Mexico Logistics and warehousing Market Outlook to 2029

By Market Structure (Organized vs Unorganized), By Mode of Transport (Road, Rail, Air, Sea), By Type of Warehousing (Industrial/Retail, Cold Storage, Container Freight, Agriculture), By End-Users (FMCG, Retail, E-commerce, Pharma, Automotive)

Report Overview

Report Code

TDR0293

Coverage

North America

Published

September 2025

Pages

80

On This Page

Report Overview

The report titled “Mexico Logistics and Warehousing Market Outlook to 2029 – By Market Structure (Organized vs Unorganized), By Mode of Transport (Road, Rail, Air, Sea), By Type of Warehousing (Industrial/Retail, Cold Storage, Container Freight, Agriculture), By End-Users (FMCG, Retail, E-commerce, Pharma, Automotive), and By Region” provides a comprehensive analysis of the logistics and warehousing market in Mexico.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Mexico Logistics and Warehousing Market Outlook to 2029 – By Market Structure (Organized vs Unorganized), By Mode of Transport (Road, Rail, Air, Sea), By Type of Warehousing (Industrial/Retail, Cold Storage, Container Freight, Agriculture), By End-Users (FMCG, Retail, E-commerce, Pharma, Automotive), and By Region” provides a comprehensive analysis of the logistics and warehousing market in Mexico. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation, key trends and developments, regulatory landscape, customer profiling, issues and challenges, and comparative landscape including competition scenario, cross-market comparison, opportunities and bottlenecks, and company profiling of major logistics and warehousing players. The report concludes with future market projections based on revenue, mode, warehousing type, regional distribution, causal analysis, and key success case studies.

Mexico Logistics and Warehousing Market Overview and Size

The Mexico logistics and warehousing market was valued at approximately MXN 1,200 Billion in 2023, driven by increasing international trade, a booming e-commerce sector, nearshoring opportunities, and rising demand for temperature-controlled warehousing. The market features both domestic and international players such as Estafeta, DHL Mexico, FedEx Express, Kuehne + Nagel, and Solistica, offering services ranging from last-mile delivery to cross-border freight and third-party logistics.

In 2023, the Mexican government launched the “Mexico Logistics Modernization Plan,” aimed at strengthening inland transport corridors and upgrading warehousing zones across central and northern Mexico. Industrial hubs such as Mexico City, Monterrey, and Guadalajara remain critical due to strong infrastructure, proximity to the U.S. border, and robust industrial base.

%252C%25202018%25E2%2580%25932023.png&w=640&q=75)

What Factors are Leading to the Growth of Mexico Logistics and Warehousing Market:

Nearshoring Boom: Amid global supply chain realignments, Mexico has emerged as a key nearshoring destination for U.S. firms. This has driven demand for integrated logistics solutions, leading to a surge in warehouse leasing in border cities like Tijuana, Ciudad Juárez, and Monterrey.

E-commerce Expansion: The rapid growth of platforms such as MercadoLibre, Amazon Mexico, and Walmart has led to a sharp rise in last-mile delivery and urban warehouse demand. E-commerce-related logistics accounted for nearly 20% of the warehousing demand in Mexico in 2023.

Infrastructure Investment: Public-private partnerships have led to infrastructure upgrades, including new rail links and intermodal terminals, enhancing connectivity between ports, industrial parks, and consumer centers.

Which Industry Challenges Have Impacted the Growth for Mexico Logistics and Warehousing Market

Infrastructure Bottlenecks: Despite ongoing investments, underdeveloped rural infrastructure and outdated port and rail systems continue to pose major logistical constraints. In 2023, over 30% of freight shipments experienced delays due to poor road conditions and congestion, especially around key border crossings like Nuevo Laredo and Tijuana. This affects time-sensitive deliveries and increases operational costs.

Fragmented Market Structure: The market remains fragmented, with a large share dominated by small and unorganized players lacking advanced technologies or scalability. Approximately 45% of logistics firms in Mexico operate with fewer than five trucks and no digital tracking systems, leading to inefficiencies and lack of transparency in services.

Security and Cargo Theft: High rates of cargo theft, especially along major highways such as those connecting Mexico City and Veracruz, have led to rising insurance premiums and reluctance among clients to transport high-value goods. In 2023, reported cargo theft incidents rose by 8% YoY, particularly targeting electronics, pharmaceuticals, and consumer goods.

What are the Regulations and Initiatives which have Governed the Market

Customs and Trade Facilitation: The Mexican government, through the SAT (Tax Administration Service), has accelerated the adoption of digital customs clearance platforms. These include electronic documentation, risk assessment tools, and bonded warehouse reforms. By 2023, over 60% of customs entries were processed digitally, significantly reducing border clearance times.

National Logistics Platform (PNLog): Launched in collaboration with the Secretariat of Communications and Transportation (SCT), this initiative aims to integrate logistics zones, inland terminals, and transportation networks across regions. Under the 2023 PNLog update, 15 new logistics corridors were proposed for seamless multimodal connectivity.

Warehouse Zoning and Compliance Regulations: Municipal governments, especially in urban centers like Guadalajara and Querétaro, have started enforcing zoning laws and safety norms for warehousing operations. In 2023, 18% of newly proposed warehouses in central Mexico faced delays due to non-compliance with environmental or construction guidelines.

Mexico Logistics and Warehousing Market Segmentation

By Market Structure: The unorganized segment continues to dominate the logistics landscape in Mexico, largely driven by small-scale transporters and independent warehousing providers who cater to regional and rural markets. These players offer cost-competitive services, local expertise, and flexibility in operations. However, the organized segment is rapidly gaining traction, particularly in urban and industrial zones, due to rising demand for end-to-end logistics, technology adoption (like WMS and TMS), and global compliance standards. Leading 3PL companies are capitalizing on the growing e-commerce and manufacturing sectors to scale operations and capture market share.

%252C%25202023.png&w=640&q=75)

By Mode of Transport: Road transport is the backbone of logistics in Mexico, accounting for the highest share due to the country’s extensive highway network and cross-border connectivity with the United States. It is especially vital for last-mile and intercity deliveries. Rail transport, though underutilized, is growing steadily with recent infrastructure upgrades. Sea freight is crucial for imports/exports via ports like Veracruz and Manzanillo, while air cargo is mainly used for high-value or time-sensitive shipments, such as electronics and pharmaceuticals.

%2520by%2520Revenue%2520Share%2520in%2520%2525%252C%25202023.png&w=640&q=75)

By Type of Warehousing: General industrial and retail warehousing constitutes the largest share of the market, serving fast-moving consumer goods (FMCG), electronics, and manufacturing. Cold storage facilities are on the rise, especially in northern Mexico, fueled by exports of perishables and demand from pharma clients. Container freight stations and bonded warehouses serve the port and border trade. Agricultural warehousing, although smaller in share, is gaining support through government programs for food security and grain storage.

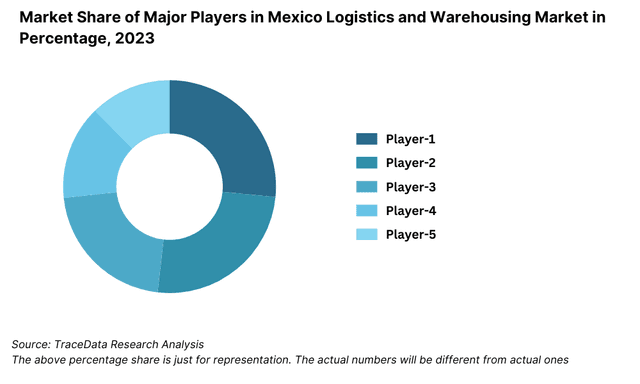

Competitive Landscape in Mexico Logistics and Warehousing Market

The Mexico logistics and warehousing market is moderately fragmented, with a mix of domestic and global players. Leading international logistics providers operate alongside strong local firms that leverage regional knowledge and networks. The rise of e-commerce, nearshoring, and industrial expansion has encouraged both traditional logistics firms and tech-driven startups to innovate and expand their service offerings.

Company | Establishment Year | Headquarters |

Estafeta | 1979 | Mexico City, Mexico |

DHL Mexico | 1969 (Global) | Mexico City, Mexico |

FedEx Express | 1971 (Global) | Memphis, USA / Mexico Ops |

Kuehne + Nagel | 1890 (Global) | Schindellegi, Switzerland |

Solistica | 2003 | Monterrey, Mexico |

Traxión | 2011 | Mexico City, Mexico |

Envía | 2005 | Monterrey, Mexico |

99minutos | 2013 | Mexico City, Mexico |

Some of the recent competitor trends and key information about competitors include:

Estafeta: A leading national courier and logistics provider, Estafeta expanded its warehousing capacity by 12% in 2023, especially in central and northern Mexico. It operates over 1,000 delivery routes and has been investing in automation and fleet electrification to improve sustainability and delivery speeds.

DHL Mexico: Part of Deutsche Post DHL Group, DHL has significantly expanded its footprint in Mexico, opening two new distribution hubs in 2023 to support the e-commerce surge. DHL's cross-border logistics services remain strong, particularly with U.S.-bound shipments from border states.

FedEx Express: FedEx Mexico continues to grow in B2B logistics and SME solutions. In 2023, it launched its "FedEx Delivery Manager" for Mexico, offering flexible delivery scheduling and package redirection, a move aimed at improving the last-mile experience.

Kuehne + Nagel: A dominant player in sea and air freight forwarding, K+N has increased its cold chain capacity in Mexico to serve pharmaceutical and perishables clients. Its Guadalajara facility was upgraded in 2023 with advanced temperature monitoring systems.

Solistica: A subsidiary of FEMSA, Solistica focuses on integrated logistics and 3PL services, especially for the beverage and retail sectors. The company introduced a predictive analytics platform in 2023 to optimize route planning and warehouse utilization.

Traxión: Known for its asset-heavy model, Traxión operates over 9,000 vehicles and saw double-digit revenue growth in 2023, driven by its e-commerce fulfillment and dedicated logistics services. The company is also investing in digital freight matching platforms.

Envía: A regional logistics provider, Envía expanded into express last-mile services across northeast Mexico in 2023. Its competitive pricing and flexible delivery options make it a preferred choice for regional e-commerce businesses.

99minutos: A last-mile delivery startup focusing on ultra-fast shipping, 99minutos reported a 40% increase in parcel volume in 2023. The company expanded its "same-day" delivery promise to over 20 Mexican cities, supported by micro-warehousing and local delivery partners.

What Lies Ahead for Mexico Logistics and Warehousing Market?

The Mexico logistics and warehousing market is projected to grow steadily through 2029, driven by the rise of e-commerce, nearshoring trends, and increasing investments in logistics infrastructure. The market is expected to witness a robust CAGR as Mexico strengthens its role as a strategic trade and manufacturing hub for North America.

Accelerated Nearshoring Opportunities: As global manufacturers increasingly shift supply chains closer to the U.S., Mexico stands to benefit from growing demand for industrial warehousing, cross-border trucking, and intermodal transport. Border cities like Tijuana, Reynosa, and Ciudad Juárez are expected to experience a surge in new warehousing projects and 3PL partnerships.

Technology Integration in Logistics: Advanced technologies such as warehouse management systems (WMS), IoT-enabled tracking, and AI-powered route optimization are expected to become mainstream by 2029. These technologies will significantly enhance supply chain visibility, reduce delivery times, and improve inventory management.

Expansion of E-commerce Fulfillment Infrastructure: With online retail growth continuing, there will be a sharp rise in demand for fulfillment centers and urban logistics hubs. By 2029, same-day and next-day delivery models are anticipated to become standard in Tier-1 cities like Mexico City, Guadalajara, and Monterrey.

Cold Chain Infrastructure Growth: Increasing demand from food exports, pharmaceuticals, and vaccine logistics will drive investments in temperature-controlled warehousing. The cold chain segment is expected to grow at a double-digit CAGR, especially in central and northern Mexico.

%252C%25202023-2029.png&w=640&q=75)

Mexico Logistics and Warehousing Market Segmentation

• By Market Structure:

o Organized Sector

o Unorganized Sector

o Third-Party Logistics (3PL) Providers

o Freight Forwarders

o Last-Mile Delivery Companies

o Multimodal Transport Operators

• By Mode of Transport:

o Road

o Rail

o Air

o Sea

• By Type of Warehousing:

o Industrial and Retail Warehousing

o Cold Storage Warehousing

o Container Freight Stations (CFS)

o Agricultural Warehousing

o E-commerce Fulfillment Centers

o Bonded Warehouses

• By End-User Industry:

o FMCG

o Retail

o E-commerce

o Automotive

o Pharmaceuticals and Healthcare

o Electronics and Consumer Durables

o Agriculture and Food Processing

• By Region:

o Northern Mexico (e.g., Monterrey, Tijuana, Ciudad Juárez)

o Central Mexico (e.g., Mexico City, Querétaro, Puebla)

o Western Mexico (e.g., Guadalajara, Jalisco)

o Eastern Mexico (e.g., Veracruz, Tamaulipas)

o Southern Mexico (e.g., Oaxaca, Chiapas, Yucatán Peninsula)

Players Mentioned in the Report:

• Estafeta

• DHL Mexico

• FedEx Express

• Kuehne + Nagel

• Solistica

• Traxión

• Envía

• 99minutos

Key Target Audience:

• Logistics Service Providers (3PLs, freight forwarders)

• E-commerce and Retail Companies

• Industrial Real Estate Developers

• Cold Chain Operators

• Supply Chain and Warehouse Technology Vendors

• Regulatory Authorities (e.g., Secretaría de Comunicaciones y Transportes – SCT, SAT)

• Trade Promotion Bodies

• Investment and Infrastructure Planners

Time Period:

• Historical Period: 2018–2023

• Base Year: 2024

• Forecast Period: 2024–2029

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Table of Contents

1. Executive Summary

2. Research Methodology

3. Ecosystem of Key Stakeholders in Mexico Logistics and Warehousing Market

4. Value Chain Analysis

4.1. Value Chain Process-Role of Entities, Stakeholders, and Challenges They Face

4.2. Revenue Streams for Mexico Logistics and Warehousing Market

4.3. Business Model Canvas for Mexico Logistics and Warehousing Market

4.4. Demand Decision-Making Process (End-Users)

4.5. Supply Decision-Making Process (Logistics Service Providers)

5. Market Structure

5.1. Logistics Spend as % of GDP in Mexico, 2018-2024

5.2. Share of Transport, Warehousing, and Value-Added Services, 2018-2024

5.3. Organized vs Unorganized Market Penetration by Region, 2024

5.4. Warehousing Space Available and Utilized by Region, 2024

6. Market Attractiveness for Mexico Logistics and Warehousing Market

7. Supply-Demand Gap Analysis

8. Market Size for Mexico Logistics and Warehousing Market Basis

8.1. Revenue, 2018-2024

8.2. Warehousing Space (in Mn Sq. Ft.), 2018-2024

8.3. Freight Volume (in Million Tons), 2018-2024

9. Market Breakdown for Mexico Logistics and Warehousing Market Basis

9.1. By Market Structure (Organized and Unorganized), 2023-2024P

9.2. By Mode of Transport (Road, Rail, Air, Sea), 2023-2024P

9.3. By Type of Warehousing (Industrial/Retail, Cold Storage, CFS, Agri, Fulfillment Centers), 2023-2024P

9.4. By Region (North, Central, West, East, South), 2023-2024P

9.5. By End-User Industry (FMCG, Retail, E-commerce, Pharma, Auto, Agri, Others), 2023-2024P

9.6. By Shipment Type (Full Truck Load, Less than Truck Load, Express, Others), 2023-2024P

10. Demand Side Analysis for Mexico Logistics and Warehousing Market

10.1. Industry-Wise Logistics Spend and Behavior

10.2. Outsourcing Trends and Challenges

10.3. Logistics Selection Criteria and Preferences

10.4. Pain Point Analysis and Unmet Needs

11. Industry Analysis

11.1. Trends and Developments in Mexico Logistics and Warehousing Market

11.2. Growth Drivers for Mexico Logistics and Warehousing Market

11.3. SWOT Analysis for Mexico Logistics and Warehousing Market

11.4. Issues and Challenges in Mexico Logistics and Warehousing Market

11.5. Government Policies and Regulations Affecting the Sector

12. Snapshot on E-commerce Fulfillment and Last-Mile Logistics

12.1. Market Size and Future Potential, 2018-2029

12.2. Key Players and Operating Models

12.3. Tech Innovations in Fulfillment and Last-Mile Delivery

13. Cold Chain Logistics Market in Mexico

13.1. Market Size, CAGR, and Drivers, 2018-2029

13.2. End-Use Segmentation (Food, Pharma, etc.)

13.3. Cold Storage Capacity by Region and Utilization

13.4. Competitive Landscape and Best Practices

14. Opportunity Matrix for Mexico Logistics and Warehousing Market-Radar Chart Representation

15. PEAK Matrix for Competitive Positioning of Logistics Players in Mexico

16. Competitor Analysis for Mexico Logistics and Warehousing Market

16.1. Benchmark of Key Players-Overview, Services, Footprint, Revenue, Fleet Size, Warehousing Space, Technology Use

16.2. Strengths and Weaknesses

16.3. Operating Model Analysis Framework

16.4. Gartner Magic Quadrant Positioning

16.5. Bowman’s Strategic Clock-Competitive Advantage Strategy

17. Future Market Size for Mexico Logistics and Warehousing Market Basis

17.1. Revenue Projections, 2025-2029

17.2. Warehousing Space Demand, 2025-2029

17.3. Freight Volume Growth, 2025-2029

18. Market Breakdown for Mexico Logistics and Warehousing Market Basis

18.1. By Market Structure (Organized and Unorganized), 2025-2029

18.2. By Mode of Transport (Road, Rail, Air, Sea), 2025-2029

18.3. By Type of Warehousing (Industrial/Retail, Cold, Fulfillment, Others), 2025-2029

18.4. By Region (North, Central, West, East, South), 2025-2029

18.5. By End-User Industry (FMCG, Retail, E-commerce, Pharma, Auto, Others), 2025-2029

18.6. By Shipment Type, 2025-2029

18.7. Recommendations and Key Strategic Moves

18.8. Opportunity Analysis by Segment and Region

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities for the Mexico Logistics and Warehousing Market. Based on this ecosystem, we shortlist the leading 5–6 logistics and warehousing players in the country based on their revenue, fleet size, warehouse footprint, and technological adoption.

Sourcing is conducted through industry articles, syndicated research, trade databases, government logistics reports, and proprietary platforms to perform desk research and collect industry-level data.

Step 2: Desk Research

We engage in an exhaustive desk research process by referencing diverse secondary and proprietary databases such as industry publications, annual trade reports, government bulletins (e.g., SCT, SAT), news articles, and company filings. This process helps gather insights on revenue segmentation, logistics infrastructure, warehousing capacity, mode-wise transportation shares, and geographic coverage.

Further analysis is conducted at the company level, including press releases, investor presentations, M&A reports, and other financial documents to build an understanding of major players’ strategies and operational metrics.

Step 3: Primary Research

We conduct structured interviews with CXOs, supply chain heads, facility managers, and other stakeholders from logistics firms, warehousing companies, 3PL providers, and end-user industries such as e-commerce, FMCG, and automotive. These interviews help validate hypotheses, confirm quantitative findings, and reveal qualitative insights on operational dynamics.

To enhance accuracy, disguised interviews are performed wherein researchers approach firms as potential clients or partners. This allows us to cross-check the validity of data shared by executives with actual operational realities, including warehouse capacity utilization, fleet operations, rate cards, and client acquisition strategies.

We adopt a bottom-up approach to estimate the logistics and warehousing revenue for each player and scale it up to arrive at the overall market size. This is further cross-verified through a top-down triangulation method.

Step 4: Sanity Check

- A combined top-down and bottom-up modeling framework is applied to ensure accuracy and consistency in market sizing. Various economic indicators (e.g., trade volumes, manufacturing output, retail sales) and segment-specific benchmarks (e.g., warehousing demand per sq. ft per industry) are used to validate final figures and growth projections.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Mexico logistics and warehousing market holds strong growth potential, reaching an estimated value of MXN 1,200 Billion in 2023. This momentum is supported by Mexico’s strategic location for nearshoring, growing e-commerce demand, and government-backed infrastructure development. The sector is poised to grow steadily through 2029, driven by supply chain realignment, improved multimodal connectivity, and rising demand for value-added logistics services.

Key players include both global and domestic firms such as Estafeta, DHL Mexico, FedEx Express, Kuehne + Nagel, Solistica, Traxión, and 99minutos. These companies are recognized for their robust logistics networks, technology-enabled operations, and sector-specific service offerings that cater to retail, e-commerce, automotive, and healthcare industries.

The primary growth drivers include Mexico’s growing role as a nearshoring hub for North American supply chains, the boom in e-commerce requiring advanced fulfillment infrastructure, and increasing demand for cold storage and temperature-controlled logistics. Public-private investments in transportation infrastructure and digital customs reforms further contribute to market expansion.

Challenges include infrastructure gaps in rural and border areas, high rates of cargo theft along key routes, and market fragmentation with a large share of unorganized players. Regulatory complexities and compliance costs for warehouse operators can also impact smaller firms. In addition, ensuring sustainability and scalability amidst growing demand remains a key concern for market players.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500