends, regulatory updates, and EV fleet adoption initiatives

9. 1 By Market Structure including global players, domestic national players, and regional operators

9. 2 By Service Type including short-term rentals, mid-term rentals, long-term leasing, and subscription-based mobility

9. 3 By Vehicle Category including kei cars, compact cars, sedans, SUVs, and light commercial vehicles

9. 4 By Customer Segment including corporate fleets, government and institutional users, individual consumers, and tourists

9. 5 By Consumer Demographics including age groups, income levels, and urban versus regional users

9. 6 By Contract Model including operating lease, finance lease, full-service lease, and pay-per-use models

9. 7 By Booking Channel including online platforms, mobile apps, corporate contracts, and walk-in counters

9. 8 By Region including Kanto, Kansai, Chubu, Kyushu, Hokkaido, Tohoku, Chugoku, Shikoku, and Okinawa

10. 1 Consumer and Corporate Landscape and Cohort Analysis highlighting corporate dominance and tourism-driven rental demand

10. 2 Vehicle and Service Selection and Purchase Decision Making influenced by price transparency, convenience, vehicle type, and bundled services

10. 3 Utilization and ROI Analysis measuring fleet utilization rates, contract tenures, and customer lifetime value

10. 4 Gap Analysis Framework addressing fleet availability gaps, seasonality challenges, and service differentiation

11. 1 Trends and Developments including growth of corporate leasing, subscription mobility, digital booking, and EV fleet adoption

11. 2 Growth Drivers including tourism recovery, declining private ownership in urban areas, and corporate fleet outsourcing

11. 3 SWOT Analysis comparing large national operators versus regional and niche mobility providers

11. 4 Issues and Challenges including high operating costs, seasonality, urban parking constraints, and fleet electrification complexity

11. 5 Government Regulations covering vehicle inspection standards, leasing and taxation frameworks, insurance requirements, and environmental policies in Japan

12. 1 Market Size and Future Potential of EV and hybrid fleets in rental and leasing

12. 2 Business Models including EV-focused leasing, mixed-fleet strategies, and subscription-based electric mobility

12. 3 Delivery Models and Type of Solutions including charging partnerships, bundled energy services, and fleet electrification management

15. 1 Market Share of Key Players by revenues and by fleet size

15. 2 Benchmark of 15 Key Competitors including national rental brands, leasing companies, global mobility players, and regional operators

15. 3 Operating Model Analysis Framework comparing rental-led models, leasing-led models, and integrated mobility platforms

15. 4 Gartner Magic Quadrant positioning leading mobility and fleet management players and emerging challengers

15. 5 Bowman’s Strategic Clock analyzing competitive advantage through service differentiation, fleet quality, and price-led strategies

16. 1 Revenues with projections

17. 1 By Market Structure including global, national, and regional players

17. 2 By Service Type including rentals, leasing, and subscriptions

17. 3 By Vehicle Category including passenger cars and light commercial vehicles

17. 4 By Customer Segment including corporate, government, and individual users

17. 5 By Consumer Demographics including age and income groups

17. 6 By Contract Model including operating lease and flexible usage models

17. 7 By Booking Channel including digital platforms and corporate contracts

17. 8 By Region including Kanto, Kansai, Chubu, Kyushu, Hokkaido, Tohoku, Chugoku, Shikoku, and Okinawa

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

We begin by mapping the complete ecosystem of the Japan Car Rental and Leasing Market across demand-side and supply-side entities. On the demand side, entities include corporate fleet users (large enterprises and SMEs), government and municipal fleets, tourism and travel users (domestic and inbound), airport and railway hub mobility demand, insurance replacement demand, and service-sector fleets (utilities, facility management, sales and service teams). Demand is further segmented by usage purpose (business mobility, leisure travel, replacement vehicle, logistics/service fleet), contract tenure (daily/weekly rental vs monthly mid-term vs multi-year lease), and service bundling level (vehicle-only vs full-service with maintenance, insurance, roadside assistance, and compliance handling). On the supply side, the ecosystem includes national rental brands, regional rental operators and franchise networks, large leasing and fleet management firms, OEM and dealer-linked fleet channels, used-vehicle and remarketing partners, insurers and roadside assistance providers, financing institutions, digital booking platforms/OTAs, and supporting infrastructure such as parking operators and EV charging networks. From this mapped ecosystem, we shortlist 6–10 leading rental and leasing players and a representative set of regional operators based on network scale, fleet size, airport/rail presence, corporate account penetration, service bundling capability, and technology enablement. This step establishes how value is created and captured across vehicle sourcing, fleet utilization, maintenance, compliance, customer acquisition, and remarketing.

Step 2: Desk Research

An exhaustive desk research process is undertaken to analyze Japan’s rental and leasing market structure, demand drivers, and segment behavior. This includes reviewing tourism and inbound travel dynamics, domestic travel patterns, corporate fleet outsourcing trends, vehicle ownership and demographic shifts, and urban mobility constraints such as parking availability and congestion. We assess customer preferences around convenience, pricing transparency, vehicle type (kei/compact/hybrid), pickup and return experiences, and bundled service expectations. Company-level analysis includes review of operator branch footprints, fleet composition strategies, digital booking capabilities, corporate leasing packages, and renewal cycles linked to compliance and quality standards. We also examine regulatory and compliance dynamics shaping the market, including inspection requirements, insurance structures, and policy direction toward low-emission fleets. The outcome of this stage is a comprehensive industry foundation that defines the segmentation logic and creates the assumptions needed for market estimation and future outlook modeling through 2035.

Step 3: Primary Research

We conduct structured interviews with car rental operators, leasing and fleet management firms, OEM/dealer fleet sales teams, corporate procurement and fleet administrators, travel ecosystem stakeholders (airport/rail hub partners, OTAs), insurers, and maintenance/remarketing partners. The objectives are threefold: (a) validate assumptions around demand concentration by segment and region, (b) authenticate segment splits by service type, vehicle category, customer segment, and contract model, and (c) gather qualitative insights on pricing behavior, utilization trends, fleet refresh cycles, residual value management, and customer expectations around service reliability and digital convenience. A bottom-to-top approach is applied by estimating active fleet size, utilization rates, average contract value, and transaction volumes across key segments and regions, which are aggregated to develop the overall market view. In selected cases, disguised customer-style interactions are conducted to validate field-level realities such as availability during peak periods, pricing dispersion across hubs, add-on charges (insurance, ETC, winter tires), and operational frictions in pickup/return processes.

Step 4: Sanity Check

The final stage integrates bottom-to-top and top-to-down approaches to cross-validate the market view, segmentation splits, and forecast assumptions. Demand estimates are reconciled with macro indicators such as inbound tourism normalization, corporate fleet penetration trends, vehicle ownership trajectory, and policy direction around electrification. Assumptions around seasonality, utilization, fleet cost inflation, and residual value sensitivity are stress-tested to understand their impact on growth and pricing. Sensitivity analysis is conducted across key variables including tourism growth intensity, corporate leasing adoption rates, EV transition speed, fuel price volatility, and regional travel dispersion beyond megacities. Market models are refined until alignment is achieved between fleet supply capacity, utilization economics, and customer demand patterns, ensuring internal consistency and robust directional forecasting through 2035.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Japan Car Rental and Leasing Market holds strong potential, supported by sustained corporate leasing penetration, normalization of inbound and domestic tourism, and a continuing shift toward access-based mobility—especially in urban centers where ownership costs and parking constraints are high. Leasing remains structurally embedded in corporate fleet procurement due to predictable monthly costs and bundled services. As hybrid/EV fleet transitions and digital-first customer journeys expand, higher-value service models are expected to strengthen market opportunity through 2035.

The market features a combination of large nationwide rental brands with strong airport and city branch networks, and major leasing/fleet management firms backed by financial groups with deep corporate penetration. Competition is shaped by fleet scale, utilization management, service reliability, digital reservation experience, and the ability to offer bundled corporate fleet solutions. Regional operators and franchise networks remain relevant in tourism-heavy destinations and local city demand pockets through proximity and service responsiveness.

Key growth drivers include recovery and expansion of tourism-led rental demand, increasing corporate preference for outsourced fleet management, rising adoption of operating leases with bundled maintenance and compliance handling, and gradual electrification trends that make leasing attractive for managing technology and residual value risk. Additional momentum comes from the rise of subscription and mid-term rental models serving flexible work patterns and urban lifestyles.

Challenges include high fleet operating costs driven by compliance and maintenance standards, utilization volatility due to seasonality and regional demand concentration, and operational constraints in dense urban areas where parking and branch logistics increase cost. The transition to EV fleets also introduces challenges around charging infrastructure availability, fleet planning complexity, and residual value uncertainty, which can impact pricing and replacement strategies across operators.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0