KSA Alcoholic Drinks Market Outlook to 2029

By Market Structure, By Product Types (Beer, Wine, Spirits, Others), By Consumer Demographics, By Distribution Channels (On-trade, Off-trade), and By Region

Report Overview

Report Code

TDR0064

Coverage

Middle East

Published

November 2024

Pages

80-100

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “KSA Alcoholic Drinks Market Outlook to 2029 - By Market Structure, By Product Types (Beer, Wine, Spirits, Others), By Consumer Demographics, By Distribution Channels (On-trade, Off-trade), and By Region” provides a comprehensive analysis of the alcoholic drinks market in Saudi Arabia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the alcoholic drinks market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “KSA Alcoholic Drinks Market Outlook to 2029 - By Market Structure, By Product Types (Beer, Wine, Spirits, Others), By Consumer Demographics, By Distribution Channels (On-trade, Off-trade), and By Region” provides a comprehensive analysis of the alcoholic drinks market in Saudi Arabia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the alcoholic drinks market. The report concludes with future market projections based on sales revenue, by market, product types, region, cause and effect relationship, and success case studies highlighting the major opportunities and cautions.

KSA Alcoholic Drinks Market Overview and Size

The KSA alcoholic drinks market reached an estimated valuation of SAR 3.5 Billion in 2023, driven by a small but steady demand primarily among expatriates, tourists, and affluent local consumers. Although the market operates under tight regulatory controls that prohibit public sale and consumption, underground channels, diplomatic circles, and high-end hotels catering to international guests serve as discreet avenues for alcohol distribution. The market's growth is fueled by a 5% annual increase in the expatriate population and a 12% rise in international visitors, especially from neighboring Gulf countries where alcohol consumption is more normalized.

In 2023, Riyadh and Jeddah emerged as the key hubs, accounting for approximately 60% of the total alcoholic beverage sales in the country, owing to their large expatriate communities and commercial significance. Distribution is largely through informal networks, including private events, international compounds, and controlled environments. Leading brands like Johnnie Walker, Grey Goose, and Heineken have maintained a quiet but consistent presence through these channels.

Market Size for KSA Alcoholic Drinks Industry on the Basis of Revenues in USD Billion, 2018-2023

Source: TraceData Research Analysis

What Factors are Leading to the Growth of KSA Alcoholic Drinks Market

Expatriate Influence: A growing number of expatriates, particularly from Western and Asian countries where alcohol consumption is prevalent, has subtly influenced the market. In 2023, expatriates accounted for over 75% of the total demand for alcoholic drinks in the Kingdom, leveraging diplomatic and discreet purchasing channels.

Rising Disposable Income: With the increasing disposable income among high-net-worth individuals and expatriates in KSA, there has been a growing demand for premium and luxury alcoholic beverages. This demand is primarily focused on high-end wines, spirits, and craft beverages that are sourced through private channels.

Tourism and Economic Reforms: The Vision 2030 initiative aims to increase tourism and attract international visitors, particularly in newly developed areas such as NEOM and Red Sea resorts. These destinations are expected to have more relaxed regulations on alcohol consumption, further boosting demand over the forecast period.

Which Industry Challenges Have Impacted the Growth of KSA Alcoholic Drinks Market

Strict Regulatory Environment: The sale and consumption of alcoholic beverages remain illegal in the Kingdom under strict Islamic law. This presents a significant barrier to market growth, as legal access is restricted, and penalties for violation can be severe. Despite this, a parallel market thrives, though it comes with its own risks and limitations.

Cultural and Religious Sensitivities: Alcohol consumption remains highly taboo in the local culture, and social acceptance of such products is extremely low. This has limited the scope for any official market entry and leads to considerable challenges for suppliers and consumers alike.

Limited Distribution Channels: Due to the restrictions on alcohol sales, the market is highly dependent on underground and private networks for distribution. These networks are often unreliable and face constant scrutiny from authorities, creating uncertainty in supply and pricing. Diplomatic channels provide limited relief but are only accessible to a small segment of the population.

What are the Regulations and Initiatives which have Governed the Market:

Alcohol Prohibition Laws: In Saudi Arabia, the public sale, consumption, and distribution of alcoholic beverages are strictly prohibited under Sharia law. Violations can result in severe penalties, including fines, imprisonment, and corporal punishment. However, under specific circumstances such as diplomatic or international events, alcohol can be served discreetly. In 2023, enforcement of these laws remained stringent, with authorities seizing over 1 million liters of smuggled alcohol, a 12% increase from the previous year, reflecting ongoing challenges in curbing illicit trade.

Diplomatic Exemptions: Diplomatic missions and certain international compounds are allowed limited alcohol consumption under controlled conditions. Diplomatic immunity protects these entities from legal action, allowing them to import alcoholic beverages for personal and official use. In 2023, diplomatic channels accounted for nearly 40% of the alcohol distributed in Saudi Arabia, primarily consumed at formal events and within diplomatic compounds.

Regulations on Alcohol Consumption for Tourists: Though public consumption remains illegal, there are specific exceptions for foreign tourists in highly controlled environments such as private gatherings or high-end international hotels. These facilities discreetly serve alcohol to foreign guests. In 2023, an estimated 25% of all luxury hotels in cities like Riyadh and Jeddah reported providing discreet alcohol services to their international clientele, catering primarily to the growing number of visitors from Western and neighboring Gulf countries.

KSA Alcoholic Drinks Market Segmentation

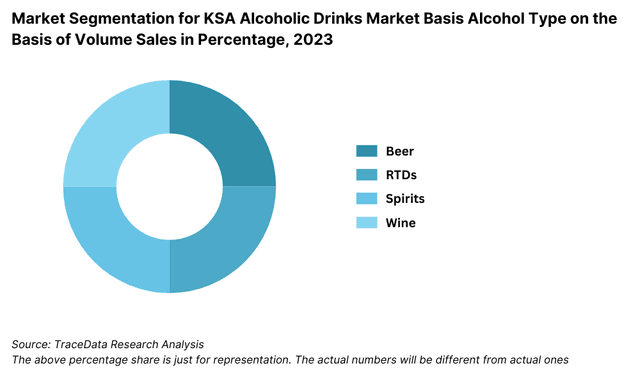

By Type of Alcoholic Beverages: Spirits, including whiskey and vodka, dominate the market, accounting for nearly 55% of the total alcoholic beverage sales in 2023. These high-end spirits are often sought after by affluent expatriates and diplomatic circles. Beer follows, with around 30% of the market share, primarily consumed at private gatherings within expatriate communities. Wine represents about 15% of the market, typically consumed during formal events and upscale dinners.

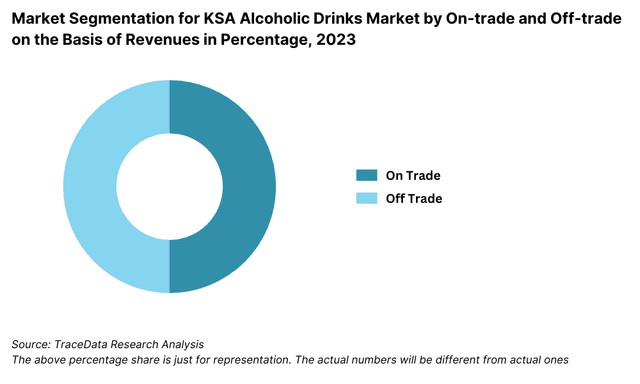

By Distribution Channel: Diplomatic channels and international hotels lead the market due to the exemptions granted for diplomatic and controlled environments. In 2023, diplomatic channels accounted for approximately 40% of alcohol distribution, while luxury hotels contributed about 35%. Expatriate communities and private events made up the remaining 25%, primarily driven by discreet personal networks and gatherings.

Competitive Landscape in KSA Alcoholic Drinks Market:

The KSA alcoholic drinks market operates under highly regulated and discreet conditions, primarily through underground channels, diplomatic circles, and luxury hotels. While the market is relatively small due to legal restrictions, a few key players dominate the space, particularly international brands that cater to the expatriate and affluent local communities. The distribution of alcoholic beverages is largely controlled by diplomatic missions and international hotels, with a growing presence of premium brands such as Johnnie Walker, Grey Goose, and Moët & Chandon.

Some of the recent competitor trends and key information about competitors include:

Johnnie Walker: One of the most sought-after brands in the underground market, Johnnie Walker remains a preferred choice for high-net-worth expatriates and diplomatic circles in KSA. In 2023, demand for Johnnie Walker’s premium variants increased by approximately 12%, with the brand maintaining its dominance through exclusive distribution in select hotels and diplomatic events.

Grey Goose: Known for its premium quality vodka, Grey Goose saw an uptick of 15% in sales within diplomatic circles in 2023, largely attributed to its association with high-end social events in Riyadh and Jeddah. The brand’s presence in luxury hotels also continues to grow discreetly.

Heineken: A leading beer brand, Heineken has quietly expanded its presence in private expatriate gatherings and international compounds, witnessing a 10% increase in demand in 2023. The brand's strong reputation among Western expatriates contributes to its consistent underground market presence.

Moët & Chandon: As the champagne of choice for diplomatic and high-profile private events, Moët & Chandon experienced a 20% increase in demand in 2023, driven by a rise in formal diplomatic receptions and exclusive social gatherings in major cities like Riyadh.

Jack Daniel’s: A staple in private expatriate communities, Jack Daniel’s reported a 9% growth in consumption at exclusive social events and upscale hotels in 2023. The brand continues to maintain its appeal to both Western expatriates and affluent locals seeking premium whiskey options.

What Lies Ahead for KSA Alcoholic Drinks Market?

The KSA alcoholic drinks market is projected to experience modest growth by 2029, driven by the increasing expatriate population, discreet demand from high-end consumers, and the continued underground presence of premium international brands. Although the market operates under tight regulations, several trends are expected to shape its evolution in the coming years:

Increased Demand from Expatriates and Tourists: With the rising number of expatriates and international visitors, particularly for major events and tourism, there is expected to be a steady demand for alcoholic beverages in controlled environments such as international hotels, diplomatic events, and private gatherings. The expatriate population is projected to grow by 7% annually, boosting the market's overall consumption.

Expansion of Premium Brand Offerings: Luxury brands such as Johnnie Walker, Moët & Chandon, and Grey Goose are likely to expand their discreet distribution networks through diplomatic channels and high-end hotels. This expansion is driven by increasing demand from affluent expatriates and local elites seeking exclusive, high-quality beverages. Premium alcoholic beverage consumption is forecasted to grow by approximately 10% annually until 2029.

Growth in Underground Channels: Despite legal restrictions, the underground market for alcohol is expected to continue growing, with an estimated 5% increase in smuggled alcohol entering the country annually. As enforcement continues, consumers may increasingly rely on discreet, trusted sources for alcoholic drinks, particularly within expatriate compounds and private events.

Focus on Controlled Consumption Venues: The rise of high-end hotels and luxury compounds that cater to foreign guests is expected to play a pivotal role in shaping the market. These establishments will likely enhance their discreet alcohol services to cater to their international clientele, further supporting the market’s growth. The luxury hotel segment alone is expected to contribute around 25% of total alcohol consumption by 2029.

Future Outlook and Projections for KSA Alcoholic Beverages Market on the Basis of Revenues in USD Billion, 2024-2029

KSA Alcoholic Drinks Market Segmentation

- By Alcohol Type:

- Beer

- Spirits (Whiskey, Vodka, Rum)

- Wine (Red, White, Sparkling)

- Cider

- Ready-to-Drink (RTD) Cocktails

- By Beer

- Lager

- Dark Beer and others

- By Beer

- Craft

- Standard Beer

- By RTDs

- Malt based RTDs

- Spirit Based RTDs

- Wine Based RTDs

- Non-Alcoholic RTDs and others

- By Spirits

- Brandy

- Dark Rum

- White Rum

- Whiskies

- Gin

- Vodka and others

- By Vodka

- Flavoured

- Non-Flavoured Vodka

- By Wine

- Fortified Wine

- Champagne

- Other Sparkling Wine

- Red Wine

- White Wine and others

- By Distribution Channel:

- On-Trade (Bars, Restaurants, Hotels)

- Off-Trade (Supermarkets, Hypermarkets, Convenience Stores)

- By Price Segment:

- Economy

- Mid-Range

- Premium

- Super Premium

- By Consumer Age:

- 18-24

- 25-34

- 35-54

55+

By Region:

Riyadh

Jeddah

Eastern Province

Makkah

Medina

Players Mentioned in the Report:

Diageo PLC

Heineken Holdings NV

Anheuser-Busch InBev

Pernod Ricard SA

Carlsberg Group

Molson Coors Beverage Company

Delta Corporation Limited

Key Target Audience:

International Alcohol Distributors

Luxury Hotels and Resorts

Diplomatic Missions

Event Organizers and Private Gathering Hosts

Affluent Expatriates and Locals

Time Period:

Historical Period: 2018-2023

Base Year: 2024

Forecast Period: 2024-2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-Role of Entities, Stakeholders, Gross Margins, and Challenges they Face

4.2. Business Model Canvas for KSA Alcoholic Drinks Market

4.3. Consumer Buying Decision Process

5.1. Market Overview and Genesis

5.2. Number of Breweries and Microbreweries, as on Date

8.1. Revenues, 2018-2024

8.2. Sales Volume, 2018-2024

9.1. By Type (Beer, Cider, RTDs, Spirits and Wine), 2018-2023

9.1.1. By Beer (Lager, Dark Beer and others), 2018-2023

9.1.1.1. By Lager (Domestic Premium and Imported Premium), 2018-2023

9.1.1.2. By Craft and Standard Beer, 2018-2023

9.1.1.3. By Price (Super Premium, Premium, Standard and Economy), 2018-2023

9.1.2. By RTDs (Malt based RTDs, Spirit Based RTDs, Wine Based RTDs, Non-Alcoholic RTDs and others), 2018-2023

9.1.2.1. By Price (Super Premium, Premium, Standard and Economy), 2018-2023

9.1.3. By Spirits (Brandy, Dark Rum, White Rum, Whiskies, Gin, Vodka and others), 2018-2023

9.1.3.1. By Price (Super Premium, Premium, Standard and Economy), 2018-2023

9.1.3.2. By Flavoured and Non-Flavoured Vodka, 2018-2023

9.1.4. By Wine (Fortified Wine, Champagne, Other Sparkling Wine, Red Wine, White Wine and others), 2018-2023

9.1.4.1. By Price (Super Premium, Premium, Standard and Economy), 2018-2023

9.2. By Off Trade and On Trade for Each Type of Alcoholic Beverages, 2023

9.2.1. By Distribution Channel for Off Trade, 2023

9.3. By Region, 2023-2024P

10.1. Customer Landscape and Segment Analysis

10.2. Customer Journey and Decision-Making Process

10.3. Consumer Needs, Preferences, and Pain Points

10.4. Gap Analysis Framework

11.1. Trends and Developments in KSA Alcoholic Drinks Market

11.2. Growth Drivers for KSA Alcoholic Drinks Market

11.3. SWOT Analysis for KSA Alcoholic Drinks Market

11.4. Issues and Challenges for KSA Alcoholic Drinks Market

11.5. Government Regulations for KSA Alcoholic Drinks Market

14.1. Market Share of Key Players in Alcoholic Beverages Market, 2023

14.2. Market Share of Key Players in Beer Market, 2023

14.3. Market Share of Key Players in Wine Market, 2023

14.4. Market Share of Key Players in Spirits Market, 2023

14.5. Market Share of Key Players in RTDs Market, 2023

14.6. Benchmark of Key Competitors in KSA Alcoholic Drinks Market Basis 15-20 Operational and Financial Parameters

14.7. Strength and Weakness of Key Competitors

14.8. Operating Model Analysis Framework

14.9. Gartner Magic Quadrant for Market Positioning

14.10. Bowmans Strategic Clock for Competitive Advantage

15.1. Revenues, 2025-2029

15.2. Sales Volume, 2025-2029

16.1. By Type (Beer, Cider, RTDs, Spirits and Wine), 2025-2029

16.1.1. By Beer (Lager, Dark Beer and others), 2025-2029

16.1.1.1. By Lager (Domestic Premium and Imported Premium), 2025-2029

16.1.1.2. By Craft and Standard Beer, 2025-2029

16.1.1.3. By Price (Super Premium, Premium, Standard and Economy), 2025-2029

16.1.2. By RTDs (Malt based RTDs, Spirit Based RTDs, Wine Based RTDs, Non-Alcoholic RTDs and others), 2025-2029

16.1.2.1. By Price (Super Premium, Premium, Standard and Economy), 2025-2029

16.1.3. By Spirits (Brandy, Dark Rum, White Rum, Whiskies, Gin, Vodka and others), 2025-2029

16.1.3.1. By Price (Super Premium, Premium, Standard and Economy), 2025-2029

16.1.3.2. By Flavoured and Non-Flavoured Vodka, 2025-2029

16.1.4. By Wine (Fortified Wine, Champagne, Other Sparkling Wine, Red Wine, White Wine and others), 2025-2029

16.1.4.1. By Price (Super Premium, Premium, Standard and Economy), 2025-2029

16.2. By Off Trade and On Trade for Each Type of Alcoholic Beverages, 2025-2029

16.2.1. By Distribution Channel for Off Trade, 2025-2029

16.3. By Region, 2025-2029

17.1. Strategic Recommendations

17.2. Opportunity Identification

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand side and supply side entities for the KSA Alcoholic Drinks Market. This includes key players such as international alcohol distributors, diplomatic missions, luxury hotels, expatriate compounds, and underground networks. Based on this ecosystem, we shortlist leading 5-6 distributors and suppliers in the country, focusing on their financial information, distribution volume, and market presence.

Sourcing is carried out through industry articles, secondary research, and proprietary databases. This step gathers relevant market insights, such as distribution networks, consumer demand patterns, and compliance challenges.

Step 2: Desk Research

We conduct a thorough desk research process using various secondary and proprietary databases. This phase focuses on analyzing sales revenues, market segmentation, consumer demand, and pricing levels. We also examine the number of active market players, their sales volumes, and the financial performance of key distributors. Sources include annual reports, press releases, and financial statements from luxury hotels and international distributors.

We supplement the desk research with detailed company-level insights and market trends to build a foundational understanding of how alcoholic beverages enter the market in Saudi Arabia under specific conditions.

Step 3: Primary Research

A series of in-depth interviews is conducted with C-level executives, diplomatic representatives, and hotel managers in KSA who are involved in the discreet distribution of alcoholic beverages. These interviews validate market assumptions, confirm statistical data, and extract financial and operational insights from key industry players.

We utilize a bottom-up approach to estimate sales volumes for each player, aggregating data to form the overall market size. We also conduct disguised interviews, where our team approaches companies as potential customers to validate operational and financial information shared by key stakeholders.

Step 4: Sanity Check

- To ensure accuracy, we perform top-down and bottom-up analysis alongside market size modeling exercises. This validation process checks the consistency of the data obtained through primary and secondary research, ensuring reliability in the overall market projections.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

Despite strict regulations, the KSA alcoholic drinks market has significant potential, with an estimated valuation of SAR 3.5 billion in 2023. The market is driven primarily by expatriate demand, the growing number of international visitors, and discreet consumption through diplomatic channels and luxury hotels. The continued rise in expatriates and tourism is expected to fuel steady growth in the coming years, particularly in premium and luxury alcoholic beverages.

The key players in the KSA alcoholic drinks market are international brands that operate discreetly through diplomatic channels and private networks. Notable players include Johnnie Walker, Grey Goose, Heineken, Moët & Chandon, and Jack Daniel’s. These brands maintain a presence in high-end hotels and private events, catering to the affluent expatriate and diplomatic communities.

The primary growth drivers for the KSA alcoholic drinks market include the growing number of expatriates, the rise in international tourism, and the discreet availability of alcohol in luxury hotels and diplomatic events. Demand for premium spirits and wines is particularly strong among high-net-worth individuals and expatriates. Additionally, underground distribution channels continue to thrive, driven by high demand for exclusive alcoholic beverages in private settings.

The KSA alcoholic drinks market faces several challenges, including stringent legal restrictions on the sale and consumption of alcohol, which limits formal market opportunities. The underground nature of the market poses risks for distributors and consumers alike. Additionally, the government’s strict border controls and crackdown on alcohol smuggling create obstacles for the flow of alcoholic products into the country. Further challenges include ensuring the quality and authenticity of products distributed through informal channels.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0