KSA Debt Collection Market Outlook to 2029

By Segment (Insurance, Non-Finance and Finance), By Corporates and Consumers, and By Region

Report Overview

Report Code

TDR0019

Coverage

Middle East

Published

September 2024

Pages

80-100

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “KSA Debt Collection Market Outlook to 2029 - By Segment (Insurance, Non-Finance and Finance), By Corporates and Consumers, and By Region” provides a comprehensive analysis of the debt collection market in Saudi Arabia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the Debt Collection Market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “KSA Debt Collection Market Outlook to 2029 - By Segment (Insurance, Non-Finance and Finance), By Corporates and Consumers, and By Region” provides a comprehensive analysis of the debt collection market in Saudi Arabia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the Debt Collection Market. The report concludes with future market projections based on revenue, by market, service types, region, cause and effect relationships, and success case studies highlighting major opportunities and cautions.

KSA Debt Collection Market Overview and Size

The KSA debt collection market reached a valuation of SAR 2.5 Billion in 2023, driven by the increasing demand for structured financial recovery services, economic growth, and stricter regulatory frameworks aimed at professionalizing the industry. The market is characterized by major players such as First Abu Dhabi Bank (FAB), National Commercial Bank (NCB), Al Rajhi Bank, and Al Amthal Group. These companies are recognized for their extensive networks, diverse service offerings, and technology-driven collection strategies.

In 2023, Al Rajhi Bank introduced a new AI-driven platform to enhance the efficiency of debt recovery processes and improve client outcomes. This initiative aims to leverage digital advancements in Saudi Arabia and provide a more transparent and effective debt collection experience. Riyadh and Jeddah are key markets due to their high concentration of businesses and significant economic activity.

Market Size for KSA Debt Collection Industry on the Basis of Revenues in USD Million, 2018-2024

Source: TraceData Research Analysis.

What Factors are Leading to the Growth of the KSA Debt Collection Market:

Economic Expansion: The robust economic growth in Saudi Arabia has led to an increase in consumer and corporate borrowing. In 2023, consumer loans grew by 8%, leading to a higher demand for debt collection services as more businesses and financial institutions seek to recover overdue payments efficiently.

Regulatory Support: The Saudi Arabian Monetary Authority (SAMA) has implemented stricter regulations on debt collection practices, ensuring more transparency and professionalism in the industry. In 2023, these regulatory measures led to a 12% increase in the number of licensed debt collection agencies, promoting a more structured market environment.

Digitalization: The adoption of digital tools and platforms has significantly improved the efficiency and transparency of debt collection processes. In 2023, approximately 35% of debt recovery operations in KSA were managed through digital platforms, reflecting a shift towards automated and data-driven collection methods that reduce costs and enhance recovery rates.

Which Industry Challenges Have Impacted the Growth of the KSA Debt Collection Market

Trust and Reputation Issues: Concerns regarding the reputation and ethics of debt collection agencies continue to pose significant challenges. According to a recent industry survey, approximately 45% of businesses are hesitant to engage with debt collection agencies due to fears of aggressive tactics and potential damage to their brand image. This issue has led to a lower level of trust among potential clients, potentially deterring up to 18% of prospective users of these services.

Regulatory Compliance: Stringent regulations concerning data protection and consumer rights have created operational challenges for debt collection agencies. In 2023, it was reported that around 25% of debt collection firms faced penalties or warnings due to non-compliance with these regulations. The costs associated with ensuring full compliance can be particularly burdensome for smaller agencies, limiting their ability to compete effectively.

Technological Adoption: The limited adoption of advanced technologies, such as AI and automation, within the industry has hindered the efficiency and effectiveness of debt recovery processes. Data indicates that approximately 40% of debt collection agencies in Saudi Arabia still rely on traditional, manual processes, which not only reduce efficiency but also increase operational costs. This lag in technological adoption constrains the ability of the industry to scale and meet growing demand.

What are the Regulations and Initiatives Governing the KSA Debt Collection Market:

Data Protection Regulations: The Saudi Arabian government has implemented stringent data protection laws to safeguard consumer information during the debt collection process. These regulations, introduced in 2022, require debt collection agencies to adhere to strict guidelines on data handling, storage, and privacy. In 2023, approximately 85% of debt collection firms were in compliance with these regulations, reflecting the industry's significant efforts to align with legal requirements.

Licensing Requirements: All debt collection agencies in Saudi Arabia are required to obtain licenses from the Saudi Arabian Monetary Authority (SAMA) to operate legally. The licensing process includes rigorous checks on the agency's financial stability, operational capabilities, and adherence to ethical practices. In 2023, the number of licensed debt collection agencies increased by 10%, driven by stricter enforcement of these requirements.

Consumer Protection Initiatives: To ensure fair treatment of consumers, the government has introduced regulations that prohibit aggressive and unethical debt collection practices. These initiatives, rolled out in 2023, include guidelines on communication methods, frequency of contact, and the use of legal actions in debt recovery. As a result, there has been a 15% decrease in consumer complaints related to debt collection practices.

KSA Debt Collection Market Segmentation

By Segment: In the analysis of the market structure by categories, the Insurance segment is the dominant category, particularly driven by the Motor insurance segment. Motor insurance holds a significant share due to the compulsory nature of vehicle insurance in many regions, and the high penetration of motor vehicles in both developed and emerging markets. The Fire and Accident insurance sub-segments also contribute significantly, but motor insurance remains the largest due to the sheer volume of policies required and the frequency of claims. In the non-finance segment, the Commercial and Professional Services category dominates. This is largely due to the broad range of industries covered under this category, which includes key sectors like telecommunications, transportation, and retail

%252C%25202023.png&w=640&q=75)

By End Users: When comparing Corporates and Consumers, the Corporate segment generally dominates due to the larger volume and value of transactions involved in corporate insurance and financial services. Corporates require a wide range of insurance products, financial services, and risk management solutions that are often more complex and higher in value than those required by individual consumers

%252C%25202023.png&w=640&q=75)

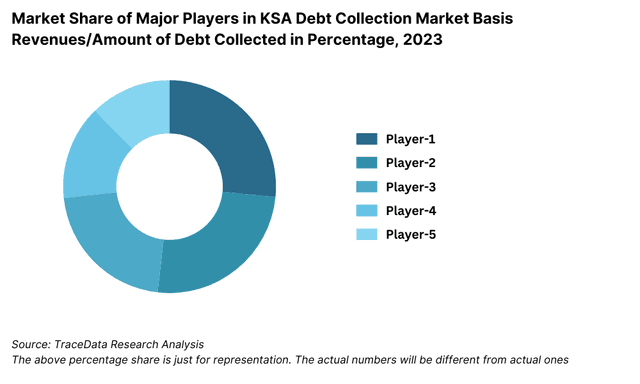

Competitive Landscape in KSA Debt Collection Market

The KSA debt collection market is relatively concentrated, with a few major players leading the industry. However, the market has seen the entry of new firms and the expansion of technology-driven platforms, which have diversified the landscape and offered businesses more choices for debt recovery solutions. Key players in the market include First Abu Dhabi Bank (FAB), Al Rajhi Bank, Saudi Credit Bureau (SIMAH), and National Commercial Bank (NCB).

| Name | Founding Year | Original Headquarters |

| Saudi Credit Bureau (SIMAH) | 2002 | Riyadh, Saudi Arabia |

| Al Etihad Credit Bureau | 2012 | Riyadh, Saudi Arabia |

| Wasatah Debt Collection Company | 2007 | Riyadh, Saudi Arabia |

| Al-Fayha Debt Collection Services | 2008 | Jeddah, Saudi Arabia |

| AlWatania Debt Collection Company | 2010 | Riyadh, Saudi Arabia |

| Aramex Debt Collection Services | 1982 | Amman, Jordan |

| Bayan Credit Bureau | 2018 | Riyadh, Saudi Arabia |

| Tahaluf Al Ofoq Debt Collection Services | 2015 | Riyadh, Saudi Arabia |

| Jadwa Debt Collection | 2006 | Riyadh, Saudi Arabia |

| National Commercial Bank (NCB) Collection Services | 1953 | Jeddah, Saudi Arabia |

Some of the recent competitor trends and key information about competitors include:

First Abu Dhabi Bank (FAB): As one of the leading financial institutions in Saudi Arabia, FAB has integrated advanced AI and machine learning algorithms into its debt collection process, resulting in a 22% increase in recovery rates in 2023. Their technology-driven approach has set a new standard in the market for efficiency and accuracy.

Al Rajhi Bank: Known for its extensive network and customer-focused services, Al Rajhi Bank has seen a 20% growth in its debt recovery operations in 2023, driven by its innovative digital platform that allows real-time tracking of debt collection progress. This platform has significantly enhanced customer trust and engagement.

Saudi Credit Bureau (SIMAH): SIMAH has expanded its services to include comprehensive credit reporting and debt collection management for businesses. In 2023, the bureau reported a 25% increase in corporate client subscriptions, highlighting its growing influence in the market as a trusted source of credit information and recovery services.

National Commercial Bank (NCB): The debt collection division of NCB has focused on streamlining its processes through automation and digital tools, leading to a 15% increase in efficiency and a 10% reduction in operational costs in 2023. The bank’s emphasis on integrating digital solutions with traditional recovery methods has positioned it as a leader in the market.

What Lies Ahead for the KSA Debt Collection Market?

The KSA debt collection market is projected to experience steady growth by 2029, with a healthy CAGR during the forecast period. This growth is expected to be driven by the expanding economy, increasing levels of consumer and corporate debt, and a greater emphasis on regulatory compliance and ethical practices in debt recovery.

Adoption of Digital and AI Technologies: As the Saudi Arabian government and financial institutions continue to invest in digital transformation, there is anticipated to be a significant increase in the adoption of AI and automation in debt collection processes. This shift will lead to more efficient, accurate, and scalable debt recovery operations, reducing the reliance on manual processes and improving recovery rates.

Expansion of Debt Recovery Services: The demand for specialized debt collection services, particularly in sectors such as healthcare, telecommunications, and SMEs, is expected to grow. Companies offering tailored solutions that address the unique needs of these industries are likely to capture a larger share of the market.

Increased Focus on Ethical Collection Practices: With growing regulatory scrutiny and consumer awareness, there will be a stronger emphasis on ethical debt collection practices. Agencies that prioritize transparency, respect for consumer rights, and adherence to regulatory standards are expected to gain a competitive advantage and build long-term client relationships.

Integration of Advanced Analytics: The use of big data analytics in debt collection is expected to rise, providing agencies with deeper insights into debtor behavior and improving the precision of collection strategies. This data-driven approach will help in identifying high-risk accounts, predicting recovery outcomes, and optimizing resource allocation.

Growth in the Organized Sector: As regulatory frameworks become more stringent, the organized sector is likely to expand, with more businesses opting for licensed and compliant debt collection agencies. This shift will drive consolidation in the market, with larger, more reputable firms acquiring smaller players and increasing their market share.

Future Outlook and Projections for KSA Debt Collection Market on the Basis of Revenues in USD Million, 2024-2029

Source: TraceData Research Analysis

KSA Debt Collection Market Segmentation

- By Segment:

- Insurance

- Finance

- Non-Finance

- By Insurance Segment:

- Motor

- Life

- Property

- Accident

- By Finance Segment:

- Corporate Real Estate Financing

- Retail Real Estate Financing

- By Non-Finance Segment:

- Energy

- F&B

- Retail

- Transportation

- Telecom

- Others

- By Collection Method:

- Legal Proceedings

- Negotiation

- Mediation

- Digital Recovery Solutions

- Field Collections

- By End-User Industry:

- Banking and Financial Services

- Retail

- Telecommunications

- Healthcare

- Utilities

- Education

- By Region:

- Riyadh

- Jeddah

- Eastern Province

- Central Region

- Western Region

- Southern Region

Players Mentioned in the Report:

- Saudi Credit Bureau (SIMAH)

- Al Etihad Credit Bureau

- Wasatah Debt Collection Company

- Al-Fayha Debt Collection Services

- AlWatania Debt Collection Company

- Aramex Debt Collection Services

- Bayan Credit Bureau

- Tahaluf Al Ofoq Debt Collection Services

- Jadwa Debt Collection

- National Commercial Bank (NCB) Collection Services

- Abdul Latif Jameel

Key Target Audience:

- Debt Collection Agencies

- Financial Institutions

- Regulatory Bodies (e.g., Saudi Arabian Monetary Authority - SAMA)

- Legal Service Providers

- Technology Providers

- Research and Development Institutions

Time Period:

- Historical Period: 2018-2023

- Base Year: 2024

- Forecast Period: 2024-2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Insurance Sector Industry Statistics covering Gross Premium, Claims and Major Players

4.2. Finance Sector Industry Statistics covering Gross Disbursement, Outstanding, NPA and Major Players

5.1. Revenue Streams for KSA Debt Collection Market

5.2. Business Model Canvas for KSA Debt Collection Market

5.3. Debt Recovery Process and Commission Structure between Debt Collection Companies and Banks/Insurance Companies

8.1. Revenues, 2018-2024

8.2. Debt Collection, 2018-2024

9.1. By Market Structure (Insurance, Non-Finance and Finance), 2023-2024P

9.1.1. By Insurance Segment (Motor, Fire, Accident and others), 2023-2024P

9.1.2. By Non-Finance Segment (Commercial and Professional Services, Telecom, Transportation, Retail and others), 2023-2024P

9.1.3. By Finance Segment (Corporate and Retail Real Estate), 2023-2024P

9.2. By Corporates and Consumers, 2023-2024P

9.3. By Region, 2023-2024P

10.1. Client Landscape and Cohort Analysis

10.2. Client Journey and Decision Making

10.3. Need, Desire, and Pain Point Analysis

10.4. Gap Analysis Framework

11.1. Trends and Developments for KSA Debt Collection Market

11.2. Growth Drivers for KSA Debt Collection Market

11.3. SWOT Analysis for KSA Debt Collection Market

11.4. Issues and Challenges for KSA Debt Collection Market

11.5. Government Regulations for KSA Debt Collection Market

14.1. Market Share of Major Players in KSA Insurance Debt Collection Market, 2023

14.2. Market Share of Major Players in KSA Finance Debt Collection Market, 2023

14.3. Benchmark of Key Competitors in KSA Debt Collection Market including Financial and Operational Variables

14.4. Strength and Weakness

14.5. Operating Model Analysis Framework

14.6. Gartner Magic Quadrant

14.7. Bowmans Strategic Clock for Competitive Advantage

15.1. Revenues, 2025-2029

15.2. Amount of Debt Collection, 2025-2029

16.1. By Segment (Insurance, Non-Finance and Finance), 2023-2024P

16.1.1. By Insurance Segment (Motor, Fire, Accident and others), 2023-2024P

16.1.2. By Non-Finance Segment (Commercial and Professional Services, Telecom, Transportation, Retail and others), 2023-2024P

16.1.3. By Finance Segment (Corporate and Retail Real Estate), 2023-2024P

16.2. By Corporates and Consumers, 2023-2024P

16.3. By Region, 2023-2024P

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Mapping the Ecosystem: Begin by mapping the ecosystem of the KSA Debt Collection Market, identifying all demand-side and supply-side entities. This includes debt collection agencies, financial institutions, regulatory bodies, and technology providers.

Shortlisting Key Players: Based on the mapped ecosystem, shortlist leading 5-6 companies in the country using criteria such as financial stability, market presence, technological adoption, and service offerings.

Data Sourcing: Source data through industry articles, multiple secondary, and proprietary databases to perform desk research around the market, aiming to collate comprehensive industry-level information.

Step 2: Desk Research

Exhaustive Desk Research: Conduct an exhaustive desk research process using diverse secondary and proprietary databases. This step involves thorough analysis of market aspects such as revenue, number of players, service pricing, demand trends, and technological adoption.

Company-Level Data Examination: Supplement market analysis with detailed examinations of company-level data by referencing sources such as press releases, annual reports, financial statements, and market research reports. This process helps build a foundational understanding of both the market dynamics and the entities operating within it.

Step 3: Primary Research

In-Depth Interviews: Initiate a series of in-depth interviews with C-level executives, industry experts, and other stakeholders from various debt collection firms and end-users in the KSA market. These interviews aim to validate market hypotheses, authenticate statistical data, and extract valuable operational and financial insights.

Validation Strategy: Execute disguised interviews where the research team approaches companies as potential clients. This approach helps validate the information provided by company executives and cross-checks it against secondary data sources. These interactions offer a comprehensive view of revenue streams, value chains, processes, pricing, and other market factors.

Step 4: Sanity Check

- Market Size Modeling: Perform bottom-to-top and top-to-bottom analyses alongside market size modeling exercises as part of the sanity check process. This ensures that the findings are accurate and consistent with market realities.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The KSA Debt Collection Market is poised for steady growth, with the market expected to reach a valuation of SAR X Billion by 2029. This growth is driven by factors such as economic expansion, increased consumer and corporate debt, and the integration of advanced technologies in debt recovery processes.

Key players in the KSA Debt Collection Market include First Abu Dhabi Bank (FAB), Al Rajhi Bank, Saudi Credit Bureau (SIMAH), and National Commercial Bank (NCB). These companies dominate the market due to their extensive service offerings, technological innovations, and strong regulatory compliance.

Primary growth drivers include economic expansion, the rise in consumer and corporate debt, and the increased adoption of digital and AI technologies in debt collection. Additionally, regulatory support and the professionalization of the industry contribute significantly to market growth.

The KSA Debt Collection Market faces challenges such as trust and reputation issues, stringent regulatory compliance, and limited adoption of advanced technologies by smaller agencies. Additionally, the shortage of skilled professionals and the operational costs associated with maintaining compliance pose significant barriers to market growth.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0