Japan Warehousing Market Outlook to 2035

By Warehouse Type, By Temperature Control, By End-Use Industry, By Ownership & Operating Model, and By Region

Report Overview

Report Code

TDR0505

Coverage

Asia

Published

January 2026

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Japan Warehousing Market Outlook to 2035 – By Warehouse Type, By Temperature Control, By End-Use Industry, By Ownership & Operating Model, and By Region” provides a comprehensive analysis of the warehousing and storage industry in Japan. The report covers an overview and genesis of the market, overall market size in terms of value, detailed market segmentation; trends and developments, regulatory and compliance landscape, buyer-level demand profiling, key issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the Japan warehousing market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Japan Warehousing Market Outlook to 2035 – By Warehouse Type, By Temperature Control, By End-Use Industry, By Ownership & Operating Model, and By Region” provides a comprehensive analysis of the warehousing and storage industry in Japan. The report covers an overview and genesis of the market, overall market size in terms of value, detailed market segmentation; trends and developments, regulatory and compliance landscape, buyer-level demand profiling, key issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the Japan warehousing market. The report concludes with future market projections based on domestic consumption patterns, manufacturing and export logistics requirements, e-commerce penetration, cold chain expansion, automation adoption, regional demand drivers, cause-and-effect relationships, and case-based illustrations highlighting the major opportunities and cautions shaping the market through 2035.

Japan Warehousing Market Overview and Size

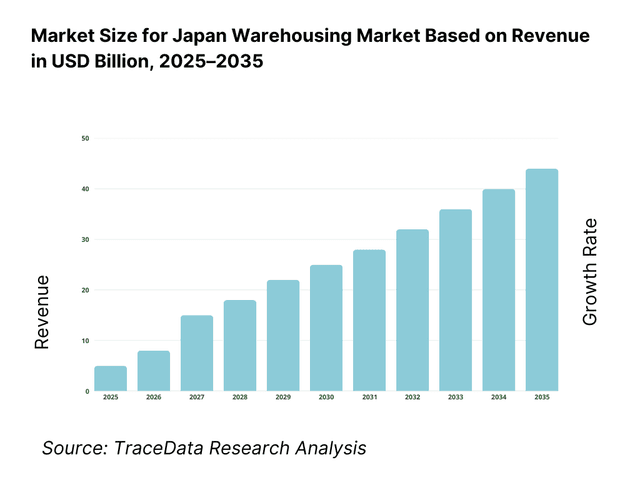

The Japan warehousing market is valued at approximately ~USD ~ billion, representing the provision of storage, handling, and value-added logistics services across ambient, temperature-controlled, and specialized warehouse facilities. Warehousing infrastructure in Japan supports a highly sophisticated supply chain ecosystem catering to manufacturing, retail, e-commerce, food and beverages, pharmaceuticals, chemicals, and international trade flows. Facilities range from traditional multi-tenant warehouses to advanced automated distribution centers and high-spec cold storage units designed to meet strict quality, safety, and compliance standards.

The market is underpinned by Japan’s dense urban consumption centers, export-oriented manufacturing base, and high expectations for delivery reliability, inventory accuracy, and product integrity. Unlike land-abundant markets, Japan’s warehousing sector operates under space constraints, driving vertical warehouse development, multi-story logistics facilities, and intensive use of automation and material handling systems. High land prices and limited availability near major metros further reinforce the focus on operational efficiency, throughput optimization, and technology-led upgrades rather than greenfield sprawl.

The Kanto region, led by Greater Tokyo, represents the largest warehousing demand center in Japan due to its concentration of population, consumption, corporate headquarters, ports, and air cargo gateways. Kansai, anchored by Osaka and Kobe, remains a critical logistics hub supporting manufacturing, retail distribution, and international trade. Chubu, centered around Nagoya, plays a strategic role in automotive and industrial supply chains, while Kyushu and other regional clusters support agri-food logistics, port-based trade, and regional distribution. Across regions, demand is increasingly shifting toward modern, compliant, and automated facilities as older warehouses face functional obsolescence.

What Factors are Leading to the Growth of the Japan Warehousing Market:

Growth of e-commerce and omni-channel distribution reshapes warehouse requirements: Japan’s e-commerce market continues to expand, driven by changing consumer behavior, aging demographics favoring home delivery, and the proliferation of omni-channel retail models. This trend is increasing demand for fulfillment centers, urban distribution hubs, and last-mile logistics facilities capable of handling high order volumes, smaller shipment sizes, and faster delivery windows. Warehouses are being designed with higher throughput, advanced sorting systems, and flexible layouts to support same-day or next-day delivery expectations, particularly in major metropolitan areas.

Cold chain expansion driven by food quality standards and pharmaceutical logistics: Japan maintains some of the world’s most stringent standards for food safety, freshness, and pharmaceutical integrity. Rising demand for frozen and chilled foods, growth in convenience and ready-to-eat meals and expanding pharmaceutical and biotech supply chains are driving sustained investment in temperature-controlled warehousing. Cold storage facilities increasingly require precise temperature zoning, redundancy systems, and compliance with regulatory and customer audit requirements, positioning cold chain warehousing as one of the fastest-growing segments of the market.

Automation, labor constraints, and productivity optimization drive facility upgrades: Japan’s structural labor shortages and aging workforce are accelerating the adoption of warehouse automation, robotics, and advanced warehouse management systems. Automated storage and retrieval systems (AS/RS), autonomous guided vehicles, and high-density racking solutions are being deployed to improve productivity, reduce manual handling, and maximize space utilization. These investments not only address labor availability challenges but also enhance accuracy, safety, and operating cost efficiency, making modern automated warehouses increasingly attractive to both operators and occupiers.

Which Industry Challenges Have Impacted the Growth of the Japan Warehousing Market:

Land scarcity, high real estate costs, and zoning constraints limit scalable warehouse development: Japan’s warehousing market operates under severe land availability constraints, particularly in major consumption and logistics hubs such as Greater Tokyo and Osaka. High land acquisition costs, competition from residential and commercial real estate, and restrictive zoning norms make large-format, low-density warehouses economically unviable in many locations. As a result, developers are compelled to invest in multi-story and high-spec facilities, which involve higher construction complexity, longer development timelines, and elevated capital expenditure. These structural constraints restrict rapid capacity addition and raise entry barriers, especially for smaller operators and first-time investors.

Aging warehouse stock and functional obsolescence increase replacement and upgrade pressures: A significant portion of Japan’s existing warehouse infrastructure was developed decades ago and is not aligned with modern logistics requirements such as high floor loading, ceiling heights suitable for automation, temperature zoning, or compliance-ready layouts. Retrofitting older facilities to meet current safety, seismic, fire, and operational standards is often costly and technically challenging. In many cases, operators face a trade-off between continuing to operate sub-scale assets with efficiency limitations or committing to high capital investment in redevelopment, slowing overall modernization momentum across the sector.

Labor shortages and rising operating costs impact warehouse economics: Japan’s structural labor shortages, driven by demographic aging and a shrinking working-age population, continue to affect warehouse operations. While automation mitigates some challenges, many facilities still require manpower for picking, packing, quality checks, and value-added services. Rising wages, reliance on temporary or contract labor, and competition with other service sectors increase operating costs and compress margins, particularly for labor-intensive warehouses serving e-commerce and retail distribution. Smaller operators with limited automation capability are disproportionately impacted by these pressures.

What are the Regulations and Initiatives which have Governed the Market:

Building safety, seismic resilience, and fire protection regulations shaping warehouse design: Japan enforces stringent building regulations to address seismic risk, fire safety, and structural integrity. Warehousing facilities must comply with detailed requirements related to earthquake resistance, structural redundancy, fire compartmentalization, sprinkler systems, smoke exhaust, and evacuation routes. These regulations significantly influence warehouse layout, building height, material selection, and construction methods. While they enhance long-term asset safety and resilience, they also increase upfront development costs and extend approval and construction timelines, particularly for large or multi-story logistics facilities.

Food safety, pharmaceutical, and cold chain compliance standards driving specialized warehousing: Warehouses handling food, beverages, pharmaceuticals, and medical products are subject to strict hygiene, temperature control, traceability, and audit requirements under Japan’s regulatory framework. Compliance with HACCP-based food safety systems, pharmaceutical good distribution practices, and customer-driven quality audits necessitates investment in monitoring systems, backup power, and controlled environments. These standards elevate the operational and capital intensity of compliant warehouses, favoring larger, professionally managed operators and limiting participation by informal or low-spec facilities.

Energy efficiency, sustainability initiatives, and disaster preparedness influencing investment decisions: Government-led initiatives promoting energy efficiency, carbon reduction, and disaster resilience increasingly shape warehouse development and upgrade strategies. Requirements and incentives related to energy-efficient equipment, LED lighting, solar integration, insulation performance, and emergency preparedness systems influence design and operating models. Additionally, expectations for business continuity planning—particularly for logistics nodes supporting essential goods—encourage investments in backup power, redundant systems, and resilient site selection. While these initiatives support long-term sustainability and reliability, they add complexity and cost to warehouse development and operations, affecting investment feasibility in marginal locations.

Japan Warehousing Market Segmentation

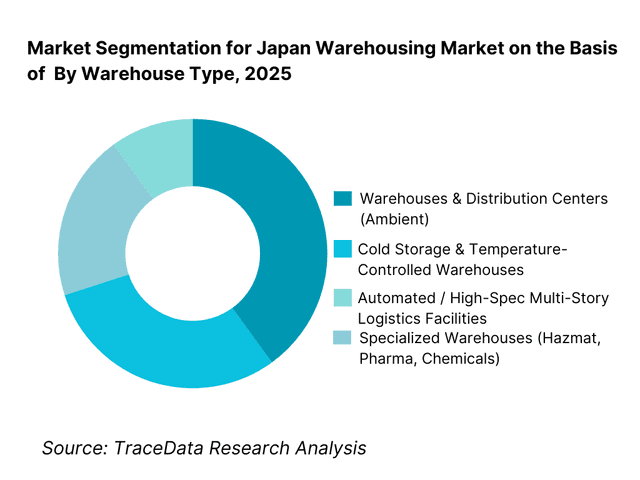

By Warehouse Type: The general warehousing and distribution center segment holds dominance in Japan’s warehousing market. This is because ambient warehouses form the backbone of domestic distribution for retail, consumer goods, manufacturing components, and e-commerce fulfillment. These facilities prioritize high throughput, inventory accuracy, proximity to consumption clusters, and integration with transport networks rather than sheer land footprint. While cold storage and specialized warehouses are expanding faster in percentage terms, general-purpose warehouses continue to account for the largest share due to their role in supporting Japan’s broad-based manufacturing and consumption economy.

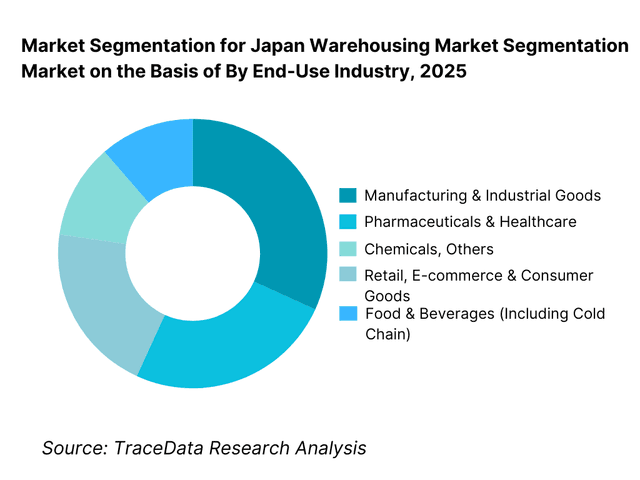

By End-Use Industry: Retail, e-commerce, and consumer goods dominate warehousing demand in Japan due to dense urban consumption, frequent replenishment cycles, and high service-level expectations. Food & beverage and pharmaceuticals represent structurally strong segments due to stringent quality and temperature requirements. Manufacturing-related warehousing remains steady, supporting automotive, electronics, and precision equipment supply chains with buffer storage, sequencing, and value-added services.

Competitive Landscape in Japan Warehousing Market

The Japan warehousing market exhibits moderate-to-high fragmentation, characterized by a mix of large integrated logistics groups, long-established warehouse specialists, and regional operators with strong local customer relationships. Market leadership is driven by network scale, service reliability, compliance capability, automation readiness, and long-term relationships with manufacturers and large corporate shippers. Large players dominate national contracts and complex cold chain or value-added logistics, while regional firms remain competitive in localized distribution, port-centric storage, and SME-focused services.

Name | Founding Year | Original Headquarters |

Nippon Express | 1937 | Tokyo, Japan |

Mitsui-Soko Holdings | 1909 | Tokyo, Japan |

Sagawa Express | 1957 | Kyoto, Japan |

Yamato Holdings | 1919 | Tokyo, Japan |

Kintetsu World Express | 1948 | Tokyo, Japan |

Marubeni Logistics | 2004 | Tokyo, Japan |

Sumitomo Warehouse | 1899 | Osaka, Japan |

Japan Logistics Systems | 1960 | Tokyo, Japan |

Some of the Recent Competitor Trends and Key Information About Competitors Include:

Nippon Express: As Japan’s largest integrated logistics provider, Nippon Express continues to strengthen its warehousing footprint through automation, cold chain expansion, and integration with international freight and contract logistics. Its competitive advantage lies in nationwide coverage, compliance depth, and the ability to support complex, multi-industry supply chains including pharmaceuticals, electronics, and automotive.

Mitsui-Soko Holdings: Mitsui-Soko remains a leading specialist in warehousing and contract logistics, with a strong focus on high-quality facilities, value-added services, and long-term client relationships. The company’s positioning is reinforced by investments in modern logistics parks, cold storage, and IT-enabled inventory management, particularly for food, chemicals, and consumer goods clients.

Yamato Holdings: Traditionally known for parcel delivery, Yamato is increasingly expanding its warehousing and fulfillment capabilities to support e-commerce and omni-channel distribution. Its strength lies in last-mile integration, urban logistics expertise, and the ability to link warehousing directly with fast, reliable delivery networks.

Sagawa Express: Sagawa continues to build warehouse-linked distribution solutions focused on speed, accuracy, and service consistency. The company benefits from strong relationships with retail and B2B shippers, leveraging its transport backbone to offer integrated storage and distribution services, particularly in high-volume domestic logistics.

Sumitomo Warehouse: With a long operating history, Sumitomo Warehouse competes through stability, asset quality, and strong presence in port-adjacent and industrial warehousing. Its focus on compliance, safety, and long-term contracts supports steady demand from manufacturing, trading houses, and international logistics customers.

What Lies Ahead for Japan Warehousing Market?

The Japan warehousing market is expected to expand steadily by 2035, supported by continued growth in e-commerce fulfillment, modernization of aging warehouse stock, and rising demand for high-spec, compliant, and technology-enabled logistics facilities. Growth momentum is further strengthened by cold chain investments, increasing outsourcing of logistics functions, and the continued shift toward multi-story and space-efficient warehouses in land-constrained metro regions. As occupiers and 3PLs prioritize service reliability, inventory visibility, and faster cycle times, Japan’s warehousing market will increasingly tilt toward automation-ready assets, resilient operations, and purpose-built facilities that can support next-generation distribution models.

Acceleration of High-Spec, Multi-Story Logistics Facilities in Metro Catchments: Japan’s structural land scarcity near Tokyo, Osaka, and Nagoya will continue to push development toward multi-story, ramp-access logistics facilities and vertical warehousing formats. These assets enable higher throughput per square meter, improved proximity to consumption nodes, and better integration with last-mile delivery networks. By 2035, developers and institutional investors are expected to prioritize Grade-A logistics parks with higher floor loading, greater ceiling heights, modern docking configurations, and stronger business continuity provisions, driving an ongoing quality upgrade cycle in the asset base.

Cold Chain Capacity Expansion Driven by Food Modernization and Pharma Integrity Requirements: Cold storage will remain one of the fastest-growing warehouse segments through 2035, supported by growing frozen and chilled food consumption, expansion of ready-to-eat categories, and higher standards for temperature traceability. Pharmaceutical and healthcare supply chains will further reinforce demand for compliant cold warehousing with monitoring systems, backup power, and audit-ready SOPs. Operators that can deliver multi-temperature zoning, reliable uptime, and strong compliance capabilities will capture premium contracts and long-duration demand from food and healthcare customers.

Automation-Led Productivity Gains Becomes Central to Warehouse Competitiveness: Japan’s labor shortages will sustain strong adoption of automation and robotics across warehousing operations. Increased deployment of AS/RS, automated sortation, AMRs/AGVs, and WMS/WES integration will reduce labor dependency and improve picking accuracy and throughput. By 2035, warehouses that are automation-ready—through layout design, power and network provisioning, standardized racking, and safety systems—will be preferred by large shippers and 3PLs, increasing the competitive gap versus older, labor-intensive facilities.

Stronger Focus on Resilience, Disaster Preparedness, and Business Continuity Planning: Japan’s exposure to earthquakes, typhoons, and supply disruptions will continue to shape warehouse site selection, construction standards, and operating models. Demand will rise for resilient facilities with seismic-ready designs, redundant power systems, emergency inventory buffering, and robust safety and monitoring protocols. Warehouses supporting essential goods, cold chain, and high-value manufacturing inputs will increasingly be evaluated on business continuity readiness, influencing how occupiers select sites and how developers prioritize asset specifications.

Japan Warehousing Market Segmentation

By Warehouse Type

• Warehouses & Distribution Centers (Ambient)

• Cold Storage & Temperature-Controlled Warehouses

• Automated / High-Spec Multi-Story Logistics Facilities

• Specialized Warehouses (Hazmat, Pharma, Chemicals)

By Temperature Control

• Ambient Warehousing

• Chilled Warehousing

• Frozen Warehousing

• Multi-Temperature / Zoned Cold Warehousing

By Ownership & Operating Model

• Self-Owned / Captive Warehousing (Manufacturers & Retailers)

• 3PL / Contract Logistics Warehousing

• Public Warehousing / Multi-Tenant Model

• Developer-Owned Logistics Parks (Lease-Based Model)

By End-Use Industry

• Retail, E-commerce & Consumer Goods

• Food & Beverages

• Manufacturing & Industrial Goods

• Pharmaceuticals & Healthcare

• Chemicals & Others

By Region

• Kanto (Greater Tokyo and surrounding prefectures)

• Kansai (Osaka–Kobe–Kyoto belt)

• Chubu (Nagoya and industrial corridor)

• Kyushu & Other Regions

Players Mentioned in the Report:

• Nippon Express

• Yamato Holdings

• Sagawa Express

• Mitsui-Soko Holdings

• Sumitomo Warehouse

• Kintetsu World Express

• Japan Logistics Systems

• Regional warehouse operators, cold storage specialists, and logistics park developers

Key Target Audience

• 3PL and contract logistics providers

• Warehousing and cold chain operators

• E-commerce companies and omni-channel retailers

• Food & beverage manufacturers and distributors

• Pharmaceutical and healthcare supply chain players

• Industrial manufacturers and export-driven enterprises

• Logistics real estate developers and institutional investors

• Government bodies and regulators influencing safety and compliance

• Technology vendors (WMS, automation, robotics, material handling)

Time Period:

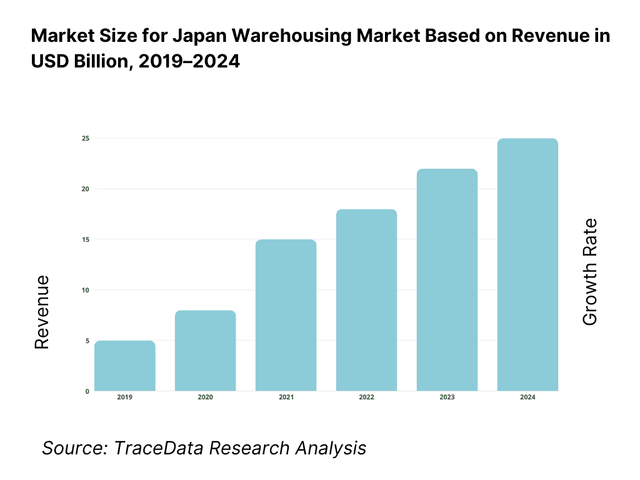

Historical Period: 2019–2024

Base Year: 2025

Forecast Period: 2025–2035

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4. 1 Delivery Model Analysis for Warehousing including captive/in-house warehousing, third-party logistics (3PL), public warehousing, developer-owned logistics parks, and multi-story urban warehouses with margins, preferences, strengths, and weaknesses

4. 2 Revenue Streams for Warehousing Market including storage revenues, handling and throughput charges, value-added services, cold chain premiums, and contract logistics revenues

4. 3 Business Model Canvas for Warehousing Market covering warehouse operators, logistics service providers, real estate developers, automation and WMS providers, transport partners, and end-user industries

5. 1 Organized Warehousing Operators vs Regional and Local Players including large integrated logistics companies, specialist cold chain operators, real estate-backed logistics parks, and small regional warehouse providers

5. 2 Investment Model in Warehousing Market including greenfield warehouse development, brownfield redevelopment, build-to-suit facilities, automation-led capex investments, and cold chain infrastructure investments

5. 3 Comparative Analysis of Warehousing Delivery by In-House Warehousing and Outsourced 3PL / Contract Logistics Models including cost, flexibility, scalability, and service-level considerations

5. 4 Logistics and Supply Chain Cost Allocation comparing warehousing spend versus transportation, last-mile delivery, and inventory holding with average logistics cost share per enterprise

8. 1 Revenues from historical to present period

8. 2 Growth Analysis by warehouse type and by operating model

8. 3 Key Market Developments and Milestones including logistics park developments, cold chain capacity additions, automation adoption, and regulatory or safety standard updates

9. 1 By Market Structure including organized warehousing players, regional operators, and captive facilities

9. 2 By Warehouse Type including ambient warehouses, cold storage, multi-story logistics facilities, and specialized warehouses

9. 3 By Operating Model including in-house warehousing, 3PL / contract logistics, and public warehousing

9. 4 By End-Use Industry including retail & e-commerce, food & beverages, manufacturing, pharmaceuticals & healthcare, and chemicals

9. 5 By Customer Type including large enterprises, SMEs, and trading houses

9. 6 By Service Type including storage, handling, value-added services, and integrated logistics

9. 7 By Temperature Control including ambient, chilled, frozen, and multi-temperature warehousing

9. 8 By Region including Kanto, Kansai, Chubu, Kyushu, and other regions of Japan

10. 1 Shipper Landscape and Industry Cohort Analysis highlighting retail, e-commerce, manufacturing, and pharma-driven demand clusters

10. 2 Warehouse Selection and Outsourcing Decision Making influenced by location, compliance, service levels, automation capability, and cost

10. 3 Utilization and ROI Analysis measuring occupancy rates, throughput efficiency, and contract tenure

10. 4 Gap Analysis Framework addressing Grade-A space shortages, cold chain gaps, labor constraints, and automation adoption challenges

11. 1 Trends and Developments including multi-story warehousing, cold chain expansion, automation and robotics, and digital WMS adoption

11. 2 Growth Drivers including e-commerce growth, aging population, food safety standards, and outsourcing of logistics functions

11. 3 SWOT Analysis comparing large integrated logistics players versus regional warehouse operators

11. 4 Issues and Challenges including land scarcity, aging warehouse stock, labor shortages, and rising operating costs

11. 5 Government Regulations covering building safety and seismic norms, fire regulations, food safety compliance, and pharmaceutical distribution standards in Japan

12. 1 Market Size and Future Potential of cold storage and temperature-controlled warehousing

12. 2 Business Models including dedicated cold storage, multi-tenant cold warehouses, and integrated cold chain logistics

12. 3 Delivery Models and Type of Solutions including frozen, chilled, and multi-temperature facilities with monitoring and backup systems

15. 1 Market Share of Key Players by revenues and warehousing capacity

15. 2 Benchmark of 15 Key Competitors including major integrated logistics providers, cold chain specialists, and logistics park developers operating in Japan

15. 3 Operating Model Analysis Framework comparing integrated logistics providers, pure-play warehousing operators, and real estate-led logistics platforms

15. 4 Gartner Magic Quadrant positioning global logistics leaders and domestic players in warehousing and contract logistics

15. 5 Bowman’s Strategic Clock analyzing competitive advantage through service differentiation, scale efficiency, and cost-led strategies

16. 1 Revenues with projections

17. 1 By Market Structure including organized players, regional operators, and captive facilities

17. 2 By Warehouse Type including ambient, cold storage, and automated facilities

17. 3 By Operating Model including in-house and outsourced warehousing

17. 4 By End-Use Industry including retail, food, manufacturing, and pharmaceuticals

17. 5 By Customer Type including large enterprises and SMEs

17. 6 By Service Type including storage, handling, and value-added services

17. 7 By Temperature Control including ambient and temperature-controlled warehousing

17. 8 By Region including Kanto, Kansai, Chubu, Kyushu, and other regions of Japan

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

We begin by mapping the complete ecosystem of the Japan Warehousing Market across demand-side and supply-side entities. On the demand side, entities include e-commerce platforms, omni-channel retailers, FMCG and consumer goods brands, food & beverage companies, pharmaceutical manufacturers and distributors, automotive and electronics manufacturers, trading houses, and public-sector bodies linked to food security and disaster-response logistics. Demand is further segmented by warehouse role (fulfillment, regional distribution, import/export buffering, returns management), facility type (ambient, cold storage, multi-story Grade-A logistics, specialized compliant storage), and operating approach (in-house vs outsourced to 3PLs). On the supply side, the ecosystem includes integrated logistics providers and 3PLs, warehousing operators, cold chain specialists, logistics real estate developers (logistics parks, multi-story assets), automation and material handling solution providers, WMS/WES technology vendors, construction and engineering firms, and compliance bodies governing building safety, fire protection, food handling, and pharmaceutical distribution. From this mapped ecosystem, we shortlist 8–12 leading warehouse operators and developers based on network scale, asset quality, cold chain capability, metro coverage, automation readiness, and enterprise contract presence. This step establishes how value is created and captured across storage, handling, value-added services, compliance, technology enablement, and integrated distribution execution.

Step 2: Desk Research

An exhaustive desk research process is undertaken to analyze Japan’s warehousing structure, demand drivers, and segment behavior. This includes reviewing Japan logistics real estate trends, e-commerce growth patterns, last-mile network evolution, cold chain expansion, and industrial supply chain requirements linked to automotive, electronics, and precision manufacturing. We assess buyer preferences around proximity to consumption nodes, service-level reliability, inventory accuracy, temperature integrity, and business continuity readiness. Company-level analysis includes review of operator service portfolios, facility footprints, warehouse specifications (floor loading, height, docking, racking), automation adoption, and sector focus (retail, food, pharma, industrial). We also examine the regulatory and compliance environment shaping facility development and operations, including seismic safety and fire requirements, food safety and traceability expectations, and pharma distribution compliance norms. The outcome of this stage is a comprehensive industry foundation that defines the segmentation logic and creates the assumptions needed for market estimation and future outlook modeling through 2035.

Step 3: Primary Research

We conduct structured interviews with warehousing operators, 3PL providers, cold storage specialists, logistics real estate developers, large shippers (retail, e-commerce, FMCG, pharma), and automation/WMS solution providers. The objectives are threefold: (a) validate assumptions around demand concentration by region and industry, outsourcing patterns, and contract structures, (b) authenticate segment splits by warehouse type, temperature category, operating model, and end-use industry, and (c) gather qualitative insights on pricing behavior, occupancy dynamics, service-level expectations, automation ROI, labor constraints, and compliance costs. A bottom-to-top approach is applied by estimating warehouse capacity utilization, typical storage and handling revenue structures, and contract volumes across major segments, which are aggregated to develop the overall market view. In selected cases, disguised buyer-style interactions are conducted with warehouse operators and brokers to validate field-level realities such as lease rate bands, typical escalation clauses, occupancy trends, availability of Grade-A space near metros, and practical constraints in onboarding cold chain or pharma-compliant customers.

Step 4: Sanity Check

The final stage integrates bottom-to-top and top-to-down approaches to cross-validate the market view, segmentation splits, and forecast assumptions. Demand estimates are reconciled with macro indicators such as retail consumption trajectory, e-commerce fulfillment expansion, cold chain penetration, manufacturing output trends, and port/airport-linked trade logistics activity. Assumptions around land constraints, multi-story development pace, labor availability, and automation adoption rates are stress-tested to understand their impact on capacity creation and service pricing. Sensitivity analysis is conducted across key variables including e-commerce growth intensity, cold chain capex cycle, regulatory tightening, energy cost volatility, and disaster-preparedness investments. Market models are refined until alignment is achieved between operator capacity additions, developer pipeline, occupancy utilization, and shipper contracting behavior, ensuring internal consistency and robust directional forecasting through 2035.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Japan warehousing market holds strong potential, supported by steady expansion in e-commerce fulfillment, continued modernization of aging warehouse infrastructure, and rising demand for compliant cold chain and high-spec facilities near dense consumption centers. As supply chains prioritize reliability, temperature integrity, and inventory visibility, demand will increasingly shift toward Grade-A, automation-ready assets and professionally managed warehouse operations. The market’s long-term potential is reinforced by outsourcing growth, value-added logistics services, and resilience-driven investments through 2035.

The market features a mix of large integrated logistics groups, specialist warehousing and cold chain operators, and logistics real estate developers building modern multi-tenant logistics parks. Competition is shaped by network scale, metro coverage, compliance capability (especially for food and pharma), automation readiness, service reliability, and ability to support multi-site enterprise contracts. Regional operators remain relevant in port-centric storage and localized distribution, while national players lead complex contract logistics and high-spec warehousing deployments.

Key growth drivers include expansion of e-commerce and omni-channel distribution, structural growth in cold chain warehousing linked to food modernization and pharmaceutical integrity requirements, and accelerating adoption of warehouse automation due to labor shortages. Additional growth momentum comes from redevelopment of obsolete facilities into multi-story Grade-A logistics assets, deeper outsourcing of warehousing and value-added services, and resilience-led investments in business continuity and disaster preparedness across critical supply chains.

Challenges include land scarcity and high real estate costs near major metros, functional obsolescence in older warehouse stock, and rising operating costs driven by labor shortages and energy intensity, especially in cold storage. Development timelines can be extended by complex building compliance requirements related to seismic safety, fire protection, and permitting. In addition, achieving automation ROI can be difficult for smaller operators due to capex intensity and the need for skilled integration of systems and process redesign.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0