KSA Personal Finance Market Outlook to 2029

By Market Structure, By Financial Institutions (Commercial Banks, NBFCs, Fintech and others), By Types of Loans (Wedding Loans, Home Renovation Loans, Travel Loan, Medical loans, Debt Consolidation Loan and Others), By Consumer Segments

Report Overview

Report Code

TDR0023

Coverage

Middle East

Published

September 2024

Pages

80-100

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled "KSA Personal Finance Market Outlook to 2029 - By Market Structure, By Financial Institutions (Commercial Banks, NBFCs, Fintech and others), By Types of Loans (Wedding Loans, Home Renovation Loans, Travel Loan, Medical loans, Debt Consolidation Loan and Others), By Consumer Segments, By Age of Borrowers, and By Region." provides a comprehensive analysis of the personal finance market in Saudi Arabia.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled "KSA Personal Finance Market Outlook to 2029 - By Market Structure, By Financial Institutions (Commercial Banks, NBFCs, Fintech and others), By Types of Loans (Wedding Loans, Home Renovation Loans, Travel Loan, Medical loans, Debt Consolidation Loan and Others), By Consumer Segments, By Age of Borrowers, and By Region." provides a comprehensive analysis of the personal finance market in Saudi Arabia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities, bottlenecks, and company profiling of major players in the Personal Finance Market. The report concludes with future market projections based on revenue, by market, product types, regions, cause-and-effect relationships, and success case studies highlighting major opportunities and cautions.

KSA Personal Finance Market Overview and Size

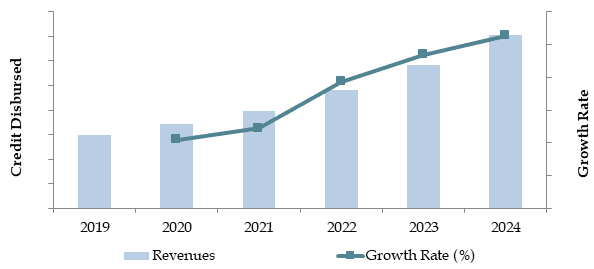

The KSA personal finance market reached a valuation of SAR 200 Billion in 2023, driven by the increasing demand for consumer loans, growing financial inclusion, and rising adoption of Islamic finance principles. Major players such as Al Rajhi Bank, Saudi National Bank, Riyad Bank, and Alinma Bank dominate the market. These institutions are recognized for their extensive financial offerings, large customer bases, and competitive loan products.

In 2023, Saudi National Bank launched new digital platforms to enhance customer experience and streamline the loan application process. This initiative aims to cater to the growing demand for convenient and accessible financial services in Saudi Arabia. Riyadh and Jeddah are key markets due to their high population density and strong economic activities.

Market Size for KSA Personal Finance Industry on the Basis of Credit Disbursed, 2018-2024

Source: TraceData Research Analysis

What Factors are Leading to the Growth of the KSA Personal Finance Market:

Economic Growth: The stable and growing economy of Saudi Arabia has led to a rise in disposable income and consumer spending, driving the demand for personal finance products such as personal loans, home loans, and credit facilities. In 2023, personal finance products accounted for 60% of all retail banking services, as consumers increasingly sought credit to support lifestyle improvements.

Growing Middle Class: The expanding middle class in Saudi Arabia has significantly boosted demand for personal finance products, particularly among individuals seeking home renovations, education, and weddings. The middle-income population in Saudi Arabia grew by 10% in recent years, driving demand for loans that can help improve living standards.

Digitalization of Financial Services: The rise of digital banking platforms has transformed the personal finance landscape, allowing consumers to easily apply for loans online, track repayments, and access financial products with greater transparency and convenience. In 2023, around 45% of personal finance transactions in Saudi Arabia were conducted digitally, reflecting the increasing reliance on technology to manage personal finances.

Which Industry Challenges Have Impacted the Growth of the KSA Personal Finance Market:

Credit Risk and Debt Management: Concerns about high personal debt levels and the ability of consumers to manage their loans have become significant challenges. According to a recent industry report, approximately 30% of borrowers are at risk of defaulting on their personal loans due to inadequate financial planning and unexpected economic downturns. This issue has led to more stringent lending practices by financial institutions, potentially limiting loan access for certain consumer segments.

Regulatory Restrictions: Strict regulatory controls, particularly around Islamic finance principles and interest rate caps, can limit the flexibility of financial institutions in offering diverse loan products. In 2023, around 15% of loan applications were rejected due to non-compliance with regulatory standards, creating barriers for both banks and consumers.

Limited Financial Literacy: A significant portion of the population lacks sufficient knowledge about personal finance products, leading to uninformed borrowing decisions. Data suggests that nearly 40% of loan holders are unclear about the terms of their loans, which increases the risk of dissatisfaction and default. This challenge not only affects the growth of the market but also highlights the need for improved financial education initiatives.

What are the Regulations and Initiatives Which Have Governed the Market:

Islamic Finance Regulations: The Saudi Arabian Monetary Authority (SAMA) mandates that personal finance products adhere strictly to Sharia-compliant principles, which include prohibitions on charging interest (riba) and speculative financial activities. In 2023, approximately 80% of personal loans issued in Saudi Arabia followed Islamic finance regulations, reflecting the significant demand for Sharia-compliant products.

Loan-to-Value (LTV) Ratio Restrictions: To curb excessive borrowing and protect both consumers and financial institutions, the Saudi government has imposed restrictions on the Loan-to-Value ratio, particularly for housing loans. In 2023, the LTV ratio was capped at 70% for first-time home buyers, limiting the maximum loan amount and requiring larger down payments from borrowers.

Financial Inclusion Initiatives: The Saudi government has introduced various initiatives to boost financial inclusion, including programs to enhance access to credit for small businesses and low-income individuals. In 2023, these initiatives led to a 15% increase in the number of micro-loans provided by financial institutions, helping underserved segments access formal credit channels.

KSA Personal Finance Market Segmentation

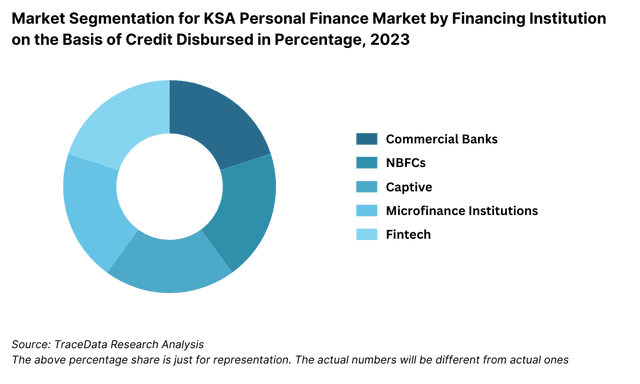

By Financial Institutions: Commercial banks dominate the personal finance market in Saudi Arabia due to their extensive reach, well-established trust with customers, and wide range of financial products. Islamic banks hold a significant share because they offer Sharia-compliant financial products that are preferred by a large portion of the population. Fintech companies are emerging players, offering innovative, digital-first solutions that cater to tech-savvy consumers, while microfinance institutions focus on providing small loans to underserved segments.

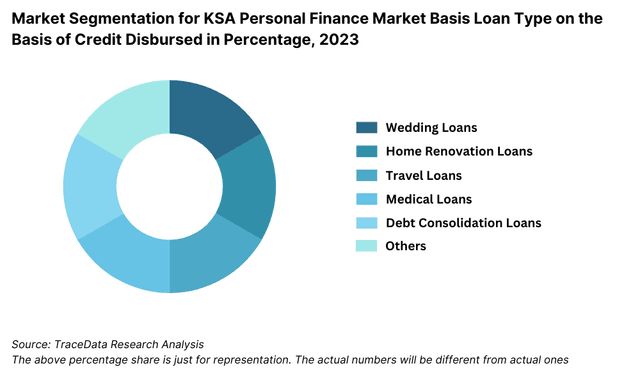

By Loan Type: Home loans dominate the personal finance market in Saudi Arabia, driven by strong demand for residential properties and government-backed housing initiatives. Personal loans follow closely, often used for education, weddings, or home improvements. Car loans also represent a significant portion of the market, supported by the growing demand for vehicle ownership.

By Age of Borrower: The 25-40 age group is the largest demographic for personal finance products, representing individuals in their prime earning years who are likely to seek loans for home purchases, education, and family expenses. The 41-55 age group also holds a considerable share, particularly in the home loan and investment segments, while the 18-24 age group is increasingly engaging with smaller loans, often through fintech platforms.

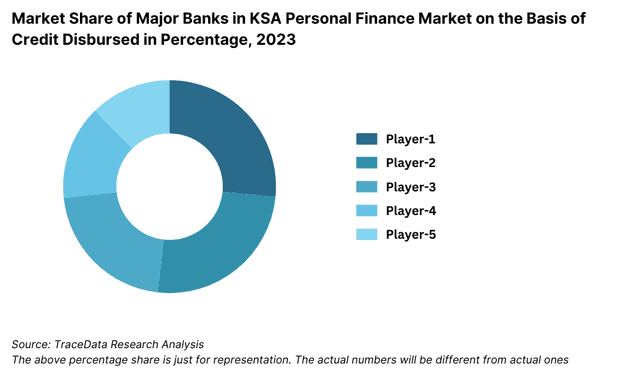

Competitive Landscape in KSA Personal Finance Market

The KSA personal finance market is relatively concentrated, with a few major financial institutions dominating the space. However, the rise of fintech firms and digital banking services has diversified the market, offering consumers more choices and innovative solutions. Major players include Al Rajhi Bank, Saudi National Bank, Riyad Bank, Alinma Bank, and various emerging fintech platforms.

| Name | Type | Founding Year | Headquarters |

| National Commercial Bank (NCB) | Bank | 1953 | Jeddah, Saudi Arabia |

| Al Rajhi Bank | Bank | 1957 | Riyadh, Saudi Arabia |

| Saudi British Bank (SABB) | Bank | 1978 | Riyadh, Saudi Arabia |

| Riyad Bank | Bank | 1957 | Riyadh, Saudi Arabia |

| Arab National Bank (ANB) | Bank | 1979 | Riyadh, Saudi Arabia |

| Alinma Bank | Bank | 2006 | Riyadh, Saudi Arabia |

| Saudi Investment Bank (SAIB) | Bank | 1976 | Riyadh, Saudi Arabia |

| Bank Albilad | Bank | 2004 | Riyadh, Saudi Arabia |

| Bank Aljazira | Bank | 1975 | Jeddah, Saudi Arabia |

| Saudi Home Loans (SHL) | NBFC | 2007 | Riyadh, Saudi Arabia |

| Saudi Finance Company (SFC) | NBFC | 1990 | Riyadh, Saudi Arabia |

| Emkan Finance | NBFC | 2019 | Riyadh, Saudi Arabia |

| Al Yusr Leasing and Financing | NBFC | 2003 | Riyadh, Saudi Arabia |

| Abdul Latif Jameel Finance | NBFC | 1945 | Jeddah, Saudi Arabia |

| Tamweel Aloula | NBFC | 2006 | Riyadh, Saudi Arabia |

| Tamara | Fintech | 2020 | Riyadh, Saudi Arabia |

| Lendo | Fintech | 2019 | Riyadh, Saudi Arabia |

| Sarwa | Fintech | 2018 | Riyadh, Saudi Arabia |

| Hala (HalaFintech) | Fintech | 2017 | Riyadh, Saudi Arabia |

| Mada Pay | Fintech | 2018 | Riyadh, Saudi Arabia |

| PayTabs | Fintech | 2014 | Dammam, Saudi Arabia |

Some of the recent competitor trends and key information about competitors include:

Al Rajhi Bank: As one of the largest Islamic banks in the world, Al Rajhi Bank remains a dominant player in the personal finance market. In 2023, the bank recorded a 12% growth in personal loan disbursements, driven by its strong customer service and extensive product offerings tailored to the needs of Saudi consumers. Al Rajhi Bank has also invested heavily in digital platforms, seeing a 25% increase in online loan applications.

Saudi National Bank: Known for its broad range of Sharia-compliant loan products, Saudi National Bank saw a 15% rise in personal loan applications in 2023. The bank's focus on simplifying the loan application process through digital channels has enhanced customer convenience, resulting in higher loan disbursements.

Riyad Bank: Riyad Bank has expanded its reach in the personal finance market by offering competitive interest rates and flexible repayment options. In 2023, the bank reported a 10% increase in personal loans, with a significant portion of growth attributed to its targeted marketing campaigns for middle-income and young borrowers.

Alinma Bank: Alinma Bank has positioned itself as a key player in the Islamic finance sector, with personal loans being one of its fastest-growing segments. In 2023, the bank experienced a 20% growth in personal finance services, particularly driven by its strong presence in both retail and corporate banking.

Tamweel Aloula: As an emerging fintech company, Tamweel Aloula has gained traction in the personal finance market by offering quick, hassle-free micro-loans through its fully digital platform. In 2023, the company saw a 30% increase in micro-loans, catering to underserved segments in rural and urban areas.

What Lies Ahead for KSA Personal Finance Market?

The KSA personal finance market is projected to grow steadily by 2029, exhibiting a healthy CAGR during the forecast period. This growth will be driven by economic expansion, increasing financial inclusion, and the rising adoption of digital and Islamic finance products.

Increased Demand for Sharia-Compliant Products: As consumer preferences continue to shift towards Islamic finance, the market is expected to see a significant rise in the demand for Sharia-compliant personal finance products. This trend will be further supported by regulatory frameworks promoting Islamic banking and growing consumer awareness of Islamic finance principles.

Digital Transformation in Banking: The rapid digitalization of the financial services sector is likely to continue reshaping the personal finance market in Saudi Arabia. With more banks and fintech companies investing in AI, automation, and data analytics, consumers will benefit from faster, more transparent, and user-friendly loan application processes.

Growth of Fintech and Microfinance: The fintech sector is expected to play a crucial role in expanding access to personal finance products, particularly among underserved and rural populations. The rise of digital lending platforms and microfinance institutions will allow for greater financial inclusion, providing small, short-term loans to individuals who may not have access to traditional banking services.

Focus on Financial Literacy: There is an increasing focus on improving financial literacy across the Kingdom. As more educational programs and initiatives are launched to help consumers better understand loan terms, credit management, and financial planning, this will likely enhance responsible borrowing and reduce default rates.

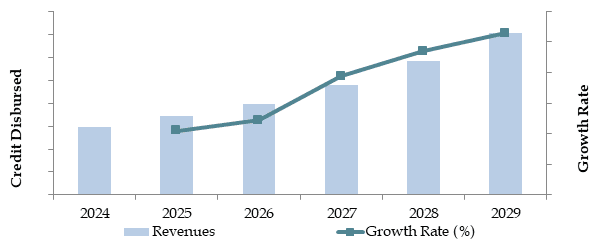

Future Outlook and Projections for KSA Personal Finance Market on the Basis of Credit Disbursed in USD Million, 2024-2029

Source: TraceData Research Analysis

KSA Personal Finance Market Segmentation

- By Market Structure:

- Organized Sources

- Unorganized Sources

- By Loan Type:

- Personal Loans

- Home Loans

- Car Loans

- Education Loans

- Micro-Loans

- Debt Consolidation Loans

- Education Loans

- By Age of Borrower:

- 18-24

- 25-40

- 41-55

- 55+

- By Income Level:

- Low-Income

- Middle-Income

- High-Income

- By Region:

- Central

- Eastern

- Western

- Northern

- Southern

- By Financial Institutions:

- Banks

- NBFCs

- Fintech

Players Mentioned in the Report:

- National Commercial Bank (NCB)

- Al Rajhi Bank

- Saudi British Bank (SABB)

- Riyad Bank

- Arab National Bank (ANB)

- Alinma Bank

- Saudi Investment Bank (SAIB)

- Bank Albilad

- Bank Aljazira

- Saudi Home Loans (SHL)

- Saudi Finance Company (SFC)

- Emkan Finance

- Al Yusr Leasing and Financing

- Abdul Latif Jameel Finance

- Tamweel Aloula

- Tamara

- Lendo

- Sarwa

- Hala (HalaFintech)

- Mada Pay

- PayTabs

Key Target Audience:

- Commercial Banks

- Islamic Banks

- Fintech Companies

- Microfinance Institutions

- Non-Banking Financial Institutions (NBFIs)

- Regulatory Bodies (e.g., SAMA - Saudi Arabian Monetary Authority)

- Research and Development Institutions

Time Period:

- Historical Period: 2018-2023

- Base Year: 2024

- Forecast Period: 2024-2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-Role of Entities, Stakeholders, and challenges they face

4.2. Revenue Streams for KSA Personal Finance Market

4.3. Business Model Canvas for KSA Personal Finance Market

5.1. Lending Market by Product Segments in KSA, 2018-2024

5.2. Ratio of Bank vs. Non-Bank Personal Lending in KSA, 2018-2024

5.4. Number of Financial Institutions in KSA with Number of Branches

8.1. Credit Disbursed, 2018-2024

8.2. Loan Outstanding, 2018-2024

9.1. By Financial Institution Type (Commercial Banks, Islamic Banks, Fintech, Microfinance Institutions), 2023-2024P

9.2. By Organized and Unorganized Forms of Personal Finance, 2018-2024

9.3. By Purpose ( Wedding Loans, Home Renovation Loans, Travel Loan, Medical loans, Debt Consolidation Loan and Others), 2018-2024

9.4. By Loan Tenure, 2018-2024

9.5. 9.4. By Region, 2023-2024P

10.1. Customer Landscape and Cohort Analysis

10.2. Customer Journey and Decision Making

10.3. Need, Desire, and Pain Point Analysis

10.4. Gap Analysis Framework

10.5. By Saudi And Non Saudi Consumers, 2023

10.6. By Type of Employment, 2023

10.7. By Age, 2023

11.1. Trends and Developments for KSA Personal Finance Market

11.2. Growth Drivers for KSA Personal Finance Market

11.3. SWOT Analysis for KSA Personal Finance Market

11.4. Issues and Challenges for KSA Personal Finance Market

11.5. Government Regulations for KSA Personal Finance Market

12.1. Market Size and Future Potential for Digital Personal Finance Market on the Basis of Credit Disbursed, 2023-2029

12.2. Business Model and Revenue Streams for Key Players Operating in Digital Personal Finance Market

12.3. Cross Comparison of Leading Digital Finance Companies including Company Overview, Funding, Management, Business Model, Tie-ups, Product offerings and Interest Rate, Success Rate of Application, Number of Users and other details

15.1. Market Share of Key Players in KSA Personal Finance Market on the Basis of Credit Disbursed, 2023

15.2. Cross Comparison of Key Players in KSA Personal Finance Market-Comparative Analysis Basis Operational and Financial Parameters\

15.3. Strength and Weakness

15.4. Operating Model Analysis Framework

15.5. Gartner Magic Quadrant

15.6. Bowmans Strategic Clock for Competitive Advantage

16.1. Credit Disbursed, 2025-2029

16.2. Loan Outstanding, 2025-2029

17.1. By Financial Institution (Commercial Banks, Islamic Banks, Fintech, Microfinance Institutions), 2023-2024P

17.2. By Organized and Unorganized Forms of Personal Finance, 2018-2024

17.3. By Purpose (Wedding Loans, Home Renovation Loans, Travel Loan, Medical loans, Debt Consolidation Loan and Others), 2018-2024

17.4. By Loan Tenure, 2018-2024

17.5. By Region, 2023-2024P

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Ecosystem Mapping: Identify all the demand-side and supply-side entities within the KSA Lending Market. This includes financial institutions, fintech companies, government agencies, and end consumers. Based on this ecosystem, we will shortlist the leading 5-6 financial institutions in the country based on their financial performance, lending portfolio, and market reach.

Data Sourcing: We gather data from industry articles, multiple secondary sources, and proprietary databases to perform comprehensive desk research on the lending market. This helps collate industry-level information such as loan disbursement volumes, interest rates, and institutional market shares.

Step 2: Desk Research

Exhaustive Research Process: Through an exhaustive desk research process, we reference a range of secondary and proprietary databases to analyze market insights. This includes metrics such as loan volumes, market players, pricing trends, and demand forecasts. We supplement this with a detailed review of company-level data sourced from press releases, annual reports, financial statements, and other relevant documents. This stage aims to construct a foundational understanding of the KSA lending market and the major institutions within it.

Step 3: Primary Research

In-Depth Interviews: We conduct in-depth interviews with C-level executives and key stakeholders from various KSA lending institutions and end-users. These interviews serve to validate hypotheses, authenticate market statistics, and obtain valuable operational and financial insights. A bottom-to-top approach is employed to evaluate the lending volumes for each player, which are then aggregated to determine overall market size.

Disguised Interviews: We implement disguised interviews by approaching companies as potential customers to cross-verify operational and financial data. This helps ensure the accuracy of data shared by company executives and supplements information sourced from secondary databases. These interactions provide comprehensive insights into revenue streams, lending processes, pricing, and value chains.

Step 4: Sanity Check

- Sanity Checks: A combination of bottom-up and top-down analysis is conducted, along with market size modeling exercises, to ensure the validity and reliability of the research findings.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The KSA personal finance market is expected to witness robust growth, reaching a valuation of SAR 5.0 billion by 2029. Key factors driving this growth include the increasing demand for consumer financing solutions, the rise of digital personal finance platforms, and the growing preference for Shariah-compliant financial products.

Prominent players in the KSA personal finance market include Al Rajhi Bank, Riyad Bank, National Commercial Bank (NCB), and SABB. These institutions lead the market due to their extensive product offerings, strong digital platforms, and focus on customer experience.

The primary growth drivers for the KSA personal finance market include increasing consumer demand for flexible and personalized financial products, the shift towards digital financial services, and the growing middle class in Saudi Arabia.

Challenges in the KSA personal finance market include stringent regulatory requirements, particularly for Islamic financing products, and concerns around data privacy and security.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0