Kuwait Warehousing Market Outlook to 2030

By Market Structure, By Facility Grade, By Warehouse Type, By Service Offering, By End-User Vertical, and By Hub/Region

Report Overview

Report Code

TDR0345

Coverage

Middle East

Published

October 2025

Pages

80

On This Page

Report Overview

The report titled “Kuwait Warehousing Market Outlook to 2030 – By Market Structure, By Facility Grade, By Warehouse Type, By Service Offering, By End-User Vertical, and By Hub/Region” provides a comprehensive analysis of the warehousing industry in Kuwait. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the warehousing market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Kuwait Warehousing Market Outlook to 2030 – By Market Structure, By Facility Grade, By Warehouse Type, By Service Offering, By End-User Vertical, and By Hub/Region” provides a comprehensive analysis of the warehousing industry in Kuwait. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the warehousing market. The report concludes with future market projections based on pallet capacity, facility grades, warehouse types, service offerings, regions, cause-and-effect relationships, and success case studies highlighting the major opportunities and cautions.

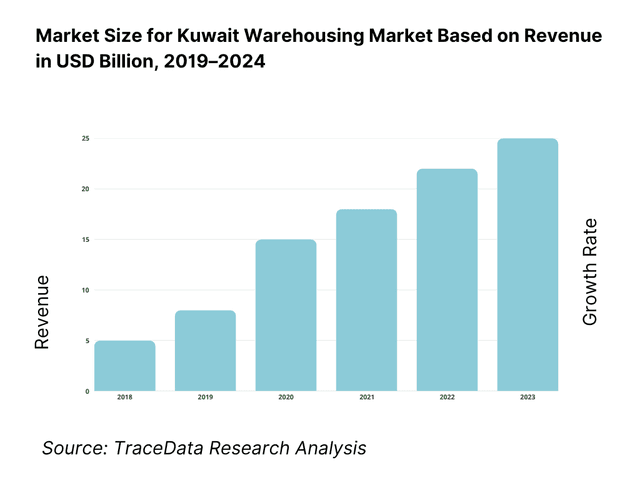

Kuwait Warehousing Market Overview and Size

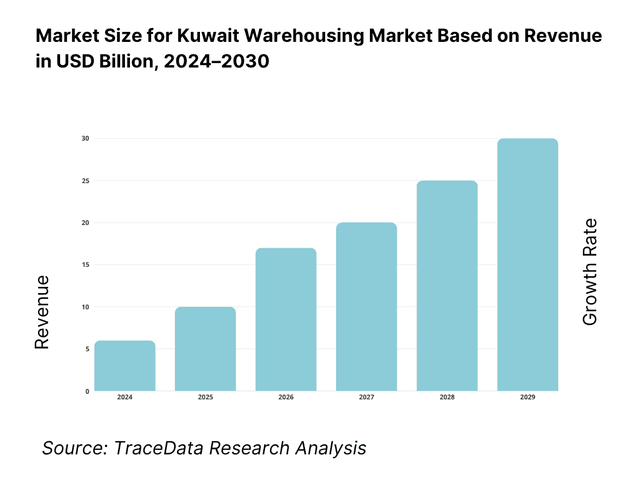

The Kuwait warehousing and logistics market is valued at USD 3.4 billion, based on published market sizing for the country’s logistics & warehousing sector and a five-year historical analysis of the market’s expansion driven by import-centric consumption, free-zone activity around Shuwaikh and Shuaiba ports, and cold-chain build-out for pharma and food. Current operating fundamentals are reinforced by 2024 hard-numbers at gateways (e.g., Shuaiba handled 282,870 TEU and holds 318,000 m² of container-terminal storage), underscoring throughput that sustains storage demand.

Warehousing demand concentrates around Shuwaikh (Kuwait’s main commercial port with 21 berths and 600,000 m² of storage area) and Shuaiba (industrial port with 20 berths) due to immediate port-gate proximity, bonded-handling availability, and direct arterial links to retail and industrial zones in Ardiya, Sulaibiya, and Mina Abdullah. Pipeline capacity in 2024 is further supported by Kuwait’s planned logistics cities—317,355 m² at Shuwaikh, ~300,000 m² at Doha, and 1,000,000 m² at Mina Abdullah—anchoring future clustering and lowering drayage times for shippers.

What Factors are Leading to the Growth of the Kuwait Warehousing Market:

Import-led demand and diversified trade baskets feed continuous storage and cross-dock needs: Kuwait’s warehousing demand is underpinned by sizeable merchandise inflows and diversified supply lines that must be staged at port-adjacent and city-proximate nodes. World Bank/WITS reports merchandise imports of US$ 32,356,000,000, with 145 import partners and 4,078 HS-6 products—driving SKU complexity and pallet intensity. The main commercial gateway, Shuwaikh Port, provides 21 berths and 600,000 m² of storage inside a 4.4 million m² estate, enabling rapid de-vanning and bonded handling. These hard trade and infrastructure numbers translate directly into high turns at ambient facilities, growing cold-chain staging for food/pharma, and strong utilization of bonded/CFS capacity.

Hyper-urban, dense consumption core and rising air-cargo reinforce near-city fulfilment: Kuwait’s entire population is urban, with 100.0 percent of residents living in cities; the country’s total population is 4,973,861. Such density compresses lead times and favors micro-fulfillment and CEP cross-docking within the Kuwait City–Ardiya–Sulaibiya belt. Air cargo further amplifies time-sensitive warehousing: Kuwait International Airport handled 210 million kg of freight (inbound: 170 million kg; outbound: 40 million kg), while the passenger terminal processed 15,616,800 travelers—expanding belly-hold lift and express flows. Together, these figures sustain high-frequency e-commerce cycles, returns processing, and temp-controlled pharma handling close to consumers.

Gateways with industrial-grade capacity anchor contract logistics and cold-chain scaling: Shuwaikh’s 21 berths and 600,000 m² storage interface with bonded flows into the city, while Kuwait’s economy in current prices sits around US$ 161,822,397,549, supporting consistent import purchasing power across FMCG, healthcare, and industrial categories. The urban base of 4,973,861 residents with 100.0 percent urbanization requires short drayage to retail and hospital networks, pushing demand for Grade-A ambient and multi-temperature nodes. With merchandise imports at US$ 32,356,000,000 and air freight at 210 million kg, operators are incentivized to expand pallet positions, reefer plugs, and GDP-compliant rooms to secure contracts in FMCG and pharma.

Which Industry Challenges Have Impacted the Growth of the Kuwait Warehousing Market:

Land-banking, zoning and proximity constraints around prime hubs: Grade-A warehousing must cluster near Shuwaikh’s 21 berths and 600,000 m² storage to minimize drayage, but industrial land inside a 4.4 million m² port estate is finite and tightly controlled, creating competition for plots and lengthening build-to-suit timelines. Kuwait’s fully urban population of 4,973,861 at 100.0 percent urbanization concentrates demand within a small national land area of 17,820 km², raising opportunity costs for alternate uses. These structural facts cap near-port plot availability, pushing some users to accept older stock or longer over-the-road hauls that inflate handling cycles and reduce service quality.

Customs process complexity and compliance overhead for bonded flows: Kuwait applies the WTO Customs Valuation Agreement with transaction-value rules and established valuation methods, while operating under the GCC Common Customs Law framework. Operators must also maintain valid licensing under the General Administration of Customs—evidenced by the government’s customs license renewal and temporary entry processes. These codified requirements add documentation and broker coordination steps to time-sensitive warehousing (e.g., pharma), especially when synchronized with airport cargo volumes of 210 million kg that funnel into bonded nodes for rapid distribution.

Energy-intensive cold-chain and operational resilience: Cold-chain rooms and reefer yards are power-hungry, and Kuwait’s electricity system remains fossil-reliant, which heightens OPEX planning for multi-temperature warehouses. The IMF pegs Kuwait’s economy in current prices near US$ 161,822,397,549, while energy statistics show limited renewable penetration in recent years (official power sector pages: MEW; energy profiles: EIA Kuwait overview). With a fully urban population of 4,973,861 and port storage of 600,000 m² in the core gateway, maintaining temperature compliance under peak loads requires backup generation, insulated envelopes, and validated monitoring—raising capital discipline and operational redundancy thresholds across facilities.

What are the Regulations and Initiatives which have Governed the Market:

GCC Common Customs Law defines bonded regimes and FTZ treatment: Kuwait adheres to the GCC Common Customs Law, which sets definitions for free zones and duty-free shops and codifies procedures for customs declarations and goods status in designated zones. For warehouse operators, this governs how imported cargo is moved, stored, and cleared inside bonded facilities before domestic release or re-export, directly shaping layout (bonded vs non-bonded bays), documentation flows, and SLA design with shippers and brokers. These provisions interface with Kuwait’s urban logistics fabric of 4,973,861 residents served by the Shuwaikh gateway’s 21 berths.

Kuwait Customs licensing & procedures operationalize cargo movements: Warehouse and logistics providers require valid customs permissions and must transact within official e-services. The State portal lists customs license renewal and temporary customs entry, while the U.S. government’s country guide confirms Kuwait’s implementation of the WTO customs valuation rules. In practice, these norms govern valuation, inspection, and release timing for flows that ultimately feed city-adjacent warehouses serving an entirely urban base (100.0 percent) and process air cargo volumes of 210 million kg through KWI.

Industrial zoning and investment facilitation under PAI and national law: The Public Authority for Industry (PAI)—established under Industry Law No. 6—facilitates industrial transactions and allocates industrial opportunities, shaping where and how warehouses can be developed within industrial estates. This zoning role interacts with port estates such as Shuwaikh’s 4.4 million m² footprint and the city’s fully urban population of 4,973,861 to determine feasible build-to-suit plots, utilities access and compliance pathways. Complementary investment regimes administered nationally (e.g., under KDIPA) align with an economy recorded at US$ 161,822,397,549 in current prices, supporting industrial property deployment where demand density is highest.

Kuwait Warehousing Market Segmentation

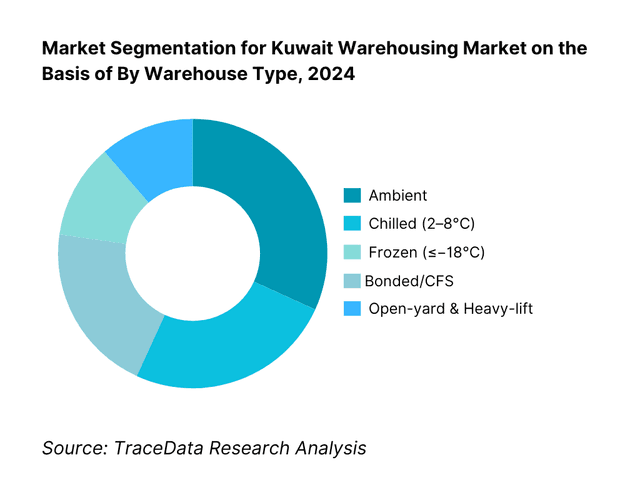

By Warehouse Type: Kuwait Warehousing Market is segmented by warehouse type into ambient, chilled, frozen, bonded/CFS, and open-yard & heavy-lift. Recently, ambient facilities have a dominant market share in Kuwait under this segmentation, owing to import-led FMCG and general merchandise flows channelled through Shuwaikh/Shuaiba and staged in Ardiya/Sulaibiya parks. Retail replenishment cycles, high SKU variety, and rapid cross-dock demand from CEP/e-commerce operators keep ambient capacity tight. Cold-chain is rising fast—supported by pharma freight (biopharma 3PL at USD 715 million) and food imports—but ambient still prevails due to broader addressable demand and lower capex per pallet.

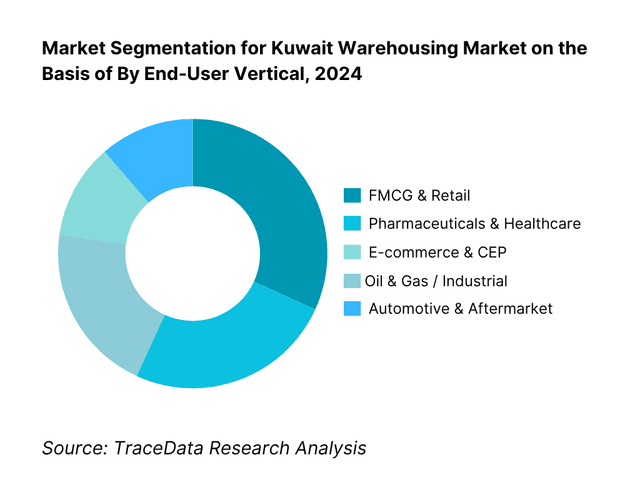

By End-User Vertical: Kuwait Warehousing Market is segmented by end-user vertical into FMCG & retail, pharmaceuticals & healthcare, e-commerce & CEP, oil & gas/industrial, and automotive & aftermarket. Recently, FMCG & retail has a dominant market share under this segmentation, driven by import-heavy consumer baskets, dense store networks in Kuwait City & Al Farwaniya, and sustained replenishment cycles that prioritize ambient DC space near port-gates. Pharma is structurally strong, underpinned by cold-chain compliance and biologics flow; e-commerce & CEP continues to build micro-fulfillment nodes, but absolute pallet positions remain weighted to FMCG due to SKU breadth and steady throughput.

Competitive Landscape in Kuwait Warehousing Market

The Kuwait warehousing market is consolidated around port-adjacent developers and integrated 3PLs, with Grade-A space led by developer-operators and multi-temperature capacity expanding in response to pharma and food flows. Competitive intensity is reinforced by global CEP/3PL networks (DHL, Kuehne+Nagel, Schenker, CEVA) alongside regional leaders (Agility Logistics Parks, GAC, KGL), while tech adoption (WMS/TMS, IoT temperature logging) differentiates service quality. Clustering near Shuwaikh/Shuaiba and along the Sulaibiya–Mina Abdullah axis concentrates supply, shortens drayage, and enables value-added services at scale

Name | Founding Year | Original Headquarters |

Agility Logistics Parks (ALP) | 1979 | Kuwait City, Kuwait |

GAC Kuwait | 1956 | Dubai, UAE |

KGL Logistics | 2000 | Kuwait City, Kuwait |

DSV (Kuwait operations) | 1976 | Hedehusene, Denmark |

Kuehne+Nagel (Kuwait operations) | 1890 | Schindellegi, Switzerland |

DB Schenker (Kuwait operations) | 1872 | Essen, Germany |

CEVA Logistics (Kuwait operations) | 2006 | Marseille, France |

DHL Supply Chain (Kuwait) | 1969 | Bonn, Germany |

UPS (Kuwait) | 1907 | Atlanta, USA |

FedEx (Kuwait) | 1971 | Memphis, USA |

Aramex Kuwait | 1982 | Dubai, UAE |

PostaPlus | 2005 | Kuwait City, Kuwait |

Hellmann Worldwide Logistics (Kuwait) | 1871 | Osnabrück, Germany |

Kuwait Transcontinental Shipping | 1977 | Kuwait City, Kuwait |

TTL Logistics | 1995 | Kuwait City, Kuwait |

Some of the Recent Competitor Trends and Key Information About Competitors Include:

Agility Logistics Parks (ALP): As the largest industrial real estate developer in Kuwait, Agility Logistics Parks expanded its Mina Abdullah facilities in 2024, adding new Grade-A warehouses with multi-temperature capabilities to meet rising demand from FMCG and pharmaceutical clients.

GAC Kuwait: GAC strengthened its value-added services portfolio in 2024, integrating bonded clearance and e-commerce fulfillment solutions to cater to Kuwait’s growing online retail sector and regional re-export flows.

KGL Logistics: Known for its strong presence in port logistics, KGL Logistics launched an upgrade of its Shuwaikh facilities in 2024, focusing on automating warehouse management systems to reduce dwell time and improve throughput efficiency.

DHL Supply Chain (Kuwait): DHL expanded its cold-chain warehousing capacity in 2024, aligning with Kuwait’s rising demand for pharmaceutical and fresh food logistics, and introduced real-time temperature monitoring for enhanced compliance with global GDP standards.

Aramex Kuwait: Aramex reinforced its last-mile logistics integration in 2024 by expanding its Ardiya hub and linking it with new micro-fulfillment centers, strengthening its positioning in Kuwait’s rapidly growing e-commerce sector.

What Lies Ahead for Kuwait Warehousing Market?

The Kuwait warehousing market is expected to expand steadily through the next planning horizon, supported by the country’s fully urban population of 4.97 million residents, merchandise imports valued at USD 32.3 billion, and the development of over 1.6 million m² of planned logistics city space across Shuwaikh, Doha, and Mina Abdullah. Growth momentum will be driven by expanding cold-chain capacity, diversification of import baskets, and regional transit trade via the GCC.

Rise of Grade-A and Multi-Temperature Facilities: The future of warehousing in Kuwait will be shaped by modern Grade-A facilities with higher clear heights, better dock-to-bay ratios, and specialized multi-temperature storage. This reflects the surging demand from pharmaceuticals, fresh food imports, and FMCG distributors.

Focus on Digitalization and Smart Warehousing: With Kuwait International Airport handling over 210 million kg of freight and e-commerce volumes rising, warehouses will increasingly adopt IoT-enabled monitoring, WMS/TMS platforms, and real-time visibility solutions to reduce dwell times and improve inventory accuracy.

Expansion of Sector-Specific Warehousing: Demand will accelerate for sector-focused nodes—ambient hubs for FMCG, GDP-compliant cold rooms for pharma, open-yard storage for oil & gas, and micro-fulfillment centers for e-commerce and CEP players—aligning infrastructure more closely with industry-specific flows.

Integration with Regional Trade and Cross-Docking: The Nuwaiseeb border crossing with Saudi Arabia positions Kuwait as a transit hub for GCC-bound cargo. This will reinforce demand for cross-docking and bonded warehousing solutions, ensuring faster throughput for re-exports while minimizing congestion at urban distribution centers.

Kuwait Warehousing Market Segmentation

By Warehouse Type

Ambient Warehouses

Chilled Warehouses (2–8 °C)

Frozen Warehouses (≤ –18 °C)

Bonded Warehouses / Container Freight Stations (CFS)

Open-Yard & Heavy-Lift Yards

By End-User Vertical (Industry Type)

FMCG & Retail

Pharmaceuticals & Healthcare

E-commerce & Courier/Express Parcel (CEP)

Oil & Gas / Industrial Goods

Automotive & Aftermarket Parts

By Facility Grade / Format

Grade-A Modern Warehouses

Grade-B Legacy Warehouses

Grade-C Older/Mixed-Use Facilities

Build-to-Suit (BTS) Developments

Modular / Micro-Fulfillment Nodes

By Service Offering

Basic Storage

Cross-Docking & Consolidation

Value-Added Services (VAS: kitting, labeling, pick-&-pack, returns)

Customs & Bonded Handling

Last-Mile Staging

By Location / Hub

Shuwaikh (Commercial Port Hub)

Shuaiba (Industrial Port Hub)

Sulaibiya (Logistics Park Cluster)

Ardiya (City-Adjacent Distribution)

Mina Abdullah (Emerging Logistics City)

Doha (New Logistics Node)

Players Mentioned in the Report:

Agility Logistics Parks (ALP)

GAC Kuwait

KGL Logistics

DSV (Kuwait)

Kuehne+Nagel (Kuwait)

DB Schenker (Kuwait)

CEVA Logistics (Kuwait)

DHL (Express/Supply Chain Kuwait)

UPS (Kuwait)

FedEx (Kuwait)

Aramex Kuwait

PostaPlus

Hellmann Worldwide Logistics (Kuwait)

Kuwait Transcontinental Shipping (KTS/TCS)

TTL Logistics

Key Target Audience

Real-estate developers & industrial park operators (Grade-A, BTS, logistics cities)

Third-party logistics (3PL) and contract logistics providers (multi-temperature networks)

Retail & FMCG conglomerates (central DCs, cross-dock, returns)

Pharmaceutical importers & distributors (GDP warehousing; biologics handling)

E-commerce & CEP platforms (fulfilment, last-mile staging)

Oil & gas operators & EPCs (heavy-lift yards; hazardous storage)

Investments and venture capitalist firms (industrial real estate, logistics tech)

Government & regulatory bodies

Time Period:

Historical Period: 2019-2024

Base Year: 2025

Forecast Period: 2025-2030

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Table of Contents

1. Executive Summary

2. Research Methodology

3. Ecosystem of Key Stakeholders in Kuwait Warehousing Market [Port authorities, Free Zone operators, Public Authority for Industry, 3PLs, freight forwarders, cold-chain specialists, real estate developers, utilities providers, e-commerce players]

4. Value Chain Analysis

4.1 Delivery Model Analysis for Warehousing [3PL Contract Logistics, Captive Warehouses, Build-to-Suit, Shared/Multi-Client, On-Dock Facilities]-margins, client preference, strengths & weaknesses

4.2 Revenue Streams for Kuwait Warehousing Market [Storage rental, cross-docking, cold-chain services, VAS (kitting, labeling, returns), customs handling, bonded warehousing]

4.3 Business Model Canvas for Kuwait Warehousing Market [Key partners, key activities, value propositions, customer segments, cost structure, revenue streams]

5. Market Structure

5.1 3PL Contract Logistics vs Captive/Owner-Operated Facilities

5.2 Investment Models in Kuwait Warehousing Market [Land lease, JV/PPP, developer-led, Free Zone-based, captive O&G facilities]

5.3 Comparative Analysis of Allocation and Utilization by Public vs Private Operators [Municipality, KPA, PAI vs Agility, GAC, KGL]

5.4 Warehousing Space Allocation by Facility Grade [Grade-A, Grade-B, Grade-C, BTS facilities]

6. Market Attractiveness for Kuwait Warehousing Market [Hub scoring-Mina Abdullah, Sulaibiya, Shuwaikh, Ardiya; rent-to-revenue benchmarks; cold-chain premium hubs; e-commerce micro-fulfillment readiness]

7. Supply-Demand Gap Analysis [Land allocated vs absorption; occupancy ratio; undersupply in cold-chain nodes; demand from FMCG, pharma, e-commerce; cross-border throughput to KSA]

8. Market Size for Kuwait Warehousing Market Basis

8.1 Revenues (Historical & Current, In USD Bn)

9. Market Breakdown for Kuwait Warehousing Market Basis

9.1 By Market Structure (3PL Contract Logistics, Captive, Developer-Leased, Free Zone, PPP/JV)

9.2 By Warehouse Type (Ambient, Chilled, Frozen, Bonded/CFS, Open-Yard/Heavy-Lift)

9.3 By Industry Verticals (FMCG & Retail, Pharmaceuticals & Healthcare, E-commerce & CEP, Oil & Gas, Automotive & Industrial)

9.4 By Facility Grade (Grade-A, Grade-B, Grade-C, BTS, Modular)

9.5 By Ownership Model (Developer-owned, 3PL-operated, Captive, Municipality/PAI, PPP/JV)

9.6 By Service Offering (Storage, Cross-docking, VAS, Customs & Bonded, Last-Mile Staging)

9.7 By Region/Hub (Mina Abdullah, Sulaibiya, Shuwaikh/KFTZ, Ardiya, Doha)

10. Demand Side Analysis for Kuwait Warehousing Market

10.1 Corporate Client Landscape & Cohort Analysis [Retailers, pharma distributors, e-commerce giants, O&G operators, automotive service chains]

10.2 Warehousing Needs & Decision-Making Process [Location choice, grade preference, contract length, rent sensitivity]

10.3 Service Effectiveness & ROI Analysis [Inventory accuracy, order turnaround time, VAS contribution to revenue]

10.4 Gap Analysis Framework [Demand vs availability, cold-chain bottlenecks, automation penetration]

11. Industry Analysis

11.1 Trends and Developments [Rise of Grade-A; automation/ASRS adoption; green warehouses; multi-temperature facilities]

11.2 Growth Drivers [E-commerce, FMCG imports, pharma cold-chain, oil & gas spare parts staging, Free Zone incentives]

11.3 SWOT Analysis for Kuwait Warehousing Market

11.4 Issues and Challenges [High power costs, land scarcity, customs dwell time, labor skill gaps]

11.5 Government Regulations [KPA port protocols, PAI zoning, KFTZ rules, customs clearance, food/pharma safety compliance]

12. Snapshot on Online/Tech-Enabled Warehousing Market in Kuwait

12.1 Market Size and Future Potential for Digital Warehousing & Smart Logistics Solutions

12.2 Business Models & Revenue Streams [On-demand warehousing, digital leasing platforms, pay-per-use cold storage]

12.3 Technology Models & Automation [IoT monitoring, WMS/TMS, RFID, ASRS, blockchain-enabled customs clearance]

13. Opportunity Matrix for Kuwait Warehousing Market (Radar Chart) [Hub attractiveness vs sector demand vs technology readiness]

14. PEAK Matrix Analysis for Kuwait Warehousing Market [Classification of players into Leaders, Challengers, Contenders, Emerging players based on capacity, reach, grade, technology adoption, cold-chain capability]

15. Competitor Analysis for Kuwait Warehousing Market

15.1 Market Share of Key Players [Agility Logistics Parks, GAC Kuwait, KGL Logistics, DSV, Aramex, DHL, PostaPlus, Kuehne+Nagel, DB Schenker, CEVA, UPS, FedEx, Hellmann, Kuwait Transcontinental Shipping, TTL Logistics]

15.2 Benchmark of Key Competitors [Company overview, USP, business strategies, business model, pallet capacity, pricing by facility grade, technology used, cold-chain fleet, major clients, strategic tie-ups, marketing strategy, recent development]

15.3 Operating Model Analysis Framework [3PL contract, BTS, Free Zone tenancy, PPP model]

15.4 Gartner Magic Quadrant Equivalent [Player positioning on completeness of offering vs execution capacity]

15.5 Bowman’s Strategic Clock for Competitive Advantage [Cost-leadership, differentiation, hybrid strategies of leading players]

16. Future Market Size for Kuwait Warehousing Market Basis

16.1 Revenues (Forward Projections, In USD Bn)

17. Market Breakdown for Kuwait Warehousing Market Basis

17.1 By Market Structure (3PL, Captive, Developer, PPP, Free Zone)

17.2 By Warehouse Type (Ambient, Chilled, Frozen, Bonded, Open-Yard)

17.3 By Industry Verticals (FMCG & Retail, Pharma & Healthcare, E-commerce & CEP, Oil & Gas, Automotive & Industrial)

17.4 By Facility Grade (Grade-A, Grade-B, Grade-C, BTS, Modular)

17.5 By Ownership Model (Developer-owned, 3PL-operated, Captive, Municipality, PPP/JV)

17.6 By Service Offering (Storage, Cross-docking, VAS, Customs & Bonded, Last-Mile Staging)

17.7 By Region/Hub (Mina Abdullah, Sulaibiya, Shuwaikh, Ardiya, Doha)

18. Recommendation [Strategic investment guidance-cold-chain, automation, Free Zone tenancy]

19. Opportunity Analysis [White-space mapping-pharma hubs, e-commerce fulfillment, bonded facilities]

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities for the Kuwait Warehousing Market. Based on this ecosystem, we will shortlist leading 5–6 warehousing and logistics providers in the country based on their facility capacity, client base, and operational footprint. Sourcing is conducted through port authority statistics, government portals (KPA, PAI, Customs), industry articles, multiple secondary, and proprietary databases to perform desk research around the market to collate industry-level information.

Step 2: Desk Research

Subsequently, we engage in an exhaustive desk research process by referencing diverse secondary and proprietary databases. This approach enables us to conduct a thorough analysis of the market, aggregating industry-level insights. We delve into aspects like the warehousing stock (ambient, chilled, frozen, bonded), end-user mix (FMCG, pharma, e-commerce, oil & gas), land allocations, and other variables. We supplement this with detailed examinations of company-level data, relying on sources such as port reports, operator websites, press releases, annual reports, financial statements, and government circulars. This process aims to construct a foundational understanding of both the market and the entities operating within it.

Step 3: Primary Research

We initiate a series of in-depth interviews with C-level executives and other stakeholders representing various Kuwait Warehousing Market operators and end-users. This interview process serves a multi-faceted purpose: to validate market hypotheses, authenticate statistical data, and extract valuable operational and financial insights from these industry representatives. A bottom-to-top approach is undertaken to evaluate revenue contributions for each player, thereby aggregating to the overall market. As part of our validation strategy, our team executes disguised interviews wherein we approach each company under the guise of potential clients. This approach enables us to validate the operational and financial information shared by company executives, corroborating this data against what is available in secondary databases. These interactions also provide us with a comprehensive understanding of pallet capacities, utilization rates, cold-chain share, value-added services, processes, and compliance factors.

Step 4: Sanity Check

A bottom-to-top and top-to-bottom analysis along with market size modeling exercises is undertaken to assess the sanity of the process. Market estimates are stress-tested against official macro anchors such as merchandise import values, port cargo throughput, airport freight volumes, and Kuwait’s fully urbanized population base. This bi-directional reconciliation ensures the robustness, accuracy, and consistency of the final Kuwait warehousing market model.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Kuwait Warehousing Market holds strong potential, valued at USD 3.4 billion in 2024. This growth is supported by the country’s import-driven economy, with merchandise imports worth USD 32.3 billion, and its fully urban population of 4.97 million residents. Expansion of logistics cities at Shuwaikh, Doha, and Mina Abdullah totaling over 1.6 million m² reinforces future supply. Rising demand from FMCG, pharmaceuticals, and e-commerce sectors further bolsters Kuwait’s warehousing capacity needs.

The Kuwait Warehousing Market features several key players, including Agility Logistics Parks (ALP), GAC Kuwait, and KGL Logistics. These companies dominate due to their large facility footprints, multi-temperature capabilities, and extensive client portfolios. Other notable players shaping the market include DHL Supply Chain, Aramex, DSV, Kuehne+Nagel, DB Schenker, CEVA, UPS, and FedEx, all of which leverage global networks alongside local expertise.

The primary growth drivers include Kuwait’s strong trade flows, with ports like Shuwaikh handling 21 berths and 600,000 m² of storage, and Shuaiba providing 20 berths with a 318,000 m² container yard. E-commerce and CEP demand is rising, supported by 210 million kg of freight handled at Kuwait International Airport. Cold-chain requirements are growing, particularly for pharmaceuticals and fresh food, reflecting biopharma logistics valued at USD 715 million. Collectively, these factors enhance the warehousing sector’s future trajectory.

The Kuwait Warehousing Market faces significant challenges, including limited land availability near urban hubs, where the country’s entire population of 4.97 million is concentrated. Customs processes add complexity, requiring strict compliance with the GCC Common Customs Law and WTO valuation procedures. Energy-intensive cold-chain operations pose another hurdle, as Kuwait’s power generation remains fossil-fuel dominant, raising costs for temperature-controlled storage. Together, these challenges demand efficiency improvements, regulatory streamlining, and investment in resilient infrastructure.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500