Malaysia Recreational Boating Market Outlook to 2030

By Market Structure, By Vessel Type, By Propulsion, By End Use, By Length Class, and By Region/Hub

Report Overview

Report Code

TDR0346

Coverage

Asia

Published

October 2025

Pages

80

On This Page

Report Overview

The report titled “Malaysia Recreational Boating Market Outlook to 2030 – By Market Structure, By Vessel Type, By Propulsion, By End Use, By Length Class, and By Region/Hub” provides a comprehensive analysis of the recreational boating market in Malaysia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the recreational boating market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Malaysia Recreational Boating Market Outlook to 2030 – By Market Structure, By Vessel Type, By Propulsion, By End Use, By Length Class, and By Region/Hub” provides a comprehensive analysis of the recreational boating market in Malaysia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the recreational boating market. The report concludes with future market projections based on fleet size, vessel imports and exports, marina berth capacities, end-use demand, cause-and-effect relationships, and success case studies highlighting the major opportunities and cautions.

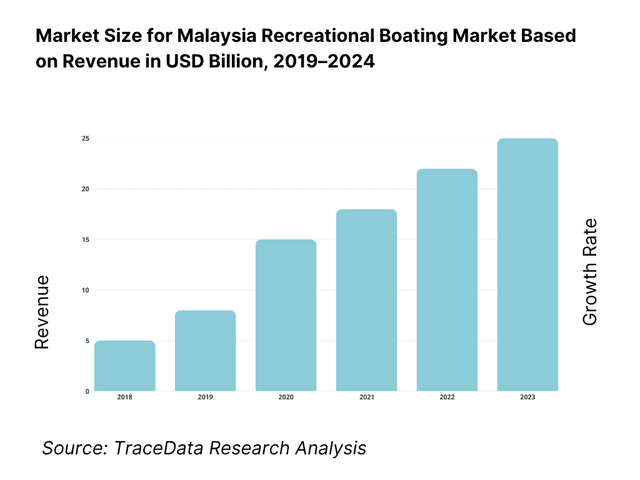

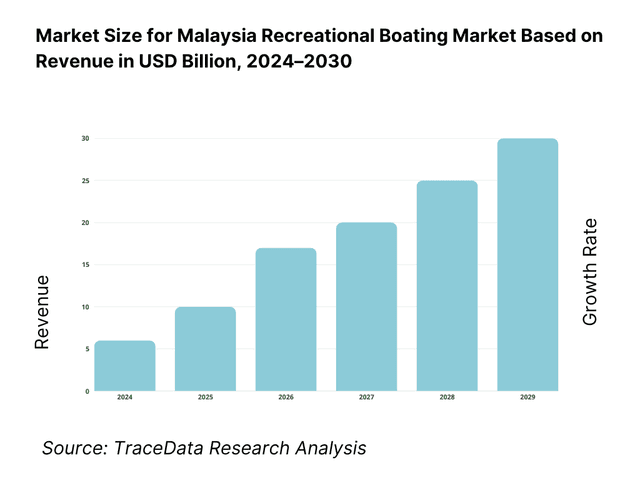

Malaysia Recreational Boating Market Overview and Size

Malaysia’s recreational‐boating economy can be anchored to verifiable hard indicators from official trade and port sources. In the latest full year, exports of recreational boats (HS 8903) reached USD 67.4 million, led by shipments to the United States, Australia and New Zealand. On the inbound side, Malaysia recorded USD 12.5 million of 890399 (rowing boats/canoes/other pleasure craft) imports, and in the following period authorities tracked MYR 127 million of total HS 8903 imports, underscoring rising domestic fleet additions in 2024. Growth is reinforced by easy yacht registration via the Langkawi registry and expanding marina capacity.

Langkawi dominates for leisure cruising because of deepwater marinas, duty-free status, and the Langkawi International Yacht Registry that streamlines flagging and ownership. Royal Langkawi Yacht Club alone provides ~234–250 berths and accepts yachts up to ~80 m, while Telaga/Rebak add sheltered moorings and yard services; together they anchor cruising routes to Penang and Sabah’s east coast islands. Competitive berthing, charter infrastructure, and gateway air links keep these hubs busiest through 2024, supported by clear entry formalities published for yacht arrivals.

What Factors are Leading to the Growth of the Malaysia Recreational Boating Market:

International arrivals and air connectivity feeding leisure cruising and charters: Malaysia’s leisure‐marine demand is underpinned by inbound tourism and air access that concentrate in boating hubs. Malaysia received 37,961,485 foreign visitors, with spending of RM106.8 billion, reinforcing charter enquiries and marina footfall in Langkawi, Penang, Johor and Sabah. Airport throughput confirms accessibility: in December, local airports handled 8.5 million passengers (4.7 million international; 3.8 million domestic), while the domestic sector closed the year at 44.2 million. These macro flows feed yacht day‐trips, multi-day charters and resort-marina occupancies along the west coast and Borneo circuits, providing a steady pipeline of customers for boat rentals, crewed leisure craft and provisioning services.

Rising purchasing power and trade-linked marine logistics supporting boat ownership and upgrades: Upmarket leisure goods—boats, marine electronics and engines—correlate with income and tradable supply chains. Malaysia’s GDP per capita (current US$) stands at 11,867.3, providing a consumer base for owner-operator boats in the 7–18 m range and higher-spec refits. Aviation and trade logistics also enable importation of premium craft and components: Malaysia’s airports handled 941,400 tonnes of air cargo, a channel frequently used for high-value spares and electronics. With tourist receipts at RM106.8 billion, hospitality-linked corporates (hotels, islands, events operators) have parallel reasons to expand watersports fleets, RIBs and tenders, creating secondary demand for service bays, haul-outs and technician hours in marina clusters.

Port and maritime network scale anchoring yacht provisioning and routing options: Malaysia sits on major Asia shipping lanes; this scale spills over into yacht provisioning, chandlery choice and professional services. UNCTAD notes Asia handles 63% of global container trade; congestion analysis shows waiting times in Singapore doubling from 24 to 40 hours, while Port Klang also lengthened—evidence of sustained maritime throughput in the corridor used by yacht logistics (ship-on-ship moves, parts shipments). With 8.5 million monthly passengers at year-end and RM106.8 billion tourism spend, Malaysia’s port-airport ecosystem underwrites reliable access to fuel, spares, surveyors and crew movements, underpinning confidence for owners and charter fleets staging from Langkawi, Penang and Kota Kinabalu.

Which Industry Challenges Have Impacted the Growth of the Malaysia Recreational Boating Market:

Monsoon-driven weather disruptions affecting passages, events and yard schedules: Malaysia’s meteorological regime creates predictable but material boating downtime. METMalaysia characterizes the Northeast Monsoon as concentrating “more than half” of annual rainfall in affected regions, with typical monthly totals above 200 mm in Sabah and widespread seasonal wet conditions noted in its climate briefs. During the 2024/25 season, official communications cited five to seven heavy-rain episodes across Kelantan, Terengganu, Pahang, Johor, Sarawak and Sabah, forcing rescheduling of regattas, reducing safe weather windows for coastal passages and concentrating refits into shorter yard slots. These macro weather counts translate into real marina-side constraints: berth re-allocations, haul-out backlogs and safety-day buffers demanded by insurers and surveyors.

Port congestion ripple effects on yacht logistics and crew flows: Commercial port dynamics influence leisure-marine logistics from spares to customs processing. UNCTAD reports a record ~250,000 container-ship port calls in H2-2023 globally, with Asia carrying 63% of container trade; operational stress raised waiting times in Singapore from 24 to 40 hours and increased queues at Port Klang. For yacht owners, these macro frictions lengthen delivery times for engines, rigging and electronics, complicate ship-on-ship transfers, and can delay pre-season fit-outs. Air travel volatility similarly affects crew changeovers—yet even at year-end peak, Malaysia’s airports still processed 8.5 million passengers in a single month, underscoring the need to book logistics and crew rotations earlier during congestion spikes.

Household purchasing power dispersion and affordability thresholds: While national affluence supports boating, income distribution sets practical ceilings for mass participation. Department of Statistics Malaysia reports a median monthly household income of RM6,338 (latest HIS cycle) and a mean of RM8,479, shaping who can allocate discretionary spend to club memberships, moorings, and leisure-marine fuel and maintenance. With tourism receipts at RM106.8 billio and GDP per capita at US$11,867.3, the market remains anchored to upper-middle income households and corporate users, while broader entry requires boat-club sharing, fractional use and charter access models calibrated to these national income medians.

What are the Regulations and Initiatives which have Governed the Market:

Boat licensing administered by the Marine Department (Jabatan Laut Malaysia): Pleasure craft operating in Malaysian waters must follow Marine Department licensing procedures. The official Boat Licensing User Guideline sets application steps, with forms lodged at regional offices and vessel documentation requirements enumerated (ownership, tonnage, safety equipment). Separate guidance addresses licensing processes for renewals and area-specific permissions. These documents are complemented by the Langkawi International Yacht Registry (LIYR) user guideline for owners seeking the Langkawi flag, aligning registration and operating permissions across duty-free hubs.

Entry compliance for foreign crew/guests via Malaysia Digital Arrival Card (MDAC): Inbound crew and guests arriving by air or sea complete the Malaysia Digital Arrival Card within three days of arrival; government advisories reiterate the requirement and exemptions for specific categories. Supporting notices from official missions confirm that all foreign citizens must file MDAC, while entry requirement pages detail documentation checks at immigration counters. For yacht operations, MDAC enables smoother crew/guest rotations through gateway airports linking directly to marina hubs in Langkawi, Penang, Johor and Sabah, reducing manual form-filling and expediting clearances.

Registry and duty-free facilitation via Langkawi International Yacht Registry (LIYR): Owners frequently leverage Langkawi’s registry and customs regime to streamline vessel administration. The LIYR user guideline issued by the Marine Department codifies yacht and entity registration (eligibility, documentation, renewal periods), giving clarity to homeport decisions. Complementary customs information provides duty processes and traveler declarations (e.g., Royal Malaysian Customs passenger duty page), which, together with Langkawi’s duty-free status under Malaysian law, support provisioning, spares intake and seasonal lay-ups for visiting and home-based fleets.

Malaysia Recreational Boating Market Segmentation

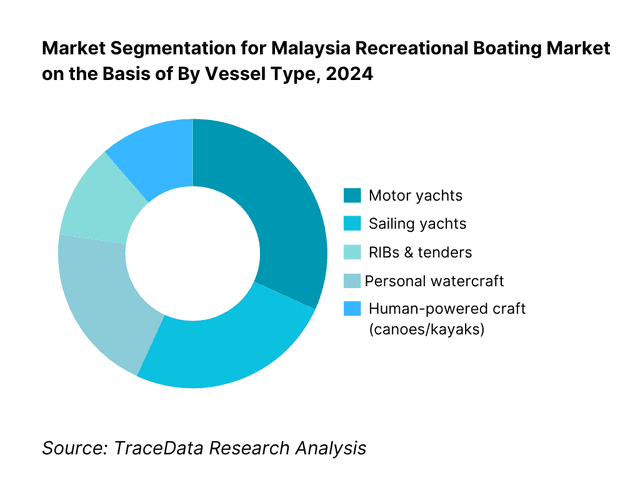

By Vessel Type: Malaysia recreational boating market is segmented by vessel type into motor yachts, sailing yachts, rigid-hulled inflatables & tenders, personal watercraft, and human-powered craft. Recently, motor yachts hold the dominant share because local manufacturing and export strengths are in powered craft under HS 8903, supported by consistent U.S./Australia demand and build-to-order activity for coastal cruising. Duty-free provisioning in Langkawi, straightforward registry services, and deepwater berths up to superyacht size drive owner preference for powered vessels with longer range and hotel-load capability on Malaysia’s island-hopping itineraries from Langkawi–Penang–Pangkor to East Malaysia.

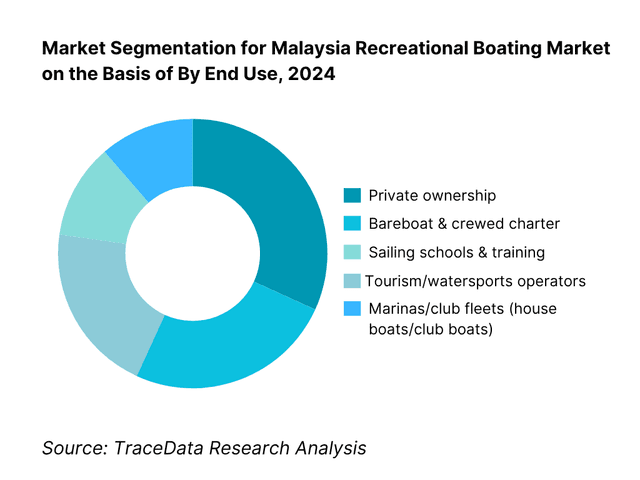

By End Use: Malaysia recreational boating market is segmented by end use into private ownership, bareboat & crewed charter, marinas/club fleets, sailing schools & training, and tourism/watersports operators. The private-ownership segment leads. It benefits from Langkawi’s simplified registry process, asset-friendly tax conditions, and proximity to maintenance yards in Johor/Pasir Gudang that support high-spec refits. Charter is expanding on the back of Langkawi’s duty-free pull and stronger international arrivals, yet boat owners still account for the majority of new registrations and imports, especially in the 9–18 m range suited to Malaysia’s coastal cruising grounds.

Competitive Landscape in Malaysia Recreational Boating Market

The Malaysia recreational boating market shows a hybrid landscape: local manufacturers and yards (Johor, Sarawak) supplying powered craft and refits; marina operators in Langkawi, Penang and Johor anchoring services and yacht tourism; and regional/international brands using Malaysia as a manufacturing or charter base. High visibility hubs such as Royal Langkawi Yacht Club and Telaga/Rebak cluster service providers (lift/repair, chandlery, provisioning), which concentrate spend and reinforce these ports’ influence on boating flows.

Name | Founding Year | Original Headquarters |

Royal Langkawi Yacht Club (RLYC) | 1996 | Langkawi, Malaysia |

Rebak Island Marina | 1995 | Langkawi, Malaysia |

Sutera Harbour Marina | 1998 | Kota Kinabalu, Malaysia |

Royal Selangor Yacht Club | 1969 | Port Klang, Malaysia |

Pen Marine Sdn Bhd | 1988 | Penang, Malaysia |

Simpson Marine (Malaysia operations) | 1984 | Hong Kong, China |

Grand Banks Yachts (American Marine) | 1956 | Hong Kong, China |

Safe World Marine Sdn Bhd | 1982 | Klang, Malaysia |

Pansar Berhad (Marine division) | 1961 | Sibu, Malaysia |

Sabrecraft Marine Sdn Bhd | 2014 | Port Klang, Malaysia |

Boat Lagoon Yachting (Malaysia) | 1994 | Phuket, Thailand |

Explorer Composite | 1970 | Melaka, Malaysia |

Pangkor Marina Malaysia | 2009 | Lumut (Perak), Malaysia |

Puteri Harbour Marina | 2009 | Iskandar Puteri, Malaysia |

Gading Marine Industry (M) Sdn Bhd | 2015 | Sitiawan (Perak), Malaysia |

Some of the Recent Competitor Trends and Key Information About Competitors Include:

Royal Langkawi Yacht Club (RLYC): One of Malaysia’s flagship marinas, RLYC reported high berth occupancy in 2024, driven by international rally events and yacht stopovers. The club enhanced its service portfolio by upgrading fuel dock facilities and expanding concierge offerings, reinforcing its position as a preferred hub for cruising yachts in Southeast Asia.

Pen Marine: A leading yacht dealership and service provider, Pen Marine strengthened its portfolio in 2024 by adding premium brands such as Ferretti and Sunreef. The company also emphasized after-sales service and brokerage support, responding to rising demand from both private owners and charter operators in Penang and Langkawi.

Simpson Marine (Malaysia operations): Known for its strong regional network, Simpson Marine expanded its Malaysia charter management offerings in 2024. With new fleet additions in the sailing catamaran category, the company tapped into growing charter demand from both inbound tourists and resident expat communities.

Safe World Marine: Exclusive distributor for Mercury and Quicksilver, Safe World Marine reported robust outboard engine sales in 2024. Demand was particularly strong in the leisure fishing and coastal cruising segments, prompting the firm to expand its service training programs and dealer support network across West Malaysia.

Sutera Harbour Marina (Kota Kinabalu): As East Malaysia’s premier marina, Sutera Harbour increased its visibility in 2024 by hosting superyacht stopovers and regional regattas. The facility enhanced its bunkering and provisioning services, positioning Kota Kinabalu as a gateway to Borneo’s diving and island-hopping circuits.

What Lies Ahead for Malaysia Recreational Boating Market?

The Malaysia recreational boating market is expected to witness consistent expansion over the next five years, supported by strong inbound tourism, rising disposable incomes, and continued investment in marina infrastructure. Langkawi, Penang, Johor, and Kota Kinabalu are likely to remain key hubs, driven by their strategic location, duty-free benefits, and growing charter demand. Favorable government support for maritime tourism, combined with Malaysia’s role as a regional hub for yacht registry and provisioning, will further strengthen market fundamentals.

Rise of Hybrid Ownership Models: The future of Malaysia’s boating market will see broader adoption of hybrid ownership models such as fractional ownership, club memberships, and charter-to-own programs. These structures will make recreational boating more accessible to the country’s rising affluent class while reducing upfront capital outlays.

Expansion of Charter and Tourism Linkages: The growth of international arrivals and domestic tourism will push demand for crewed charters, sailing schools, and leisure trips around island circuits. Partnerships between marinas, tourism boards, and private operators are expected to expand fleet sizes and develop bundled luxury tourism packages.

Focus on Marina and Infrastructure Modernization: Investments in deepwater berths, haul-out yards, and service centers will play a central role in supporting superyacht stopovers and longer-term layups. As traffic through Langkawi, Pangkor, and Sabah marinas increases, operators will prioritize digital berth management systems, enhanced fuel docks, and refit facilities.

Integration of Green and Smart Technologies: The market will increasingly integrate electric propulsion, eco-friendly hull coatings, and digital monitoring tools. Early trials of electric outboards and connected navigation systems are likely to grow, aligning Malaysia’s boating ecosystem with global sustainability trends and attracting environmentally conscious yacht owners.

Malaysia Recreational Boating Market Segmentation

By Vessel Type

Motor Yachts

Sailing Yachts (Monohull & Multihull)

Rigid-Hulled Inflatable Boats (RIBs) & Tenders

Personal Watercraft (Jet Skis)

Human-Powered Craft (Kayaks, Canoes)

By Propulsion

Outboard Engines (Petrol)

Inboard Engines (Diesel)

Sterndrive / I/O Units

Sail-powered with Auxiliary Engines

Hybrid & Electric Propulsion

By End Use

Private Ownership (HNWI, families, expats)

Bareboat Charter

Crewed Charter & Luxury Events

Sailing Schools & Training Programs

Watersports & Tourism Operators (resorts, hotels, diving companies)

By Length Class

<7 meters (Small craft, PWCs, RIBs)

7–12 meters (Day boats, fishing boats, weekend cruisers)

12–18 meters (Charter yachts, leisure cruisers)

18–24 meters (Mini superyachts)

24 meters (Superyachts)

By Hull Material

Fiberglass/GRP (Composite)

Aluminium

Steel

Inflatable/Hypalon (RIBs, tenders)

Wood/Other Traditional Builds

By Region/Hub

Langkawi (duty-free, LIYR registry, superyacht hub)

West Coast Peninsula (Penang, Port Klang, Johor/Puteri Harbour)

East Coast Peninsula (Tioman, Redang, Terengganu)

Sabah (Kota Kinabalu, Sutera Harbour, Jesselton)

Sarawak (Miri, Bintulu)

Players Mentioned in the Report:

Royal Langkawi Yacht Club (RLYC)

Telaga Harbour Marina

Rebak Island Marina

Sutera Harbour Marina (Kota Kinabalu)

Puteri Harbour Marina (Johor)

Royal Selangor Yacht Club (Port Klang)

Pen Marine Sdn. Bhd.

Simpson Marine (Malaysia operations)

Safe World Marine Sdn. Bhd.

Pansar Company Sdn. Bhd.

HLY Marine Sdn. Bhd.

Explorer Composite / Explorer Boats

Sabrecraft Marine Sdn. Bhd.

Grand Banks Yachts (Johor facility)

Dream Yacht Charter (Langkawi base)

Key Target Audience

Private boat owners & UHNW family offices (seeking registry, berthing, and management options)

Marina investors & infrastructure funds (brownfield/greenfield berths, haul-out, travel-lift capacity)

Boatbuilders & OEM component suppliers (hulls, engines, electrics, nav/telematics)

Charter operators & fleet managers (bareboat/crewed program expansion in Langkawi & Borneo)

Tourism boards & destination management companies (Ministry of Tourism, Arts and Culture Malaysia – MOTAC)

Government & regulatory bodies (Marine Department Malaysia; Royal Malaysian Customs; Immigration Department – MDAC implementation)

Insurance & marine finance lenders (hull/machinery, P&I; credit for dealer networks)

Investments and venture capitalist firms

Time Period:

Historical Period: 2019-2024

Base Year: 2025

Forecast Period: 2025-2030

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Table of Contents

1. Executive Summary

2. Research Methodology

3. Ecosystem of Key Stakeholders in Malaysia Recreational Boating Market-Marina Operators, Yacht Clubs, Dealers & Distributors, OEMs (Engines & Electronics), Local Builders, Charter Operators, Surveyors, Insurance Providers, Regulators (Marine Department, Customs, CIQP), Training Schools

4. Value Chain Analysis

4.1. Delivery Model Analysis for Recreational Boating-Direct Purchase, Dealer Network, Charter-to-Own, Fractional Ownership, Marina Club Membership (Margins, Preferences, Strengths, Weaknesses)

4.2. Revenue Streams for Malaysia Recreational Boating Market (Boat Sales, Marina Berths, Charter Revenues, Maintenance & Refits, Accessories/Chandlery, Training & Certifications)

4.3. Business Model Canvas for Malaysia Recreational Boating Market (Key Partners, Key Activities, Value Propositions, Customer Segments, Revenue Streams, Cost Structures, Channels, Customer Relationships, Resources)

5. Market Structure

5.1. Organized Dealers/Brokers vs. Individual Owner-Operators

5.2. Investment Model in Malaysia Recreational Boating Market (Marina Concessions, Dealerships, Charter Bases, Boat Clubs, Financing)

5.3. Comparative Analysis of Funnelling Process by Private Marinas vs. Government-Linked Hubs

5.4. Boating Expenditure Allocation by Customer Type (HNWI, Charter Clients, Sportfishing, Day-Boat Families)

6. Market Attractiveness for Malaysia Recreational Boating Market-Segment profitability, Berth utilization, Superyacht inflows, Marina capex intensity, Regulatory friction

7. Supply-Demand Gap Analysis-Berth capacity vs. active fleet, Charter demand vs. fleet size, Skilled workforce gap, Marina pipeline projects

8. Market Size for Malaysia Recreational Boating Market Basis

8.1. Revenues, Historical to Current

9. Market Breakdown for Malaysia Recreational Boating Market Basis

9.1. By Market Structure (Organized Dealers/Charter vs. Unorganized Owner-Operators)

9.2. By Craft Type (Sailing Yachts, Motor Yachts, Day Boats, RIBs/PWs, Catamarans)

9.3. By Use Case (Private Leisure, Charter, Fishing & Diving, Watersports, Corporate Events)

9.4. By Company Size of Operators (Large Dealers/Marinas, Medium Enterprises, SMEs/Owner-Operators)

9.5. By Customer Designation (HNWI Individuals, Families, Tourists, Corporate Buyers, Clubs)

9.6. By Mode of Ownership (Outright Purchase, Fractional, Club Membership, Charter-to-Own)

9.7. By Open and Customized Programs (Shared Cruises vs. Tailor-Made Yachting Experiences)

9.8. By Region (Langkawi, West Coast Corridor, East Coast, Sabah, Sarawak)

10. Demand Side Analysis for Malaysia Recreational Boating Market

10.1. Customer Cohort Analysis (HNWI, Expat Communities, Domestic Tourists, International Arrivals)

10.2. Boating Needs and Decision-Making Process (Craft Type, Berthing, Maintenance, Financing)

10.3. Program Effectiveness & ROI Analysis (Charter Utilization, Marina Yield, Owner-Operator Economics)

10.4. Gap Analysis Framework (Demand Hotspots vs. Infrastructure Readiness)

11. Industry Analysis

11.1. Trends and Developments (Foiling & E-boats, Catamaran Uptake, Marina Real Estate Integration, Digital Aggregator Platforms)

11.2. Growth Drivers (Tourism Inflows, HNWI Density, Charter Demand, Duty-Free Zones)

11.3. SWOT Analysis for Malaysia Recreational Boating Market

11.4. Issues and Challenges (Berth Scarcity, Import Duties Outside Duty-Free Zones, Skilled Workforce, Safety Compliance)

11.5. Government Regulations (Marine Department, LIYR Registration, Customs/TIP, Safety Standards, Environmental Mandates)

12. Snapshot on Online & Digital Platforms in Recreational Boating

12.1. Market Size and Future Potential of Online Charter Aggregators in Malaysia

12.2. Business Model and Revenue Streams (Commission, Subscription, Direct Sales)

12.3. Digital Delivery Models and Service Offerings (Charter Booking, Marina Berth Reservations, Boat Clubs, Maintenance Platforms)

13. Opportunity Matrix for Malaysia Recreational Boating Market-Presented with Radar Chart

14. PEAK Matrix Analysis for Malaysia Recreational Boating Market

15. Competitor Analysis for Malaysia Recreational Boating Market

15.1. Market Share of Key Players in Malaysia Recreational Boating Market (Basis Revenues & Fleet/Inventory)

15.2. Benchmark of Key Competitors Including Variables: (Company Overview, Investment & Funding, Revenues, Number of Listings, Pricing Models, Subscribers, Fleet Size, Partnerships)

15.3. Operating Model Analysis Framework

15.4. Gartner Magic Quadrant (Adapted for Dealer/Charter/Marina Landscape)

15.5. Bowman’s Strategic Clock for Competitive Advantage

16. Future Market Size for Malaysia Recreational Boating Market Basis

16.1. Revenues, Forecast Period

17. Market Breakdown for Malaysia Recreational Boating Market Basis (Future)

17.1. By Market Structure (Organized vs. Unorganized)

17.2. By Craft Type (Sailing Yachts, Motor Yachts, Day Boats, RIBs/PWs, Catamarans)

17.3. By Use Case (Private, Charter, Fishing & Diving, Watersports, Corporate)

17.4. By Company Size of Operators

17.5. By Customer Designation

17.6. By Mode of Ownership

17.7. By Open and Customized Programs

17.8. By Region (Langkawi, West Coast, East Coast, Sabah, Sarawak)

18. Recommendation

19. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all demand-side and supply-side entities in the Malaysia Recreational Boating Market. On the demand side, this includes private boat owners, high-net-worth individuals, charter customers, sailing schools, and tourism operators. On the supply side, it includes marinas, yacht clubs, domestic boatbuilders, international dealerships, engine OEM distributors, refit yards, and regulatory bodies such as the Marine Department Malaysia. Based on this ecosystem, we shortlist 5–6 leading competitors including marina operators, boatbuilders, and dealers, benchmarked by fleet size, berth capacity, after-sales service footprint, and regional coverage.

Step 2: Desk Research

An exhaustive desk research process is conducted by referencing diverse secondary and proprietary databases. We aggregate industry-level insights such as trade values of HS 8903 (pleasure boats), marina berth capacity statistics, household income data, and tourism inflows. Company-level information is compiled from press releases, annual reports, operator websites, and financial disclosures. This enables analysis of factors including registered vessel counts, marina utilization rates, and after-sales service capabilities. Particular attention is given to regulatory documents issued by the Marine Department (e.g., licensing, Langkawi International Yacht Registry guidelines) and Immigration Malaysia (e.g., MDAC requirements for foreign crew).

Step 3: Primary Research

In-depth interviews are initiated with stakeholders across the value chain — marina managers, dealership principals, refit yard operators, charter company executives, and government regulators. These interactions serve to validate desk research hypotheses, confirm operational data, and provide insights into revenue flows. A bottom-to-top approach is employed by mapping berth occupancy and fleet utilization, then aggregating it to the national level. Disguised interviews are also conducted under the guise of potential charter clients or owners, enabling validation of service tariffs, maintenance processes, and vessel availability. This triangulation ensures the robustness of revenue streams, value chains, and cost structures.

Step 4: Sanity Check

A dual approach of bottom-to-top (aggregating vessel sales, imports, marina berths, and charters) and top-to-bottom (aligning with macroeconomic tourism receipts, household income distribution, and maritime trade volumes) is used to ensure accuracy. Market size modeling is reconciled against both official trade values and on-ground operational statistics, ensuring consistency in the final outputs. This process establishes a validated and auditable framework for understanding the Malaysia Recreational Boating Market.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Malaysia Recreational Boating Market holds strong potential, supported by the country’s strategic location along key Southeast Asian cruising routes and its duty-free hubs such as Langkawi. With 37.9 million tourist arrivals and tourism receipts of RM106.8 billion recorded by Tourism Malaysia in 2024, demand for yacht charters, marina berths, and leisure craft ownership is set to deepen. The market’s potential is further enhanced by the growth of luxury tourism, expanding marina infrastructure in Langkawi, Johor, and Kota Kinabalu, and the ease of yacht registration through the Langkawi International Yacht Registry.

The Malaysia Recreational Boating Market is shaped by marina operators, boatbuilders, and dealership networks. Leading players include Royal Langkawi Yacht Club, Telaga Harbour Marina, Sutera Harbour Marina, Pen Marine, and Simpson Marine. These companies dominate through berth capacity, premium yacht brands, and after-sales service networks. Other notable contributors include Safe World Marine (Mercury distributor), Rebak Island Marina, and Grand Banks Yachts’ Johor facility, all of which strengthen the supply-side ecosystem by offering vessel sales, engine distribution, marina services, and refit capabilities.

Key growth drivers include Malaysia’s tourism inflows, with airports handling 8.5 million passengers in December alone, underpinning strong connectivity to boating hubs. Rising GDP per capita at USD 11,867.3, reported by the World Bank, supports higher leisure spending and ownership of yachts and personal watercraft. Furthermore, Malaysia’s strategic maritime network, with Port Klang and Johor serving as major global shipping corridors, creates a robust logistics ecosystem that indirectly benefits yacht provisioning, spares, and crew access. Together, these factors stimulate charter demand, yacht imports, and marina expansion.

The Malaysia Recreational Boating Market faces notable challenges. Seasonal Northeast Monsoon rainfall exceeding 200 mm in parts of Sabah and Sarawak restricts safe boating windows and strains marina scheduling. Port congestion also impacts yacht logistics, with UNCTAD noting rising waiting times in Singapore from 24 to 40 hours, which slows spares and new craft deliveries. Additionally, median monthly household income at RM6,338, as reported by Malaysia’s Department of Statistics, highlights affordability constraints for mass boating adoption, confining ownership largely to high-net-worth individuals and corporate operators.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500