New Zealand Auto Finance Market Outlook to 2029

By Loan Types, By Vehicle Type, By Lender Category, By Consumer Demographics, and By Region

Report Overview

Report Code

TDR0134

Coverage

Asia

Published

April 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “New Zealand Auto Finance Market Outlook to 2029 - By Loan Types, By Vehicle Type, By Lender Category, By Consumer Demographics, and By Region” provides a comprehensive analysis of the auto finance market in New Zealand. The report covers an overview and genesis of the industry, overall market size in terms of loan disbursements, market segmentation, trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the auto finance market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “New Zealand Auto Finance Market Outlook to 2029 - By Loan Types, By Vehicle Type, By Lender Category, By Consumer Demographics, and By Region” provides a comprehensive analysis of the auto finance market in New Zealand. The report covers an overview and genesis of the industry, overall market size in terms of loan disbursements, market segmentation, trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the auto finance market. The report concludes with future market projections based on loan disbursements, by market segments, financial institutions, regional impact, cause and effect relationships, and success case studies highlighting the major opportunities and cautions.

New Zealand Auto Finance Market Overview and Size

The New Zealand auto finance market reached a valuation of NZD 15 Billion in 2023, driven by the increasing adoption of vehicle financing, growing preference for new and used cars, and rising disposable incomes. The market is characterized by major financial institutions such as ANZ, Westpac, ASB Bank, BNZ, and specialized auto lenders like UDC Finance and Heartland Bank. These institutions are known for their extensive loan portfolios, competitive interest rates, and customer-centric services.

In 2023, BNZ introduced a new digital auto loan application platform, simplifying the lending process and enhancing customer convenience. This initiative aligns with the growing digitalization trend in New Zealand’s financial sector and caters to the increasing preference for online banking and financial transactions. Auckland and Wellington remain key markets due to their high vehicle ownership rates and economic activity.

Market Size for New Zealand Auto Finance Industry Size on the Basis of Credit Disbursements in USD Billion, 2018-2024

What Factors are Leading to the Growth of the New Zealand Auto Finance Market

Economic Factors: The rise in per capita income and a stable economic environment have encouraged consumers to opt for auto financing. In 2023, approximately 70% of vehicle purchases in New Zealand were financed through loans, highlighting the reliance on credit for car ownership.

Growing Urbanization: As urban populations increase, demand for personal vehicles has grown, further fueling the need for auto financing. Urban centers such as Auckland, Christchurch, and Wellington have witnessed a surge in vehicle ownership, boosting the auto finance market.

Digitalization of Financial Services: The emergence of digital lending platforms has simplified the loan application and approval process. In 2023, over 45% of auto loan applications in New Zealand were processed through digital channels, reflecting the shift towards online financial services.

Which Industry Challenges Have Impacted the Growth of the New Zealand Auto Finance Market

Interest Rate Volatility: Fluctuations in interest rates impact borrowing costs, making auto loans less attractive during high-interest periods. In 2023, the Reserve Bank of New Zealand’s monetary policy adjustments led to variable interest rates, affecting auto loan affordability.

Stringent Regulatory Requirements: The New Zealand government has implemented stricter lending regulations to ensure responsible borrowing. These regulations, while protecting consumers, have also increased compliance costs for financial institutions.

Credit Accessibility Issues: Limited credit history or lower credit scores remain barriers for some consumers, particularly younger buyers and new immigrants. Data indicates that around 30% of potential borrowers face difficulties securing financing due to credit constraints.

What are the Regulations and Initiatives Which Have Governed the Market

Vehicle Financing Regulations: The New Zealand government mandates responsible lending standards, ensuring that consumers are not burdened with unmanageable debt. In 2023, lenders were required to perform stricter affordability assessments before approving auto loans, reducing default risks.

Consumer Credit Laws: The Credit Contracts and Consumer Finance Act (CCCFA) regulates lending practices, emphasizing transparency in interest rates, fees, and loan terms. Amendments in 2022 tightened borrower affordability checks, impacting loan approval rates.

Government Incentives for Electric Vehicles: To promote sustainable transportation, the government offers rebates on electric vehicle (EV) purchases, making financing for EVs more attractive. In 2023, EV financing increased by 12% due to these incentives.

New Zealand Auto Finance Market Segmentation

By Lender Type: Banks dominate the market with structured auto loan offerings, while non-bank lenders and fintech platforms have gained traction due to their flexible and faster approval processes. Peer-to-peer lending platforms are also gaining attention as alternative financing options.

By Vehicle Type: Financing for new vehicles represents a major share but used vehicle financing is growing steadily as consumers seek cost-effective alternatives. Hybrid and electric vehicles are also gaining market share due to increasing government support and incentives.

By Loan Type: Secured loans, where the vehicle acts as collateral, are the most common, while unsecured loans are less prevalent but growing in popularity due to digital lending advancements. Balloon payment options and lease-to-own financing structures are also increasing in demand as consumers look for flexible financing solutions.

Competitive Landscape in New Zealand Auto Finance Market

The New Zealand auto finance market is relatively concentrated, with a few major financial institutions and non-bank lenders dominating the space. However, the expansion of digital lending platforms has diversified the market, offering consumers more choices and competitive loan products. The rising adoption of AI-driven credit assessment tools and digital verification methods has further streamlined the lending process, allowing for quicker approvals and greater access to financing for underserved demographics.

| Name | Founding Year | Original Headquarters |

| ANZ Auto Finance | 1835 | Melbourne, Australia |

| ASB Bank Car Loan | 1847 | Auckland, New Zealand |

| Westpac Auto Finance | 1817 | Sydney, Australia |

| BNZ (Bank of New Zealand) Auto Loan | 1861 | Wellington, New Zealand |

| Kiwibank Car Loan | 2002 | Wellington, New Zealand |

| Heartland Bank Auto Finance | 1875 | Auckland, New Zealand |

| Toyota Financial Services New Zealand | 1982 | Toyota City, Japan |

| BMW Financial Services New Zealand | 1988 | Munich, Germany |

| Volkswagen Financial Services NZ | 1949 | Braunschweig, Germany |

| UDC Finance (ANZ Subsidiary) | 1938 | Auckland, New Zealand |

| Marac Finance (Heartland Group) | 1952 | Auckland, New Zealand |

| Latitude Financial Services NZ | 2015 | Melbourne, Australia |

| Go Car Finance | 2000 | Auckland, New Zealand |

| Finance Now Car Loans | 2000 | Dunedin, New Zealand |

Some of the recent competitor trends and key information about competitors include:

ANZ: As one of the leading banks in New Zealand, ANZ recorded a 10% increase in auto loan disbursements in 2023, driven by competitive interest rates and digital lending services. The bank has expanded its online platforms, making loan applications more seamless.

Westpac: Westpac saw a 15% rise in vehicle loan approvals in 2023 due to its flexible repayment plans and innovative financing solutions tailored to first-time car buyers. The bank has also implemented eco-friendly incentives for electric vehicle (EV) financing.

ASB Bank: Focused on customer experience, ASB Bank introduced AI-driven loan approval systems, reducing approval times and enhancing transparency in loan disbursement. The bank also offers specialized financing packages for hybrid and electric vehicles.

BNZ: Known for its strong digital presence, BNZ expanded its online auto finance offerings in 2023, increasing its share in the used car financing segment by 12%. The bank has also collaborated with fintech firms to offer instant pre-approvals on vehicle loans.

UDC Finance: A key player in commercial and personal auto loans, UDC Finance strengthened its presence by collaborating with car dealerships across New Zealand. The lender has also launched new lease-to-own vehicle financing options to attract a wider customer base.

Heartland Bank: Heartland Bank has been focusing on electric vehicle financing, with a 20% rise in EV loan approvals in 2023. The bank has introduced specialized loan structures with lower interest rates for environmentally friendly vehicles.

What Lies Ahead for New Zealand Auto Finance Market?

The New Zealand auto finance market is projected to grow steadily by 2029, exhibiting a significant CAGR during the forecast period. This growth is expected to be driven by economic stability, digital lending advancements, and increased consumer demand for auto loans. Additionally, the introduction of AI-powered risk assessment models and blockchain-based smart contracts is expected to enhance transparency and efficiency in loan processing.

Shift Towards Electric Vehicles: As the New Zealand government continues to promote sustainability initiatives, there is anticipated to be an increase in financing for electric vehicles (EVs). Government incentives and low-interest loans for EVs will support this transition. More financial institutions are expected to offer green auto loans with preferential rates to support the adoption of environmentally friendly vehicles.

Integration of Technology: The integration of AI and big data analytics in loan processing and credit risk assessment is expected to streamline financing operations, improving approval efficiency and consumer satisfaction. Automated loan approval processes will enable faster access to financing, reducing paperwork and processing time for borrowers.

Growth of Online Auto Loan Platforms: Digital platforms are expected to gain further traction, providing consumers with instant loan approvals and paperless transactions, enhancing accessibility and convenience. Peer-to-peer lending solutions and fintech collaborations are also projected to play a crucial role in expanding auto financing accessibility.

Expansion of Used Car Financing: With rising vehicle prices, demand for used car financing is expected to grow, prompting lenders to offer competitive rates and flexible repayment plans. Certified pre-owned vehicle financing programs will likely see increased adoption, offering customers peace of mind through warranty-backed used cars.

Future Outlook and Projections for New Zealand Car Finance Market Size on the Basis of Loan Disbursements in USD Billion, 2024-2029

New Zealand Auto Finance Market Segmentation

- By Market Structure:

- Banks

- Non-Bank Financial Institutions

- Peer-to-Peer Lending Platforms

- Digital Auto Loan Providers

- Captive Finance Companies

- Credit Unions and Cooperatives

- By Vehicle Type:

- New Cars

- Used Cars

- Electric Vehicles (EVs)

- Hybrid Vehicles

- Commercial Vehicles

- By Loan Type:

- Secured Auto Loans

- Unsecured Auto Loans

- Balloon Payment Loans

- Lease-to-Own Financing

- Hire Purchase Agreements

- By Consumer Demographics:

- First-Time Buyers

- Young Professionals (18-34)

- Middle-Aged Consumers (35-54)

- Senior Citizens (55+)

- Low-Income Households

- High-Income Households

- By Region:

- Auckland

- Wellington

- Canterbury

- Waikato

- Otago

- Other Regional Areas

Players Mentioned in the Report (Banks):

- ANZ Bank New Zealand

- ASB Bank

- Bank of New Zealand (BNZ)

- Westpac New Zealand

- Kiwibank

- TSB Bank

- Heartland Bank

Players Mentioned in the Report (NBFCs):

- UDC Finance

- Avanti Finance

- MTF Finance

- Latitude Financial Services

- Harmoney

- Laybuy

Players Mentioned in the Report (Captive):

- Toyota Financial Services New Zealand

- Mercedes-Benz Financial Services New Zealand

- BMW Financial Services New Zealand

- Volkswagen Finance New Zealand

- Nissan Financial Services New Zealand

- Ford Credit New Zealand

- Honda Financial Services New Zealand

Key Target Audience:

- Auto Loan Providers

- Banks and Non-Banking Financial Institutions

- Digital Lending Platforms

- Vehicle Dealerships and Showrooms

- Regulatory Bodies (e.g., Reserve Bank of New Zealand)

- Research and Development Institutions

Time Period:

- Historical Period: 2018-2023

- Base Year: 2024

- Forecast Period: 2024-2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-Role of Entities, Stakeholders, and challenges they face.

4.2. Relationship and Engagement Model between Banks-Dealers, NBFCs-Dealers and Captive-Dealers-Commission Sharing Model, Flat Fee Model and Revenue streams

5.1. New Car and Used Car Sales in New Zealand by type of vehicle, 2018-2024

8.1. Credit Disbursed, 2018-2024

8.2. Outstanding Loan, 2018-2024

9.1. By Market Structure (Bank-Owned, Multi-Finance, and Captive Companies), 2023-2024

9.2. By Vehicle Type (Passenger, Commercial and EV), 2023-2024

9.3. By Region, 2023-2024

9.4. By Type of Vehicle (New and Used), 2023-2024

9.5. By Average Loan Tenure (0-2 years, 3-5 years, 6-8 years, above 8 years), 2023-2024

10.1. Customer Landscape and Cohort Analysis

10.2. Customer Journey and Decision-Making

10.3. Need, Desire, and Pain Point Analysis

10.4. Gap Analysis Framework

11.1. Trends and Developments for New Zealand Car Finance Market

11.2. Growth Drivers for New Zealand Car Finance Market

11.3. SWOT Analysis for New Zealand Car Finance Market

11.4. Issues and Challenges for New Zealand Car Finance Market

11.5. Government Regulations for New Zealand Car Finance Market

12.1. Market Size and Future Potential for Online Car Financing Aggregators, 2018-2029

12.2. Business Model and Revenue Streams

12.3. Cross Comparison of Leading Digital Car Finance Companies Based on Company Overview, Revenue Streams, Loan Disbursements/Number of Leads Generated, Operating Cities, Number of Branches, and Other Variables

13.1. Finance Penetration Rate and Average Down Payment for New and Used Cars, 2018-2029

13.2. How Finance Penetration Rates are Changing Over the Years with Reasons

13.3. Type of Car Segment for which Finance Penetration is Higher

17.1. Market Share of Key Banks in New Zealand Car Finance Market, 2024

17.2. Market Share of Key NBFCs in New Zealand Car Finance Market, 2024

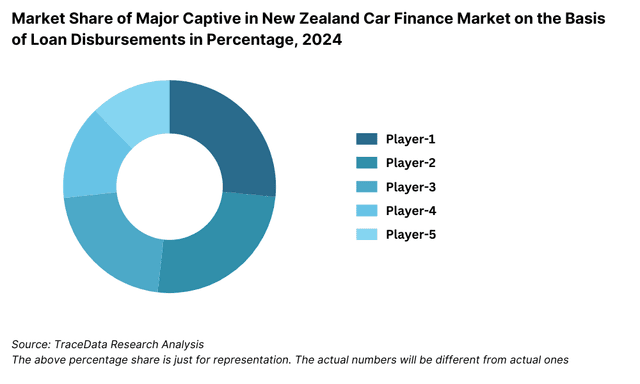

17.3. Market Share of Key Captive in New Zealand Car Finance Market, 2024

17.4. Benchmark of Key Competitors in New Zealand Car Finance Market, including Variables such as Company Overview, USP, Business Strategies, Strengths, Weaknesses, Business Model, Number of Branches, Product Features, Interest Rate, NPA, Loan Disbursed, Outstanding Loans, Tie-Ups and others

17.5. Strengths and Weaknesses

17.6. Operating Model Analysis Framework

17.7. Gartner Magic Quadrant

17.8. Bowmans Strategic Clock for Competitive Advantage

18.1. Credit Disbursed, 2025-2029

18.2. Outstanding Loan, 2025-2029

19.1. By Market Structure (Bank-Owned, Multi-Finance, and Captive Companies), 2025-2029

19.2. By Vehicle Type (Passenger, Commercial and EV), 2025-2029

19.3. By Region, 2025-2029

19.4. By Type of Vehicle (New and Used), 2025-2029

19.5. By Average Loan Tenure (0-2 years, 3-5 years, 6-8 years, above 8 years), 2025-2029

19.6. Recommendations

19.7. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities for the New Zealand Auto Finance Market. Basis this ecosystem, we will shortlist leading 5-6 financial institutions in the country based on their financial information, loan disbursement capacity, and market presence.

Sourcing is made through industry reports, multiple secondary sources, and proprietary databases to perform desk research and collate industry-level information.

Step 2: Desk Research

We conduct an exhaustive desk research process referencing diverse secondary and proprietary databases. This approach enables us to perform a thorough analysis of the market, aggregating industry-level insights. We delve into aspects like loan disbursement trends, market players, interest rate structures, demand, and other key indicators. We supplement this with detailed examinations of company-level data, relying on sources like press releases, annual reports, financial statements, and similar documents. This process helps establish a foundational understanding of both the market and its key players.

Step 3: Primary Research

We initiate a series of in-depth interviews with C-level executives and other stakeholders representing various financial institutions and end-users in the New Zealand Auto Finance Market. This interview process serves multiple purposes: to validate market hypotheses, authenticate statistical data, and extract valuable operational and financial insights from these industry representatives. A bottom-up approach is undertaken to evaluate loan disbursement volumes for each player, thereby aggregating to the overall market size.

As part of our validation strategy, our team executes disguised interviews where we approach each company under the guise of potential customers. This approach enables us to validate operational and financial information shared by company executives, cross-referencing it against secondary databases. These interactions also provide comprehensive insights into revenue streams, value chains, pricing structures, and other factors.

Step 4: Sanity Check

- A bottom-up and top-down analysis, along with market size modeling exercises, is undertaken to assess and validate the overall market projections. Discrepancies between primary and secondary data sources are resolved through iterative adjustments, ensuring the highest level of accuracy in our estimates.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The New Zealand auto finance market is expected to experience steady growth, driven by the increasing demand for vehicle financing solutions, expanding digital lending platforms, and government incentives for electric vehicle financing. The market is estimated to reach NZD 20 billion by 2029, supported by evolving consumer preferences and innovative financial products.

The key players in the New Zealand auto finance market include ANZ, Westpac, ASB Bank, BNZ, UDC Finance, and Heartland Bank. Other emerging lenders such as Squirrel Money, Harmoney, and Simplify Loans are also making significant contributions to the market.

The major growth drivers include economic stability, increasing vehicle ownership rates, digital advancements in lending, and favorable government policies supporting auto financing. The rising trend of electric vehicle adoption is also contributing to market expansion.

The key challenges include fluctuating interest rates, stringent regulatory requirements, and accessibility of credit for low-income consumers, and competition among financial institutions. Additionally, the high cost of vehicle ownership and evolving credit risk management practices may impact loan approvals and market growth.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0