Pakistan Logistics and Warehousing Market Outlook to 2029

By Market Structure, By Services, By End Users, By Mode of Transport, By Type of Warehousing, and By Region.

Report Overview

Report Code

TDR0177

Coverage

Asia

Published

May 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Pakistan Logistics and Warehousing Market Outlook to 2029 - By Market Structure, By Services, By End Users, By Mode of Transport, By Type of Warehousing, and By Region.” provides a comprehensive analysis of the logistics and warehousing industry in Pakistan. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the logistics and warehousing industry.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Pakistan Logistics and Warehousing Market Outlook to 2029 - By Market Structure, By Services, By End Users, By Mode of Transport, By Type of Warehousing, and By Region.” provides a comprehensive analysis of the logistics and warehousing industry in Pakistan. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the logistics and warehousing industry. The report concludes with future market projections based on revenue, by services, transport mode, warehouse type, region, cause and effect relationship, and success case studies highlighting the major opportunities and cautions.

Pakistan Logistics and Warehousing Market Overview and Size

The Pakistan logistics and warehousing market reached a valuation of PKR 1,980 Billion in 2023, driven by infrastructure investments, e-commerce expansion, CPEC-related developments, and increasing trade activities. Major players such as TCS Logistics, BlueEx, Agility Logistics, DHL Pakistan, and Pakistan Post dominate the industry with expansive networks, multimodal logistics offerings, and warehousing infrastructure in key trade hubs including Karachi, Lahore, Faisalabad, and Islamabad.

In 2023, TCS expanded its warehousing capacity in Karachi and Lahore to cater to the growing demands of e-commerce fulfillment and B2B distribution. The launch of digital logistics platforms has also enhanced transparency and efficiency in inventory management, tracking, and delivery services. Karachi and Lahore remain central nodes due to their connectivity to ports, industrial clusters, and regional demand centers.

Market Size for Pakistan Logistics and Warehousing Industry on the Basis of Revenue in USD Billion, 2018-2024

What Factors are Leading to the Growth of Pakistan Logistics and Warehousing Market:

Infrastructure Development: Massive infrastructure projects under the China-Pakistan Economic Corridor (CPEC) have significantly enhanced logistics corridors, road networks, and connectivity between ports and inland regions. Between 2018 and 2023, over PKR 600 billion was invested in transport and logistics-related infrastructure.

E-commerce Growth: With over 130 million internet users and rising smartphone penetration, e-commerce in Pakistan is witnessing exponential growth, which in turn has driven demand for last-mile delivery and storage solutions. In 2023, warehousing demand from e-commerce accounted for over 18% of total warehousing space in key cities.

Industrial and Manufacturing Expansion: Rising exports in textiles, pharmaceuticals, and agri-based products have created a need for temperature-controlled storage, bulk warehousing, and efficient freight handling. Export-driven sectors have boosted the demand for value-added logistics services like cold chain and cross-docking.

Which Industry Challenges Have Impacted the Growth for Pakistan Logistics and Warehousing Market

Infrastructure Bottlenecks: Despite ongoing development, Pakistan continues to face serious infrastructure limitations including poor road conditions, limited rail connectivity, and outdated port facilities. According to industry estimates, over 35% of logistics companies report delivery delays due to infrastructure issues, which not only reduce efficiency but also increase operational costs by an estimated 18%.

High Operational Costs: Rising fuel prices, warehousing rents, and frequent delays in customs clearance contribute to elevated operational costs. In 2023, logistics providers reported that fuel alone accounted for nearly 40% of total transportation expenses. These high costs are particularly burdensome for small to medium-sized logistics firms, limiting their scalability and competitiveness.

Fragmented Market and Informal Sector Dominance: Pakistan’s logistics industry is highly fragmented, with a large share of the market dominated by informal or unorganized players. This limits the adoption of modern practices such as real-time tracking, digital inventory management, and standardized warehousing processes. As of 2023, more than 60% of logistics providers lacked access to digital logistics infrastructure.

What are the Regulations and Initiatives Which Have Governed the Market

Pakistan Single Window (PSW) Initiative: Launched to streamline cross-border trade, the PSW system reduces documentation and clearance times by integrating all regulatory authorities on a single digital platform. As of late 2023, the PSW has been implemented at 21 ports and border locations, cutting average clearance time by 36% for import shipments.

National Freight and Logistics Policy (NFLP): The Ministry of Planning launched the NFLP to modernize the logistics sector, focusing on multimodal transport, regulatory reforms, and infrastructure development. This policy aims to reduce logistics costs from the current 18% of GDP to 12% by 2030.

Warehousing Standards and Cold Chain Guidelines: In 2023, the Pakistan Standards and Quality Control Authority (PSQCA) introduced new guidelines for warehousing infrastructure, especially focused on temperature-sensitive goods such as pharmaceuticals and perishables. The standards require temperature monitoring, power backup, and structured layout for large-scale warehouse operators.

Pakistan Logistics and Warehousing Market Segmentation

By Market Structure: The logistics and warehousing industry in Pakistan is largely dominated by unorganized players, especially in first and last-mile delivery services. These players typically offer low-cost services with minimal formal processes, catering to price-sensitive SMEs and rural markets. However, the organized sector is rapidly expanding due to demand from e-commerce platforms, multinational manufacturers, and retail chains. Organized players offer value-added services like inventory tracking, cold chain management, and automation, making them preferred partners for large-scale operations.

By Mode of Transport:Road transport dominates Pakistan’s logistics sector due to underdeveloped rail and air cargo infrastructure. It accounts for the majority of domestic freight movement, especially for FMCG, textiles, and agriculture. Rail freight is used for bulk commodities like coal and cement but is hindered by poor network coverage. Air freight, although expensive, is used for high-value and perishable goods. Multimodal logistics solutions are emerging with CPEC corridor developments aimed at integrating road, rail, and port infrastructure.

By Type of Warehousing: The warehousing sector is segmented into General Warehousing, Cold Chain Warehousing, and Bonded Warehousing. General warehousing caters to the bulk of demand from retail and industrial sectors. Cold chain facilities are limited but growing, primarily supporting pharmaceuticals, meat, and dairy. Bonded warehouses are concentrated near major ports like Karachi and Port Qasim, facilitating international trade and customs clearance.

Competitive Landscape in Pakistan Logistics and Warehousing Market

The Pakistan logistics and warehousing market is moderately fragmented, with a mix of local and international players. However, the industry is witnessing rapid consolidation and digital transformation as global logistics firms, e-commerce enablers, and domestic 3PL providers expand their footprint. Key players such as TCS Logistics, Agility Pakistan, DHL Supply Chain, Ryder Pakistan, and BlueEx are leading the shift toward more integrated and technology-driven logistics solutions.

| Company Name | Founding Year | Original Headquarters |

| TCS (Tranzum Courier Service) | 1983 | Karachi, Pakistan |

| BlueEX (Blue Logistics Pvt. Ltd.) | 2005 | Karachi, Pakistan |

| PCL (Pak Cargo Logistics) | 2005 | Lahore, Pakistan |

| Gerry’s International (FedEx Licensee) | 1963 | Karachi, Pakistan |

| Agility Logistics Pakistan | 1979 (Pakistan: ~2006) | Kuwait City, Kuwait |

| RAH Global Logistics | 2011 | Karachi, Pakistan |

| Pakistan International Container Terminal (PICT) | 2002 | Karachi, Pakistan |

| APL Logistics Pakistan | 2000 (Pakistan: ~2010s) | Scottsdale, USA |

| TML Logistics Pvt. Ltd. | 2010 | Karachi, Pakistan |

| DB Schenker Pakistan | 1872 (Pakistan: ~2000s) | Essen, Germany |

| DHL Global Forwarding Pakistan | 1969 (Pakistan: ~1980s) | Bonn, Germany |

| Kuehne + Nagel Pakistan | 1890 (Pakistan: ~2000s) | Schindellegi, Switzerland |

| Maersk Logistics Pakistan | 1904 (Pakistan: ~2000s) | Copenhagen, Denmark |

| CEVA Logistics Pakistan | 2006 (Pakistan: ~2010s) | Marseille, France |

| Yusen Logistics Pakistan | 1955 (Pakistan: ~2000s) | Tokyo, Japan |

| Nippon Express Pakistan | 1937 (Pakistan: ~1990s) | Tokyo, Japan |

| UPS Pakistan (via local partner) | 1907 (Pakistan: ~1990s) | Atlanta, USA |

Some of the recent competitor trends and key information about competitors include:

TCS Logistics: As one of the largest and oldest logistics players in Pakistan, TCS has expanded its warehousing space by 18% in 2023, adding temperature-controlled facilities to support the growing pharma and food sectors. The company also launched a centralized logistics management platform to offer real-time visibility to its enterprise clients.

Agility Pakistan: A global logistics powerhouse, Agility Pakistan has focused on industrial logistics and cold chain warehousing, particularly in Karachi and Lahore. In 2023, the company reported a 22% growth in contract logistics revenue, driven by FMCG and healthcare clients.

DHL Supply Chain Pakistan: DHL operates multi-user warehousing facilities and is a preferred 3PL provider for multinational companies in Pakistan. The firm recently launched a green logistics initiative aimed at reducing emissions by converting part of its fleet to electric vehicles in 2024.

Ryder Pakistan: Known for its warehousing automation and RFID inventory systems, Ryder Pakistan has been expanding into Tier-2 cities to serve regional FMCG distribution. In 2023, Ryder reported a 30% year-on-year growth in e-commerce logistics partnerships.

BlueEx: BlueEx specializes in last-mile delivery and fulfillment services for e-commerce platforms. The company operates over 80 warehouses and pickup hubs nationwide. In 2023, it introduced AI-powered route optimization, reducing delivery turnaround times by 17%.

What Lies Ahead for Pakistan Logistics and Warehousing Market?

The Pakistan logistics and warehousing market is projected to experience consistent growth by 2029, with a promising CAGR fueled by infrastructure investments, rising domestic consumption, and the increasing role of e-commerce and manufacturing in the national economy.

CPEC-Driven Infrastructure Expansion: With continued progress under the China-Pakistan Economic Corridor (CPEC), Pakistan is expected to witness significant improvements in transport corridors, dry ports, and logistics parks. These developments will boost connectivity across regions and enable faster, cost-efficient movement of goods both domestically and for transit trade to Central Asia.

Adoption of Smart Warehousing Technologies: The market is shifting toward the adoption of smart warehousing solutions, including warehouse management systems (WMS), real-time inventory tracking, and robotics for order fulfillment. By 2029, an increasing share of organized warehouse operators are expected to adopt digital technologies to improve productivity and reduce operational inefficiencies.

Rise of Integrated 3PL Solutions: There is a growing preference among large manufacturers and e-commerce firms for integrated third-party logistics (3PL) providers offering bundled services like transportation, warehousing, customs clearance, and last-mile delivery. This trend is likely to drive consolidation in the sector and encourage investment in large-scale, multi-user logistics hubs.

Growth of Cold Chain and Pharma Logistics: The pharmaceutical, food, and agriculture sectors are expected to significantly boost demand for cold chain warehousing and temperature-controlled logistics. With increasing health consciousness and food safety regulations, cold chain infrastructure is projected to expand in urban and semi-urban areas across Pakistan by 2029.

Future Outlook and Projections for Pakistan Logistics and Warehousing Market on the Basis of Revenues in USD Billion, 2024-2029

Pakistan Logistics and Warehousing Market Segmentation

• By Market Structure: o Organized Logistics Providers

o Unorganized/Informal Logistics Operators

o First-Mile Logistics Providers

o Last-Mile Delivery Services

o Freight Forwarders

o Third-Party Logistics (3PL)

o Fourth-Party Logistics (4PL)

• By Service Type: o Transportation

o Warehousing

o Inventory Management

o Packaging & Labeling

o Cold Chain Logistics

o Customs Brokerage

o Reverse Logistics

• By End User Industry: o FMCG

o E-commerce & Retail

o Pharmaceuticals

o Automotive

o Electronics & Appliances

o Agriculture & Food Processing

o Textiles & Apparel

o Oil & Gas

• By Mode of Transport: o Road

o Rail

o Air

o Sea

o Multimodal

• By Type of Warehousing: o General Warehousing

o Cold Chain Warehousing

o Bonded Warehousing

o Distribution Centers

o Fulfillment Centers

o Container Freight Stations

• By Region: o Sindh

o Punjab

o Khyber Pakhtunkhwa

o Balochistan

o Islamabad Capital Territory

o Gilgit-Baltistan

Players Mentioned in the Report:

Freight Forwarding Companies

- Combined Freight International (CFIPAK)

- Costa Logistics Pakistan

- Qadri Movers and Packers

- Balance Logistics & Relocation

- Global Logistic Group

- Bismillah Logistics

- Flash Logistics

- Freight Forwarders Pakistan

- Ample Shipping & Logistic Services

- SUPERTERRA Container Line

- Crystal Global Shipping

- Shipner Shipping and Agencies

- VMR Lines

- Oceanic Star Line

- W Container Lines

- Ravian International Agencies Pakistan

- EMKAY Lines

- ACUTE Shipping and Logistics

Warehousing Companies

- Maersk Integrated Logistics Park (MILP)

- Gujrat Steel Pvt. Ltd.

- Shispare Pvt. Ltd.

- Oware

- One Union Solutions

- JN International

- CFIPAK

- National Logistics Corporation (NLC)

- Lahore Movers

E-Commerce Logistics Companies

- TCS

- BlueEX

- Rider

- Daraz Express

- InstaWorld

- M&P Express Logistics

- FastEx

- Dreamco Express

- Safe Express Logistics

Express Logistics Companies

TCS

M&P Express Logistics

Leopards Courier

BlueEX

DHL Express Pakistan

FedEx Pakistan

UPS Pakistan

Aramex Pakistan

Dreamco Express

FastEx

Key Target Audience:

• Logistics Companies

• Warehouse Developers

• Cold Chain Operators

• E-commerce Fulfillment Providers

• Industrial Manufacturers

• Regulatory Authorities (e.g., Pakistan Railways, PSQCA)

• Trade and Transport Ministries

• Investment and Infrastructure Development Agencies

Time Period:

• Historical Period: 2018–2023

• Base Year: 2024

• Forecast Period: 2024–2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Macroeconomic framework for Pakistan Including GDP (2018-2024), GDP Growth (2018-2024), GDP Contribution by Sector

4.2. Logistics Sector Contribution to GDP and how the contribution has been changing in the historical assessment

4.3. Ease of Doing Business in Pakistan

4.4. LPI Index of Pakistan and Improvements in the last 10-15 Years

4.5. Custom Procedure and Custom Charges in Pakistan Logistics market

5.1. Landscape of Investment Parks and Free Trade Zones in Pakistan

5.2. Current Scenario for Logistics Infrastructure in Pakistan

5.3. Road Infrastructure in Pakistan including Road Network, Toll Charges and Toll Network, Major Goods Traded through Road, Major Flow Corridors for Road (Inbound and Outbound)

5.4. Air Infrastructure in Pakistan including Total Volume Handled, FTK for Air Freight, Major Inbound and Outbound Flow Corridors, Major Goods traded through Air, Number of Commercial and passenger Airports, Air Freight Volume by Ports and other Parameters

5.5. Sea Infrastructure in Pakistan including Total Volume Handled, FTK for Sea Freight, Major Inbound and Outbound Flow Corridors, Major Goods Traded through Sea, Number of Ports for Coastal and Ocean Freight, Number of Vessels, Sea Freight Volume by Ports and other Parameters

5.6. Rail Infrastructure in Pakistan including Total Volume Handled, FTK for Rail Freight, Major Inbound and Outbound Flow Corridors, Major Goods Traded through Rail and others

6.1. Basis Revenues, 2018-2024P

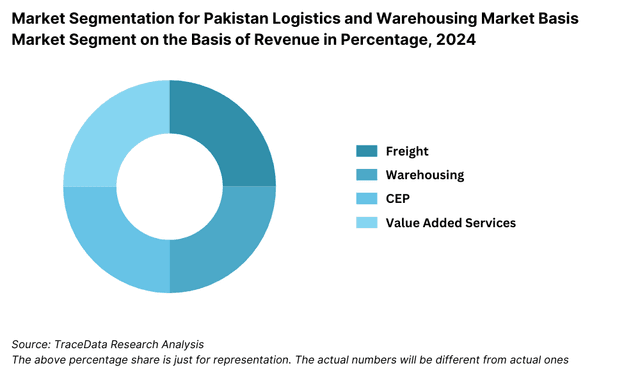

7.1. By Segment (Freight Forwarding, Warehousing, CEP and Value-Added Services), 2018-2024P

7.2. By End User Industries, 2018-2024P

8.1. Market Overview and Genesis

8.2. Pakistan Freight Forwarding Market Size by Revenues, 2018-2024P

8.3. Pakistan 3PL Freight Forwarding Market Segmentation, 2018-2024P

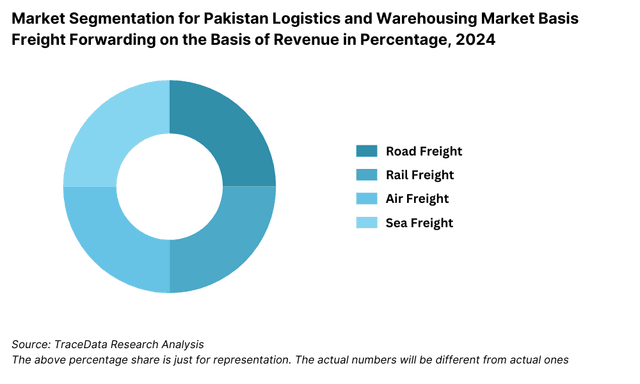

8.3.1. By Mode of Freight Transport (Road, Sea, Air and Rail), 2018-2024P

8.3.1.1. Price per FTK for Road/Air/Sea and Rail in Pakistan

8.3.1.2. Road Freight (Domestic and International Volume, FTK and Revenue; Number of Registered Vehicles)

8.3.1.3. Road Freight Domestic and International Corridors

8.3.1.4. Ocean Freight (Domestic and International Volume, FTK and Revenue; Volume by Commodity; Sea Ports Key Statistics)

8.3.1.5. Air Freight (Domestic and International Volume, FTK and Revenue)

8.3.1.6. Rail Freight (Domestic and International Volume, FTK and Revenue; Volume by Commodity and Region)

8.3.1.7. Export-Import Scenario (Value by Mode of Transport, Commodity and Country; Volume by Principal Commodities)

8.3.2. By Intercity Road Freight Corridors, 2018-2024P

8.3.3. By International Road Freight Corridors (China, Thailand and Pakistan), 2018-2024P

8.3.4. By End User (Industrial, FMCG, F&B, Retail and Others), 2018-2024P

8.4. Snapshot of Freight Truck Aggregators in Pakistan Including Company Overview, USP. Business Strategies, Future Plans, Business Model, Number of Fleets, Margins/Commission, Number of Booking, Major Clients, Average Booking Amount, Major Routes and others

8.5. Competitive Landscape in Pakistan Freight Forwarding Market, 2021

8.5.1. Heat Map of Major Players in Pakistan Freight Forwarding on the Basis of Service offering

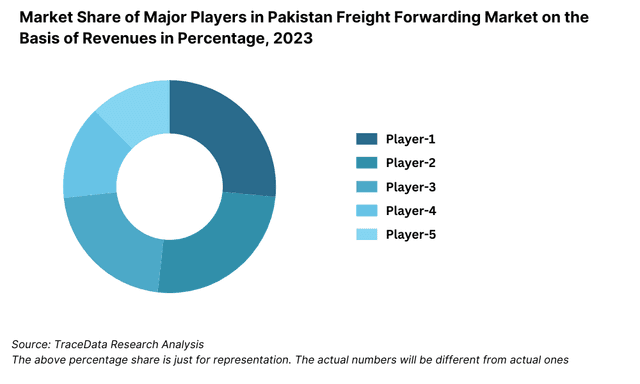

8.5.2. Market Share of Maior Players in Pakistan Freight Forwarding Market, 2023

8.5.3. Cross Comparison of Major Players in Freight Forwarding Companies on the Basis of Parameters including Volume of Road Freight, Inception Year, Number of Fleets (Owned and Subcontracted), Fleets by Type, Occupancy Rate, Number of Employees, Major Route Network, Major Clients, Revenues, Volume of Sea Freight, Volume of Air Freight, USP, Business Strategy, Technology, (2023)

8.6. Pakistan 3PL Freight Forwarding Future Market Size by Revenues, 2025-2029

8.7. Pakistan Freight Forwarding Market Segmentation, 2025-2029

8.7.1. Future Market Segmentation by Mode of Freight Transport (Road, Sea, Air and Rail), 2025-2029

8.7.2. Future Market Segmentation by International Road Freight Corridors (China, Thailand and Pakistan), 2025-2029

8.7.3. Future Market Segmentation by End User (Industrial, FMCG, F&B, Retail and Others), 2025-2029

9.1. Market Overview and Genesis

9.2. Value Chain Analysis in Pakistan Warehousing Market including entities, margins, role of each entity, process flow, challenges and other aspects

9.3. Pakistan Warehousing Market Size on the Basis of Revenues and Warehousing Space, 2018-2024P

9.4. Pakistan 3PL Warehousing Segmentation

9.4.1. Pakistan Warehousing Revenue by Business Model (Industrial/Retail, ICD/CFS and Cold Storage), 2018-2024P

9.4.2. Pakistan Warehousing By Type of Warehouse (General, Open Yard, Freezer/Chiller, Ambient and Bonded Warehouses), 2018-2024P

9.4.3. Pakistan Warehousing Revenue by End User (Industrial & Construction, FMCG, Retail, Food & Beverage and Others), 2018-2024P

9.4.4. 3PL Warehousing Space by Region, 2024P

9.5. Competitive Landscape in Pakistan 3PL Warehousing Market

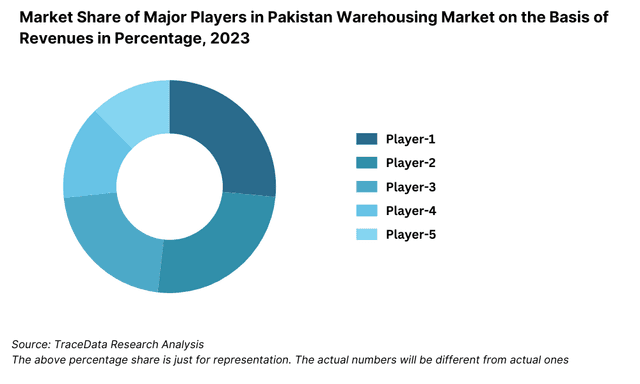

9.5.1. Market share of Top 10 Companies in Pakistan Warehousing Market, 2023

9.5.2. Cross Comparison of Top 10 3PL Warehousing Companies on the Basis of Parameters including Company Overview, USP, Business Strategy, Future Plans, Technology, Revenues from Warehousing, Number of Warehouses, Warehousing Space, Location of Warehouses, Type of Warehouses, Occupancy Rate, Rental Rates, Clients and others, (2023)

9.6. Pakistan Warehousing Future Market Size on the Basis of Revenues, 2025-2029

9.7. Pakistan Warehousing Market Future Segmentation

9.7.1. Pakistan Warehousing Revenue by Business Model (Industrial/Retail, ICD/CFS and Cold Storage), 2025-2029

9.7.2. Pakistan Warehousing Revenue By Type of Warehouse (General, Open Yard, Freezer/Chiller, Ambient and Bonded Warehouses), 2025-2029

9.7.3. Pakistan Warehousing Revenue by End User (Industrial & Construction, FMCG, Retail, Food & Beverage and Others), 2025-2029

10.1. Market Overview and Genesis

10.2. Value Chain Analysis in Pakistan CEP Market including entities, margins, role of each entity, process flow, challenges and other aspects

10.3. Revenue Composition and Contribution Between First Mile/Mid Mile and Last Mile Delivery-Analysis for Domestic and International Shipments

10.4. Pakistan CEP Market Size on the Basis of Revenues and Shipments, 2018-2024P

10.5. Pakistan CEP Market Segmentation, 2021

10.5.1. Segmentation by Mails and Documents, E-Commerce Shipments and Express Cargo, 2023-2024P

10.5.2. Segmentation by International and Domestic Express, 2023-2024P

10.5.3. Segmentation by B2B, B2C and C2C, 2023-2024P

10.5.4. Segmentation by Period of Delivery, 2023-2024P

10.6. Competitive Landscape in 3PL Market, 2021

10.6.1. Overview and Genesis, Market Nature, Market Stage and Major Competing Parameters

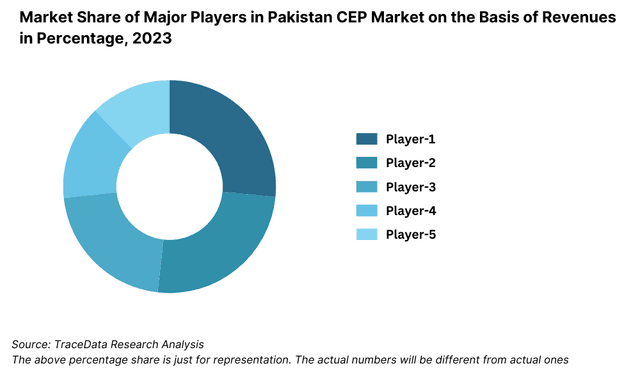

10.6.2. Market Share of Companies in Pakistan CEP Market on the Basis of Revenues/Number of Shipments, 2023

10.6.3. Market Share of Top 5 Companies in Pakistan E-Commerce Shipment Market on the Basis of Revenues/Number of Shipments, 2023

10.6.4. Cross Comparison of Top 10 Pakistan CEP Companies on the Basis of Parameters including Company Overview, USP, Business Strategy, Future Plans, Technology, Number of last Mile Delivery Shipments, Revenues, Major Clients, Number of Fleets, Number of Employees, Number of Riders, Number of Pin Code Served, Major Service Offering and others

10.7. Pakistan CEP Market Size on the Basis of Revenues and Shipments, 2025-2029

10.8. Pakistan CEP Market Segmentation

10.8.1. Segmentation by Mails and Documents, E-Commerce Shipments and Express Cargo, 2025-2029

10.8.2. Segmentation by International and Domestic Express, 2025-2029

10.8.3. Segmentation by B2B, B2C and C2C, 2025-2029

10.8.4. Segmentation by Period of Delivery, 2025-2029

11.1. Customer Cohort Analysis and End User Paradigm for Different Industry Verticals under Logistics Sector (Telecommunications, FMCG, Automotive, Apparel, F&B, Construction and Pharmaceuticals)

11.2. Understanding on Logistics Spend by End User, 2023-2024P

11.3. End User Preferences in terms of In-House or Outsourcing Logistics Services and Reason for Selection; Segregate this by Size of Company on the Basis of Revenues

11.4. Major Logistics Company who are Specialized in Serving Each Type of End User (Telecommunications, FMCG, Apparel, F&B, Construction and Pharmaceuticals)

11.5. Detailed Landscape of Each End Users across Parameters including Major Products Manufactured and Traded, Emerging Products, Type of Services Required, and Type of Services Outsourced, Major Companies, Contract Duration, Likelihood to Recommend, Market Orientation, Major Clusters, Type of Sourcing Preference, Pain Points, Facilities/Services Required, Future Outlook. Market Size for End User Industry Vertical with Growth Rate, 2018-2024P

12.1. Basis Revenues, 2025-2029

13.1. By Segment (Freight Forwarding, Warehousing, CEP and Value-Added Services), 2025-2029

13.2. By End User Industries, 2025-2029

13.3. Recommendation

13.4. Opportunity Analysis

1. Executive Summary (Pakistan Logistics and Warehousing Market)

2. Research Methodology (Pakistan Logistics and Warehousing Market)

3. Ecosystem of Key Stakeholders in Pakistan Logistics and Warehousing Market

4. Macroeconomic Framework for Pakistan

4.1 Macroeconomic Framework for Pakistan Including GDP, GDP Growth and GDP Contribution by Sector

4.2 Logistics Sector Contribution to GDP and Evolution in the Historical Assessment

4.3 Ease of Doing Business and Investment Climate in Pakistan

4.4 Logistics Performance Index of Pakistan and Improvements in the Historical Period

4.5 Customs Procedures and Customs Charges in Pakistan Logistics Market

5. Infrastructure in Pakistan Logistics & Warehousing Market

5.1 Landscape of Logistics Parks, Industrial Estates, SEZs and Free Trade Zones in Pakistan (Logistics Parks & FTZs-Pakistan)

5.2 Current Scenario for Logistics Infrastructure in Pakistan-Road, Rail, Sea, Air and Multimodal (Infrastructure Readiness-Pakistan)

5.3 Road Infrastructure in Pakistan Including Road Network, Toll Charges and Toll Network, Major Goods Traded through Road, Major Flow Corridors for Road

5.4 Air Infrastructure in Pakistan Including Total Volume Handled, FTK for Air Freight, Major Inbound and Outbound Flow Corridors, Major Goods Traded through Air, Number of Commercial and Passenger Airports, Air Freight Volume by Airports and Other Parameters (Air Freight Infrastructure-Pakistan)

5.5 Sea Infrastructure in Pakistan Including Total Volume Handled, FTK for Sea Freight, Major Inbound and Outbound Flow Corridors, Major Goods Traded through Sea, Number of Ports for Coastal and Ocean Freight, Number of Vessels, Sea Freight Volume by Ports and Other Parameters (Sea and Port Infrastructure-Pakistan)

5.6 Rail Infrastructure in Pakistan Including Total Volume Handled, FTK for Rail Freight, Major Inbound and Outbound Flow Corridors, Major Goods Traded through Rail and Other Parameters (Rail Freight Infrastructure-Pakistan)

5.7 Dry Ports, ICDs, CFS Facilities and Inland Container Terminals in Pakistan

6. Pakistan Logistics and Warehousing Market Size

6.1 Market Size on the Basis of Revenues

7. Pakistan Logistics and Warehousing Market Segmentation

7.1 By Segment-Freight Forwarding, Warehousing, CEP and Value-Added Services

7.2 By End User Industries-Telecommunications, FMCG, Automotive, Apparel, F&B, Construction, Pharmaceuticals and Others

7.3 By Mode-Road, Sea, Air and Rail (Market Segmentation by Mode-Pakistan)

7.4 By Region-Karachi/Sindh, Lahore/Punjab, Islamabad/Rawalpindi, Central Pakistan, Border and Corridor Clusters (Market Segmentation by Region-Pakistan)

7.5 By Ownership-In-house vs Outsourced Logistics

8. Pakistan Freight Forwarding Market

8.1 Market Overview and Genesis

8.2 Pakistan Freight Forwarding Market Size by Revenues

8.3 Pakistan 3PL Freight Forwarding Market Segmentation

8.3.1 By Mode of Freight Transport-Road, Sea, Air and Rail

8.3.1.1 Price per FTK for Road, Air, Sea and Rail in Pakistan

8.3.1.2 Road Freight-Domestic and International Volume, FTK and Revenue; Number of Registered Commercial Vehicles (Road Freight KPIs-Pakistan)

8.3.1.3 Road Freight Domestic and International Corridors-Karachi-Lahore, Karachi-Islamabad, Karachi-Quetta, Lahore-Peshawar and Others

8.3.1.4 Ocean Freight-Domestic and International Volume, FTK and Revenue; Volume by Commodity; Sea Ports Key Statistics (Sea Freight KPIs-Pakistan)

8.3.1.5 Air Freight-Domestic and International Volume, FTK and Revenue

8.3.1.6 Rail Freight-Domestic and International Volume, FTK and Revenue; Volume by Commodity and Region (Rail Freight KPIs-Pakistan)

8.3.1.7 Export-Import Scenario-Value by Mode of Transport, Commodity and Country; Volume by Principal Commodities (Trade and Modal Split-Pakistan)

8.3.2 By Intercity Road Freight Corridors-Karachi-Lahore, Karachi-Faisalabad, Lahore-Islamabad, Karachi-Peshawar and Others

8.3.3 By International Road Freight Corridors-China, Afghanistan, Iran, Central Asia and Other Cross-Border Routes (International Road Corridors-Pakistan)

8.3.4 By End User-Industrial, FMCG, F&B, Retail and Others

8.4 Snapshot of Freight Truck Aggregators in Pakistan Including Company Overview, USP, Business Strategies, Future Plans, Business Model, Number of Fleets, Margins/Commission, Number of Bookings, Major Clients, Average Booking Amount, Major Routes and Other Parameters

8.5 Competitive Landscape in Pakistan Freight Forwarding Market

8.5.1 Heat Map of Major Players in Pakistan Freight Forwarding on the Basis of Service Offering (Service Offering Heat Map-Pakistan Freight)

8.5.2 Market Share of Major Players in Pakistan Freight Forwarding Market

8.5.3 Cross Comparison of Major Freight Forwarding Companies on the Basis of Parameters Including Fleet Size (Owned and Subcontracted), Volume of Road Freight, Volume of Sea Freight, Volume of Air Freight, Network Coverage, Technology Adoption, Service Mix and Revenue Scale

8.5.4 Detailed Profiles of Major Freight Forwarding and Integrated Logistics Companies in Pakistan

8.6 Pakistan Freight Forwarding Future Market Size by Revenues

8.7 Pakistan Freight Forwarding Market Segmentation-Future Outlook

8.7.1 Future Market Segmentation by Mode of Freight Transport-Road, Sea, Air and Rail

8.7.2 Future Market Segmentation by International Road Freight Corridors-China, Afghanistan, Iran, Central Asia and Others

8.7.3 Future Market Segmentation by End User-Industrial, FMCG, F&B, Retail and Others

9. Pakistan Warehousing Market

9.1 Market Overview and Genesis

9.2 Value Chain Analysis in Pakistan Warehousing Market Including Entities, Margins, Role of Each Entity, Process Flow, Challenges and Other Aspects

9.3 Pakistan Warehousing Market Size on the Basis of Revenues and Warehousing Space (Warehousing Market Size and Stock-Pakistan)

9.4 Pakistan Warehousing Market Segmentation

9.4.1 Pakistan Warehousing Revenue by Business Model-Industrial/Retail, ICD/CFS and Cold Storage

9.4.2 Pakistan Warehousing by Type of Warehouse-General, Open Yard, Freezer/Chiller, Ambient and Bonded Warehouses

9.4.3 Pakistan Warehousing Revenue by End User-Industrial & Construction, FMCG, Retail, Food & Beverage and Others

9.4.4 3PL Warehousing Space by Region-Karachi/Sindh, Lahore/Punjab, Islamabad/Rawalpindi, Central and Northern Regions

9.5 Competitive Landscape in Pakistan Warehousing Market

9.5.1 Market Share of Top Companies in Pakistan Warehousing Market

9.5.2 Cross Comparison of Top Warehousing Companies on the Basis of Parameters Including Company Overview, USP, Business Strategy, Future Plans, Technology, Revenues from Warehousing, Number of Warehouses, Warehousing Space, Location of Warehouses, Type of Warehouses, Occupancy Rate, Rental Rates, Clients and Other Parameters

9.6 Pakistan Warehousing Future Market Size on the Basis of Revenues

9.7 Pakistan Warehousing Market Future Segmentation

9.7.1 Pakistan Warehousing Revenue by Business Model-Industrial/Retail, ICD/CFS and Cold Storage

9.7.2 Pakistan Warehousing Revenue by Type of Warehouse-General, Open Yard, Freezer/Chiller, Ambient and Bonded Warehouses

9.7.3 Pakistan Warehousing Revenue by End User-Industrial & Construction, FMCG, Retail, Food & Beverage and Others

10. Pakistan CEP (Courier, Express and Parcel) Market

10.1 Market Overview and Genesis

10.2 Value Chain Analysis in Pakistan CEP Market Including Entities, Margins, Role of Each Entity, Process Flow, Challenges and Other Aspects

10.3 Revenue Composition and Contribution Between First Mile/Mid Mile and Last Mile Delivery-Analysis for Domestic and International Shipments

10.4 Pakistan CEP Market Size on the Basis of Revenues and Shipments

10.5 Pakistan CEP Market Segmentation (Segmentation-Pakistan CEP)

10.5.1 Segmentation by Mails and Documents, E-Commerce Shipments and Express Cargo (Shipment Type Segmentation-Pakistan CEP)

10.5.2 Segmentation by International and Domestic Express

10.5.3 Segmentation by B2B, B2C and C2C

10.5.4 Segmentation by Period of Delivery

10.6 Competitive Landscape in Pakistan CEP Market

10.6.1 Overview and Genesis, Market Nature, Market Stage and Major Competing Parameters

10.6.2 Market Share of Companies in Pakistan CEP Market on the Basis of Revenues/Number of Shipments (Market Share-Pakistan CEP)

10.6.3 Market Share of Top Companies in Pakistan E-Commerce Shipment Market on the Basis of Revenues/Number of Shipments

10.6.4 Cross Comparison of Top Pakistan CEP Companies on the Basis of Parameters Including Company Overview, USP, Business Strategy, Future Plans, Technology, Number of Last Mile Delivery Shipments, Revenues, Major Clients, Number of Fleets, Number of Employees, Number of Riders, Number of Serviceable Locations, Major Service Offering and Other Parameters (Cross Comparison-Pakistan CEP)

10.7 Pakistan CEP Future Market Size on the Basis of Revenues and Shipments

10.8 Pakistan CEP Market Future Segmentation

10.8.1 Segmentation by Mails and Documents, E-Commerce Shipments and Express Cargo-Future (Future Shipment Type Split-Pakistan CEP)

10.8.2 Segmentation by International and Domestic Express-Future

10.8.3 Segmentation by B2B, B2C and C2C-Future

10.8.4 Segmentation by Period of Delivery-Future

11. End User Analysis

11.1 Customer Cohort Analysis and End User Paradigm for Different Industry Verticals-Telecommunications, FMCG, Automotive, Apparel, F&B, Construction and Pharmaceuticals (End User Cohorts-Pakistan)

11.2 Understanding Logistics Spend by End User

11.3 End User Preferences in Terms of In-House or Outsourcing Logistics Services and Reasons for Selection; Segregated by Size of Company on the Basis of Revenues

11.4 Major Logistics Companies Specialized in Serving Each Type of End User-Telecommunications, FMCG, Apparel, F&B, Construction and Pharmaceuticals

11.5 Detailed Landscape of Each End User Across Parameters Including Major Products Manufactured and Traded, Emerging Products, Type of Services Required, Type of Services Outsourced, Major Companies, Contract Duration, Likelihood to Recommend, Market Orientation, Major Clusters, Type of Sourcing Preference, Pain Points, Facilities/Services Required, Future Outlook; Market Size for End User Industry Verticals with Growth Rate (End User Profiles-Pakistan)

12. Pakistan Logistics and Warehousing Future Market Size

12.1 Basis Revenues (Pakistan Logistics and Warehousing Future Market Size)

13. Pakistan Logistics and Warehousing Future Market Segmentation

13.1 By Segment-Freight Forwarding, Warehousing, CEP and Value-Added Services (Future Segmentation by Service-Pakistan)

13.2 By End User Industries (Future Segmentation by End User-Pakistan)

13.3 Recommendation

13.4 Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities for the Pakistan Logistics and Warehousing Market. This includes logistics service providers, warehousing operators, transportation companies, regulatory bodies, and key end-user industries such as FMCG, e-commerce, pharmaceuticals, and manufacturing.

Basis this mapping, we shortlist leading 5–6 logistics and warehousing players in the country based on their financial performance, warehousing footprint, logistics network, and service offerings.

Sourcing is conducted using industry articles, public reports, proprietary databases, company websites, government bulletins, and trade publications to compile relevant data and insights.

Step 2: Desk Research

We undertake extensive desk research by referencing diverse secondary and proprietary databases to build a foundational understanding of the Pakistan logistics market.

This includes data aggregation on market size (by revenue), number of logistics operators, warehousing capacity, freight volumes, operational costs, regulatory environment, and technology adoption.

Company-level insights are drawn from press releases, annual reports, investor presentations, trade association reports, and government portals to understand financial performance, strategic initiatives, client base, and infrastructure.

We also review infrastructure development plans under CPEC, government logistics policies, and SEZ initiatives.

Step 3: Primary Research

A series of in-depth interviews are conducted with C-level executives and operations heads across leading logistics firms, warehousing operators, freight forwarders, cold chain providers, and major end-user industries.

The objective is to validate secondary data, gather granular operational insights, and understand market drivers, pricing structures, margins, and pain points in service delivery.

Bottom-to-top estimation methods are used to derive freight volumes and warehousing capacity per player, which are then aggregated to estimate market size and structure.

Disguised interviews are also conducted with sales teams and warehouse managers under the pretext of being potential customers to validate pricing, service standards, and warehouse space availability.

Step 4: Sanity Check

A combination of top-down and bottom-up modeling approaches is applied to test the consistency and accuracy of the market size estimations.

- Triangulation is performed between primary inputs, desk research data, and internal hypothesis to ensure coherence and realism across key market metrics.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Pakistan logistics and warehousing market is expected to grow significantly, reaching a projected valuation of PKR 2.1 Trillion by 2029. This growth is driven by increasing domestic consumption, expansion in e-commerce, manufacturing sector development, and ongoing infrastructure enhancements under initiatives like CPEC. The shift towards organized logistics and the integration of digital technologies further strengthen the market’s long-term potential.

The market is led by key players such as TCS Logistics, Agility Pakistan, DHL Supply Chain Pakistan, Ryder Pakistan, and BlueEx. These companies are recognized for their extensive logistics networks, warehousing infrastructure, and integrated service offerings. Other emerging players include Leopards Courier, PCL Logistics, and regional 3PLs specializing in e-commerce fulfillment.

Key growth drivers include increased demand from e-commerce, FMCG, and pharmaceutical sectors, government investment in trade corridors and dry ports, and the adoption of technology-driven logistics solutions. The National Freight and Logistics Policy and digital platforms like the Pakistan Single Window are also accelerating market efficiency and transparency.

The market faces several challenges including infrastructure limitations, high operational costs, and a dominance of informal logistics providers. Regulatory inconsistencies across provinces, lack of standardization in warehousing, and insufficient cold chain infrastructure also hinder service quality and scalability. Additionally, limited access to financing for small logistics firms remains a key constraint to modernization.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0