Japan Logistics Market Outlook to 2035

By Service Type, By End-Use Industry, By Transport Mode, By Fulfillment & Distribution Model, and By Region

Report Overview

Report Code

TDR0504

Coverage

Asia

Published

January 2026

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Japan Logistics Market Outlook to 2035 – By Service Type, By End-Use Industry, By Transport Mode, By Fulfillment & Distribution Model, and By Region” provides a comprehensive analysis of the logistics and supply chain industry in Japan. The report covers an overview and evolution of the market, overall market size in terms of value, detailed market segmentation; trends and developments, regulatory and infrastructure landscape, shipper- and buyer-level demand profiling, key issues and challenges, and the competitive landscape including competition dynamics, cross-comparison, opportunities and bottlenecks, and profiling of major logistics service providers operating in Japan.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Japan Logistics Market Outlook to 2035 – By Service Type, By End-Use Industry, By Transport Mode, By Fulfillment & Distribution Model, and By Region” provides a comprehensive analysis of the logistics and supply chain industry in Japan. The report covers an overview and evolution of the market, overall market size in terms of value, detailed market segmentation; trends and developments, regulatory and infrastructure landscape, shipper- and buyer-level demand profiling, key issues and challenges, and the competitive landscape including competition dynamics, cross-comparison, opportunities and bottlenecks, and profiling of major logistics service providers operating in Japan.

The report concludes with future market projections based on domestic consumption patterns, e-commerce penetration, industrial production trends, supply chain restructuring, automation and digital logistics adoption, port and airport modernization, regional demand drivers, cause-and-effect relationships, and case-based illustrations highlighting the major opportunities and risks shaping the Japan logistics market through 2035.

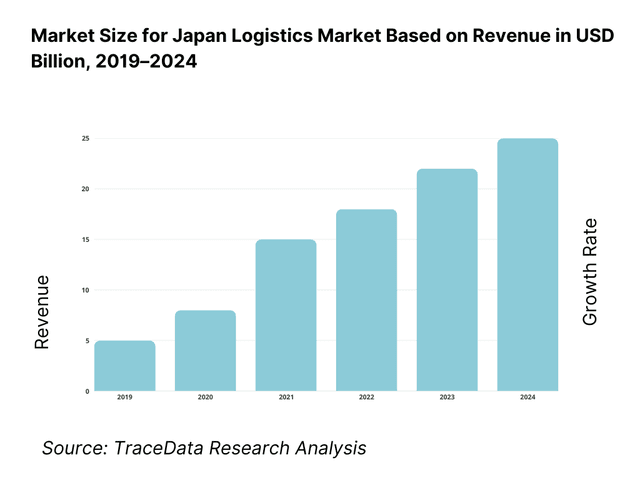

Japan Logistics Market Overview and Size

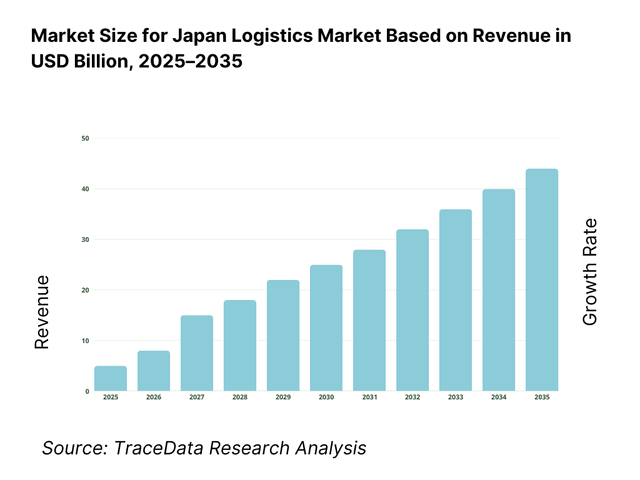

The Japan logistics market is valued at approximately ~USD ~ billion, representing the movement, storage, handling, and value-added management of goods across domestic and international supply chains. The market encompasses freight transportation (road, rail, air, and maritime), warehousing and distribution, contract logistics, cold chain logistics, last-mile delivery, and integrated third-party logistics (3PL) services supporting industrial, commercial, and consumer supply chains.

Japan’s logistics ecosystem is shaped by a highly developed manufacturing base, dense urban consumption centers, advanced port and airport infrastructure, and one of the world’s most demanding service-level environments. Logistics operations in Japan emphasize reliability, precision, time-definite delivery, and damage-free handling, reflecting stringent customer expectations across B2B and B2C segments. The market also operates under structural constraints such as limited land availability, high urban real estate costs, an aging workforce, and strict regulatory and safety standards.

The Greater Tokyo metropolitan region represents the largest logistics demand center in Japan, driven by population density, consumption concentration, e-commerce fulfillment requirements, and proximity to major ports such as Tokyo and Yokohama. The Kansai region, anchored by Osaka, Kobe, and Kyoto, forms the second-largest logistics hub with strong linkages to manufacturing, retail, and international trade. The Chubu region benefits from automotive and industrial manufacturing clusters, while Kyushu and other regional markets are increasingly important for regional distribution, export-oriented manufacturing, and cold chain logistics linked to food and pharmaceuticals.

What Factors are Leading to the Growth of the Japan Logistics Market:

Rising e-commerce penetration and omnichannel retail expansion strengthen logistics demand: Japan’s e-commerce market continues to expand steadily, supported by high internet penetration, aging consumers adopting online shopping, and increasing use of quick-commerce and scheduled home delivery models. This growth directly increases demand for urban fulfillment centers, sortation hubs, last-mile delivery networks, and temperature-controlled logistics. Logistics providers are required to support high-frequency, low-volume deliveries with strict time windows, driving investments in automation, route optimization, and micro-fulfillment infrastructure. The need to balance speed, service quality, and cost efficiency reinforces demand for specialized logistics solutions and integrated 3PL partnerships.

Manufacturing resilience and supply chain restructuring drive contract logistics and regional distribution growth: Japan remains a global hub for automotive, electronics, machinery, chemicals, and precision equipment manufacturing. In response to supply chain disruptions and geopolitical risks, manufacturers are re-evaluating sourcing strategies, inventory buffers, and regional distribution footprints. This has led to greater reliance on professional logistics providers for inbound logistics, plant logistics, warehousing, and outbound distribution. Contract logistics models offering integrated transportation, storage, and value-added services are increasingly preferred as manufacturers seek flexibility, cost transparency, and operational resilience without expanding in-house logistics capabilities.

Labor shortages and cost pressures accelerate automation and logistics modernization: Japan’s aging population and declining workforce have made labor availability one of the most critical constraints in the logistics sector. Driver shortages, warehouse labor constraints, and rising wage costs are pushing logistics operators to invest in automation, robotics, warehouse management systems, and digital platforms. Automated storage and retrieval systems, autonomous material handling, AI-based demand forecasting, and advanced transport management systems are becoming central to maintaining service levels while controlling costs. These structural pressures support long-term growth in high-value logistics services and technology-enabled logistics models rather than purely asset-light transportation offerings.

Which Industry Challenges Have Impacted the Growth of the Japan Logistics Market:

Severe labor shortages across drivers, warehouse staff, and last-mile delivery personnel constrain capacity expansion: Japan’s logistics sector is structurally impacted by an aging population, declining working-age demographics, and limited inflow of logistics labor, particularly in trucking and warehousing. Shortages of long-haul and regional truck drivers have intensified under tighter working-hour regulations and compliance requirements, leading to capacity constraints, higher operating costs, and delivery bottlenecks during peak periods. In urban areas, last-mile delivery faces additional pressure due to rising parcel volumes, narrow delivery windows, and limited drop-off infrastructure. These labor constraints reduce operational flexibility, slow network expansion, and push logistics providers to ration capacity or increase pricing, impacting overall market scalability.

High land costs, space constraints, and urban density limit warehousing expansion and network optimization: Japan’s major consumption centers—particularly the Tokyo metropolitan region—face acute shortages of large, modern logistics facilities due to limited land availability, high real estate prices, and zoning restrictions. Developing large-format distribution centers or multi-story warehouses requires significant capital investment, complex site planning, and long development timelines. Smaller operators struggle to secure strategically located warehousing space, while even large logistics players face challenges balancing proximity to consumers with cost efficiency. These structural constraints increase logistics costs, reduce inventory buffering flexibility, and limit the pace at which fulfillment and distribution networks can be reconfigured to meet evolving demand patterns.

Fragmentation across transport modes and legacy operating models reduces efficiency gains: Despite Japan’s advanced infrastructure, logistics operations remain fragmented across road, rail, coastal shipping, and air freight, with limited interoperability and uneven adoption of integrated planning systems. Many small and mid-sized transport operators continue to rely on legacy dispatching, paper-based documentation, and relationship-driven contracting, which constrains productivity improvements. Coordination challenges between shippers, carriers, and warehouse operators can result in underutilized assets, empty backhauls, and limited visibility across the supply chain. These inefficiencies reduce margin headroom for logistics providers and slow the sector’s transition toward fully integrated, data-driven logistics models.

What are the Regulations and Initiatives which have Governed the Market:

Work-style reform laws and trucking regulations shaping operating models and capacity planning: Japan’s work-style reform policies, including stricter limits on overtime and driving hours for truck drivers, have significantly altered logistics operating economics. These regulations are designed to improve labor conditions and safety but also reduce effective driving capacity and increase the need for additional drivers, relays, or modal shifts. Logistics companies must redesign routes, increase use of intermediate hubs, or shift freight to rail and coastal shipping where feasible. While these initiatives support long-term sustainability, they impose short- to medium-term cost pressures and require structural changes in network design and fleet utilization.

Infrastructure modernization and modal shift initiatives supporting rail and coastal logistics: Government-led initiatives encourage modal shifts away from long-haul trucking toward rail freight and coastal shipping to reduce emissions, ease driver shortages, and improve logistics resilience. Investments in intermodal terminals, port efficiency upgrades, and rail freight capacity aim to make non-road transport more commercially viable for manufacturers and distributors. These policies influence shipper behavior, particularly for bulk, automotive, and industrial cargo, and shape long-term logistics planning by incentivizing multi-modal network designs rather than road-dominated distribution models.

Environmental regulations and decarbonization targets influencing fleet and facility investments: Japan’s carbon reduction commitments and sustainability policies increasingly affect logistics operations, particularly in fleet management, fuel choice, and warehouse energy performance. Logistics providers are under growing pressure from regulators and corporate customers to reduce emissions through fuel-efficient vehicles, electric delivery vans, alternative fuels, and energy-efficient warehouses. Compliance with environmental standards adds to capital expenditure requirements and increases the complexity of fleet and facility planning. However, these regulations also accelerate the shift toward higher-value, technology-enabled logistics services that prioritize efficiency, transparency, and sustainability compliance.

Japan Logistics Market Segmentation

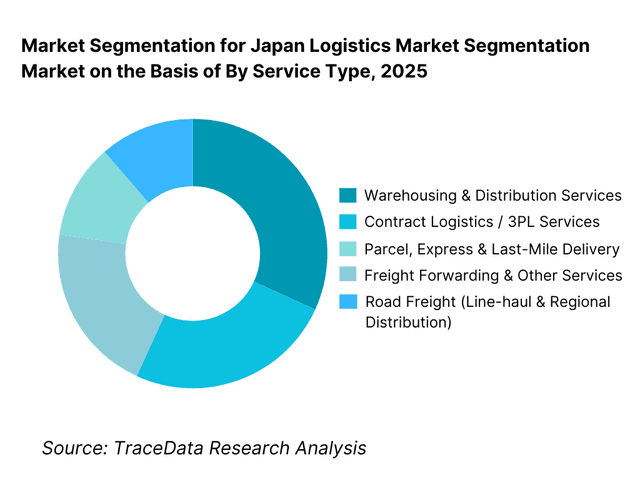

By Service Type: Transportation and freight services hold dominance within the Japan logistics market. This is because Japan’s supply chains are highly time-sensitive, geographically dense, and service-quality driven, with strong reliance on road freight for domestic distribution and maritime/air freight for international trade. Line-haul trucking, regional distribution, and parcel delivery form the backbone of goods movement, supported by Japan’s advanced highway network and high delivery-frequency requirements. While warehousing, contract logistics, and value-added services are expanding—particularly in e-commerce and manufacturing—transportation remains the largest revenue contributor due to volume intensity and operational criticality.

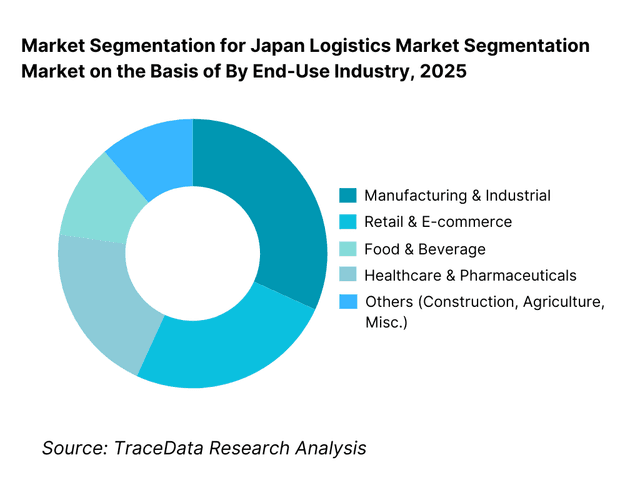

By End-Use Industry: Manufacturing and consumer-linked industries dominate logistics demand in Japan. Automotive, electronics, machinery, food, and chemicals require high-frequency, precision-driven logistics with strict quality, handling, and delivery standards. Retail and e-commerce continue to expand their logistics footprint rapidly, particularly in urban fulfillment, returns management, and temperature-controlled distribution. Healthcare and pharmaceuticals represent a smaller but high-value segment, driven by compliance requirements and cold chain integrity.

Competitive Landscape in Japan Logistics Market

The Japan logistics market exhibits moderate-to-high concentration, characterized by a group of large domestic logistics conglomerates with nationwide networks, diversified service portfolios, and deep integration into manufacturing and retail supply chains. Market leadership is driven by service reliability, nationwide coverage, operational discipline, technology adoption, and long-standing shipper relationships rather than aggressive price competition. Large players dominate complex, high-volume, and contract-based logistics programs, while regional operators and niche specialists remain active in localized transport, SME logistics, and specialized cargo segments.

Name | Founding Year | Original Headquarters |

Nippon Express | 1937 | Tokyo, Japan |

Yamato Holdings | 1919 | Tokyo, Japan |

SG Holdings | 1957 | Kyoto, Japan |

Kintetsu World Express | 1948 | Tokyo, Japan |

Mitsui-Soko Holdings | 1909 | Tokyo, Japan |

Hitachi Transport System | 1950 | Tokyo, Japan |

Sankyu | 1918 | Tokyo, Japan |

Nissin Corporation | 1937 | Yokohama, Japan |

Some of the Recent Competitor Trends and Key Information About Competitors Include:

Nippon Express: As Japan’s largest comprehensive logistics provider, Nippon Express plays a central role in industrial, international freight, and contract logistics. The company’s strength lies in its ability to manage complex, multi-country supply chains while maintaining Japan-grade service precision. Its competitive position is reinforced by strong ties with manufacturers, extensive overseas networks, and growing investments in digital logistics platforms and integrated solutions.

Yamato Holdings: Yamato dominates the domestic parcel and last-mile delivery segment, particularly in B2C and small-parcel logistics. The company is known for its dense delivery network, time-slot delivery innovation, and high service reliability. Rising e-commerce volumes continue to support Yamato’s scale, though labor constraints and delivery cost pressures are pushing operational restructuring and selective pricing adjustments.

SG Holdings (Sagawa Express): SG Holdings remains a major force in domestic transportation and parcel logistics, with a strong presence in B2B distribution and regional freight. Its positioning benefits from strong corporate shipper relationships and efficient trunk-line operations. The company continues to invest in automation and route optimization to address driver shortages and cost efficiency challenges.

Kintetsu World Express: KWE is a key player in international freight forwarding and global supply chain management, particularly for electronics, automotive, and industrial customers. Its competitive advantage lies in air and ocean freight coordination, cross-border logistics expertise, and integration with Japanese multinational supply chains operating across Asia, Europe, and the Americas.

Mitsui-Soko Holdings: Mitsui-Soko has a long-standing presence in warehousing and contract logistics, with strengths in industrial storage, chemical logistics, and value-added services. The company benefits from stable, long-term client relationships and continues to modernize its warehouse portfolio through automation and multi-story urban facilities.

What Lies Ahead for Japan Logistics Market?

The Japan logistics market is expected to expand steadily through 2035, supported by stable domestic consumption, continued growth in e-commerce, manufacturing supply chain restructuring, and rising reliance on professional logistics service providers. While overall growth will remain measured compared to high-growth emerging markets, the Japan logistics sector will increasingly shift toward higher-value, technology-enabled, and service-intensive models. Long-term momentum will be driven by automation, modal diversification, urban fulfillment requirements, and the need to maintain service reliability under labor and cost constraints. Logistics providers that can deliver consistency, transparency, and operational resilience will remain central to Japan’s supply chain ecosystem.

Transition Toward High-Value, Integrated Logistics and Contract-Based Models: The future of the Japan logistics market will see a continued shift away from standalone transportation toward integrated contract logistics and end-to-end supply chain solutions. Manufacturers, retailers, and e-commerce players are increasingly outsourcing warehousing, distribution, inventory management, and value-added services to logistics specialists to improve efficiency and reduce fixed costs. Demand is rising for providers that can combine transportation, storage, packaging, kitting, returns management, and IT-enabled visibility under long-term contracts. This transition favors large, established logistics groups with nationwide networks, compliance capabilities, and sector-specific expertise.

Acceleration of Automation, Robotics, and Digital Logistics Platforms: Labor shortages and rising operating costs will accelerate investments in warehouse automation, robotics, and digital logistics platforms. Automated storage and retrieval systems, picking robots, AI-based demand forecasting, and advanced warehouse and transport management systems will become standard features of modern logistics operations. Digitalization will also improve coordination across shippers, carriers, and warehouses, reducing inefficiencies such as empty runs and underutilized assets. Through 2035, productivity gains from automation will be a critical differentiator for logistics providers seeking to maintain margins while meeting Japan’s high service standards.

Growing Importance of Urban Fulfillment and Multi-Story Logistics Facilities: Urban logistics will play a more prominent role as e-commerce penetration deepens and same-day or next-day delivery expectations become normalized. Limited land availability and high real estate costs in major metropolitan areas will drive the development of multi-story logistics facilities and compact urban distribution hubs. These facilities will require higher capital investment, advanced material handling systems, and precise operational planning. Logistics companies capable of operating efficiently in dense urban environments will gain strategic advantages in serving retail, food delivery, and consumer goods supply chains.

Modal Diversification and Supply Chain Resilience Initiatives: Japan’s logistics market will increasingly adopt multi-modal transport strategies to address driver shortages, cost pressures, and environmental objectives. Greater use of rail freight, coastal shipping, and intermodal solutions will complement road transport, particularly for long-haul and bulk movements. These shifts will reshape network design and require stronger coordination between transport modes, ports, and inland terminals. Supply chain resilience, rather than pure cost minimization, will become a core decision driver for shippers and logistics planners.

Japan Logistics Market Segmentation

By Service Type

- Road Freight (Line-haul & Regional Distribution)

- Warehousing & Distribution Services

- Contract Logistics / 3PL Services

- Parcel, Express & Last-Mile Delivery

- Freight Forwarding & Other Logistics Services

By Transport Mode

- Road

- Rail

- Coastal & Ocean Freight

- Air Freight

- Multi-Modal / Intermodal Logistics

By End-Use Industry

- Manufacturing & Industrial

- Retail & E-commerce

- Food & Beverage

- Healthcare & Pharmaceuticals

- Automotive

- Others (Construction, Chemicals, Consumer Goods)

By Fulfillment & Distribution Model

- In-House Logistics

- Outsourced 3PL / Contract Logistics

- Dedicated Distribution Centers

- Urban Fulfillment & Micro-Hubs

- Cross-Docking & Hub-and-Spoke Models

By Region

- Kanto (Greater Tokyo)

- Kansai

- Chubu

- Kyushu

- Rest of Japan

Players Mentioned in the Report:

- Nippon Express

- Yamato Holdings

- SG Holdings (Sagawa Express)

- Kintetsu World Express

- Mitsui-Soko Holdings

- Hitachi Transport System

- Sankyu

- Nissin Corporation

- Regional logistics operators, specialized transport companies, and niche cold chain providers

Key Target Audience

- Logistics service providers and 3PL companies

- Freight transport operators and fleet owners

- Warehousing developers and logistics real estate investors

- Manufacturing and industrial companies

- Retailers and e-commerce platforms

- Food, pharmaceutical, and cold chain operators

- Government agencies and infrastructure planners

- Private equity and infrastructure-focused investors

Time Period:

Historical Period: 2019–2024

Base Year: 2025

Forecast Period: 2025–2035

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4. 1 Delivery Model Analysis for Logistics including road freight, rail freight, coastal shipping, air cargo, warehousing, contract logistics, and last-mile delivery with margins, preferences, strengths, and weaknesses

4. 2 Revenue Streams for Logistics Market including transportation revenues, warehousing revenues, contract logistics fees, value-added services, and express/parcel delivery revenues

4. 3 Business Model Canvas for Logistics Market covering shippers, logistics service providers, 3PLs, transport operators, warehousing developers, technology providers, and infrastructure operators

5. 1 Global Logistics Providers vs Domestic and Regional Players including integrated logistics conglomerates, parcel delivery companies, freight forwarders, and regional transport operators

5. 2 Investment Model in Logistics Market including fleet investments, warehousing and distribution center development, automation and robotics investments, and digital logistics platforms

5. 3 Comparative Analysis of Logistics Distribution Models by in-house logistics versus outsourced 3PL and contract logistics models including dedicated and shared networks

5. 4 Shipper Logistics Spend Allocation comparing transportation, warehousing, last-mile delivery, and value-added services with average logistics spend as a percentage of revenue

8. 1 Revenues from historical to present period

8. 2 Growth Analysis by service type and by transport mode

8. 3 Key Market Developments and Milestones including logistics policy reforms, infrastructure upgrades, automation adoption, and major contract wins

9. 1 By Market Structure including integrated logistics providers, parcel and express companies, freight forwarders, and regional operators

9. 2 By Service Type including transportation, warehousing, contract logistics, and value-added services

9. 3 By Transport Mode including road, rail, coastal and ocean freight, air freight, and multimodal logistics

9. 4 By End-Use Industry including manufacturing, retail and e-commerce, food and beverage, healthcare and pharmaceuticals, and automotive

9. 5 By Shipper Type including large enterprises, SMEs, and public-sector entities

9. 6 By Fulfillment Model including dedicated distribution centers, hub-and-spoke networks, cross-docking, and urban fulfillment hubs

9. 7 By Contract Type including spot-based services, short-term contracts, and long-term contract logistics

9. 8 By Region including Kanto, Kansai, Chubu, Kyushu, and Rest of Japan

10. 1 Shipper Landscape and Cohort Analysis highlighting manufacturing-led and consumption-driven logistics demand

10. 2 Logistics Provider Selection and Purchase Decision Making influenced by service reliability, coverage, pricing, and technology integration

10. 3 Performance and ROI Analysis measuring delivery lead times, cost efficiency, service quality, and contract stickiness

10. 4 Gap Analysis Framework addressing capacity constraints, service differentiation gaps, and technology adoption

11. 1 Trends and Developments including automation, robotics, digital logistics platforms, and modal diversification

11. 2 Growth Drivers including e-commerce expansion, outsourcing of logistics, supply chain resilience focus, and aging workforce dynamics

11. 3 SWOT Analysis comparing large integrated providers versus regional and niche logistics operators

11. 4 Issues and Challenges including labor shortages, high operating costs, urban space constraints, and regulatory compliance

11. 5 Government Regulations covering transport laws, work-style reforms, safety standards, and decarbonization policies in Japan

12. 1 Market Size and Future Potential of cold chain logistics for food, pharmaceuticals, and healthcare

12. 2 Business Models including dedicated cold chain operators and integrated temperature-controlled logistics services

12. 3 Delivery Models and Type of Solutions including refrigerated transport, temperature-controlled warehousing, and monitoring technologies

15. 1 Market Share of Key Players by revenues and service mix

15. 2 Benchmark of 15 Key Competitors including major domestic logistics groups, parcel delivery leaders, freight forwarders, and regional specialists

15. 3 Operating Model Analysis Framework comparing integrated logistics models, parcel-focused models, and specialized contract logistics providers

15. 4 Gartner Magic Quadrant positioning global and domestic logistics leaders and challengers

15. 5 Bowman’s Strategic Clock analyzing competitive advantage through service differentiation versus cost-led logistics strategies

16. 1 Revenues with projections

17. 1 By Market Structure including integrated providers, parcel companies, and regional operators

17. 2 By Service Type including transportation, warehousing, and contract logistics

17. 3 By Transport Mode including road, rail, coastal, air, and multimodal

17. 4 By End-Use Industry including manufacturing, retail and e-commerce, and healthcare

17. 5 By Shipper Type including large enterprises and SMEs

17. 6 By Fulfillment Model including centralized and urban distribution networks

17. 7 By Contract Type including spot and long-term contracts

17. 8 By Region including Kanto, Kansai, Chubu, Kyushu, and Rest of Japan

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

We begin by mapping the complete ecosystem of the Japan Logistics Market across demand-side and supply-side entities. On the demand side, entities include manufacturing companies (automotive, electronics, machinery, chemicals), retail and e-commerce players, food and beverage companies, pharmaceutical and healthcare firms, importers and exporters, and public-sector agencies involved in infrastructure, defense, and emergency logistics. Demand is further segmented by logistics function (transportation, warehousing, fulfillment, cold chain), shipment profile (bulk vs parcel, ambient vs temperature-controlled), service criticality (time-definite vs cost-optimized), and sourcing model (in-house logistics vs outsourced 3PL/contract logistics).

On the supply side, the ecosystem includes integrated logistics conglomerates, parcel and express companies, trucking operators, warehousing developers and operators, freight forwarders, cold chain specialists, port and terminal operators, rail and coastal shipping providers, technology vendors (WMS/TMS, automation), and regulatory and infrastructure authorities. From this mapped ecosystem, we shortlist 8–12 leading logistics service providers and a representative set of regional and specialized operators based on network scale, service breadth, industry exposure, geographic coverage, and role in industrial, retail, and e-commerce supply chains. This step establishes how value is created and captured across transportation, storage, fulfillment, and value-added logistics services.

Step 2: Desk Research

An exhaustive desk research process is undertaken to analyze the structure, demand drivers, and operational dynamics of the Japan logistics market. This includes review of domestic freight volumes, e-commerce growth trends, manufacturing output patterns, port and airport throughput, warehousing stock evolution, and urban logistics constraints. We assess shipper preferences around service reliability, delivery frequency, lead-time certainty, and outsourcing decisions.

Company-level analysis includes review of logistics players’ service portfolios, network footprints, automation investments, sector focus, and contract logistics capabilities. We also examine regulatory and policy frameworks affecting the sector, including work-style reform laws, trucking regulations, modal shift initiatives, and decarbonization targets. The outcome of this stage is a robust industry foundation that defines segmentation logic and establishes baseline assumptions for market sizing and long-term outlook modeling.

Step 3: Primary Research

We conduct structured interviews with logistics service providers, 3PL operators, trucking companies, warehouse operators, manufacturing supply chain heads, retail and e-commerce logistics managers, and industry experts. The objectives are threefold: (a) validate assumptions around demand concentration, outsourcing penetration, and service mix, (b) authenticate segment splits by service type, transport mode, end-use industry, and region, and (c) gather qualitative insights on pricing behavior, labor availability, capacity constraints, automation adoption, and customer expectations around service quality and reliability.

A bottom-to-top approach is applied by estimating shipment volumes, average logistics spend, and contract penetration across key industries and regions, which are aggregated to form the overall market view. In selected cases, disguised shipper-style interactions are conducted to validate operational realities such as delivery lead times, capacity tightness, pricing sensitivity, and service differentiation between large and mid-sized logistics providers.

Step 4: Sanity Check

The final stage integrates bottom-to-top and top-to-down approaches to cross-validate market size estimates, segmentation splits, and forecast assumptions. Demand estimates are reconciled with macro indicators such as industrial production trends, retail sales growth, trade volumes, and infrastructure investment patterns. Assumptions related to labor shortages, automation penetration, modal shift adoption, and environmental compliance costs are stress-tested to assess their impact on logistics capacity and pricing. Sensitivity analysis is conducted across variables including e-commerce growth intensity, outsourcing penetration, and urban logistics constraints. Market models are refined until alignment is achieved between shipper demand, service provider capacity, and infrastructure realities, ensuring consistency and credible directional forecasting through 2035.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Japan logistics market holds steady long-term potential, supported by stable domestic consumption, continued expansion of e-commerce, and the critical role of logistics in manufacturing-led supply chains. While volume growth is moderate, value growth is driven by higher service intensity, automation, contract logistics expansion, and demand for precision-driven, time-definite delivery. As labor constraints and service expectations intensify, logistics providers offering integrated and technology-enabled solutions are expected to capture increasing value through 2035.

The market is dominated by large domestic logistics conglomerates and parcel delivery leaders with nationwide networks and deep integration into industrial and retail supply chains. These players coexist with regional transport operators, warehousing specialists, and niche providers focused on cold chain, international forwarding, or specific industries. Competition is shaped by service reliability, network density, automation capability, and long-standing shipper relationships rather than aggressive price competition.

Key growth drivers include rising e-commerce penetration, increasing outsourcing of logistics by manufacturers and retailers, expansion of contract logistics models, and growing demand for urban fulfillment and cold chain services. Additional momentum comes from automation, digital logistics platforms, and modal diversification initiatives aimed at improving productivity and resilience amid labor shortages. The emphasis on service quality and reliability continues to reinforce demand for professional logistics services.

Challenges include severe labor shortages, rising operating and real estate costs, limited land availability for warehousing in urban centers, and operational constraints driven by regulatory compliance. Capacity pressures in trucking, particularly for long-haul and regional distribution, can impact service flexibility and pricing. Additionally, the fragmented structure of parts of the transport sector and uneven adoption of digital tools can limit efficiency gains, particularly among small and mid-sized operators.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0