KSA Home Furniture Market Outlook to 2035

By Product Category, By Room Type, By Material, By Price Segment, By Sales Channel, and By Region

Report Overview

Report Code

TDR0466

Coverage

Middle East

Published

January 2026

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “KSA Home Furniture Market Outlook to 2035 – By Product Category, By Room Type, By Material, By Price Segment, By Sales Channel, and By Region” provides a comprehensive analysis of the home furniture industry in the Kingdom of Saudi Arabia. The report covers an overview and genesis of the market, overall market size in terms of value, detailed market segmentation; trends and developments, regulatory and standards landscape, buyer-level demand profiling, key issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the KSA home furniture market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “KSA Home Furniture Market Outlook to 2035 – By Product Category, By Room Type, By Material, By Price Segment, By Sales Channel, and By Region” provides a comprehensive analysis of the home furniture industry in the Kingdom of Saudi Arabia. The report covers an overview and genesis of the market, overall market size in terms of value, detailed market segmentation; trends and developments, regulatory and standards landscape, buyer-level demand profiling, key issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the KSA home furniture market. The report concludes with future market projections based on residential construction activity, urban housing expansion, household formation trends, consumer lifestyle shifts, localization of furniture manufacturing, retail modernization, regional demand drivers, cause-and-effect relationships, and case-based illustrations highlighting the major opportunities and cautions shaping the market through 2035.

KSA Home Furniture Market Overview and Size

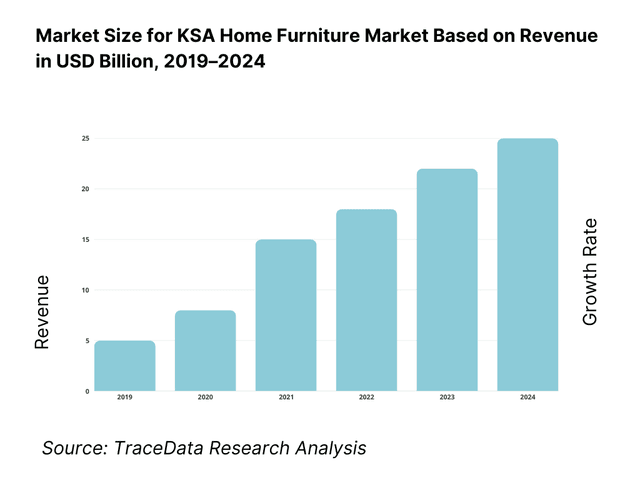

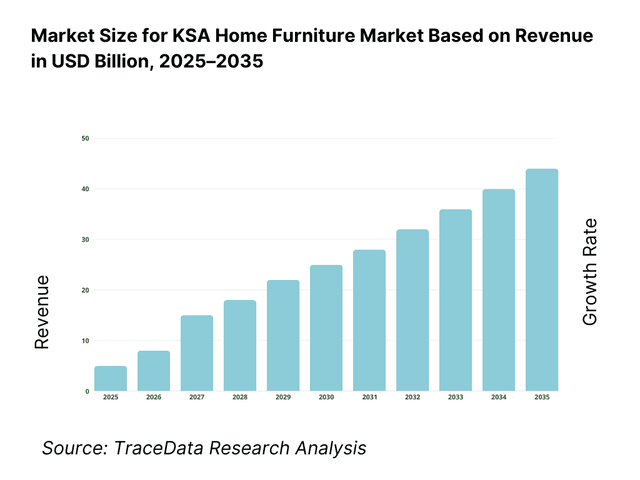

The KSA home furniture market is valued at approximately ~USD ~ billion, representing the sale of furniture products used in residential settings, including living rooms, bedrooms, dining areas, kitchens, home offices, and outdoor residential spaces. The market encompasses a wide range of furniture categories such as seating, tables, storage units, beds, wardrobes, modular furniture, and décor-integrated functional furniture, supplied through both organized and unorganized retail channels.

The market is anchored by Saudi Arabia’s expanding housing stock, high household formation rates among young nationals, sustained residential development under Vision 2030, and rising disposable incomes that support discretionary spending on home improvement and interior aesthetics. Furniture demand is closely linked to new home completions, apartment handovers, villa developments, and refurbishment activity, particularly in urban centers where lifestyle-oriented housing formats are gaining prominence.

Saudi Arabia’s home furniture market also reflects evolving consumer preferences toward modern designs, space-efficient layouts, modular and ready-to-assemble furniture, and coordinated interior themes. The increasing influence of global retail brands, exposure to international design trends, and digital retail platforms has reshaped buyer expectations around quality, customization, pricing transparency, and delivery timelines.

From a regional perspective, the Central Region, led by Riyadh, represents the largest demand center due to high population concentration, large-scale residential projects, and strong purchasing power. The Western Region follows, supported by housing demand in Jeddah, Makkah, and Madinah, including both permanent residences and secondary homes. The Eastern Region contributes steady demand driven by urban housing, expatriate populations, and higher-income households. Southern and Northern regions account for smaller but gradually expanding demand, supported by government housing initiatives and localized retail expansion.

What Factors are Leading to the Growth of the KSA Home Furniture Market:

Expansion of residential construction and housing delivery supports sustained furniture demand: Saudi Arabia continues to invest heavily in residential real estate development as part of its national housing and urban development agenda. Large-scale housing programs, private developer-led communities, and mixed-use urban projects are increasing the number of new housing units delivered annually. Each new home creates demand across multiple furniture categories, including core essentials such as beds, sofas, wardrobes, dining sets, and storage solutions. Furniture purchases are often front-loaded at the time of home handover, making residential construction cycles a primary demand driver for the market.

Rising household formation, young population, and lifestyle upgrades increase replacement and first-time purchases: The Kingdom’s young demographic profile, combined with higher marriage rates, nuclear family structures, and increasing female workforce participation, is driving new household formation. First-time homeowners and renters typically invest in complete furniture sets, while existing households are increasingly upgrading furniture to reflect changing lifestyle preferences. Demand is shifting from purely functional furniture toward products that offer improved aesthetics, comfort, and alignment with modern interior design trends, supporting higher average ticket sizes over time.

Growing preference for modern, modular, and space-efficient furniture formats: Urban living, apartment-style housing, and compact floor plans are increasing the relevance of modular, multifunctional, and space-saving furniture solutions. Consumers are showing greater interest in modular sofas, extendable dining tables, storage-integrated beds, and customizable wardrobes. These formats allow flexibility, scalability, and efficient space utilization, particularly in urban apartments. Organized furniture retailers and international brands have played a key role in shaping this preference by introducing standardized modular systems tailored to regional living patterns.

Which Industry Challenges Have Impacted the Growth of the KSA Home Furniture Market:

Dependence on imported raw materials and finished furniture increases cost volatility and lead-time uncertainty: A significant portion of the home furniture sold in Saudi Arabia—particularly mid- to premium-segment products—relies on imported raw materials, semi-finished components, or fully assembled furniture sourced from Asia, Europe, and regional manufacturing hubs. Fluctuations in freight rates, foreign exchange movements, and global raw material prices for wood, engineered boards, fabrics, foams, and metals can directly impact landed costs. These dynamics create pricing volatility for retailers and manufacturers, complicate inventory planning, and may reduce price competitiveness in cost-sensitive consumer segments. Longer import lead times can also constrain product availability during peak housing handover cycles, affecting sales conversion.

Fragmented supply base and variable quality standards create inconsistency in consumer experience: The KSA home furniture market includes a mix of large organized retailers, regional manufacturers, small workshops, and import traders. While this diversity supports wide product availability, it also results in uneven quality standards, after-sales service capability, and warranty practices. Inconsistent finishing quality, durability concerns, and limited customization flexibility among lower-tier suppliers can affect consumer confidence. For organized players, maintaining consistent quality across private-label and third-party sourced products remains a challenge, particularly when scaling across regions with different supplier ecosystems.

Logistics, last-mile delivery, and installation complexity impact customer satisfaction and operating costs: Furniture logistics in Saudi Arabia involves handling bulky, fragile, and high-value products that often require specialized transportation, warehousing, and in-home installation. Challenges related to last-mile delivery—such as access constraints in high-density residential areas, coordination with customers, and availability of trained installation crews—can increase delivery costs and lead to delays. Returns and replacements are particularly costly in furniture retail, and service failures during delivery or installation can negatively impact brand perception and repeat purchases.

What are the Regulations and Initiatives which have Governed the Market:

Quality, safety, and consumer protection regulations governing furniture products and materials: Home furniture sold in Saudi Arabia must comply with national standards and regulations related to product safety, material quality, and consumer protection. These include requirements for structural integrity, load-bearing capacity, stability of furniture items, and the use of safe materials, particularly for products such as beds, seating, and children’s furniture. Compliance with labeling, warranty disclosure, and after-sales service obligations is increasingly emphasized, shaping how manufacturers and retailers design products and communicate value to consumers.

Import regulations, conformity assessment, and certification requirements influencing sourcing decisions: Imported furniture and furniture components are subject to conformity assessment procedures, documentation requirements, and certification under Saudi regulatory frameworks. These processes influence supplier selection, sourcing geographies, and shipment timelines. Retailers and distributors must ensure compliance with applicable standards for materials, finishes, and packaging, which can increase administrative overhead and favor larger players with established compliance capabilities over smaller importers.

Localization initiatives and industrial development programs supporting domestic furniture manufacturing: Under Vision 2030, Saudi Arabia is promoting local manufacturing across multiple consumer goods categories, including furniture. Industrial incentives, economic zones, and support for SME manufacturing encourage local production of wooden furniture, metal furniture, upholstery, and modular systems. These initiatives aim to reduce import dependence, create employment, and strengthen domestic value chains. Over time, localization policies are expected to influence sourcing strategies, expand private-label manufacturing, and improve cost competitiveness of locally produced furniture in the mid-market segment.

KSA Home Furniture Market Segmentation

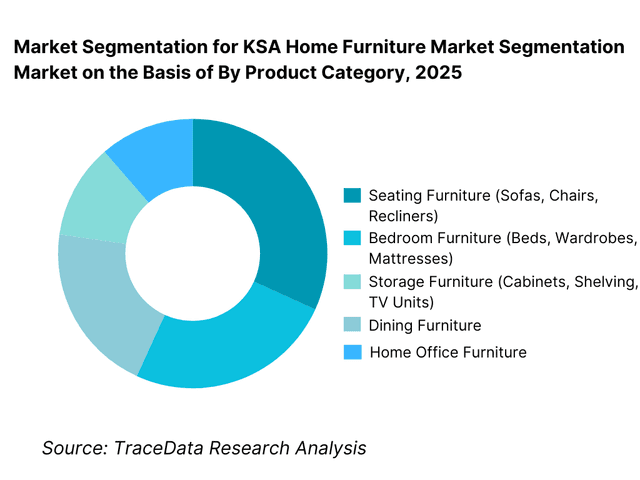

By Product Category: Seating and bedroom furniture hold dominance. Seating and bedroom furniture represent the largest share of the KSA home furniture market, as these categories are core to both first-time household furnishing and replacement demand. Sofas, beds, wardrobes, and mattresses account for a significant portion of furniture spending due to their functional necessity, higher average selling prices, and frequent upgrade cycles linked to lifestyle and design preferences. Living room seating benefits from social and family-oriented home layouts common in Saudi households, while bedroom furniture demand is reinforced by high household formation rates and new housing handovers. Storage and dining furniture follow steadily, supported by apartment living and modern interior layouts, while home office and outdoor furniture remain smaller but fast-growing segments.

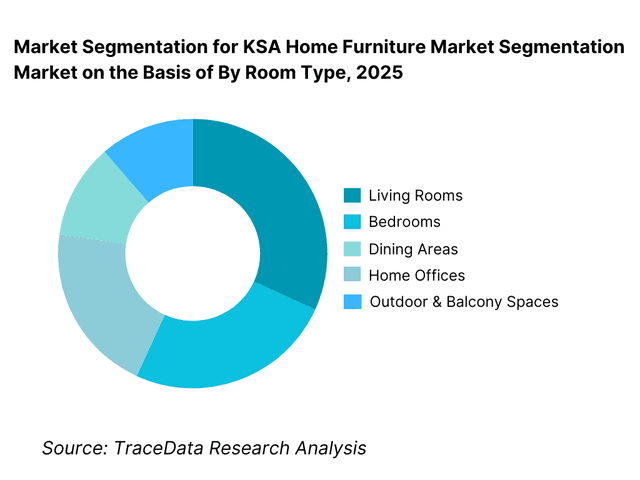

By Room Type: Living rooms and bedrooms dominate household furniture spending. Living rooms and bedrooms account for the majority of furniture demand in Saudi homes, as these spaces receive the highest investment in terms of comfort, aesthetics, and functionality. Living rooms are central to family gatherings and guest hosting, driving demand for premium seating and coordinated furniture sets. Bedrooms represent consistent demand due to the need for multiple room setups within a household and higher replacement frequency for beds and mattresses. Dining areas, home offices, and outdoor spaces contribute smaller but growing shares as lifestyle preferences evolve.

Competitive Landscape in KSA Home Furniture Market

The KSA home furniture market exhibits moderate concentration, characterized by the presence of large international furniture retailers, regional brands, and domestic manufacturers operating alongside a fragmented base of local workshops and import traders. Competitive intensity is shaped by product design, pricing, brand perception, showroom experience, delivery reliability, and after-sales service. International brands and large regional players dominate organized retail and mall-based formats, while local manufacturers and carpentry units remain competitive in customized and made-to-order furniture segments.

Name | Founding Year | Original Headquarters |

IKEA | 1943 | Älmhult, Sweden |

Home Centre | 1995 | Dubai, UAE |

PAN Emirates | 1992 | Sharjah, UAE |

Ashley Furniture | 1945 | Wisconsin, USA |

Al Rugaib Furniture | 1958 | Dammam, Saudi Arabia |

Pottery Barn | 1949 | California, USA |

West Elm | 2002 | New York, USA |

Midas Furniture | 1993 | Dubai, UAE |

Some of the Recent Competitor Trends and Key Information About Competitors Include:

IKEA: IKEA continues to dominate the organized furniture retail segment in Saudi Arabia through its large-format stores, standardized modular furniture systems, and strong value-for-money positioning. The brand benefits from high brand recall, efficient supply chains, and strong alignment with apartment living and young households. Localization of select product ranges and integration of digital ordering and delivery services strengthen its market position.

Home Centre: Home Centre maintains a strong presence in mid-range furniture and home décor, with a focus on coordinated collections and lifestyle-led merchandising. Its competitiveness is supported by broad assortments, frequent promotions, and mall-based store locations that attract family shoppers.

PAN Emirates: PAN Emirates competes aggressively on pricing and variety, offering a wide mix of contemporary and traditional designs. The brand’s ability to cater to value-conscious consumers while maintaining acceptable quality levels supports steady demand across urban markets.

Ashley Furniture: Ashley Furniture operates primarily in the mid-to-premium segment, emphasizing comfort-oriented seating and bedroom furniture. Its positioning appeals to consumers seeking durable, larger-format furniture suited for villas and spacious apartments.

Al Rugaib Furniture: As a long-established Saudi brand, Al Rugaib Furniture benefits from strong local market understanding, regional store coverage, and a balanced portfolio spanning mid-range to premium products. The company’s reputation for quality and service supports loyalty among domestic consumers.

What Lies Ahead for KSA Home Furniture Market?

The KSA home furniture market is expected to expand steadily through 2035, supported by sustained residential construction activity, rising household formation, and ongoing lifestyle upgrades among Saudi consumers. Growth momentum is reinforced by Vision 2030–linked housing initiatives, increasing urbanization, and the expansion of organized retail and omnichannel furniture platforms. As homebuyers and renters increasingly seek coordinated interiors, modern designs, and reliable delivery and installation services, home furniture spending will remain closely aligned with housing handovers and renovation cycles across the Kingdom.

Transition Toward Modular, Space-Efficient, and Lifestyle-Oriented Furniture Solutions: The future of the KSA home furniture market will see a continued shift from standalone furniture purchases toward modular, multifunctional, and coordinated furniture systems. Urban apartments and modern housing layouts are increasing demand for space-efficient sofas, storage-integrated beds, modular wardrobes, and adaptable dining solutions. Consumers are placing greater emphasis on furniture that balances aesthetics, functionality, and flexibility, particularly among younger households and first-time homeowners. Brands that offer configurable systems, consistent design languages, and customization within standardized platforms are expected to capture higher-value demand.

Growing Role of Organized Retail, Omnichannel Models, and Branded Private Labels: Organized furniture retailers and brand-led showrooms will continue to gain share at the expense of fragmented, unorganized sellers. Large-format stores, mall-based outlets, and digitally integrated showrooms enable consumers to visualize complete home setups and make bundled purchases. E-commerce and omnichannel models will increasingly support discovery, comparison, and repeat purchases, particularly for standardized furniture and accessories. Private-label furniture ranges will expand further, allowing retailers to control pricing, margins, and product differentiation while improving supply chain reliability.

Increased Focus on Local Manufacturing, Assembly, and Supply Chain Localization: Localization of furniture manufacturing and assembly will play a more prominent role through 2035, aligned with Saudi Arabia’s broader industrial development agenda. Domestic production of wooden furniture, metal frames, upholstery, and modular components is expected to expand, particularly in the mid-range segment. Local manufacturing reduces import lead times, improves responsiveness to demand fluctuations, and supports competitive pricing. Over time, localized supply chains are expected to improve quality consistency and enable faster product refresh cycles.

Rising Importance of Delivery Reliability, Installation Quality, and After-Sales Service: As furniture purchases become higher value and more design-driven, consumers will increasingly prioritize service quality alongside product attributes. Reliable delivery scheduling, professional installation, damage-free handling, and responsive after-sales support will become critical differentiators. Retailers and manufacturers that invest in logistics infrastructure, trained installation teams, and digital order tracking will strengthen brand trust and customer retention.

KSA Home Furniture Market Segmentation

By Product Category

• Seating Furniture (Sofas, Chairs, Recliners)

• Bedroom Furniture (Beds, Wardrobes, Mattresses)

• Storage Furniture (Cabinets, Shelving, TV Units)

• Dining Furniture

• Home Office Furniture

• Outdoor & Other Furniture

By Room Type

• Living Rooms

• Bedrooms

• Dining Areas

• Home Offices

• Outdoor & Balcony Spaces

By Material

• Wood & Engineered Wood

• Upholstered (Fabric & Leather-based)

• Metal

• Plastic & Composite

By Price Segment

• Economy

• Mid-Range

• Premium

By Sales Channel

• Organized Furniture Retail & Brand Showrooms

• E-commerce & Omnichannel

• Traditional Carpentry & Local Workshops

• Other Channels

By Region

• Central Region

• Western Region

• Eastern Region

• Southern Region

• Northern Region

Players Mentioned in the Report:

• IKEA

• Home Centre

• PAN Emirates

• Ashley Furniture

• Al Rugaib Furniture

• Pottery Barn

• West Elm

• Midas Furniture

• Local furniture manufacturers, carpentry workshops, and private-label suppliers

Key Target Audience

• Furniture manufacturers and component suppliers

• Organized furniture retailers and brand owners

• Residential real estate developers and housing project developers

• Interior designers and fit-out contractors

• Logistics, delivery, and installation service providers

• E-commerce and omnichannel furniture platforms

• Private equity and consumer-focused investors

• Government bodies involved in housing and industrial localization initiatives

Time Period:

Historical Period: 2019–2024

Base Year: 2025

Forecast Period: 2025–2035

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4. 1 Delivery Model Analysis for Home Furniture-Organized Retail, E-commerce/Omnichannel, Direct-to-Consumer, Custom Carpentry [Margins, Preference, Strength & Weakness]

4. 2 Revenue Streams for KSA Home Furniture Market [Product Sales, Private Labels, Custom Orders, Installation & After-Sales Services]

4. 3 Business Model Canvas for KSA Home Furniture Market [Key Partners, Key Activities, Value Propositions, Customer Segments, Cost Structure, Revenue Streams]

5. 1 Local Players vs Global Brands [Saudi Manufacturers vs International Furniture Brands]

5. 2 Investment Model in KSA Home Furniture Market [Local Manufacturing Investments, Retail Expansion, PE/VC Investments, Strategic Partnerships]

5. 3 Comparative Analysis of Furniture Demand in New Housing vs Replacement Market [Buying Triggers, Budget Allocation, Design Preferences]

5. 4 Furniture Spend Allocation by Household Type [Apartments, Villas, Gated Communities]

8. 1 Revenues (Historical Trend)

9. 1 By Market Structure (Organized Retail vs Unorganized/Custom Furniture)

9. 2 By Product Category (Seating, Bedroom, Dining, Storage, Home Office, Outdoor)

9. 3 By Material (Wood & Engineered Wood, Upholstered, Metal, Plastic & Composite)

9. 4 By Price Segment (Economy, Mid-Range, Premium)

9. 5 By Room Type (Living Room, Bedroom, Dining Area, Home Office, Outdoor Spaces)

9. 6 By Sales Channel (Retail Stores, E-commerce, Direct/Custom Orders)

9. 7 By Branded vs Private Label Furniture

9. 8 By Region (Central Region, Western Region, Eastern Region, Southern Region, Northern Region)

10. 1 Household & Developer Buyer Landscape and Cohort Analysis

10. 2 Furniture Purchase Drivers & Decision-Making Process

10. 3 Value Perception, Quality Expectations & Spend Analysis

10. 4 Gap Analysis Framework

11. 1 Trends & Developments in KSA Home Furniture Market

11. 2 Growth Drivers for KSA Home Furniture Market

11. 3 SWOT Analysis for KSA Home Furniture Market

11. 4 Issues & Challenges for KSA Home Furniture Market

11. 5 Government Regulations for KSA Home Furniture Market

12. 1 Market Size and Future Potential for Organized & E-commerce Furniture in KSA

12. 2 Business Models & Revenue Streams [Private Labels, D2C, Omnichannel Retailing]

12. 3 Delivery Models & Furniture Offerings [Ready-to-Assemble, Modular, Custom Furniture]

15. 1 Market Share of Key Players in KSA Home Furniture Market (By Revenues)

15. 2 Benchmark of Key Competitors [Company Overview, USP, Business Strategies, Business Model, Store Footprint, Revenues, Pricing Strategy, Product Portfolio, Key Customer Segments, Strategic Partnerships, Marketing Strategy, Recent Developments]

15. 3 Operating Model Analysis Framework

15. 4 Competitive Positioning Matrix for Furniture Brands

15. 5 Bowman’s Strategic Clock for Competitive Advantage

16. 1 Revenues (Projections)

17. 1 By Market Structure (Organized Retail and Custom Furniture)

17. 2 By Product Category (Seating, Bedroom, Dining, Storage, Home Office, Outdoor)

17. 3 By Material (Wood, Upholstered, Metal, Plastic & Composite)

17. 4 By Price Segment (Economy, Mid-Range, Premium)

17. 5 By Room Type (Living, Bedroom, Dining, Home Office, Outdoor)

17. 6 By Sales Channel (Retail, E-commerce, Direct/Custom)

17. 7 By Branded vs Private Label Furniture

17. 8 By Region (Central, Western, Eastern, Southern, Northern)

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

We begin by mapping the complete ecosystem of the KSA Home Furniture Market across demand-side and supply-side entities. On the demand side, entities include residential real estate developers, individual homeowners, rental housing operators, expatriate households, interior designers, fit-out contractors, and bulk buyers furnishing housing projects and serviced residences. Demand is further segmented by housing type (apartments, villas, gated communities), purchase trigger (new home handover, replacement, refurbishment), price sensitivity (economy, mid-range, premium), and buying channel (organized retail, e-commerce, custom carpentry).

On the supply side, the ecosystem includes international furniture brands, regional furniture retailers, domestic furniture manufacturers, carpentry workshops, upholstery units, material suppliers (wood, engineered boards, fabrics, foams, metals), logistics and installation service providers, e-commerce platforms, and regulatory and conformity assessment bodies. From this mapped ecosystem, we shortlist 8–12 leading organized furniture retailers and manufacturers based on store footprint, brand strength, product breadth, pricing architecture, localization initiatives, and presence across major Saudi regions. This step establishes how value is created and captured across design, sourcing, manufacturing, retail, delivery, installation, and after-sales service.

Step 2: Desk Research

An exhaustive desk research process is undertaken to analyze the KSA home furniture market structure, demand drivers, and segment behavior. This includes reviewing residential construction pipelines, housing delivery programs, urbanization trends, household formation dynamics, and consumer spending patterns related to home improvement and furnishings. We analyze shifts in consumer preferences toward modern, modular, and space-efficient furniture, as well as the growing role of organized retail and omnichannel sales models.

Company-level analysis includes review of retailer positioning, product category focus, private-label strategies, sourcing geographies, pricing tiers, and service offerings such as delivery, installation, and warranties. We also assess regulatory and compliance dynamics related to furniture imports, product standards, consumer protection, and localization initiatives influencing sourcing and manufacturing decisions. The outcome of this stage is a comprehensive industry foundation that defines segmentation logic and establishes the assumptions used for market estimation and long-term outlook modeling.

Step 3: Primary Research

We conduct structured interviews with furniture manufacturers, organized retailers, sourcing and merchandising heads, interior designers, fit-out contractors, logistics providers, and end consumers. The objectives are threefold:

(a) validate assumptions around demand concentration by product category, price segment, and region.

(b) authenticate market splits by room type, material, and sales channel; and

(c) gather qualitative insights on pricing behavior, discounting intensity, import lead times, inventory planning, delivery challenges, and consumer expectations around quality and after-sales service.

A bottom-to-top approach is applied by estimating household-level furniture spend, new housing handover volumes, and replacement cycles across key regions, which are aggregated to develop the overall market view. In selected cases, disguised buyer-style interactions are conducted with retailers and carpentry workshops to validate field-level realities such as customization timelines, installation quality, delivery reliability, and common service-related pain points.

Step 4: Sanity Check

The final stage integrates bottom-to-top and top-to-down approaches to cross-validate market size estimates, segmentation splits, and forecast assumptions. Demand estimates are reconciled with macro indicators such as housing completions, population growth, income trends, and consumer spending on durable goods. Assumptions around import dependency, localization pace, pricing inflation, and retail expansion are stress-tested to understand their impact on market growth. Sensitivity analysis is conducted across key variables including housing delivery rates, consumer confidence, e-commerce penetration, and private-label expansion. Market models are refined until alignment is achieved between supplier capacity, retail throughput, and end-user demand, ensuring internal consistency and robust directional forecasting through 2035.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The KSA home furniture market holds strong long-term potential, supported by sustained residential construction activity, rising household formation, and increasing consumer spending on home interiors and lifestyle upgrades. Demand is reinforced by Vision 2030–linked housing initiatives, urban apartment living, and a growing preference for organized retail and branded furniture solutions. As replacement and refurbishment cycles expand alongside new home deliveries, the market is expected to maintain steady growth through 2035.

The market features a mix of international furniture brands, regional Middle East retailers, established Saudi furniture companies, and a fragmented base of local carpentry workshops. Organized retailers dominate mid-range and premium segments through large-format showrooms and omnichannel models, while local manufacturers and workshops remain relevant in customized and made-to-order furniture. Competition is shaped by design appeal, pricing, delivery reliability, and after-sales service quality.

Key growth drivers include expansion of residential housing stock, rising household formation among young nationals, increasing urbanization, and evolving consumer preferences toward modern and modular furniture. Additional momentum comes from retail modernization, growing e-commerce penetration, improved logistics and installation capabilities, and government-led initiatives supporting local furniture manufacturing and supply chain localization.

Challenges include dependence on imported furniture and raw materials, exposure to freight and currency volatility, fragmented quality standards among suppliers, and complexity in last-mile delivery and installation. Demand cyclicality linked to housing handovers and promotional buying periods can also impact inventory planning and margin stability. Addressing service consistency and after-sales reliability remains critical for long-term brand differentiation.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0