Maldives NFT & Blockchain Gaming Market Outlook to 2030

By Participation Model, By Tourism & Venue Vertical, By Game Genre, By Blockchain/Infrastructure, By Monetization Model, and By User Cohort

Report Overview

Report Code

TDR0348

Coverage

Asia

Published

October 2025

Pages

80

On This Page

Report Overview

The report titled “Maldives NFT & Blockchain Gaming Market Outlook to 2030 – By Participation Model, By Tourism & Venue Vertical, By Game Genre, By Blockchain/Infrastructure, By Monetization Model, and By User Cohort” provides a comprehensive analysis of the NFT and blockchain gaming market in the Maldives. The report covers an overview and genesis of the industry, overall market indicators in terms of adoption, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the NFT and blockchain gaming market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Maldives NFT & Blockchain Gaming Market Outlook to 2030 – By Participation Model, By Tourism & Venue Vertical, By Game Genre, By Blockchain/Infrastructure, By Monetization Model, and By User Cohort” provides a comprehensive analysis of the NFT and blockchain gaming market in the Maldives. The report covers an overview and genesis of the industry, overall market indicators in terms of adoption, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the NFT and blockchain gaming market. The report concludes with future market projections based on participation models, tourism and venue activations, blockchain infrastructure, monetization methods, user cohorts, cause-and-effect relationships, and success case studies highlighting the major opportunities and cautions.

Maldives NFT & Blockchain Gaming Market Overview and Size

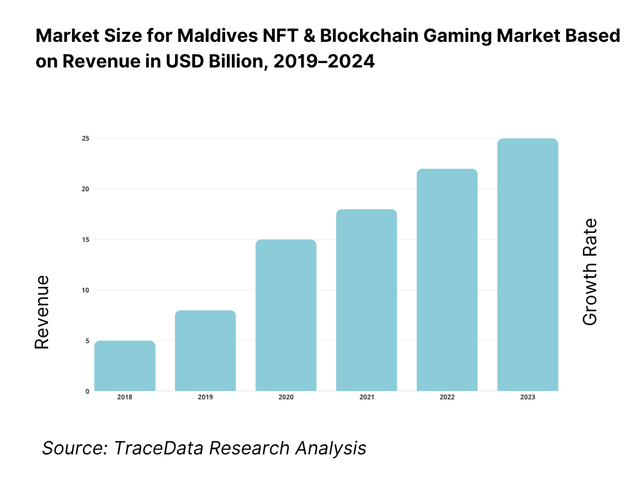

The Maldives NFT and Blockchain Gaming Market is currently valued at US$8 million as of 2024.The addressable base is anchored by 1,878,543 international arrivals and ~435,800 internet users locally, supported by ~376,000 social identities, creating recurring spikes in digital leisure spending and discovery. Global Web3 gaming hovered around ~1.1 million daily active wallets on average in the year, indicating deep content supply and tooling maturity that publishers can localize into Maldives’ resort ecosystems. In the following year, arrivals reached roughly ~2.05 million, and internet users grew to ~448,000, strengthening the top-of-funnel for on-chain titles and tourism-utility NFTs.

Activity concentrates in Greater Malé (dense population, airport proximity, payments infrastructure) and resort-heavy atolls north and south of Malé where guest Wi-Fi, venue apps, and curated experiences enable NFT ticketing, loyalty, and in-venue quests. The concentration is reinforced by MMA-licensed payment service providers, robust 4G/5G mobile coverage by two MNOs, and operational readiness of resorts that collectively hosted over two million inbound guests in the following year. The combination of connectivity, venue operations, and spend-ready tourist cohorts sustains pilot-to-scale pathways.

What Factors are Leading to the Growth of the Maldives NFT & Blockchain Gaming Market:

Tourism scale creates a ready-made top-of-funnel for tokenized game items and venue NFTs: Inbound leisure demand is unusually dense for a micro-market: the Maldives welcomed 1,878,543 tourist arrivals in the concluding year and 2,050,000 arrivals in the following year, both recorded by the authorities. The resident base was 527,799 people, so international inflows dwarf the domestic population and concentrate spend in resort islands and Greater Malé. This continuous inflow sustains QR/NFC onboarding at venues and ticketed experiences that can mint NFTs without relying solely on domestic gamers. These real-economy volumes support predictable player acquisition and secondary trading depth during resort seasons.

Digital readiness lowers onboarding friction for custodial and seedless wallets: The Maldives exhibits high communications penetration relative to its size: mobile subscriptions stood at ~142 per 100 people and internet use reached ~84.7 per 100 people, with both indicators reported in the latest World Bank/ITU series. A digitally reachable base of ~445,000–450,000 individuals (proxied by population and internet-use share) supports account-abstraction logins and guest-mode wallets in resort apps, reducing in-venue drop-offs. Strong mobile networks from two licensed MNOs also enable web/PWA distribution paths when app-store constraints apply, and they stabilize in-resort play sessions for on-chain games and loyalty redemptions.

High-income tourism economy and formal payment rails support compliant on-ramps: Macroeconomic capacity to transact is visible in headline indicators: nominal GDP reached US$6.98 billion and GDP per person reached US$13,215.5 in the latest releases. Tourism remains the lead earner, with the World Bank noting a record 2.05 million inbound visitors in the following year and a rebound in travel receipts (official WDI series). With the National Payment System Act (Law No. 8/2021) in force and a formal licensing regime for Payment Service Providers, venues can pair fiat rails with custodial wallets for KYC-tiered purchases, refunds and chargeback handling—key conditions for mainstream NFT and in-game transaction adoption in resorts.

Which Industry Challenges Have Impacted the Growth of the Maldives NFT & Blockchain Gaming Market:

FX, settlement and off-ramp frictions in a small, import-reliant economy: A small open economy with US$6.98 billion output and concentrated resort receipts must convert between MVR and foreign currency frequently for suppliers and investors. Under the central bank’s remit, most domestic transactions are required to settle in MVR, with defined exemptions under foreign-currency regulations—this complicates direct off-ramps from NFT marketplaces into foreign accounts for venues without PSP arrangements. The IMF’s Financial System Stability work also flags needs to strengthen liquidity operations and risk-based AML supervision, which affects how quickly gaming venues can scale higher-throughput cash-outs.

Connectivity dispersion across atolls raises quality-of-service hurdles for real-time play: While internet use is ~84.7 per 100 people and mobile penetration is ~142 per 100 people, geography creates long tails in last-mile performance between resort islands and remote atolls. The sandbox/innovation brief for the monetary authority documents only two mobile network operators, which simplifies regulatory coordination but limits redundancy for island-hopping events and esports activations. For blockchain titles that depend on session stability and quick signing, operators must design offline-tolerant flows, asset streaming and low-latency caches to cushion variable throughput during peak resort occupancy.

Compliance burden (KYC/AML/CFT) for small teams and indie studios: The Prevention of Money Laundering and Terrorism Financing Act (2014) sets obligations on customer due diligence and suspicious-transaction reporting, and the central bank’s Regulation on Payment Services (2022) imposes conditions on electronic-money issuance. For game publishers integrating fiat top-ups and NFT withdrawals via local PSPs, these rules translate to tiered KYC thresholds, sanctions screening and travel-rule awareness. The World Bank’s payment-systems oversight papers indicate that only licensed banks and MNOs may issue e-money, constraining indie teams and pushing them toward PSP partnerships for compliance capacity.

What are the Regulations and Initiatives which have Governed the Market:

National Payment System Act (Law No. 8/2021) and PSP licensing guidelines define rails: The central piece of payments law—NPS Act 8/2021—establishes oversight, licensing, operational and settlement requirements for payment systems, with the Guideline on Licensing of Payment Services setting entry criteria for PSPs. A World Bank program note reports eight Payment Service Providers licensed under the new framework, enabling venues to route card/QR top-ups into custodial wallets with chargeback recourse and settlement SLAs. For blockchain-gaming deployments in resorts, this law is the anchor for compliant on-ramps and refunds tied to digital goods.

AML/CFT law and supervisory expectations shape KYC tiers and NFT cash-outs: The Prevention of Money Laundering and Terrorism Financing Act (2014) and subsequent supervisory guidance require reporting entities and payment providers to conduct customer due diligence, maintain records and report suspicious activity. The IMF’s financial-stability assessment calls for stronger risk-based AML/CFT supervision and clarified enforcement standards—signals that PSP partners will keep KYC thresholds conservative for higher-risk flows, including peer-to-peer withdrawals of digital assets. For publishers, aligning wallet tiers with PSP KYC levels is necessary for scalable redemptions and tournament payouts.

Personal data protection is moving from draft to formalization—design for privacy-by-default: While a comprehensive data-protection statute is not yet enacted, a Privacy and Personal Data Protection Bill has been circulated for public comment by the government. UNDP’s 2025 policy note also lists a 2024 draft in the legislative pipeline. For Web3 gaming, this makes privacy-by-default designs—local processing, data minimization, and selective disclosure—essential ahead of final lawmaking, especially when resort guest apps collect identity and payment data to provision custodial wallets. Teams should architect for future compliance rather than retrofitting later.

Maldives NFT & Blockchain Gaming Market Segmentation

By Participation Model: The Maldives NFT & blockchain gaming market is segmented by participation model into custodial, non-custodial, hybrid, guest passes, and KYC-tiered cohorts. Recently, custodial access is functionally dominant because resort guests and casual players value frictionless onboarding (email/social login, card on-ramp, recovery), while venues need chargeback workflows with licensed PSPs. MMA’s payment regime and two MNOs’ coverage further support custodial flows in guest apps and QR/NFC journeys, making seed-less wallets the default at check-in or concierge onboarding.

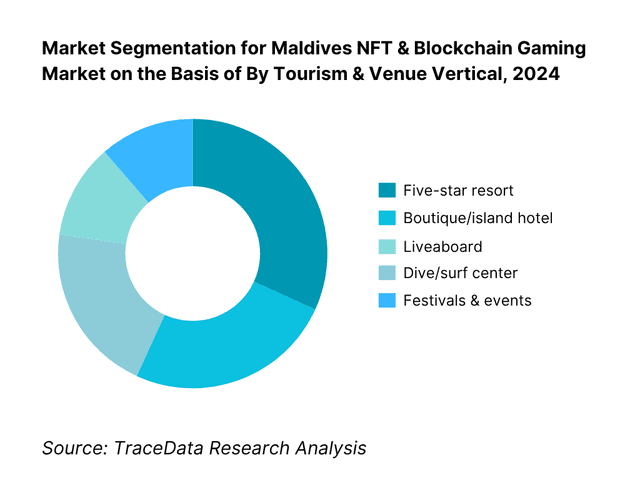

By Tourism & Venue Vertical: Maldives NFT & blockchain gaming market is segmented by tourism & venue vertical into five-star resorts, boutique/island hotels, liveaboards, dive/surf centers, and festivals & events. Recently, five-star resorts lead effectively because they host the highest-spend guests, operate mature guest apps, and run curated activities that lend themselves to token-gated perks, digital collectibles, and event ticketing. With over ~2.0 million international arrivals in the following year and robust resort Wi-Fi, premium properties are first adopters for on-chain loyalty, proof-of-experience NFTs, and co-branded mints.

Competitive Landscape in Maldives NFT & Blockchain Gaming Market

The Maldives NFT & blockchain gaming landscape is shaped by global Web3 game publishers and marketplaces that are accessible to Maldivian residents and tourists, alongside local venue operators and licensed PSP rails. Global platforms dominate tooling, liquidity, and IP pipelines (per DappRadar’s global coverage of Web3 gaming activity), while MMA’s National Payment System Act and PSP licensing set the integration guardrails for fiat on-/off-ramps in guest journeys. This consolidation underscores the influence of a handful of international ecosystems and venue partners.

Name | Founding Year | Original Headquarters |

Sky Mavis (Axie Infinity) | 2018 | Ho Chi Minh City, Vietnam |

Animoca Brands | 2014 | Hong Kong, China |

Immutable | 2018 | Sydney, Australia |

Gala Games | 2019 | San Francisco, USA |

The Sandbox (Pixowl/Animoca) | 2011 | San Francisco, USA |

Decentraland Foundation | 2015 | Buenos Aires, Argentina |

Sorare | 2018 | Paris, France |

Mythical Games | 2018 | Los Angeles, USA |

Horizon Blockchain Games | 2017 | Toronto, Canada |

Illuvium | 2020 | Sydney, Australia |

Wemade (WEMIX) | 2000 | Seongnam, South Korea |

Netmarble (MARBLEX) | 2000 | Seoul, South Korea |

Com2uS (XPLA) | 1998 | Seoul, South Korea |

Yield Guild Games | 2020 | Manila, Philippines |

OpenSea | 2017 | New York, USA |

Some of the Recent Competitor Trends and Key Information About Competitors Include:

Sky Mavis (Axie Infinity): As a pioneer in play-and-earn gaming, Sky Mavis has expanded its ecosystem through the Ronin chain, introducing account abstraction wallets in 2024 to simplify onboarding for casual players and tourists. This aligns with the rising demand for low-friction access in emerging markets like the Maldives.

Animoca Brands: Known for its extensive portfolio of blockchain-based games, Animoca Brands has strengthened partnerships with hospitality and entertainment sectors in 2024, focusing on NFT-driven loyalty programs and metaverse activations that can be adapted to resort-based experiences in the Maldives.

Immutable: Specializing in scaling NFT games, Immutable launched its zkEVM chain in 2024, enabling developers to deploy low-cost and compliant NFT marketplaces. This infrastructure offers strong potential for Maldives-based resorts looking to issue digital collectibles for guests.

Gala Games: A leader in Web3 entertainment, Gala Games expanded its portfolio into music and film NFTs in 2024, showcasing a cross-media strategy. Such diversification creates opportunities for Maldivian festivals and events to leverage Gala’s ecosystem for token-gated experiences.

The Sandbox: The Sandbox has enhanced its creator toolkit and brand activations in 2024, onboarding major global IPs into its metaverse. Its UGC focus positions it as a strong partner for Maldivian cultural festivals and tourism operators seeking immersive virtual showcases.

What Lies Ahead for Maldives NFT & Blockchain Gaming Market?

The Maldives NFT & blockchain gaming market is expected to advance steadily, powered by the country’s strong tourism inflows, high digital adoption, and a supportive payments framework under the National Payment System Act (8/2021). With over 2.05 million tourist arrivals and more than 445,000 internet users, the market is positioned for expansion as resorts, liveaboards, and event operators increasingly experiment with token-gated experiences, loyalty NFTs, and blockchain-enabled gaming solutions. Growth will also be supported by account abstraction wallets, which simplify onboarding for casual players and tourists.

Rise of Venue-Led NFT & Gaming Integrations: The future of blockchain gaming in the Maldives is likely to be shaped by resort and event-driven activations, where NFTs function as tickets, loyalty perks, or proof-of-experience collectibles. This venue-first model is driven by the country’s reliance on international arrivals and the need to integrate digital collectibles seamlessly into premium guest journeys. Resorts and festivals will lead adoption, using NFTs to differentiate experiences and build repeat visitation.

Focus on Compliance-Centric Ecosystems: As the Maldives Monetary Authority strengthens oversight through licensed Payment Service Providers (PSPs), there will be a growing emphasis on compliant custodial wallets and tiered KYC solutions. The market will move towards balancing innovation with regulatory requirements, ensuring that token transactions remain secure, transparent, and AML/CFT-compliant. This will create trust among tourists, operators, and financial institutions, anchoring sustainable long-term growth.

Expansion of Cross-Sector Use Cases: Blockchain gaming and NFTs are set to expand beyond pure entertainment into tourism, sports, cultural events, and water-sports centers. From dive log NFTs and surf achievement badges to festival ticketing and resort loyalty passes, multiple verticals will adopt tokenization. This diversification will support higher transaction volumes, improve guest engagement, and create a resilient ecosystem that does not rely solely on speculative play-and-earn models.

Leveraging Web3 Infrastructure & Global IP: The deployment of low-cost Layer-2 blockchains like Immutable zkEVM, Polygon, and Ronin will make NFTs cheaper to mint and trade, while major publishers like Animoca Brands, Sky Mavis, and Sorare will introduce branded IP experiences to Maldivian players and tourists. With mobile penetration at 142 per 100 people and internet adoption at 84.7 per 100 people, the Maldives has the digital infrastructure to localize global Web3 gaming trends and adapt them to its unique tourism-driven economy.

Maldives NFT & Blockchain Gaming Market Segmentation

By Participation Model

Custodial Wallet Access

Non-Custodial (Self-Custody)

Account-Abstracted / Hybrid Seedless

Guest-Pass (Venue-Issued Temporary Access)

KYC-Tiered Cohorts

By Tourism & Venue Vertical

Five-Star Resorts

Boutique / Island Hotels

Liveaboards

Dive & Surf Centers

Festivals & Cultural Events

By Game Genre

Role-Playing & Adventure Games (RPGs)

Sports & Fantasy Leagues (incl. Cricket/Football NFTs)

Trading Card & Strategy Games

Metaverse & Sandbox Worlds

Casual & Hyper-Casual Mobile Games with NFT Cosmetics

By Blockchain / Infrastructure

Polygon

BNB Chain

Ronin

Solana

Ethereum L2s / Rollups

By Monetization Model

Primary NFT Sales / Mints

Secondary Market Royalties

Play-and-Earn Token Systems (with sinks & sources)

Subscriptions & Battle Passes

Advertising & Sponsorship Integrations

Players Mentioned in the Report:

Sky Mavis (Axie Infinity)

Animoca Brands (incl. The Sandbox, Phantom Galaxies)

Immutable

Gala Games

The Sandbox

Decentraland Foundation

Sorare

Mythical Games

Horizon Blockchain Games (Sequence, Skyweaver)

Illuvium

Wemade (WEMIX)

Netmarble (MARBLEX)

Com2uS (XPLA)

Yield Guild Games

OpenSea

Key Target Audience

Investments and venture capitalist firms (Web3 gaming & consumer tech funds)

Government and regulatory bodies — Maldives Monetary Authority (MMA), Ministry of Tourism, Communication Authority of Maldives

Resort & hotel owner-operators (island and five-star brands)

Liveaboard fleet owners and dive/surf center operators

Licensed Payment Service Providers (PSPs) and acquiring banks

Mobile network operators & ISPs (in-venue connectivity partners)

Esports organizers & gaming communities (regional guilds)

Digital creators & influencer networks active in leisure/tourism

Time Period:

Historical Period: 2019-2024

Base Year: 2025

Forecast Period: 2025-2030

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Table of Contents

1. Executive Summary

2. Research Methodology

3. Ecosystem of Key Stakeholders in Maldives NFT & Blockchain Gaming Market (players; indie studios & publishers; resorts/liveaboards/water-sports centers; MNOs/ISPs; PSPs/banks/OTC; NFT marketplaces; wallet providers; chains/L2s; guilds & esports; creators/streamers; regulators & tourism bodies)

4. Value Chain Analysis

4.1. Delivery Model Analysis (custodial wallets; non-custodial AA wallets; web/PWA; app store-compliant builds; venue QR/NFC onboarding-margins, preference, strengths & weaknesses)

4.2. Revenue Streams (primary NFT mints; secondary royalties; subscriptions/battle passes; ad & sponsorship; resort co-marketing; IP licensing; in-app purchases via fiat; event ticketing; merchandise & collectibles)

4.3. Business Model Canvas (customer segments: residents/tourists/expats/guilds; value propositions: token-gated experiences/loyalty; channels: resort apps/social mini-apps; key partners: PSPs/MNOs/resorts; cost structure; revenue structure; compliance resources)

5. Market Structure

5.1. Indie Developers vs. AAA/Publisher-Backed Titles (tooling depth; distribution power; live-ops maturity; compliance readiness)

5.2. Investment Models (token grants; publisher advances; resort innovation budgets; chain/ecosystem funds; venture/PE; revenue-share with venues)

5.3. Comparative Acquisition Funnels: Resort-Led vs. Pure Online (concierge/QR onboarding vs. social/ads; CAC, activation, Day-7 retention, upsell to NFTs)

5.4. Web3 Budget Allocation by Company Size (micro/indie, mid-tier, large publishers-split across dev, UA, creator, compliance, audits, liquidity & grants)

6. Market Attractiveness for Maldives NFT & Blockchain Gaming (tourism arrivals; ARPDAU uplift via venue utilities; MVR on/off-ramp ease; data cost & latency; regulatory clarity; seasonality; competitive intensity)

7. Supply-Demand Gap Analysis (local developer capacity; wallet support SLAs; venue tech enablement; guild demand vs. quality content; fiat on-ramp throughput vs. peak events)

8. Market Size for Maldives NFT & Blockchain Gaming (In USD Bn)

8.1. Revenues (publisher gross bookings, NFT GMV, ad & sponsorship, royalties, venue commissions)

9. Market Breakdown for Maldives NFT & Blockchain Gaming

9.1. By Participation Model (custodial access; non-custodial; hybrid; guest passes; KYC-tiered cohorts)

9.2. By Game Genre (RPG & adventure; sports & fantasy; trading card/strategy; metaverse/sandbox; casual & hyper-casual with NFT cosmetics)

9.3. By Tourism & Venue Vertical (five-star resort; boutique/island hotel; liveaboard; dive/surf center; festivals & events)

9.4. By User Cohort (local residents; expat workforce; inbound tourists; students/young professionals; esports/guild players)

9.5. By Distribution Channel (Google Play-compliant builds; web/PWA; resort guest apps/QR; social mini-apps; PC launchers)

9.6. By Blockchain/Infrastructure (Polygon; BNB Chain; Ronin; Solana; Ethereum L2/rollups)

9.7. By Monetization Model (primary mints; secondary royalties; subscriptions; tokens with sinks/sources; ads & sponsorships)

9.8. By Region/Atoll Cluster (Malé & Greater Malé; central atolls; southern atolls; northern atolls; airport/transit zones)

10. Demand-Side Analysis for Maldives NFT & Blockchain Gaming

10.1. Player & Partner Cohorts (tourists by trip purpose & spend tier; residents by device & ARPU; resort categories; guilds by game affinity)

10.2. Decision-Making Process (wallet choice; KYC thresholds; resort procurement & IT/security approvals; PSP selection; chain grants)

10.3. Program Effectiveness & ROI (LTV by cohort; NFT attach & resale velocity; venue ancillary revenue; sponsor ROAS; retention & reactivation)

10.4. Gap Analysis Framework (onboarding friction; language/MVR pricing; bandwidth limits; fraud risk; age-gating & family segments)

11. Industry Analysis

11.1. Trends & Developments (custodial→AA wallets; sustainable P&E; venue SDKs; off-chain proofs; cross-chain liquidity; creator economy)

11.2. Growth Drivers (tourism footfall; social discovery; resort partnerships; grants & ecosystem funds; mobile-first usage)

11.3. SWOT Analysis (tourism synergy; small TAM challenge; venue IP leverage; policy/FX frictions)

11.4. Issues & Challenges (UX; scams/phishing; gas volatility; app-store policies; cross-border compliance)

11.5. Government & Regulatory Environment (PSP licensing; AML/CFT & KYC tiers; consumer protection; advertising & age-rating; taxation of digital goods & royalties)

12. Snapshot on Online/On-Chain Gaming & NFT Commerce

12.1. Market Size & Future Potential (Maldives-aligned Web3 gaming & NFT commerce)

12.2. Business Models & Revenue Stacks (mint/royalty/subscription/ads/IP licensing; venue commissions)

12.3. Delivery Models & Course-Equivalents (player education paths: wallet 101; safety; venue staff enablement; creator toolchains)

13. Opportunity Matrix for Maldives NFT & Blockchain Gaming (radar across tourism utility readiness; on-ramp depth; bandwidth resilience; localization; compliance; liquidity; creator enablement; partner ecosystem)

14. PEAK Matrix Analysis for Maldives NFT & Blockchain Gaming (leaders; major contenders; aspirants-scored on innovation, execution, compliance, venue readiness, liquidity, UX)

15. Competitor Analysis for Maldives NFT & Blockchain Gaming

15.1. Market Share of Key Players (accessible user base; GMV; titles present in Maldives; chain coverage)

15.2. Benchmark of Key Competitors (company overview; USP; strategy; business model; live-ops depth; number of titles; revenues/GMV; pricing/take-rates; tech stack; best-selling titles; major partners/resorts; marketing; recent developments)

15.3. Operating Model Analysis Framework (publishing; creator ecosystem; venue integrations; fraud/risk; compliance ops; support SLAs)

15.4. Magic Quadrant-Style Positioning (vision completeness vs. execution ability for MV context)

15.5. Bowman’s Strategic Clock (price/value positioning for NFTs & passes; differentiation levers)

16. Future Market Size for Maldives NFT & Blockchain Gaming (In USD Bn)

16.1. Revenues (publisher gross bookings, NFT GMV, venue & sponsorship economics, royalties)

17. Future Market Breakdown for Maldives NFT & Blockchain Gaming

17.1. By Participation Model (custodial; non-custodial; hybrid; guest passes; KYC-tiered)

17.2. By Game Genre (RPG; sports/fantasy; trading card/strategy; metaverse/sandbox; casual/hyper-casual)

17.3. By Tourism & Venue Vertical (resort; boutique/island; liveaboard; dive/surf; festivals/events)

17.4. By User Cohort (residents; expats; tourists; students; guild/esports)

17.5. By Distribution Channel (app store-compliant; web/PWA; resort guest apps/QR; social mini-apps; PC launchers)

17.6. By Blockchain/Infrastructure (Polygon; BNB Chain; Ronin; Solana; Ethereum L2/rollups)

17.7. By Monetization Model (mints; royalties; subscriptions; tokens; ads/sponsorships)

17.8. By Region/Atoll Cluster (Malé & Greater Malé; central; southern; northern; airport/transit)

18. Recommendation (entry sequencing, compliance path, chain & PSP pairing, resort pilot playbooks, KPI guardrails)

19. Opportunity Analysis (white spaces: venue SDK gaps; creator academies; low-bandwidth UX; MVR pricing; fraud tooling; family-friendly experiences)

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities for the Maldives NFT & Blockchain Gaming Market. Based on this ecosystem, we will shortlist leading 5–6 blockchain game publishers and infrastructure providers accessible in the Maldives based on their market reach, partnerships with resorts/events, and user accessibility. Sourcing is conducted through government portals, industry articles, multiple secondary, and proprietary databases to perform desk research around the market to collate industry-level information.

Step 2: Desk Research

Subsequently, we engage in an exhaustive desk research process by referencing diverse secondary and proprietary databases. This approach enables us to conduct a thorough analysis of the market, aggregating industry-level insights. We delve into aspects like the number of global publishers active in the Maldives, resort-driven demand for NFTs, internet/mobile penetration, payment rails under the National Payment System Act, and regulatory conditions. We supplement this with detailed examinations of company-level data, relying on sources like press releases, annual reports, developer documentation, and financial statements. This process aims to construct a foundational understanding of both the market and the entities operating within it.

Step 3: Primary Research

We initiate a series of in-depth interviews with C-level executives and other stakeholders representing various Maldives NFT & Blockchain Gaming Market companies, resorts, liveaboards, and payment service providers. This interview process serves a multi-faceted purpose: to validate market hypotheses, authenticate statistical data, and extract valuable operational and financial insights from these industry representatives. A bottom-to-top approach is undertaken to evaluate revenue contributions for each player, thereby aggregating to the overall market. As part of our validation strategy, our team executes disguised interviews wherein we approach each company under the guise of potential clients. This approach enables us to validate the operational and financial information shared by company executives, corroborating this data against what is available in secondary databases. These interactions also provide us with a comprehensive understanding of revenue streams, value chains, processes, pricing, and other factors.

Step 4: Sanity Check

A bottom-to-top and top-to-bottom analysis along with market size modeling exercises is undertaken to assess the sanity of the process.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Maldives NFT & Blockchain Gaming Market holds significant potential, driven by the country’s strong tourism foundation and high digital adoption. With 2,050,000 international tourist arrivals recorded in the latest year and an internet penetration of ~84.7 users per 100 people, the environment is primed for resort-based NFT ticketing, tokenized experiences, and blockchain-enabled games. The potential is further enhanced by the Maldives’ premium positioning in global tourism, where high-spending guests are willing to engage with innovative digital experiences like loyalty NFTs, proof-of-experience collectibles, and play-to-earn gaming opportunities.

The Maldives NFT & Blockchain Gaming Market features several global key players accessible to residents, expats, and tourists. These include Sky Mavis (Axie Infinity), Animoca Brands (The Sandbox, Phantom Galaxies), Immutable, Gala Games, and The Sandbox. Other notable players shaping the ecosystem are Decentraland Foundation, Sorare, Mythical Games, Horizon Blockchain Games, Illuvium, Wemade (WEMIX), Netmarble (MARBLEX), Com2uS (XPLA), Yield Guild Games, and OpenSea. These companies dominate through strong IP partnerships, global liquidity, accessible custodial wallets, and SDKs that can integrate with Maldivian resorts, events, and tourism operators.

The primary growth drivers include macroeconomic and digital readiness factors. The Maldives recorded a GDP per capita of US$13,215.5 and GDP of US$6.98 billion, highlighting strong disposable income levels relative to its population of 527,799. The large volume of international arrivals (2.05 million) adds continuous new user funnels for resort-driven NFT activations. Moreover, mobile subscriptions stand at ~142 per 100 people, supporting seamless access to blockchain gaming through custodial and account abstraction wallets. These structural drivers combine to create a unique convergence of tourism demand, digital connectivity, and high-value customer cohorts.

The Maldives NFT & Blockchain Gaming Market faces distinct challenges. First, the geographic dispersion across atolls leads to uneven connectivity, despite high internet use, which affects real-time gameplay and NFT minting during peak tourist seasons. Second, the compliance burden under the National Payment System Act (Law No. 8/2021) and AML/CFT regulations means indie developers and small operators must rely heavily on licensed PSPs for fiat on-ramps and refunds, adding costs and complexity. Third, liquidity risks emerge in such a small domestic market, as venues and operators must link with global NFT marketplaces to sustain trading depth and player engagement.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500