Japan Online Grocery Market Outlook to 2029

By Product Type, By Customer Segments, By Delivery Modes, By Payment Methods, and By Region

Report Overview

Report Code

TDR0106

Coverage

Asia

Published

December 2024

Pages

80-100

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Japan Online Grocery Market Outlook to 2029 – By Product Type, By Customer Segments, By Delivery Modes, By Payment Methods, and By Region” provides a comprehensive analysis of the online grocery market in Japan. The report covers an overview and genesis of the industry, the overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer profiling, challenges and opportunities, and the competitive landscape, including the competition scenario, cross-comparisons, opportunities, bottlenecks, and company profiling of major players in the online grocery market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Japan Online Grocery Market Outlook to 2029 – By Product Type, By Customer Segments, By Delivery Modes, By Payment Methods, and By Region” provides a comprehensive analysis of the online grocery market in Japan. The report covers an overview and genesis of the industry, the overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer profiling, challenges and opportunities, and the competitive landscape, including the competition scenario, cross-comparisons, opportunities, bottlenecks, and company profiling of major players in the online grocery market. The report concludes with future market projections based on revenue by market segment, product type, region, and payment mode, along with case studies highlighting success factors and potential risks.

Japan Online Grocery Market Overview and Size

The Japan online grocery market reached an estimated value of JPY 2.8 trillion in 2023, driven by the growing adoption of e-commerce, increasing urbanization, and changing consumer lifestyles. The market is dominated by key players such as Rakuten Seiyu Netsuper, AEON Digital Grocery, Amazon Japan, Ito-Yokado, and Life Corporation. These companies leverage robust digital platforms, extensive product offerings, and efficient delivery systems to cater to Japan's tech-savvy and time-conscious consumers.

In 2023, Rakuten Seiyu Netsuper launched an enhanced subscription model that offers same-day delivery options and exclusive discounts to loyal customers. This initiative aims to strengthen its position in the highly competitive online grocery market by improving customer retention and satisfaction. Tokyo, Osaka, and Kanagawa are major hubs, accounting for a significant share of the market due to their dense populations and advanced digital infrastructure.

Market Size of Japan Online Grocery Industry on the Basis of GMV in USD Billion, 2018–2024

Key Factors Driving the Growth of the Japan Online Grocery Market

Urbanization and Busy Lifestyles: The rapid urbanization in Japan and the growing trend of dual-income households have significantly increased the demand for online grocery services. In 2023, approximately 70% of Japanese households in metropolitan areas utilized online grocery platforms, reflecting a shift toward convenient shopping solutions.

Technological Advancements: The integration of AI, machine learning, and big data analytics has enabled personalized shopping experiences, improved inventory management, and faster delivery services. For example, Amazon Japan's implementation of AI-driven delivery routes in 2023 reduced delivery times by 25%.

Aging Population: With over 28% of Japan’s population aged 65 and above, online grocery services offer a critical solution for elderly consumers who face mobility challenges. Many companies provide senior-friendly platforms and additional assistance, making online shopping more accessible for this demographic.

Which Industry Challenges Have Impacted the Growth of the Japan Online Grocery Market?

Logistical Complexities: One of the significant challenges faced by the online grocery market in Japan is the complexity of last-mile delivery. With densely populated urban areas and rural regions requiring diverse logistics strategies, companies often struggle to ensure timely and cost-effective deliveries. In 2023, it was reported that nearly 15% of online grocery orders faced delivery delays, impacting customer satisfaction and retention.

High Operational Costs: The high costs of warehouse management, cold chain logistics, and workforce maintenance pose significant barriers to profitability in the online grocery sector. These costs are particularly challenging for smaller players, limiting their ability to scale and compete with established companies.

Consumer Trust and Freshness Concerns: Despite advancements in technology, consumers remain wary about the freshness and quality of perishable items purchased online. According to a survey conducted in 2023, 35% of consumers expressed concerns about the quality of fresh produce, leading to lower adoption rates for specific product categories.

What Are the Regulations and Initiatives Which Have Governed the Market?

Food Safety Standards: The Japanese government enforces stringent regulations to ensure the safety of groceries sold online. These include requirements for proper packaging, temperature-controlled storage, and detailed labeling. In 2023, over 80% of online grocery businesses complied fully with these regulations, reflecting high industry standards but also imposing significant compliance costs on new entrants.

E-commerce and Data Protection Laws: Companies operating in the online grocery space must adhere to Japan’s Act on the Protection of Personal Information (APPI), ensuring consumer data privacy and secure payment gateways. These regulations bolster consumer confidence but require businesses to invest heavily in cybersecurity measures.

Sustainability Policies: To align with Japan’s 2050 Carbon Neutrality Goal, the government has introduced guidelines encouraging the use of eco-friendly packaging and green delivery practices. In 2023, 45% of online grocery orders utilized sustainable packaging solutions, a trend driven by both regulatory pressures and consumer demand.

Japan Online Grocery Market Segmentation

By Product Type: Fresh produce is a major category, driven by Japan's culinary emphasis on quality and seasonal ingredients. In 2023, fresh produce accounted for 35% of total online grocery sales, making it the largest segment. Packaged goods, including snacks, beverages, and ready-to-eat meals, represent a significant portion, appealing to urban consumers seeking convenience. Organic and specialty foods are also gaining traction, constituting 15% of total sales, fueled by rising health and environmental awareness.

%252C%25202023.png&w=640&q=75)

By Delivery Mode: Same-day delivery dominates, particularly in metropolitan areas, due to high consumer expectations for speed and convenience. In 2023, 40% of all orders were completed through same-day delivery. Scheduled deliveries are popular among working professionals who prefer groceries delivered at specific times, while click-and-collect options cater to budget-conscious shoppers who value flexibility and reduced delivery fees.

Competitive Landscape in Japan Online Grocery Market

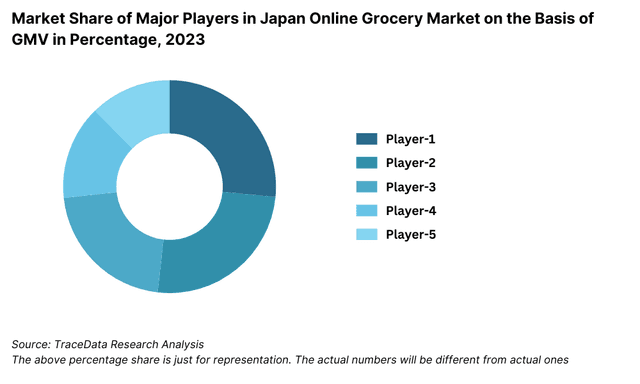

The Japan online grocery market is relatively concentrated, with a few major players dominating the space. However, the emergence of new entrants and the expansion of specialized platforms such as Rakuten Seiyu Netsuper, AEON Digital Grocery, Amazon Japan, Ito-Yokado, and Life Corporation have diversified the market, offering consumers a range of innovative services and product options.

Company Name | Establishment Year | Headquarters |

|---|---|---|

Rakuten SEIYU | 2018 | Tokyo, Japan |

Aeon Supermarket | 1926 | Chiba, Japan |

Amazon Fresh Japan | 2017 | Tokyo, Japan |

Ito-Yokado Net Supermarket | 1920 | Tokyo, Japan |

Maruetsu Net Super | 1945 | Tokyo, Japan |

Life Supermarket Online | 1956 | Osaka, Japan |

Tokyu Store Online | 1956 | Tokyo, Japan |

Daiei Online Supermarket | 1957 | Kobe, Japan |

Okuwa Online Store | 1961 | Wakayama, Japan |

Coop Deli | 1992 | Tokyo, Japan |

Some of the recent competitor trends and key information about competitors include:

Rakuten Seiyu Netsuper: A leading online grocery platform, Rakuten Seiyu Netsuper reported a 25% increase in active users in 2023, attributed to its enhanced subscription services and same-day delivery options. The platform is also leveraging AI technology to improve product recommendations and inventory management.

AEON Digital Grocery: Known for its strong regional presence, AEON Digital Grocery achieved a 20% growth in sales in 2023, driven by its sustainability initiatives and eco-friendly packaging. The company’s focus on fresh produce and traditional Japanese groceries has helped it maintain a loyal customer base.

Amazon Japan: Leveraging its global logistics network, Amazon Japan saw a 30% increase in grocery sales in 2023, particularly in urban areas. The introduction of advanced same-day delivery slots and bulk purchase discounts has positioned Amazon Japan as a preferred choice for tech-savvy customers.

Ito-Yokado: With its focus on fresh and seasonal products, Ito-Yokado recorded a 15% increase in online grocery sales in 2023. Its hybrid model, integrating in-store pickup and delivery options, has been particularly successful in suburban regions.

Life Corporation: Specializing in subscription-based grocery services, Life Corporation experienced a 10% rise in sales in 2023, mainly from repeat customers. Its emphasis on affordability and value-added services, such as meal kits and cooking tutorials, has attracted a broad customer demographic.

What Lies Ahead for Japan Online Grocery Market?

The Japan online grocery market is projected to grow steadily by 2029, exhibiting a strong CAGR during the forecast period. This growth will be driven by increasing consumer reliance on e-commerce platforms, urbanization, and technological advancements in the grocery delivery ecosystem.

Shift Towards Sustainable Practices: With Japan’s commitment to achieving carbon neutrality by 2050, the online grocery market is expected to see a surge in environmentally friendly practices. This includes the adoption of sustainable packaging, electric delivery vehicles, and green supply chain management. Consumers are increasingly favoring platforms that prioritize environmental sustainability, making this a key growth driver.

Expansion of Same-Day Delivery Services: To meet the growing demand for convenience, major players are expected to enhance their same-day delivery capabilities, particularly in urban and suburban areas. Investments in logistics infrastructure and AI-powered route optimization are anticipated to reduce delivery times and enhance customer satisfaction.

Integration of Advanced Technologies: The use of AI and big data analytics will play a significant role in personalizing the shopping experience, optimizing inventory management, and streamlining delivery processes. These technologies will provide consumers with tailored recommendations, ensure product availability, and improve overall operational efficiency.

Rising Popularity of Subscription Models: Subscription-based grocery services, offering benefits such as exclusive discounts and flexible delivery options, are expected to grow in popularity. These models cater to busy households and repeat customers, providing a reliable revenue stream for online grocery platforms.

Future Outlook and Projections for Japan Online Grocery Market on the Basis of GMV in USD Billion, 2024-2029

Japan Online Grocery Market Segmentation

- By Market Structure:

- Omni-Channel Retailers

- Online-Only Retailers

- By Product Type:

- Fresh Produce (Fruits, Vegetables, Meat, Seafood)

- Packaged Foods (Snacks, Beverages, Canned Goods)

- Health and Organic Products

- Frozen Foods

- Household Essentials

- By Delivery Mode:

- Same-Day Delivery

- Next-Day Delivery

- Scheduled Delivery

- Click-and-Collect

- By Customer Segments:

- Urban Professionals

- Young Families

- Elderly Consumers

- Health-Conscious Consumers

- By Region:

- Tokyo

- Osaka

- Kanagawa

- Kyushu

- Hokkaido

Players Mentioned in the Report:

- Rakuten SEIYU

- Aeon Supermarket

- Amazon Fresh Japan

- Ito-Yokado Net Supermarket

- Maruetsu Net Super

- Life Supermarket Online

- Tokyu Store Online

- Daiei Online Supermarket

- Okuwa Online Store

- Coop Deli

Key Target Audience:

- Online Grocery Retailers

- E-commerce Platforms

- Logistics and Delivery Service Providers

- Payment Gateway Providers

- Regulatory Bodies (e.g., Ministry of Agriculture, Forestry and Fisheries)

- Research and Development Institutions

Time Period:

- Historical Period: 2018–2023

- Base Year: 2024

- Forecast Period: 2024–2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process: Role of Entities, Stakeholders, and Challenges They Face

4.2. Sourcing Model and Supply Chain Process for Online Grocery Market in Japan

4.3. Brick and Mortar v/s Online Grocery Shopping

4.4. Revenue Streams for Japan Online Grocery Market

4.5. Business Model Canvas for Japan Online Grocery Market

5.1. Growth of Online Retail in Japan, 2018-“2024

5.2. Online vs. Offline Grocery Sales in Japan, 2018-“2024

5.3. Spending on Grocery Delivery Services in Japan, 2024

5.4. Regional Penetration of Online Grocery Platforms by Ci

6.1. Operating Model: Marketplace and Inventory Model

6.2. Process of On Boarding a Grocery Store

6.3. Role & Responsibilities of Company and Partner Grocery Store

6.4. Operating Model: Omnichannel Model

6.5. Cross Comparison of Operating Models (Marketplace and Omnichannel) based on Delivery Time, Inventory, Gross Margin, Product Assortment, Players, Revenue Streams, Advantages & Disadvantages

6.6. How Companies Manage Logistics?

6.7. Gaps & Possible Solutions of Managing Logistics

9.1. GMV, 2018-“2024

9.2. Number of Orders, 2018-“2024

10.1. By Delivery Time (Same-Day, Next-Day, Scheduled Delivery, Click-and-Collect), 2023-“2024P

10.2. By Average Order Value, 2023-“2024P

10.3. By Region, 2023-“2024P

10.4. By Product Type (Fresh Produce, Packaged Goods, Health and Organic Products, Frozen Foods, Household Essentials), 2023-“2024P

10.5. By Mode of Payment, 2023-2024P

11.1. Customer Landscape and Cohort Analysis

11.2. Customer Journey and Decision-Making

11.3. Need, Desire, and Pain Point Analysis

11.4. Gap Analysis Framework

12.1. Trends and Developments for Japan Online Grocery Market

12.2. Growth Drivers for Japan Online Grocery Market

12.3. SWOT Analysis for Japan Online Grocery Market

12.4. Issues and Challenges for Japan Online Grocery Market

12.5. Government Regulations for Japan Online Grocery Market

13.1. Market Share of Logistics Providers in Grocery Delivery, 2018-“2029

13.2. Innovations in Grocery Logistics: AI-Driven Delivery, Electric Vehicles, and Sustainable Practices

13.3. Cost Structures and Efficiency Improvements in Last-Mile Delivery

16.1. Market Share of Key Players in Japan Online Grocery Market Basis GMV/Number of Orders, 2023

16.2. Benchmark of Key Competitors in Japan Online Grocery Market, Including Variables Such as Year of Establishment, Business Model, Number of Partner Grocery Stores/Supermarkets & Hypermarkets, Delivery Fleet, Delivery Charges, Delivery Time, Cancellation Rate, Product Listings, & Employees, Approximate Annual Orders, Market Share on the basis of Number of Orders, Market Share on the basis of GMV and others

16.3. Strength and Weakness Analysis

16.4. Operating Model Analysis Framework

16.5. Gartner Magic Quadrant

16.6. Bowmans Strategic Clock for Competitive Advantage

17.1. GMV, 2025-“2029

17.2. Number of Orders, 2025-“2029

18.1. By Delivery Time (Same-Day, Next-Day, Scheduled Delivery, Click-and-Collect), 2025-“2029

18.2. By Average Order Value, 2025-“2029

18.3. By Region, 2025-“2029

18.4. By Product Type (Fresh Produce, Packaged Goods, Health and Organic Products, Frozen Foods, Household Essentials), 2025-“2029

18.5. By Mode of Payment, 2025-“2029

18.10. Recommendations

18.11. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities for the Japan Online Grocery Market. Based on this ecosystem, we will shortlist leading 5-6 companies in the market based on their financial information, market share, and digital presence.

Sourcing is made through industry reports, government publications, multiple secondary, and proprietary databases to conduct desk research around the market, enabling the collection of industry-level data.

Step 2: Desk Research

Engage in comprehensive desk research using a variety of secondary and proprietary databases. This process involves analyzing market-level data, including revenue streams, number of players, product categories, consumer preferences, and pricing trends.

Conduct an in-depth review of company-level data from press releases, annual reports, financial statements, and market research publications to understand the strategies of key players. This step establishes a solid foundation for understanding the market dynamics and competitive landscape.

Step 3: Primary Research

Initiate a series of structured interviews with C-level executives, product managers, and other stakeholders from key companies operating in the Japan Online Grocery Market. This process aims to validate market assumptions, refine statistical insights, and extract detailed operational data.

Conduct bottom-to-top and top-to-bottom evaluations to assess individual company contributions to the market size. Disguised interviews are undertaken to cross-verify operational and financial data shared during primary interviews with secondary sources, ensuring accuracy and reliability.

Step 4: Sanity Check

- Perform bottom-to-top and top-to-bottom market analysis along with market size modeling to conduct a final sanity check. This step ensures that all estimates and projections align with industry standards and are consistent across various sources.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Japan Online Grocery Market is expected to experience significant growth, reaching a projected valuation of JPY 5.2 trillion by 2029. This growth is driven by increasing digital adoption, urbanization, and the integration of advanced technologies in the grocery retail ecosystem.

Key players include Rakuten Seiyu Netsuper, AEON Digital Grocery, Amazon Japan, Ito-Yokado, and Life Corporation. These companies dominate the market due to their strong digital presence, extensive product offerings, and efficient logistics networks.

Major growth drivers include the rise of same-day delivery services, consumer demand for convenience, and increased adoption of cashless payment systems. The popularity of subscription-based models and the growing emphasis on sustainable practices also contribute to market expansion.

Key challenges include logistical complexities, high operational costs, and consumer concerns regarding the freshness of perishable items. Additionally, reaching rural areas with limited infrastructure and addressing the technological adoption gap among elderly consumers remain critical barriers.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0