Philippines Alcoholic Drinks Market Outlook to 2029

By Market Structure, By Product Types (Beer, Wine, Spirits, Others), By Consumer Demographics, By Distribution Channels (On-trade, Off-trade), and By Region

Report Overview

Report Code

TDR0076

Coverage

Asia

Published

November 2024

Pages

80-100

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Philippines Alcoholic Drinks Market Outlook to 2029 - By Market Structure, By Product Types (Beer, Wine, Spirits, Others), By Consumer Demographics, By Distribution Channels (On-trade, Off-trade), and By Region” provides a comprehensive analysis of the alcoholic drinks market in the Philippines. The report covers an overview and genesis of the industry, the overall market size in terms of revenue, market segmentation, trends and developments, regulatory landscape, consumer profiling, challenges and issues, and a competitive landscape including key players, opportunities, and bottlenecks.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Philippines Alcoholic Drinks Market Outlook to 2029 - By Market Structure, By Product Types (Beer, Wine, Spirits, Others), By Consumer Demographics, By Distribution Channels (On-trade, Off-trade), and By Region” provides a comprehensive analysis of the alcoholic drinks market in the Philippines. The report covers an overview and genesis of the industry, the overall market size in terms of revenue, market segmentation, trends and developments, regulatory landscape, consumer profiling, challenges and issues, and a competitive landscape including key players, opportunities, and bottlenecks. The report concludes with future market projections based on sales revenue, market segmentation, regions, and case studies highlighting the major opportunities and challenges.

Philippines Alcoholic Drinks Market Overview and Size

The Philippines' alcoholic drinks market reached a valuation of PHP 500 billion in 2023, driven by rising disposable income, a young demographic, and increasing social acceptance of alcohol consumption. Major players include San Miguel Corporation, Ginebra San Miguel, Emperador, and Tanduay. These companies have solidified their positions through extensive distribution networks, strong branding, and a wide portfolio of products.

In 2023, San Miguel Brewery launched several limited-edition beer products to cater to the growing premium beer market, aiming to capture a segment of young urban consumers. Metro Manila, Cebu, and Davao are key markets due to their high population density, urbanization, and developed infrastructure.

Market Size for Philippines Alcoholic Drinks Industry on the Basis of Volume Sales in Liters, 2018-2024

Source: TraceData Research Analysis

What Factors are Leading to the Growth of the Philippines Alcoholic Drinks Market?

Economic Factors: Increased disposable income and economic recovery post-pandemic have boosted alcohol sales. In 2023, alcoholic beverages accounted for approximately 30% of total beverage sales in the Philippines. This growth is particularly noticeable in the beer segment, where both mass-market and premium brands have seen rising demand.

Demographic Shift: The expanding young population, particularly those aged 18-34, accounts for a large portion of alcohol consumption. In recent years, this demographic has been more open to trying new types of alcohol, especially premium brands. The urban population in this age group has grown by 8%, and this shift has directly influenced the demand for diverse alcoholic beverages.

Social Media Influence: Digital platforms have been instrumental in shaping consumer preferences, especially among younger audiences. Alcohol brands have increasingly turned to influencers and social media campaigns to market their products. In 2023, 35% of alcohol brands' marketing expenditure was allocated to digital channels.

Which Industry Challenges Have Impacted the Growth for the Philippines Alcoholic Drinks Market

Quality and Safety Concerns: Concerns about the quality and safety of locally produced and imported alcoholic drinks have posed significant challenges. A 2023 industry survey revealed that 45% of consumers are wary of counterfeit alcohol, which is a major issue in the unregulated segments of the market. This has negatively impacted consumer trust and reduced the willingness of some buyers to try new or unfamiliar brands.

Regulatory Constraints: Stringent government regulations on the production, distribution, and advertisement of alcoholic beverages have limited market growth. For instance, the Philippines imposes high excise taxes on alcoholic drinks, which raises prices and restricts access, particularly among price-sensitive consumers. In 2023, increased tax rates resulted in a 12% decline in sales of spirits and lower-priced beverages.

Public Health Campaigns and Restrictions: The government’s initiatives to reduce alcohol consumption through public health campaigns and stricter drinking age enforcement have posed challenges for market expansion. In addition, city ordinances restricting the sale of alcohol during certain hours and events like liquor bans during elections further limit sales opportunities. Data indicates that such restrictions have deterred up to 18% of potential buyers, particularly in rural and smaller urban areas.

What are the Regulations and Initiatives which have Governed the Market:

Alcohol Taxation Policies: The Philippine government imposes high excise taxes on alcoholic beverages, which vary by type and alcohol content. These taxes are adjusted annually, impacting pricing and consumption patterns. In 2023, the excise tax on spirits increased by 5%, leading to a noticeable slowdown in sales growth for low- to mid-tier spirits brands, as higher prices made these products less accessible to budget-conscious consumers.

Advertising Restrictions: The government enforces strict regulations on the advertising of alcoholic beverages, particularly regarding their promotion to younger audiences. Television, radio, and online ads are restricted during certain hours, and content must adhere to specific guidelines that prohibit targeting minors. In 2023, these restrictions were tightened, resulting in a 10% reduction in alcohol-related advertising spending.

Local Liquor Ban Ordinances: Several cities in the Philippines have implemented liquor bans during certain periods, including religious holidays, election seasons, and specific community events. These bans have led to temporary sales losses, particularly in urban areas. In 2023, the liquor ban during the election period resulted in a 15% drop in alcohol sales for that quarter.

Philippines Alcoholic Drinks Market Segmentation

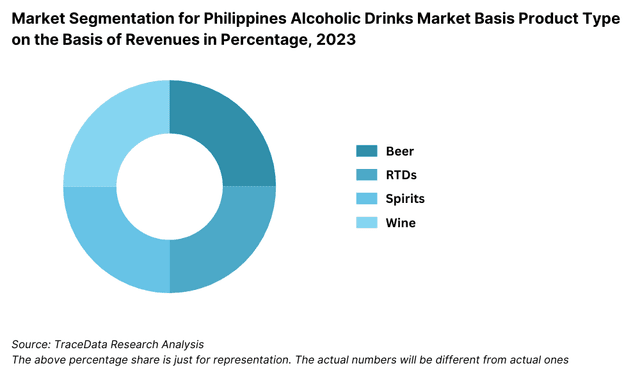

By Type of Drink: Beer dominates the alcoholic drinks market in the Philippines, accounting for over 60% of total consumption due to its affordability, accessibility, and strong cultural association with social gatherings. Spirits, particularly rum and gin, follow closely, driven by local brands like Tanduay and Ginebra San Miguel. Wine remains a smaller but growing segment, gaining popularity among higher-income consumers and urban professionals who are increasingly exploring imported and premium wine options.

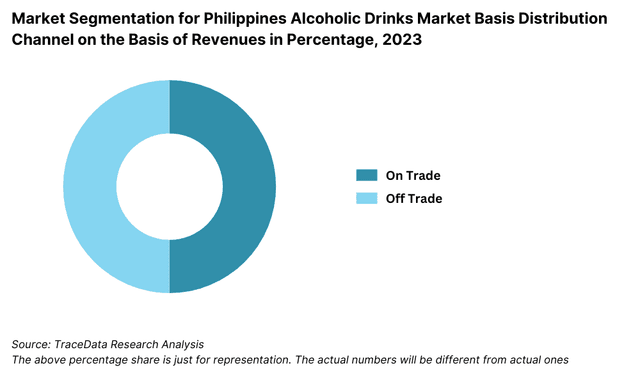

By Distribution Channel: Supermarkets and hypermarkets are the leading distribution channels, capturing over 40% of total sales due to their convenience and widespread presence. Convenience stores and sari-sari stores also play a significant role, especially in rural and suburban areas, where they serve as primary points of purchase for beer and low-priced spirits. Online sales of alcoholic beverages have grown rapidly in recent years, accounting for around 15% of total sales in 2023, driven by the increasing use of e-commerce platforms and mobile apps.

By Region: Metro Manila is the largest market for alcoholic beverages due to its dense population, high levels of disposable income, and vibrant nightlife. The Visayas and Mindanao regions also contribute significantly, with key cities like Cebu and Davao driving regional demand. Northern Luzon, while smaller in size, has seen steady growth due to rising consumer income and increasing penetration of modern retail channels.

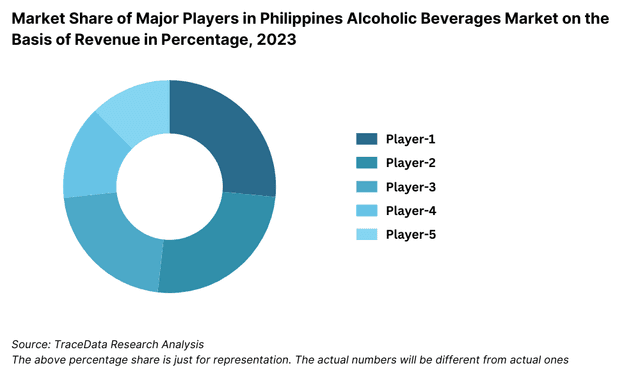

Competitive Landscape in the Philippines Alcoholic Drinks Market

The Philippines alcoholic drinks market is highly competitive, with several established players dominating key segments. However, the rise of new brands and the expansion of imported products have diversified the market, offering consumers more variety and premium options. Major players include San Miguel Corporation, Ginebra San Miguel, Emperador, and Tanduay, which maintain a strong presence across multiple product categories, including beer, spirits, and wine.

| Company Name | Establishment Year | Headquarters |

|---|---|---|

| San Miguel Brewery Inc. | 1890 | Mandaluyong, Philippines |

| Tanduay Distillers Inc. | 1854 | Manila, Philippines |

| Ginebra San Miguel Inc. | 1834 | Manila, Philippines |

| Heineken Philippines | 1864 | Amsterdam, Netherlands |

| Diageo Philippines | 1997 | London, United Kingdom |

| Emperador Distillers Inc. | 1979 | Quezon City, Philippines |

| Don Papa Rum (Bleeding Heart Rum Co.) | 2012 | Negros, Philippines |

| Pernod Ricard Philippines | 1975 | Paris, France |

| Bacardi Philippines | 1862 | Hamilton, Bermuda |

| AB InBev | 2008 | Leuven, Belgium |

Some of the recent competitor trends and key information about competitors include:

San Miguel Corporation: As the largest player in the alcoholic drinks market, San Miguel has a commanding presence in the beer segment, accounting for over 65% of the beer market in the Philippines. In 2023, the company introduced new premium craft beer options to cater to the growing interest in niche and higher-end products, marking a 12% increase in sales in this segment.

Ginebra San Miguel: Known for its iconic gin brand, Ginebra San Miguel reported a 20% rise in sales in 2023 due to strong demand for its flavored gin variants among younger consumers. The brand’s extensive distribution network and its affordable pricing have helped it maintain market dominance in the spirits category.

Emperador: Emperador, a global leader in brandy, reported a 15% growth in domestic sales in 2023, driven by increased marketing efforts and the introduction of premium brandy offerings. Its international acquisitions have also contributed to its reputation as a top-tier spirits producer, further enhancing its brand image.

Tanduay Distillers, Inc.: Tanduay remains the leading player in the rum segment, holding a significant market share both domestically and internationally. In 2023, the company experienced a 10% growth in exports, particularly to the U.S. market. Tanduay’s focus on digital marketing and partnerships with sports teams has increased brand visibility among younger audiences.

Asia Brewery: Competing primarily in the beer and RTD (ready-to-drink) segments, Asia Brewery saw an 18% growth in its flavored alcoholic beverage sales in 2023, driven by the popularity of its products among millennials. The company’s innovative marketing campaigns targeting younger consumers have helped it secure a foothold in the competitive market.

What Lies Ahead for the Philippines Alcoholic Drinks Market?

The Philippines alcoholic drinks market is expected to experience steady growth by 2029, driven by increasing consumer demand, evolving preferences for premium products, and expanding distribution networks. Several key trends are anticipated to shape the market's future:

Premiumization of Alcoholic Drinks: As disposable incomes rise and consumers develop a taste for higher-quality beverages, there will be a growing shift towards premium brands, particularly in the wine and spirits categories. This trend will be especially strong in urban areas, where young professionals are driving demand for premium and imported products.

Expansion of Ready-to-Drink (RTD) Products: The demand for convenient, ready-to-drink (RTD) alcoholic beverages is set to rise, particularly among younger consumers who prioritize convenience and new flavors. In 2023, RTD products grew by 12%, and this segment is expected to continue expanding as more brands introduce innovative flavors and marketing campaigns targeted at millennials and Gen Z consumers.

Rising Demand for Craft and Specialty Beers: Craft beer is gaining traction in the Philippines, particularly in major cities like Metro Manila, Cebu, and Davao. Local breweries and international craft brands are expected to see increased demand as consumers seek unique and high-quality beer experiences. By 2029, craft beer consumption is projected to account for a growing portion of the overall beer market.

Focus on Sustainability and Social Responsibility: As environmental awareness grows, there will be greater emphasis on sustainable practices within the alcoholic drinks market. Brands are expected to focus on eco-friendly packaging, reduced carbon footprints, and social responsibility campaigns. Companies that invest in sustainable sourcing and production methods are likely to resonate more with environmentally conscious consumers.

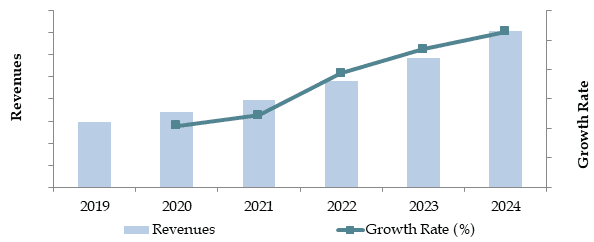

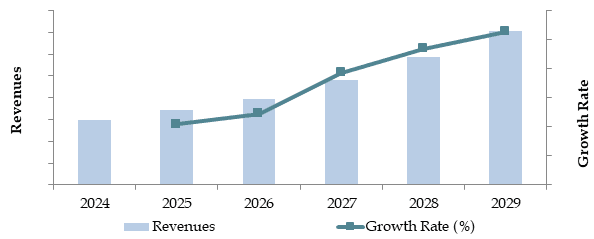

Future Outlook and Projections for Philippines Alcoholic Beverages Market on the Basis of Revenues in USD Billion, 2024-2029

Philippines Alcoholic Drinks Market Segmentation

- By Alcohol Type:

- Beer

- Spirits (Whiskey, Vodka, Rum)

- Wine (Red, White, Sparkling)

- Cider

- Ready-to-Drink (RTD) Cocktails

- By Beer

- Lager

- Dark Beer and others

- By Beer

- Craft

- Standard Beer

- By RTDs

- Malt based RTDs

- Spirit Based RTDs

- Wine Based RTDs

- Non-Alcoholic RTDs and others

- By Spirits

- Brandy

- Dark Rum

- White Rum

- Whiskies

- Gin

- Vodka and others

- By Vodka

- Flavoured

- Non-Flavoured Vodka

- By Wine

- Fortified Wine

- Champagne

- Other Sparkling Wine

- Red Wine

- White Wine and others

- By Distribution Channel:

- On-Trade (Bars, Restaurants, Hotels)

- Off-Trade (Supermarkets, Hypermarkets, Convenience Stores)

- By Price Segment:

- Economy

- Mid-Range

- Premium

- Super Premium

- By Consumer Age:

- 18-24

- 25-34

- 35-54

- 55+

- By Region:

- Metro Manila

- Luzon

- Visayas

- Mindanao

Players Mentioned in the Report:

- Kenya Breweries Ltd. (Tusker)

- KWAL (Kenya Wine Agencies Ltd.)

- East African Breweries Ltd. (EABL)

- Heineken

- Diageo PLC

- Distell Group

- Bila Shaka

Key Target Audience:

- Alcoholic Beverage Manufacturers

- Alcohol Distributors and Retailers

- Online Alcohol Marketplaces

- Regulatory Bodies (e.g., Food and Drug Administration, Department of Trade and Industry)

- Research and Development Institutions

Time Period:

- Historical Period: 2018-2023

- Base Year: 2024

- Forecast Period: 2024-2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-Role of Entities, Stakeholders, Gross Margins, and Challenges they Face

4.2. Business Model Canvas for Philippines Alcoholic Drinks Market

4.3. Consumer Buying Decision Process

5.1. Market Overview and Genesis

5.2. Number of Breweries and Microbreweries, as on Date

8.1. Revenues, 2018-2024

8.2. Sales Volume, 2018-2024

9.1. By Type (Beer, Cider, RTDs, Spirits and Wine), 2018-2023

9.1.1. By Beer (Lager, Dark Beer and others), 2018-2023

9.1.1.1. By Lager (Domestic Premium and Imported Premium), 2018-2023

9.1.1.2. By Craft and Standard Beer, 2018-2023

9.1.1.3. By Price (Super Premium, Premium, Standard and Economy), 2018-2023

9.1.2. By RTDs (Malt based RTDs, Spirit Based RTDs, Wine Based RTDs, Non-Alcoholic RTDs and others), 2018-2023

9.1.2.1. By Price (Super Premium, Premium, Standard and Economy), 2018-2023

9.1.3. By Spirits (Brandy, Dark Rum, White Rum, Whiskies, Gin, Vodka and others), 2018-2023

9.1.3.1. By Price (Super Premium, Premium, Standard and Economy), 2018-2023

9.1.3.2. By Flavoured and Non-Flavoured Vodka, 2018-2023

9.1.4. By Wine (Fortified Wine, Champagne, Other Sparkling Wine, Red Wine, White Wine and others), 2018-2023

9.1.4.1. By Price (Super Premium, Premium, Standard and Economy), 2018-2023

9.2. By Off Trade and On Trade for Each Type of Alcoholic Beverages, 2023

9.2.1. By Distribution Channel for Off Trade, 2023

9.3. By Province, 2023-2024P

10.1. Customer Landscape and Segment Analysis

10.2. Customer Journey and Decision-Making Process

10.3. Consumer Needs, Preferences, and Pain Points

10.4. Gap Analysis Framework

11.1. Trends and Developments in Philippines Alcoholic Drinks Market

11.2. Growth Drivers for Philippines Alcoholic Drinks Market

11.3. SWOT Analysis for Philippines Alcoholic Drinks Market

11.4. Issues and Challenges for Philippines Alcoholic Drinks Market

11.5. Government Regulations for Philippines Alcoholic Drinks Market

14.1. Market Share of Key Players in Alcoholic Beverages Market, 2023

14.2. Market Share of Key Players in Beer Market, 2023

14.3. Market Share of Key Players in Wine Market, 2023

14.4. Market Share of Key Players in Spirits Market, 2023

14.5. Market Share of Key Players in RTDs Market, 2023

14.6. Benchmark of Key Competitors in Philippines Alcoholic Drinks Market Basis 15-20 Operational and Financial Parameters

14.7. Strength and Weakness of Key Competitors

14.8. Operating Model Analysis Framework

14.9. Gartner Magic Quadrant for Market Positioning

14.10. Bowmans Strategic Clock for Competitive Advantage

15.1. Revenues, 2025-2029

15.2. Sales Volume, 2025-2029

16.1. By Type (Beer, Cider, RTDs, Spirits and Wine), 2025-2029

16.1.1. By Beer (Lager, Dark Beer and others), 2025-2029

16.1.1.1. By Lager (Domestic Premium and Imported Premium), 2025-2029

16.1.1.2. By Craft and Standard Beer, 2025-2029

16.1.1.3. By Price (Super Premium, Premium, Standard and Economy), 2025-2029

16.1.2. By RTDs (Malt based RTDs, Spirit Based RTDs, Wine Based RTDs, Non-Alcoholic RTDs and others), 2025-2029

16.1.2.1. By Price (Super Premium, Premium, Standard and Economy), 2025-2029

16.1.3. By Spirits (Brandy, Dark Rum, White Rum, Whiskies, Gin, Vodka and others), 2025-2029

16.1.3.1. By Price (Super Premium, Premium, Standard and Economy), 2025-2029

16.1.3.2. By Flavoured and Non-Flavoured Vodka, 2025-2029

16.1.4. By Wine (Fortified Wine, Champagne, Other Sparkling Wine, Red Wine, White Wine and others), 2025-2029

16.1.4.1. By Price (Super Premium, Premium, Standard and Economy), 2025-2029

16.2. By Off Trade and On Trade for Each Type of Alcoholic Beverages, 2025-2029

16.2.1. By Distribution Channel for Off Trade, 2025-2029

16.3. By Province, 2025-2029

17.1. Strategic Recommendations

17.2. Opportunity Identification

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

We begin by mapping the ecosystem to identify all demand-side and supply-side entities involved in the Philippines Alcoholic Drinks Market. Based on this ecosystem, we shortlist the leading 5-6 producers in the country, considering factors such as their financial information, production capacity, and volume of sales.

Industry articles, multiple secondary, and proprietary databases are utilized for desk research to gather industry-level information.

Step 2: Desk Research

An exhaustive desk research process is conducted by referencing a variety of secondary and proprietary databases. This process enables a comprehensive analysis of the market by aggregating key insights on factors such as sales revenue, number of market players, pricing levels, and demand trends.

The research also delves into company-level data, relying on sources like press releases, annual reports, financial statements, and other related documents. This approach helps us establish a foundational understanding of the market and the companies operating within it.

Step 3: Primary Research

We conduct a series of in-depth interviews with C-level executives and other stakeholders from various companies in the Philippines Alcoholic Drinks Market. The interviews serve multiple purposes: validating market hypotheses, authenticating statistical data, and gaining valuable operational and financial insights from industry representatives.

A bottom-to-top approach is used to evaluate volume sales for each player, which is then aggregated to estimate the overall market.

As part of the validation process, we carry out disguised interviews by approaching companies as potential customers. This strategy helps to cross-check the information provided by executives and compare it with secondary database insights, ensuring accuracy in understanding revenue streams, value chain dynamics, pricing strategies, and other operational factors.

Step 4: Sanity Check

- Bottom-to-top and top-to-bottom analyses, along with market size modeling exercises, are employed to ensure the accuracy and reliability of the market data and insights generated through the research process. This sanity check serves as the final validation step in confirming the robustness of our research findings.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Philippines alcoholic drinks market is expected to experience steady growth, with a market size projected to reach PHP 700 billion by 2029. This growth is fueled by factors such as rising disposable incomes, increasing urbanization, and shifting consumer preferences toward premium and craft beverages. Additionally, the expanding digital landscape has enabled greater access to a variety of alcoholic products through online channels.

Key players in the Philippines alcoholic drinks market include San Miguel Corporation, Ginebra San Miguel, Emperador, and Tanduay Distillers, Inc. These companies dominate the market through their extensive distribution networks, strong brand recognition, and diverse product offerings. Other notable players include Asia Brewery and Novellino Wines, which cater to niche segments such as RTD beverages and local wine.

The primary growth drivers include rising disposable income levels, a growing middle class, and the increasing social acceptance of alcohol consumption. Additionally, the trend toward premiumization and the expansion of e-commerce platforms have contributed to the market's growth by providing consumers with more options and convenient access to a variety of alcoholic beverages.

The Philippines alcoholic drinks market faces several challenges, including high excise taxes that raise product prices, regulatory restrictions on advertising and distribution, and the growing impact of public health campaigns. Furthermore, quality concerns related to counterfeit alcohol in unregulated segments of the market may also undermine consumer trust and slow growth in certain areas.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0