Kenya Auto Finance Market Outlook to 2029

- By Type of Financing Institution, By Vehicle Type, By Loan Tenure, By New vs Used Vehicle, and By Region.

Report Overview

Report Code

TDR0153

Coverage

Africa

Published

April 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Kenya Auto Finance Market Outlook to 2029 - By Type of Financing Institution, By Vehicle Type, By Loan Tenure, By New vs Used Vehicle, and By Region.” provides a comprehensive analysis of the auto finance market in Kenya. The report covers an overview and genesis of the industry, overall market size in terms of credit disbursed and outstanding loans, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the Auto Finance Market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Kenya Auto Finance Market Outlook to 2029 - By Type of Financing Institution, By Vehicle Type, By Loan Tenure, By New vs Used Vehicle, and By Region.” provides a comprehensive analysis of the auto finance market in Kenya. The report covers an overview and genesis of the industry, overall market size in terms of credit disbursed and outstanding loans, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the Auto Finance Market. The report concludes with future market projections based on disbursed credit, by market, product types, region, cause and effect relationship, and success case studies highlighting the major opportunities and cautions.

Kenya Auto Finance Market Overview and Size

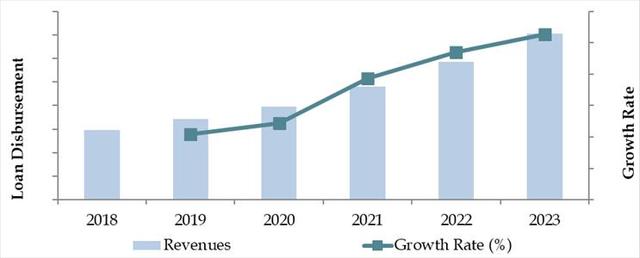

The Kenya auto finance market reached a valuation of KES 250 Billion in outstanding auto loans in 2023, driven by the increasing demand for vehicle ownership, rising urbanization, and evolving consumer behavior towards structured financing options. The market is characterized by major players such as NCBA Bank, Co-operative Bank, Watu Credit, Mogo Kenya, Sidian Bank, and Toyota Kenya Finance. These companies are recognized for their diverse financing schemes, dealership integrations, and customized offerings for both private buyers and commercial users.

In 2023, Watu Credit expanded its two-wheeler and tuk-tuk financing services across Kenya’s coastal and western regions, improving last-mile access to vehicle financing for informal sector workers. Nairobi and Mombasa are key markets due to their commercial density and established automotive networks.

Market Size for Kenya Auto Finance Industry on the Basis of Credit Disbursed in KES Billion, 2018-2023

What Factors are Leading to the Growth of Kenya Auto Finance Market:

Economic Factors: Kenya’s growing middle-income population and rising vehicle import volumes are fueling demand for affordable vehicle financing. Used vehicles account for nearly 85% of all registered vehicles in Kenya in 2023, with financing options offering cost savings and structured payment models for low to middle-income consumers. The increasing need for private and commercial mobility post-pandemic has also played a role in boosting loan disbursements.

Growing Informal and Gig Economy: The expansion of Kenya’s informal workforce, particularly in logistics, delivery, and ride-hailing, is creating demand for flexible auto financing. Two-wheelers and tuk-tuks financed by digital NBFCs such as Watu Credit and Mogo Kenya have become the entry point to asset ownership for gig workers. Monthly repayment plans and low documentation processes have supported growth in this segment.

Digitalization: The rise of mobile-based loan disbursements and credit scoring has streamlined the auto loan journey. In 2023, over 50% of new auto loan applications were initiated via mobile or digital channels. Integration with mobile money services like M-Pesa allows for real-time repayments, reducing default rates and widening financial inclusion. Players like NCBA Loop and Branch are offering mobile-integrated vehicle loan products.

Which Industry Challenges Have Impacted the Growth for Kenya Auto Finance Market

High Interest Rates and Risk Premiums: Despite financial inclusion efforts, the average interest rates on auto loans in Kenya remain significantly high, especially for used vehicles and informal sector borrowers. In 2023, typical annual interest rates ranged from 16% to 25% for NBFCs and microlenders. This has impacted affordability, with an estimated 30% of potential borrowers opting out due to unaffordable repayment burdens. The perceived credit risk, especially among self-employed individuals without formal income documentation, continues to restrict financing availability.

Limited Credit History and Underwriting Gaps: A major constraint in the market is the limited availability of reliable credit history data, particularly among first-time borrowers and informal economy participants. In a recent financial access survey, nearly 40% of auto finance rejections were due to lack of verifiable income or credit history. While mobile lending platforms are addressing this, the underwriting gap remains a structural hurdle for expanding access.

Depreciation and Collateral Value Concerns: For lenders, the resale and residual value of financed vehicles — especially used imports — poses risk in case of loan defaults. The lack of centralized pricing benchmarks for second-hand vehicles complicates risk modeling. According to 2023 data, over 35% of used vehicles depreciate more than 20% annually, limiting their acceptability as collateral in the eyes of traditional lenders.

What are the Regulations and Initiatives which have Governed the Market:

Motor Vehicle Import Regulations: The Kenya Bureau of Standards (KEBS) mandates that all imported used vehicles must not be older than 8 years from the date of first registration and must comply with Euro IV emission standards as of 2023. This has slightly reduced the volume of cheaper but older vehicles entering the market, indirectly impacting the demand for financing among price-sensitive buyers.

Credit Information Sharing Framework: The Central Bank of Kenya (CBK) and Credit Reference Bureaus (CRBs) regulate the credit information ecosystem. Since 2022, updated frameworks require all licensed lenders to report positive and negative borrower data, which is enhancing credit profiling. Over 9 million Kenyans are now listed with CRBs, improving underwriting quality for auto finance.

Digital Credit Guidelines: In 2023, CBK issued regulatory frameworks for Digital Credit Providers (DCPs), bringing fintech-based lenders like Mogo and Watu Credit under formal compliance. The move has enhanced borrower protection, transparency, and standardization of terms, especially in the two-wheeler and tuk-tuk financing segments.

Kenya Auto Finance Market Segmentation

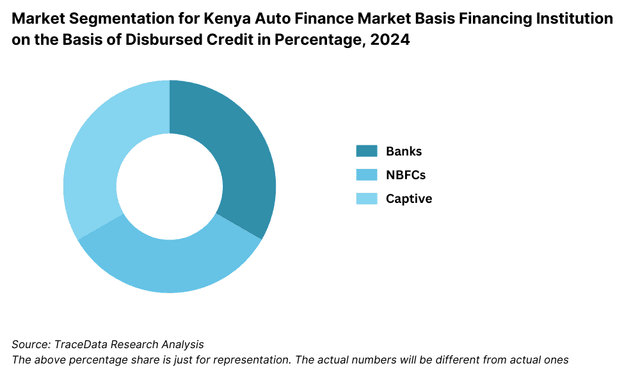

By Type of Financing Institution: Commercial banks dominate the auto finance landscape in Kenya due to their wide branch networks, stronger capital base, and ability to offer lower interest rates for salaried individuals and corporates. Institutions such as NCBA Bank, Co-operative Bank, and Equity Bank lead in terms of market share. On the other hand, Non-Banking Financial Companies (NBFCs) such as Watu Credit and Mogo Kenya are gaining traction by focusing on underserved and informal sector customers with simplified documentation and fast disbursal. Captive finance arms such as Toyota Kenya Finance and DT Dobie’s in-house financing unit support dealer sales with customized schemes, zero down-payment options, and bundled insurance products.

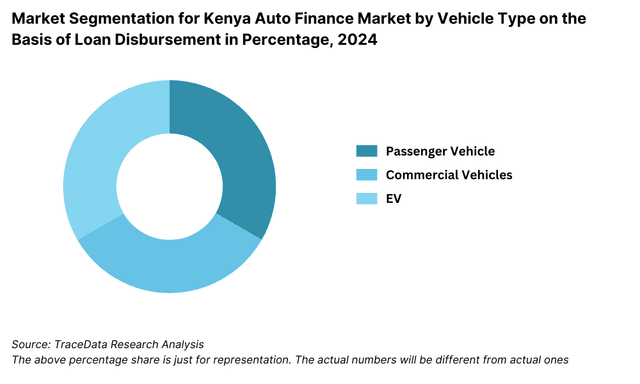

By Vehicle Type: Passenger vehicles form the bulk of financed vehicles in Kenya, particularly compact sedans, hatchbacks, and SUVs used for personal and ride-hailing purposes. They account for a significant share due to increased ownership aspirations and financing options for both new and used units. Two-wheelers and tuk-tuks are largely financed by NBFCs and digital lenders catering to gig workers and small-scale transport entrepreneurs. Commercial vehicles, especially light trucks and pickups, are primarily financed for SME and logistics applications, supported by fleet financing programs.

By Loan Tenure: Auto loans in Kenya are predominantly offered with tenures between 36 to 60 months. A tenure of 48 months is most popular among salaried and formal borrowers as it offers a balanced monthly repayment structure. Meanwhile, informal sector and gig economy borrowers prefer shorter tenures (12–24 months) due to variable incomes and reduced long-term commitments. Digital lenders often offer more flexible repayment schedules aligned with daily or weekly earnings, especially in two-wheeler financing.

Competitive Landscape in Kenya Auto Finance Market

The Kenya auto finance market is moderately fragmented, with both traditional banks and emerging non-banking financial companies (NBFCs) actively operating in the space. In recent years, the expansion of fintech-based lenders and vehicle dealership tie-ups has further diversified the competitive landscape, providing consumers with more accessible, tech-driven, and tailored financing options.

| Company Name | Founding Year | Original Headquarters |

| MOGO Kenya | 2012 | Nairobi, Kenya |

| Watu Credit | 2015 | Mombasa, Kenya |

| Mwananchi Credit | 2010 | Nairobi, Kenya |

| Hakki Africa | 2015 | Nairobi, Kenya |

| Ngao Credit | 2012 | Nairobi, Kenya |

| CFAO Motors Kenya | 1964 | Nairobi, Kenya |

| Autochek Kenya | 2020 | Nairobi, Kenya |

| Motorhub Limited | 2011 | Nairobi, Kenya |

| Simba Corp | 1948 | Nairobi, Kenya |

| Stanbic Bank Kenya | 1958 | Nairobi, Kenya |

| I&M Bank Kenya | 1974 | Nairobi, Kenya |

| NCBA Group | 1959 | Nairobi, Kenya |

| KCB Group | 1896 | Nairobi, Kenya |

| Absa Bank Kenya | 1916 | Nairobi, Kenya |

Some of the recent competitor trends and key information about competitors include:

NCBA Bank: One of the largest lenders in Kenya's auto finance sector, NCBA continues to dominate vehicle financing through its “Asset Finance” product line. In 2023, it reported a 20% increase in auto loan disbursement, with a strong focus on corporate fleets and salaried individuals. Its digital onboarding and dealer integrations are improving loan processing turnaround time.

Co-operative Bank: Known for its expansive branch network and relationship with SACCOs, Co-operative Bank has made major inroads in SME and PSV (Public Service Vehicle) financing. In 2023, the bank introduced a co-financing scheme with Simba Corporation targeting light commercial vehicles, resulting in a 17% increase in loan volumes.

Equity Bank: Equity has aggressively expanded its vehicle loan portfolio by leveraging its mobile app platform and integrating credit scoring tools. In 2023, more than 50% of its auto loans were processed via digital channels. The bank’s partnership with Isuzu East Africa has enabled it to cater to commercial vehicle customers more effectively.

Watu Credit: A fast-growing NBFC focused on two-wheeler and tuk-tuk financing, Watu Credit has financed over 400,000 vehicles as of 2023 across Kenya. Its branchless model, low down payment schemes, and M-Pesa-based repayments have made it highly accessible to gig workers and informal sector earners.

Mogo Kenya: Mogo focuses on motorbike and used car financing with a technology-first approach. In 2023, it expanded its product line to include ride-hailing car loans with flexible repayment schedules. The lender grew its customer base by 28% year-on-year through targeted marketing and quick loan disbursal systems.

Toyota Kenya Finance: The captive arm of Toyota Kenya, it offers structured auto loans for new Toyota vehicles with benefits such as zero processing fees and low down payments. In 2023, the firm launched a trade-in program allowing customers to finance new cars by exchanging older models, boosting new vehicle sales by 12%.

Sidian Bank: Known for working capital solutions, Sidian Bank entered the auto finance market by focusing on asset-backed loans for small fleet owners. Its simplified credit appraisal process and partnership with local dealerships have made it a preferred lender in secondary towns.

What Lies Ahead for Kenya Auto Finance Market?

The Kenya auto finance market is projected to experience steady growth by 2029, supported by a growing middle class, rapid digitalization of financial services, and rising vehicle ownership needs across urban and peri-urban areas. The market is expected to register a strong CAGR during the forecast period, as both formal and informal segments continue to demand affordable and flexible financing solutions.

Rise of Digital Lending Platforms: The continued penetration of smartphones and mobile money platforms is expected to drive digital auto loan applications and disbursements. Fintech lenders are anticipated to expand their presence, especially in two-wheeler and tuk-tuk financing, using AI-driven credit scoring and instant approvals to target underbanked customers. By 2029, it is estimated that over 65% of auto loans will be processed through digital platforms.

Expansion of Green Mobility Financing: With the government promoting the adoption of electric vehicles (EVs) and hybrids through excise duty reductions, financing options for low-emission vehicles are expected to rise. Financial institutions may introduce green auto loans with preferential interest rates, particularly targeting fleet operators and urban mobility startups. This transition will be gradual but important in diversifying the financing mix.

Increased Focus on Used Vehicle Financing: The demand for used cars, which make up over 85% of vehicle imports, will remain strong due to their affordability. Financing products tailored specifically for used vehicles—including bundled insurance, extended repayment tenures, and trade-in financing—are expected to increase significantly, particularly among first-time buyers and small business owners.

Development of Credit Scoring Alternatives: Traditional credit scoring methods will increasingly be supplemented by alternative data sources such as mobile transaction history, ride-hailing app earnings, and utility bill payments. This evolution will widen the credit net and improve auto loan accessibility for self-employed and gig economy workers, especially in rural and semi-urban areas.

Future Outlook and Projections for Kenya Car Finance Market Size on the Basis of Loan Disbursements in USD Billion, 2024-2029

Kenya Auto Finance Market Segmentation

By Type of Financing Institution:

Commercial Banks

Non-Banking Financial Companies (NBFCs)

Captive Finance Companies

Digital Lending Platforms

Microfinance Institutions

By Vehicle Type:

Passenger Vehicles

Commercial Vehicles

Two-Wheelers (Boda Bodas)

Tuk-Tuks (Three-Wheelers)

Electric Vehicles (EVs)

By Loan Tenure:

<12 Months

12–24 Months

25–36 Months

37–60 Months

By Vehicle Condition:

New Vehicles

Used Vehicles

By Borrower Type:

Salaried Individuals

Self-Employed / Informal Sector

SMEs and Fleet Operators

Gig Economy Workers

Ride-Hailing Drivers

By Region:

Nairobi

Mombasa

Kisumu

Nakuru

Eldoret

Other Regions (Meru, Nyeri, Thika, Machakos)

Players Mentioned in the Report (Banks):

- Absa Bank Kenya

- Access Bank Kenya

- Co-operative Bank of Kenya

- Equity Bank Kenya

- Family Bank

- I&M Bank

- KCB Bank Kenya

- National Bank of Kenya

- NCBA Bank Kenya

- Stanbic Bank Kenya

Players Mentioned in the Report (NBFCs):

- M-KOPA

- Kopo Kopo

- Lipa Later

- Watu Gari

- MOGO Kenya

- Mwananchi Credit

- HAKKI Africa

- Ngao Credit

- Autochek

- ASL Credit

Players Mentioned in the Report (Captive):

- Toyota Financial Services Kenya

- Volkswagen Financial Services Kenya

- Mercedes-Benz Financial Services Kenya

- Stellantis Financial Services Kenya

- CFAO Mobility Kenya

Key Target Audience:

Commercial Banks

NBFCs and Microfinance Institutions

Automotive OEMs and Dealership Networks

Ride-Hailing and Logistics Startups

Fintech and Digital Lending Platforms

Government and Regulatory Bodies (e.g., Central Bank of Kenya, NTSA)

Research and Development Institutions

International Development Agencies

Time Period:

Historical Period: 2018–2023

Base Year: 2024

Forecast Period: 2024–2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-Role of Entities, Stakeholders, and challenges they face.

4.2. Relationship and Engagement Model between Banks-Dealers, NBFCs-Dealers and Captive-Dealers-Commission Sharing Model, Flat Fee Model and Revenue streams

5.1. New Car and Used Car Sales in Kenya by type of vehicle, 2018-2024

8.1. Credit Disbursed, 2018-2024

8.2. Outstanding Loan, 2018-2024

9.1. By Market Structure (Bank-Owned, Multi-Finance, and Captive Companies), 2023-2024

9.2. By Vehicle Type (Passenger, Commercial and EV), 2023-2024

9.3. By Region, 2023-2024

9.4. By Type of Vehicle (New and Used), 2023-2024

9.5. By Average Loan Tenure (0-2 years, 3-5 years, 6-8 years, above 8 years), 2023-2024

10.1. Customer Landscape and Cohort Analysis

10.2. Customer Journey and Decision-Making

10.3. Need, Desire, and Pain Point Analysis

10.4. Gap Analysis Framework

11.1. Trends and Developments for Kenya Car Finance Market

11.2. Growth Drivers for Kenya Car Finance Market

11.3. SWOT Analysis for Kenya Car Finance Market

11.4. Issues and Challenges for Kenya Car Finance Market

11.5. Government Regulations for Kenya Car Finance Market

12.1. Market Size and Future Potential for Online Car Financing Aggregators, 2018-2029

12.2. Business Model and Revenue Streams

12.3. Cross Comparison of Leading Digital Car Finance Companies Based on Company Overview, Revenue Streams, Loan Disbursements/Number of Leads Generated, Operating Cities, Number of Branches, and Other Variables

13.1. Finance Penetration Rate and Average Down Payment for New and Used Cars, 2018-2029

13.2. How Finance Penetration Rates are Changing Over the Years with Reasons

13.3. Type of Car Segment for which Finance Penetration is Higher

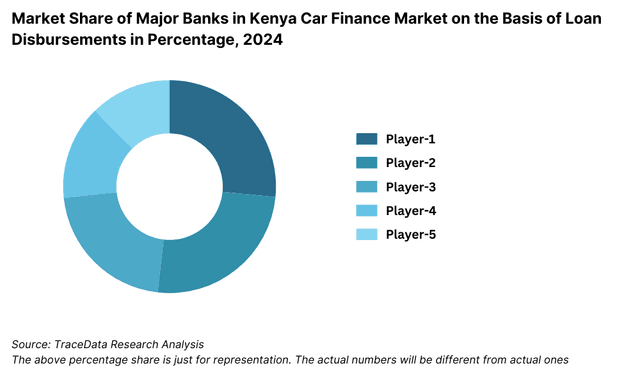

17.1. Market Share of Key Banks in Kenya Car Finance Market, 2024

17.2. Market Share of Key NBFCs in Kenya Car Finance Market, 2024

17.3. Market Share of Key Captive in Kenya Car Finance Market, 2024

17.4. Benchmark of Key Competitors in Kenya Car Finance Market, including Variables such as Company Overview, USP, Business Strategies, Strengths, Weaknesses, Business Model, Number of Branches, Product Features, Interest Rate, NPA, Loan Disbursed, Outstanding Loans, Tie-Ups and others

17.5. Strengths and Weaknesses

17.6. Operating Model Analysis Framework

17.7. Gartner Magic Quadrant

17.8. Bowmans Strategic Clock for Competitive Advantage

18.1. Credit Disbursed, 2025-2029

18.2. Outstanding Loan, 2025-2029

19.1. By Market Structure (Bank-Owned, Multi-Finance, and Captive Companies), 2025-2029

19.2. By Vehicle Type (Passenger, Commercial and EV), 2025-2029

19.3. By Region, 2025-2029

19.4. By Type of Vehicle (New and Used), 2025-2029

19.5. By Average Loan Tenure (0-2 years, 3-5 years, 6-8 years, above 8 years), 2025-2029

19.6. Recommendations

19.7. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand side and supply side entities for Kenya Auto Finance Market. Basis this ecosystem, we shortlist the leading 5–6 financiers in the country based upon their disbursed credit volume, customer base, segment focus (e.g., new cars, used cars, two-wheelers), and geographic reach.

Sourcing is made through industry articles, regulatory filings, financial service portals, news reports, and proprietary databases to perform desk research and collate industry-level information.

Step 2: Desk Research

We undertake an extensive desk research process by referencing a variety of secondary and proprietary databases. This enables comprehensive analysis of the Kenya Auto Finance sector, covering parameters such as size of disbursed credit, outstanding loans, number of lending institutions, regional breakdown, and key demand segments.

Company-level data including credit disbursement trends, partnerships, digital strategies, and borrower demographics are reviewed using press releases, investor presentations, regulatory disclosures, and financial reports.

Step 3: Primary Research

In-depth interviews are conducted with key stakeholders including senior executives from banks, NBFCs, digital lenders, auto dealerships, and consumer borrowers. These interviews help validate market hypotheses, authenticate data collected during desk research, and uncover hidden trends in the financing and vehicle ownership ecosystem.

Bottom to top approach is used to estimate disbursed credit and loan volume per player, which is then aggregated to derive total market size.

Our team also conducts disguised interviews, approaching institutions under the pretext of potential clients. This enables verification of operational data (e.g., loan approval timelines, down payment norms, interest rates, and product offerings), and cross-checking against secondary data to ensure reliability and depth of insights.

Step 4: Sanity Check

- Bottom to top and top to bottom triangulation models are used to ensure consistency and reliability of estimated market size and segment splits. The market is validated using financial modeling techniques and growth projections aligned with macroeconomic indicators, vehicle import volumes, and credit market trends.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Kenya auto finance market holds strong growth potential, reaching an estimated outstanding loan base of KES 250 Billion in 2023. This growth is underpinned by increasing vehicle ownership aspirations, rising used car imports, and the growing acceptance of structured financing across both formal and informal customer segments. The expansion of mobile and digital lending platforms has further enhanced accessibility, especially for first-time and underserved borrowers.

Key players in the Kenya auto finance market include NCBA Bank, Co-operative Bank, Equity Bank, and Sidian Bank. Non-bank lenders such as Watu Credit and Mogo Kenya are also making significant inroads, especially in two-wheeler and tuk-tuk financing. Toyota Kenya Finance and Isuzu East Africa’s in-house finance partnerships support new vehicle sales through structured captive financing models.

Growth in the market is driven by multiple factors, including the affordability gap between new and used vehicles, digitalization of credit disbursement and collections, and the expanding gig economy. The rise of informal transport services, increasing access to credit via mobile money, and favorable vehicle import policies further support the demand for auto financing across consumer categories.

The Kenya auto finance market faces several challenges such as high interest rates, lack of formal credit history among informal sector borrowers, and concerns over the residual value of financed used vehicles. Additionally, regulatory compliance for NBFCs and limited awareness among rural consumers continue to restrict full-scale market penetration. Strengthening data-driven underwriting and regulatory frameworks will be crucial to unlocking long-term growth.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0