Netherlands Auto Finance Market Outlook to 2029

By Market Structure, By Loan Providers, By Vehicle Type, By Consumer Age Group, By Financing Tenure and By Region

Report Overview

Report Code

TDR0168

Coverage

Europe

Published

May 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Netherlands Auto Finance Market Outlook to 2029 – By Market Structure, By Loan Providers, By Vehicle Type, By Consumer Age Group, By Financing Tenure and By Region” provides a comprehensive analysis of the auto finance industry in the Netherlands. The report covers the overview and genesis of the industry, overall market size in terms of disbursed loans, market segmentation, key trends and developments, regulatory landscape, customer behavior analysis, challenges, and the competitive landscape, including cross-comparison, opportunities and bottlenecks, and company profiling of major players in the Auto Finance Market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Netherlands Auto Finance Market Outlook to 2029 – By Market Structure, By Loan Providers, By Vehicle Type, By Consumer Age Group, By Financing Tenure and By Region” provides a comprehensive analysis of the auto finance industry in the Netherlands. The report covers the overview and genesis of the industry, overall market size in terms of disbursed loans, market segmentation, key trends and developments, regulatory landscape, customer behavior analysis, challenges, and the competitive landscape, including cross-comparison, opportunities and bottlenecks, and company profiling of major players in the Auto Finance Market. The report concludes with future market projections based on disbursed loan value, segmentation by provider type, vehicle type, consumer demographics, cause-and-effect relationships, and success case studies highlighting major opportunities and potential risks.

Netherlands Auto Finance Market Overview and Size

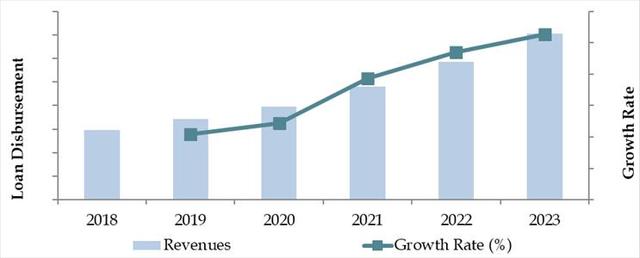

The Netherlands auto finance market reached a valuation of EUR 19.5 Billion in 2023, driven by rising vehicle ownership, an increasing preference for financing over outright purchases, and the expansion of digital lending platforms. Key players such as ALFAM, ABN AMRO, ING Lease, Volkswagen Pon Financial Services, and Santander Consumer Finance dominate the market with strong digital capabilities, competitive interest rates, and robust partnerships with car dealerships across the country.

In 2023, ABN AMRO expanded its digital auto loan offerings to include AI-driven credit assessments, significantly reducing processing time. Major urban centers like Amsterdam, Rotterdam, and Utrecht remain focal points of auto loan disbursement due to their high car ownership rates and well-developed transportation ecosystems.

Market Size for Netherlands Auto Finance Industry on the Basis of Loan Disbursed, 2018–2023

What Factors are Leading to the Growth of Netherlands Auto Finance Market:

Affordability & Inflationary Pressures: Rising car prices, coupled with broader inflation trends, have prompted consumers to seek financing options rather than outright purchases. As of 2023, approximately 72% of new car purchases and 54% of used car purchases in the Netherlands were financed, reflecting a strong reliance on loan services.

Digital Financing Ecosystem: The Dutch market has seen a rapid digitization of financial services. In 2023, over 60% of auto finance applications were processed through digital platforms. Consumers increasingly value the convenience of comparing loan options, completing paperwork, and receiving approvals entirely online.

Shift Towards Electric Vehicles (EVs): Government incentives and environmental awareness have accelerated the adoption of EVs, many of which are financed due to their higher upfront costs. Finance providers have begun offering EV-specific loan products with longer tenures and lower interest rates, further stimulating growth.

Which Industry Challenges Have Impacted the Growth for Netherlands Auto Finance Market

Rising Interest Rates:As the European Central Bank implemented monetary tightening measures, borrowing costs have risen. In 2023, the average auto loan interest rate in the Netherlands increased to 5.2%, compared to 3.8% in 2021. This has discouraged some consumers from financing vehicle purchases, particularly in lower income brackets. Industry analysts estimate that the increased rates led to a 7–9% drop in loan applications year-over-year.

Strict Credit Approval Norms: Dutch financial institutions follow conservative credit assessment protocols, which limit access to auto loans for young adults, freelancers, and recent immigrants. Around 29% of declined applications in 2023 were due to insufficient credit history or irregular income, affecting market inclusivity and growth potential.

Data Privacy Concerns: With growing reliance on digital platforms and AI-powered assessments, consumer concerns about the use and storage of personal financial data have emerged. A recent survey showed that 41% of auto loan customers expressed unease about how their data is managed, especially among younger demographics. These concerns can delay or discourage online loan adoption.

What are the Regulations and Initiatives which have Governed the Market:

Consumer Credit Protection Regulations: The Dutch Authority for the Financial Markets (AFM) mandates strict consumer protection guidelines for auto financing. These include caps on maximum interest rates, clear disclosure of total loan costs, and the right to early repayment without penalties. In 2023, over 85% of financing agreements complied with the updated transparency standards, boosting borrower confidence.

Sustainable Mobility Initiatives: The Netherlands government actively supports low-emission mobility through programs such as the “SEPP” (Subsidie Elektrische Personenauto's Particulieren) scheme. This includes subsidies for electric vehicle purchases and associated financing. In 2023, nearly €85 million was allocated under SEPP, contributing to a 22% year-over-year increase in EV auto loans.

PSD2 and Open Banking Framework: Under the EU’s Revised Payment Services Directive (PSD2), Dutch lenders can access verified financial data to make faster, more accurate loan decisions. This has improved risk assessment but also raised compliance demands. By 2023, nearly 65% of auto loan approvals were based on open banking data integrations, reducing manual underwriting time by over 40%.

Netherlands Auto Finance Market Segmentation

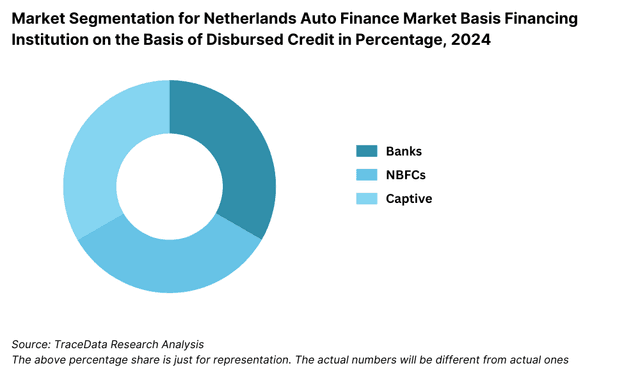

By Market Structure: Bank-led financing dominates the Netherlands auto finance market, driven by the strong presence of major banks like ABN AMRO, ING, and Rabobank. These institutions offer competitive interest rates, long-standing trust, and a wide range of flexible loan products. Captive finance companies—such as Volkswagen Pon Financial Services and Stellantis Financial Services—hold a notable share due to their direct ties with automotive brands, enabling tailored financing deals, promotional offers, and bundled services. Non-bank lenders and digital-only platforms have gained traction among tech-savvy consumers, offering faster processing times and simplified application procedures.

By Vehicle Type: New cars account for the majority of financed vehicles due to manufacturer incentives and promotional financing rates, especially in the electric vehicle (EV) segment. Consumers prefer financing new EVs given their high upfront costs. Used car financing is also expanding, particularly among younger consumers and those seeking affordability. In 2023, used vehicles made up approximately 35–40% of total auto loans disbursed.

.png&w=640&q=75)

By Consumer Age Group: Individuals aged 30–45 represent the largest segment of auto finance users, owing to their financial stability and higher purchasing power. However, there's a rising trend among younger consumers (20–29) accessing digital platforms for used car loans and subscription models. Meanwhile, the 50+ demographic favors traditional banking channels and is more likely to finance higher-end vehicles.

Competitive Landscape in Netherlands Auto Finance Market

The Netherlands auto finance market is moderately concentrated, with established banks and captive finance companies holding significant market share. However, the rise of fintech lenders and digital-first platforms is reshaping the competitive dynamics, offering faster, tech-enabled financing solutions. Key players include ALFAM (a subsidiary of ABN AMRO), ING Lease, Volkswagen Pon Financial Services, Santander Consumer Finance, DirectLease, and AutoFinanciering.nl.

| Company Name | Founding Year | Original Headquarters |

| LeasePlan Corporation N.V. | 1963 | Amsterdam, Netherlands |

| DLL Group (De Lage Landen) | 1969 | Eindhoven, Netherlands |

| Santander Consumer Finance Benelux | 2004 | Utrecht, Netherlands |

| CA Auto Finance Nederland B.V. | 1969 | Amsterdam, Netherlands |

| Toyota Motor Finance Netherlands | 2000 | Amsterdam, Netherlands |

| Arval BNP Paribas Netherlands | 1989 | Rueil-Malmaison, France |

| Volkswagen Financial Services | 1948 | Braunschweig, Germany |

| ING Group | 1991 | Amsterdam, Netherlands |

| Credit Europe Bank N.V. | 1994 | Amsterdam, Netherlands |

| Auto.nl | 2011 | Amsterdam, Netherlands |

Some of the recent competitor trends and key information about competitors include:

ALFAM (ABN AMRO): A major player in consumer lending, ALFAM introduced an AI-powered risk assessment system in 2023 that reduced loan approval time by 30%. The company financed over €2.3 billion in auto loans last year, with a strong presence in both new and used vehicle segments.

ING Lease: Known for its focus on sustainable mobility, ING Lease saw a 27% year-over-year increase in financing for electric vehicles (EVs). Its flexible green leasing options have attracted environmentally conscious consumers and fleet buyers.

Volkswagen Pon Financial Services: As a captive finance company, VW Pon Financial Services reported a 15% growth in dealer-linked financing in 2023. It remains a leader in new car financing, especially for VW, Audi, SEAT, and Škoda models in the Netherlands.

Santander Consumer Finance: With a focus on retail auto lending, Santander launched a fully digital loan processing system in 2023, driving a 20% increase in online loan applications. Its partnership with multiple dealerships has strengthened its omnichannel reach.

DirectLease: A pioneer in online leasing, DirectLease expanded its B2C offerings in 2023 with simplified contracts and no-deposit deals. The company saw 18% growth in short-term leases, appealing to younger, urban customers.

AutoFinanciering.nl: This fintech startup gained momentum with its instant loan comparison engine. In 2023, it saw a 35% increase in loan inquiries, driven by its transparent pricing and user-friendly digital platform.

What Lies Ahead for Netherlands Auto Finance Market?

The Netherlands auto finance market is projected to continue its upward trajectory through 2029, with a stable CAGR supported by digital innovation, increased EV adoption, and evolving consumer financing behavior. Structural shifts in mobility preferences, combined with supportive government policies, will play a key role in shaping the market's growth.

Acceleration in Electric Vehicle Financing: As the Netherlands intensifies its push for carbon neutrality, the demand for electric vehicles (EVs) is expected to surge. This will directly impact auto finance, with lenders introducing EV-specific financing solutions, such as lower interest rates, extended tenures, and bundled charging infrastructure packages. By 2029, EVs could account for over 50% of all new vehicle financing deals in the country.

Advancement of AI and Open Banking: The integration of AI algorithms and open banking protocols (PSD2) will revolutionize risk profiling, enabling near-instantaneous credit decisions and customized loan offerings. This will reduce default rates while expanding credit access to underserved segments. By leveraging consumer consented data, lenders will offer smarter, more flexible products tailored to individual financial behaviors.

Growth of Subscription and Lease-to-Own Models: Changing attitudes towards car ownership—especially among younger consumers—will drive demand for subscription-based financing and lease-to-own structures. These models allow greater flexibility and lower upfront costs, aligning with a growing preference for usage over ownership. Auto financiers will diversify into mobility-as-a-service (MaaS) offerings to stay competitive.

Stronger Emphasis on ESG and Green Financing: Financial institutions in the Netherlands are increasingly integrating Environmental, Social, and Governance (ESG) criteria into their lending practices. This will lead to greater promotion of green auto finance products, including incentives for low-emission vehicles, carbon-neutral leasing programs, and partnerships with sustainability-focused automakers.

Future Outlook and Projections for Netherlands Car Finance Market Size on the Basis of Loan Disbursements in USD Billion, 2024-2029

Netherlands Auto Finance Market Segmentation

• By Market Structure:

o Bank-led Financing

o Captive Finance Companies

o Online-Only Lending Platforms

o Dealership Financing

o Independent Financial Brokers

o Peer-to-Peer Lending Platforms

• By Vehicle Type:

o New Vehicles

o Used Vehicles

o Electric Vehicles (EVs)

o Hybrid Vehicles

o Commercial Vehicles

• By Loan Provider:

o ALFAM (ABN AMRO)

o ING Lease

o Santander Consumer Finance

o Volkswagen Pon Financial Services

o DirectLease

o AutoFinanciering.nl

• By Consumer Age Group:

o 18–29

o 30–45

o 46–60

o 60+

• By Financing Tenure:

o 12–24 Months

o 25–36 Months

o 37–60 Months

o 60+ Months

• By Region:

o Randstad (Amsterdam, Rotterdam, The Hague, Utrecht)

o North Brabant

o Gelderland

o Limburg

o Friesland & Groningen

o Zeeland & Drenthe

Players Mentioned in the Report (Banks):

- ABN AMRO

- ING Bank

- Rabobank

- SNS Bank

- Nationale-Nederlanden Bank

- InterBank

Players Mentioned in the Report (NBFCs):

- DLL Group

- TrueNoord

- Home Credit Group

- Lendahand

- Factris

- CreditAccess Asia

Players Mentioned in the Report (Captive):

- Volkswagen Financial Services Netherlands

- BMW Financial Services Netherlands

- Mercedes-Benz Financial Services Netherlands

- Toyota Financial Services Netherlands

- Ford Credit Netherlands

- Volvo Financial Services

- Stellantis Financial Services Netherlands

Key Target Audience:

• Auto Financing Institutions

• Banks and Credit Unions

• Automotive Dealerships

• Regulatory Bodies (e.g., Dutch Authority for the Financial Markets – AFM)

• Digital Lending Startups and Fintechs

• Research and Policy Organizations

• Electric Vehicle Manufacturers

Time Period:

• Historical Period: 2018–2023

• Base Year: 2024

• Forecast Period: 2024–2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-Role of Entities, Stakeholders, and challenges they face.

4.2. Relationship and Engagement Model between Banks-Dealers, NBFCs-Dealers and Captive-Dealers-Commission Sharing Model, Flat Fee Model and Revenue streams

5.1. New Car and Used Car Sales in Netherlands by type of vehicle, 2018-2024

8.1. Credit Disbursed, 2018-2024

8.2. Outstanding Loan, 2018-2024

9.1. By Market Structure (Bank-Owned, Multi-Finance, and Captive Companies), 2023-2024

9.2. By Vehicle Type (Passenger, Commercial and EV), 2023-2024

9.3. By Region, 2023-2024

9.4. By Type of Vehicle (New and Used), 2023-2024

9.5. By Average Loan Tenure (0-2 years, 3-5 years, 6-8 years, above 8 years), 2023-2024

10.1. Customer Landscape and Cohort Analysis

10.2. Customer Journey and Decision-Making

10.3. Need, Desire, and Pain Point Analysis

10.4. Gap Analysis Framework

11.1. Trends and Developments for Netherlands Car Finance Market

11.2. Growth Drivers for Netherlands Car Finance Market

11.3. SWOT Analysis for Netherlands Car Finance Market

11.4. Issues and Challenges for Netherlands Car Finance Market

11.5. Government Regulations for Netherlands Car Finance Market

12.1. Market Size and Future Potential for Online Car Financing Aggregators, 2018-2029

12.2. Business Model and Revenue Streams

12.3. Cross Comparison of Leading Digital Car Finance Companies Based on Company Overview, Revenue Streams, Loan Disbursements/Number of Leads Generated, Operating Cities, Number of Branches, and Other Variables

13.1. Finance Penetration Rate and Average Down Payment for New and Used Cars, 2018-2029

13.2. How Finance Penetration Rates are Changing Over the Years with Reasons

13.3. Type of Car Segment for which Finance Penetration is Higher

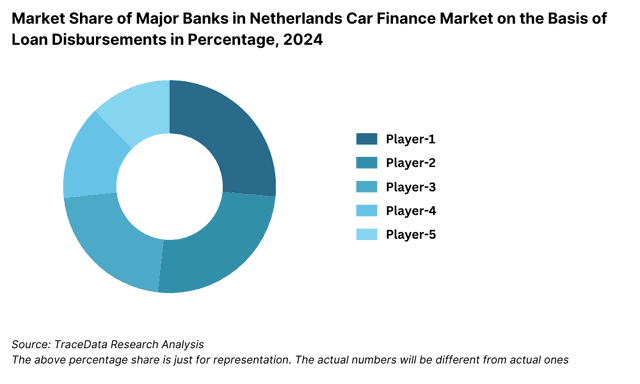

17.1. Market Share of Key Banks in Netherlands Car Finance Market, 2024

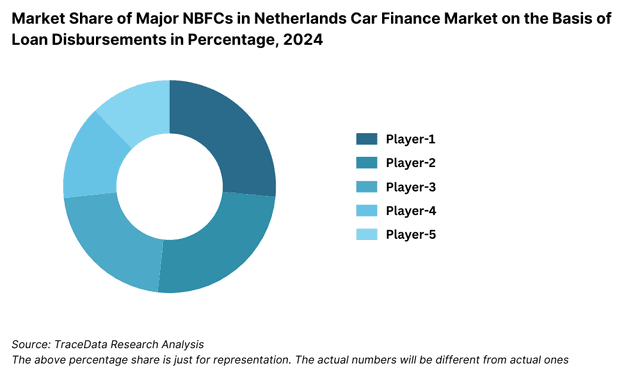

17.2. Market Share of Key NBFCs in Netherlands Car Finance Market, 2024

17.3. Market Share of Key Captive in Netherlands Car Finance Market, 2024

17.4. Benchmark of Key Competitors in Netherlands Car Finance Market, including Variables such as Company Overview, USP, Business Strategies, Strengths, Weaknesses, Business Model, Number of Branches, Product Features, Interest Rate, NPA, Loan Disbursed, Outstanding Loans, Tie-Ups and others

17.5. Strengths and Weaknesses

17.6. Operating Model Analysis Framework

17.7. Gartner Magic Quadrant

17.8. Bowmans Strategic Clock for Competitive Advantage

18.1. Credit Disbursed, 2025-2029

18.2. Outstanding Loan, 2025-2029

19.1. By Market Structure (Bank-Owned, Multi-Finance, and Captive Companies), 2025-2029

19.2. By Vehicle Type (Passenger, Commercial and EV), 2025-2029

19.3. By Region, 2025-2029

19.4. By Type of Vehicle (New and Used), 2025-2029

19.5. By Average Loan Tenure (0-2 years, 3-5 years, 6-8 years, above 8 years), 2025-2029

19.6. Recommendations

19.7. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side (consumers, dealerships) and supply-side entities (banks, captive finance companies, online lenders) for the Netherlands Auto Finance Market. Based on this ecosystem, we shortlist the leading 5–6 auto finance providers in the country by evaluating their financial information, loan disbursement volumes, and market reach.

Sourcing is done through industry articles, government publications, automotive finance portals, and multiple secondary and proprietary databases to perform initial desk research and gather market-level information.

Step 2: Desk Research

We conduct extensive desk research using a combination of secondary and proprietary databases. This allows for a comprehensive analysis of the market, including data on loan volumes, interest rates, market players, vehicle financing penetration, and consumer trends.

We gather company-level insights from financial reports, investor presentations, media articles, and official websites. This step builds the foundation for understanding market performance, pricing trends, segment contributions, and key competitor strategies.

Step 3: Primary Research

A series of in-depth interviews are carried out with executives from leading Dutch banks, leasing companies, online loan platforms, automotive dealerships, and regulatory experts. These conversations serve to validate desk research findings, fill data gaps, and capture granular insights about operational models, financing structures, and future outlooks.

As part of our validation process, we conduct disguised interviews posing as prospective customers to independently verify pricing, approval processes, and credit terms. This bottom-up approach helps triangulate volume estimates and obtain authentic market intelligence across consumer, dealer, and financier levels.

Step 4: Sanity Check

- We use both bottom-up and top-down modeling techniques to verify consistency across multiple data points. This involves triangulating findings from primary interviews, secondary research, and company financials to confirm the reliability of overall market sizing, growth projections, and segment-level analysis. Sanity checks ensure that forecasts and insights are aligned with historical trends and realistic market assumptions.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Netherlands Auto Finance Market is set for consistent growth through 2029, reaching an estimated loan disbursement value of EUR 19.5 billion in 2023. This growth is driven by rising vehicle ownership, increasing electric vehicle (EV) adoption, and a strong shift toward digital lending platforms. The market's potential is further enhanced by government incentives, evolving consumer financing behavior, and innovations in AI-driven risk assessment and open banking integrations.

Key players in the Netherlands Auto Finance Market include ALFAM (a subsidiary of ABN AMRO), ING Lease, Volkswagen Pon Financial Services, Santander Consumer Finance, DirectLease, and AutoFinanciering.nl. These companies hold strong market positions due to their robust loan portfolios, strategic dealer partnerships, and digital transformation efforts.

Growth is fueled by several factors, including the increased financing of electric and hybrid vehicles, growing consumer preference for flexible ownership models like leasing and subscriptions, and the rise of digital-first platforms enabling quick, seamless loan approvals. Additionally, government subsidies for EVs and strong ESG (Environmental, Social, Governance) alignment among financial institutions are propelling market expansion.

The market faces key challenges such as rising interest rates, which impact borrowing affordability, and strict credit approval norms, which restrict access for younger or freelance workers. Data privacy concerns related to digital lending and compliance burdens from open banking and PSD2 regulations also present hurdles. Furthermore, the transition to EV financing requires product innovation to accommodate higher upfront vehicle costs.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0