KSA Toys and Games Market Outlook to 2029

By Branded and Local Players, By Product Type (Educational Toys, Electronic Toys, Action Figures, Dolls, Games and Puzzles, Ride-Ons), By Age Group, By Distribution Channel, and By Region

Report Overview

Report Code

TDR0067

Coverage

Middle East

Published

November 2024

Pages

80-100

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “KSA Toys and Games Market Outlook to 2029 - By Branded and Local Players, By Product Type (Educational Toys, Electronic Toys, Action Figures, Dolls, Games and Puzzles, Ride-Ons), By Age Group, By Distribution Channel, and By Region” provides a comprehensive analysis of the toys and games market in the Kingdom of Saudi Arabia (KSA).

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “KSA Toys and Games Market Outlook to 2029 - By Branded and Local Players, By Product Type (Educational Toys, Electronic Toys, Action Figures, Dolls, Games and Puzzles, Ride-Ons), By Age Group, By Distribution Channel, and By Region” provides a comprehensive analysis of the toys and games market in the Kingdom of Saudi Arabia (KSA). The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the Toys and Games Market. The report concludes with future market projections based on sales revenue, by market structure, product types, region, cause and effect relationship, and success case studies highlighting the major opportunities and cautions.

KSA Toys and Games Market Overview and Size

The KSA toys and games market reached a valuation of SAR 4.5 billion in 2023, driven by factors such as a growing youth population, rising disposable income, and increasing consumer awareness of educational and developmental toys. The market is characterized by the presence of both domestic and international players, including Al-Othaim, Jarir Bookstore, Al Mutlaq Group, and global brands such as Lego, Hasbro, and Mattel. These companies are recognized for their diverse product offerings, innovative marketing strategies, and strong distribution networks.

In 2023, Lego opened a flagship store in Riyadh, introducing its latest interactive play concepts. This move is aimed at enhancing customer experience and capitalizing on the growing preference for branded and high-quality toys. Major cities such as Riyadh, Jeddah, and Dammam serve as key markets due to their high population density and well-developed retail infrastructure.

Market Size for KSA Toys and Games Market on the Basis of Revenue in INR Crores, 2018-2024

Source: TraceData Research Analysis.

What Factors are Leading to the Growth of KSA Toys and Games Market:

Growing Young Population: The increasing youth population in Saudi Arabia, which constitutes over 30% of the total population, is a key driver for the toys and games market. The demand for toys and educational games is on the rise as parents prioritize developmental and interactive products for their children. This trend is especially pronounced in urban areas like Riyadh and Jeddah, where families have higher purchasing power.

Rising Disposable Income: With economic diversification and increasing employment opportunities, disposable income in KSA has seen a steady rise. Higher disposable income has led to increased spending on non-essential items, including toys and games, making the market highly lucrative for both local and international brands. In 2023, premium and branded toys accounted for 45% of the total market share.

Government Initiatives and Reforms: Saudi Arabia’s Vision 2030, which emphasizes social development and family entertainment, has positively impacted the toys and games industry. The government's focus on creating family-friendly entertainment hubs, coupled with reduced import duties on select children’s products, has spurred market growth. As a result, the market witnessed a growth rate of 8.5% in 2023 compared to the previous year.

Which Industry Challenges Have Impacted the Growth of the KSA Toys and Games Market:

High Dependence on Imports: The KSA toys and games market relies heavily on imports, making it vulnerable to fluctuations in international trade policies, shipping delays, and currency exchange rates. In 2023, approximately 75% of toys sold in KSA were imported, leading to increased costs and price volatility. This dependence on foreign markets has also resulted in longer lead times and limited availability of certain products.

Cultural and Religious Sensitivities: The Saudi market is highly sensitive to cultural and religious norms, which restricts the types of toys and games that can be sold. Certain toys that do not align with cultural values face outright bans or limited distribution. This creates a challenge for international companies looking to enter the market and requires them to adapt their product offerings to comply with local regulations.

Intense Market Competition: The KSA toys and games market is characterized by intense competition from both global and regional players. Established global brands such as Lego and Hasbro dominate the market with their high-quality offerings, making it challenging for smaller local brands to gain market share. In 2023, global brands accounted for approximately 60% of the market, leaving limited room for new entrants.

What are the Regulations and Initiatives which have Governed the KSA Toys and Games Market:

Product Safety Standards: The Saudi Standards, Metrology and Quality Organization (SASO) mandates stringent safety standards for all toys and games sold in the country. These standards include regulations on materials used, product labeling, and safety warnings to ensure the well-being of children. In 2023, SASO updated its toy safety guidelines to align with international best practices, which resulted in the recall of approximately 5% of non-compliant products from the market.

Import Regulations and Tariffs: The Saudi government imposes specific import tariffs and customs duties on toys and games, depending on the product category. The 2022 introduction of a reduced tariff for educational and developmental toys aimed to make these products more accessible to the general population. This initiative has encouraged the import of educational toys, which saw a 15% increase in imports compared to the previous year.

Localization Initiatives (Nitaqat Program): To promote local content and reduce dependency on imports, the government has implemented localization initiatives, encouraging companies to establish manufacturing units within the country. Under the Nitaqat program, companies that meet certain Saudization targets are provided with benefits such as tax breaks and easier access to government contracts. As of 2023, around 10% of toys sold in the country are locally manufactured, a figure expected to rise with continued government support.

KSA Toys and Games Market Segmentation

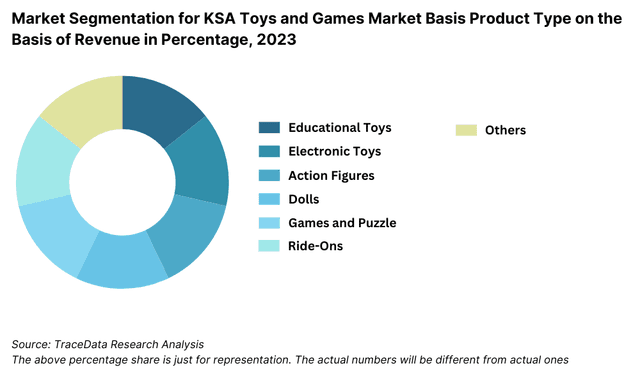

By Product Type: The toys and games market in KSA is segmented into educational toys, outdoor and sports toys, electronic toys, dolls and action figures, and board games. Educational toys are witnessing rapid growth due to increased awareness among parents regarding early childhood development. In 2023, educational toys contributed to approximately 35% of the total market revenue, followed by outdoor and sports toys, which held a 25% share due to the rising popularity of physical activities among children.

By Age Group: The market is divided into different age groups: 0-3 years, 4-8 years, 9-12 years, and 13+ years. Toys targeting the 4-8 years age group hold the largest market share due to the increasing demand for interactive and educational products. In 2023, this age group accounted for 40% of total sales, reflecting parents' focus on developmental toys. Toys for children aged 9-12 years are also gaining traction with a 30% share, driven by the popularity of science and robotics kits.

By Sales Channel: The market is segmented into brick-and-mortar stores, online stores, and specialty toy stores. Brick-and-mortar stores dominate the sales channel segmentation, accounting for 55% of total sales in 2023 due to the preference for in-person product inspection and immediate purchase. Online stores have seen significant growth, contributing to 30% of total sales in 2023, driven by the increasing adoption of e-commerce and convenience in delivery services.

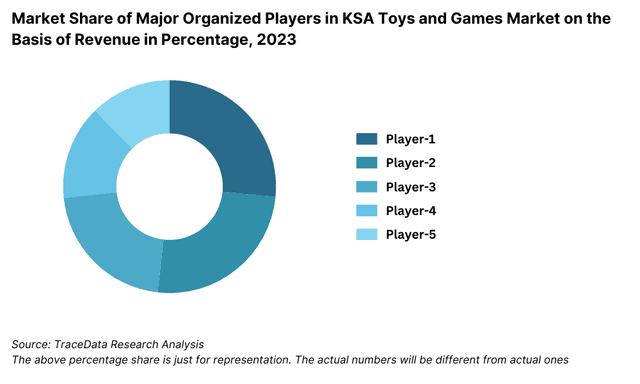

Competitive Landscape in KSA Toys and Games Market

The KSA toys and games market is moderately fragmented, with a mix of international and local players dominating the space. Major global brands such as Lego, Hasbro, and Mattel hold a significant share, while regional retailers like Al-Othaim and Jarir Bookstore contribute substantially to the market. The entry of new companies and the rise of e-commerce platforms have diversified the market, providing consumers with a wider range of products and services.

| Company Name | Establishment Year | Headquarters |

|---|---|---|

| Mattel, Inc. | 1945 | El Segundo, California, USA |

| Hasbro, Inc. | 1923 | Pawtucket, Rhode Island, USA |

| LEGO Group | 1932 | Billund, Denmark |

| Spin Master Corp. | 1994 | Toronto, Canada |

| MGA Entertainment | 1979 | Chatsworth, California, USA |

| Bin Salman Fty For Plastic & Toys | 1998 | Riyadh, Saudi Arabia |

| SAMACO Toys and Leisure | 1975 | Jeddah, Saudi Arabia |

| Toy Triangle | 1999 | Riyadh, Saudi Arabia |

| Clementoni | 1963 | Recanati, Italy |

Ravensburger Group | 1883 | Ravensburg, Germany |

Some of the recent competitor trends and key information about competitors include:

Al-Othaim: As one of the leading local retailers, Al-Othaim recorded a 12% increase in toy sales in 2023, driven by its strategic location in malls and shopping centers. The company’s focus on offering a diverse range of toys and games at competitive prices has helped it maintain a strong market presence.

Jarir Bookstore: Known for its comprehensive selection of educational and developmental toys, Jarir Bookstore saw a 15% growth in toy sales in 2023. The company’s strong emphasis on e-commerce and online promotions has contributed to increased sales in both urban and rural regions of Saudi Arabia.

Lego Group: The Lego Group experienced a 20% increase in sales in 2023, following the launch of a flagship store in Riyadh. The company's innovative product lines and interactive in-store experiences have made it a popular choice among Saudi families.

Hasbro: Hasbro reported a 10% growth in sales in 2023, largely attributed to the success of its digital initiatives and interactive toy offerings. The company's strategic partnerships with local retailers have expanded its reach within the KSA market.

Mattel: Mattel saw an 8% rise in toy sales in 2023, driven by the popularity of its Barbie and Hot Wheels product lines. The company’s collaboration with local distributors and targeted marketing campaigns have enhanced its brand visibility and customer engagement.

What Lies Ahead for KSA Toys and Games Market?

The KSA toys and games market is expected to grow significantly by 2029, exhibiting a steady CAGR during the forecast period. This growth will be driven by factors such as increased consumer spending, rising awareness of developmental and educational toys, and expanding distribution channels.

Increased Demand for Educational and STEM Toys: As Saudi parents continue to place emphasis on educational outcomes and cognitive development, there is expected to be a growing demand for STEM (Science, Technology, Engineering, and Mathematics) toys. These toys, which foster problem-solving and critical thinking skills, are anticipated to account for 25% of the total market by 2029. The trend is further supported by the Ministry of Education's efforts to promote STEM learning in schools.

Expansion of E-Commerce Channels: With the increasing penetration of internet services and the rising popularity of online shopping, e-commerce is projected to become a major sales channel for toys and games. In 2023, online toy sales contributed 30% of the total market revenue, and this share is expected to grow to 45% by 2029. The convenience of home delivery, availability of a wider range of products, and competitive pricing are key factors driving this shift towards digital platforms.

Rise in Licensing and Character-Based Toys: The growing influence of Western media and entertainment in KSA is expected to drive demand for licensed character toys based on popular movies, TV shows, and comic books. In 2023, licensed toys accounted for 20% of the market share, and this segment is projected to expand further as international franchises continue to gain popularity in the region.

Adoption of Sustainable and Eco-Friendly Toys: With increasing awareness about environmental sustainability, there is a rising trend towards eco-friendly and sustainably manufactured toys. Companies are focusing on using recyclable materials and reducing plastic usage in their products. By 2029, eco-friendly toys are expected to represent 10% of the total market, driven by growing consumer preference for environmentally conscious brands.

Future Outlook and Projections for KSA Toys and Games Market on the Basis of Revenue in USD Billion, 2024-2029

KSA Toys and Games Market Segmentation

- By Market Structure:

Organized Sector

Unorganized Sector

- By Product Type:

- Educational Toys

- Outdoor and Sports Toys

- Electronic Toys

- Dolls and Action Figures

- Puzzles and Board Games

- By Age Group:

- 0-3 Years

- 4-8 Years

- 9-12 Years

- 13+ Years

- By Sales Channel:

- Brick-and-Mortar Stores

- E-Commerce Platforms

- Specialty Stores

- By Region:

- Central Region (Riyadh)

- Western Region (Jeddah, Makkah)

- Eastern Region (Dammam, Khobar)

- Northern Region

- Southern Region

Players Mentioned in the Report:

- LEGO System A/S

- Toys Brand Trading Company

- Samaco Toys & Leisure

- Toy Triangle

- Toys R Us

- Simba Toys

- Toy Town

- Clementoni

- Melissa & Doug

- Wasit Saudi Corp.

- Guangdong Family of Childhood Industrial Co., Ltd

Key Target Audience:

- Toy Manufacturers and Distributors

- Online Marketplaces

- Educational and Developmental Institutions

- Regulatory Bodies (e.g., SASO, Ministry of Commerce)

- Research and Development Institutions

Time Period:

- Historical Period: 2018-2023

- Base Year: 2024

- Forecast Period: 2024-2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

3.1. Manufacturers and Suppliers

3.2. Distribution Channels

3.3. Retailers and E-commerce Platforms

3.4. Consumer Groups

4.1. Value Chain Process-Entity relationships, Margin Analysis, Distributor, Dealers, Traders and Retailers

4.2. Business Model Canvas for the KSA Toys and Games Market

5.1. Population by Age Group

5.2. Estimated Time Spent by Age Group on Toys and Recreational Activities

8.1. Revenues, 2018-2024

8.2. Sales Volume, 2018-2024

9.1. By Market Structure (Organized and Unorganized Market), 2023-2024P

9.2. By Product Type (Educational Toys, Electronic Toys, Action Figures, Dolls, Games and Puzzles, Action Figures, Ride-Ons and others), 2023-2024P

9.3. By Age Group (0-2 years, 3-5 years, 6-8 years, 9-14 years), 2023-2024P

9.4. By Distribution Channel (Specialty Stores, Hypermarkets/ Supermarkets, Online Channels), 2023-2024P

9.5. By Region (North, South, West, East, Central), 2023-2024P

9.6. By Price Range, 2023-2024P

9.7. By Type of Play (Active Play, Creative Play, Learning Play, Technology-Based Play), 2023-2024P

10.1. Customer Segmentation and Profile

10.2. Customer Journey and Buying Decision Process

10.3. Key Motivations and Pain Points

10.4. Product Preferences and Buying Trends

11.1. Trends and Developments in KSA Toys and Games Market

11.2. Growth Drivers for KSA Toys and Games Market

11.3. SWOT Analysis for KSA Toys and Games Market

11.4. Issues and Challenges for KSA Toys and Games Market

11.5. Government Regulations for KSA Toys and Games Market

12.1. Market Size and Future Potential for Online Toys and Games Market, 2018-2029

12.2. Business Model and Revenue Streams

12.3. Cross Comparison of Leading Online Toy Platforms Basis Operational and Financial Parameters

15.1. Market Share of Key Organized Brands in KSA Toys and Games Market, FY2024

15.2. Market Share of Key Distributors in KSA Toys and Games Market, FY2024

15.3. Benchmark of Key Competitors in KSA Toys and Games Market Including Operational and Financial Parameters

15.4. Strength and Weakness Analysis

15.5. Operating Model Analysis Framework

15.6. Porters Five Forces Analysis for Competitor Strategy

15.7. Gartner Magic Quadrant

15.8. Bowmans Strategic Clock for Competitive Advantage

16.1. Revenues, 2025-2029

16.2. Sales Volume, 2025-2029

17.1. By Market Structure (Organized and Unorganized Market), 2025-2029

17.2. By Product Type (Educational Toys, Electronic Toys, Action Figures, Dolls, Games and Puzzles, Ride-Ons), 2025-2029

17.3. By Age Group (0-2 years, 3-5 years, 6-8 years, 9-14 years), 2025-2029

17.4. By Distribution Channel (Specialty Stores, Hypermarkets/Supermarkets, Online Channels), 2025-2029

17.5. By Region (North, South, West, East, Central), 2025-2029

17.6. By Price Range, 2025-2029

17.7. By Type of Play (Active Play, Creative Play, Learning Play, Technology-Based Play), 2025-2029

17.8. Recommendation and Strategic Insights

17.9. Opportunity Analysis for KSA Toys and Games Market

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand side and supply side entities for KSA Toys and Games Market. Basis this ecosystem, we will shortlist leading 5-6 players in the market based upon their financial information, product offerings, and distribution networks.

Sourcing is made through industry articles, multiple secondary, and proprietary databases to perform desk research around the market to collate industry-level information.

Step 2: Desk Research

Subsequently, we engage in an exhaustive desk research process by referencing diverse secondary and proprietary databases. This approach enables us to conduct a thorough analysis of the market, aggregating industry-level insights. We delve into aspects like the revenue contributions by product type, key players, consumer preferences, and regulatory landscape. We supplement this with detailed examinations of company-level data, relying on sources like press releases, annual reports, financial statements, and similar documents. This process aims to construct a foundational understanding of both the market and the entities operating within it.

Step 3: Primary Research

We initiate a series of in-depth interviews with C-level executives and other stakeholders representing various KSA Toys and Games Market companies and end-users. This interview process serves a multi-faceted purpose: to validate market hypotheses, authenticate statistical data, and extract valuable operational and financial insights from these industry representatives. Bottom-to-top approach is undertaken to evaluate volume sales for each player, thereby aggregating to the overall market.

As part of our validation strategy, our team executes disguised interviews wherein we approach each company under the guise of potential business partners or customers. This approach enables us to validate the operational and financial information shared by company executives, corroborating this data against what is available in secondary databases. These interactions also provide us with a comprehensive understanding of revenue streams, value chain, product pricing, and other factors.

Step 4: Sanity Check

- Bottom-to-top and top-to-bottom analysis along with market size modeling exercises is undertaken to assess the sanity check process.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The KSA toys and games market is expected to witness significant growth, reaching a valuation of SAR 6.2 billion by 2029. This growth is fueled by factors such as a young and expanding population, increased consumer spending on non-essential items, and rising awareness of educational and developmental toys. Additionally, the growing e-commerce sector and increasing number of international brands entering the market are enhancing accessibility and driving market potential.

The KSA Toys and Games Market features several key players, including Al-Othaim, Jarir Bookstore, and Panda Retail. These companies dominate the market due to their extensive distribution networks, strong brand presence, and diverse product offerings. International brands such as Lego, Hasbro, and Mattel are also prominent players, leveraging their global brand equity and innovative product lines to capture market share.

The primary growth drivers include demographic factors such as a growing youth population and increasing urbanization, which are driving demand for toys and games. Additionally, rising disposable incomes and increased spending on children's entertainment are boosting market growth. The market is also benefiting from the expanding digital landscape, which has made it easier for consumers to access a wider range of products and brands.

The KSA Toys and Games Market faces several challenges, including cultural and religious sensitivities that limit the types of toys that can be sold. High dependence on imports makes the market vulnerable to fluctuations in international trade policies and shipping delays. Furthermore, competition from established global brands presents a significant challenge for local companies trying to capture market share.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0