Philippines Car Rental and leasing Market Outlook to 2035

By Rental Duration, By Customer Type, By Vehicle Segment, By Service Model, and By Region

Report Overview

Report Code

TDR0503

Coverage

Asia

Published

January 2026

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Philippines Car Rental and Leasing Market Outlook to 2035 – By Rental Duration, By Customer Type, By Vehicle Segment, By Service Model, and By Region” provides a comprehensive analysis of the car rental and vehicle leasing industry in the Philippines. The report covers an overview and genesis of the market, overall market size in terms of value, detailed market segmentation; trends and developments, regulatory and operating landscape, customer-level demand profiling, key issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the Philippines car rental and leasing...

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Philippines Car Rental and Leasing Market Outlook to 2035 – By Rental Duration, By Customer Type, By Vehicle Segment, By Service Model, and By Region” provides a comprehensive analysis of the car rental and vehicle leasing industry in the Philippines. The report covers an overview and genesis of the market, overall market size in terms of value, detailed market segmentation; trends and developments, regulatory and operating landscape, customer-level demand profiling, key issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the Philippines car rental and leasing market.

The report concludes with future market projections based on tourism recovery and expansion, urban mobility trends, corporate fleet outsourcing, infrastructure development, ride-hailing substitution dynamics, regional demand drivers, cause-and-effect relationships, and case-based illustrations highlighting the major opportunities and cautions shaping the market through 2035.

Philippines Car Rental and Leasing Market Overview and Size

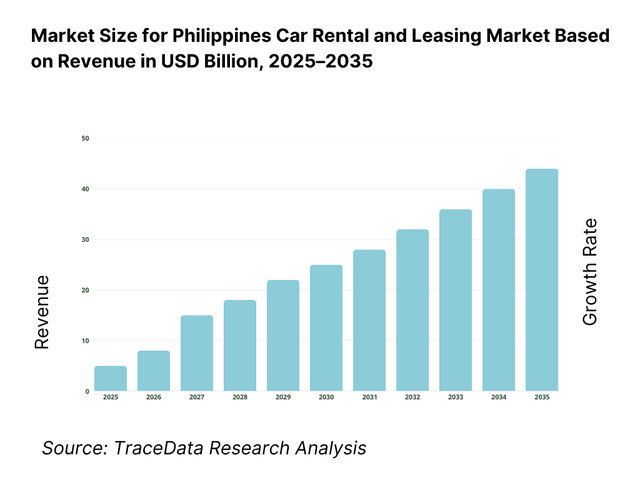

The Philippines car rental and leasing market is valued at approximately ~USD ~ billion, representing revenues generated from short-term self-drive rentals, chauffeur-driven rentals, long-term operating leases, and corporate fleet leasing services. The market spans a wide range of vehicle categories including economy cars, sedans, SUVs, vans, and light commercial vehicles, catering to tourists, corporate clients, government agencies, and urban consumers seeking flexible mobility solutions.

The market is anchored by the Philippines’ growing tourism economy, increasing business travel, expanding urban population, and rising preference for asset-light mobility among both individuals and enterprises. Car rental services play a critical role in serving domestic and international tourists across key gateways such as Metro Manila, Central Visayas, and Northern Mindanao, while leasing services are increasingly adopted by corporations to optimize fleet management, reduce capital expenditure, and improve operational flexibility.

The car rental and leasing market also benefits from the country’s improving road infrastructure, airport expansions, and inter-city connectivity projects, which collectively enhance the feasibility of self-drive and chauffeur-driven rental models. Additionally, the increasing penetration of digital booking platforms and app-based reservation systems has improved service accessibility, pricing transparency, and utilization rates across both organized and semi-organized operators.

Metro Manila represents the largest demand center for car leasing and chauffeur-driven rentals, driven by corporate offices, multinational companies, BPO operations, and government institutions. Tourist-driven rental demand is concentrated in regions such as Central Visayas (Cebu, Bohol), Western Visayas, Ilocos, and key leisure destinations, where short-term rentals and airport-based services dominate. Secondary cities and emerging urban clusters are witnessing gradual growth in long-term leasing as companies expand regional operations and adopt centralized fleet strategies.

What Factors are Leading to the Growth of the Philippines Car Rental and Leasing Market

Expansion of tourism, domestic travel, and air connectivity strengthens short-term rental demand: The Philippines continues to invest in tourism promotion, airport modernization, and regional air connectivity, leading to rising domestic and inbound travel volumes. Tourists increasingly prefer rental cars for flexibility in inter-city travel, island-hopping itineraries, and access to destinations with limited public transport coverage. Self-drive and chauffeur-driven rental services benefit from this trend, particularly in leisure-focused regions where convenience, time efficiency, and privacy are key decision criteria. The growth of airport-based rental counters and online pre-booking platforms further accelerates adoption among both domestic and international travelers.

Corporate preference for fleet outsourcing drives long-term leasing adoption: Companies across sectors such as BPO, pharmaceuticals, FMCG, logistics, utilities, and professional services are increasingly shifting from owned fleets to leased vehicles. Operating leases allow organizations to convert fixed capital costs into predictable operating expenses while outsourcing vehicle procurement, maintenance, insurance, and compliance to specialized leasing providers. This trend is particularly strong among large corporates and multinational firms operating in Metro Manila and major regional hubs, where fleet standardization, uptime reliability, and administrative efficiency are prioritized over vehicle ownership.

Urban congestion and changing mobility preferences increase reliance on flexible vehicle access: Rapid urbanization, traffic congestion, and rising vehicle ownership costs are influencing consumer attitudes toward car ownership in major Philippine cities. For specific use cases such as short-term business travel, weekend leisure trips, project-based assignments, or seasonal mobility needs, renting or leasing vehicles offers a cost-effective and flexible alternative. This behavioral shift supports steady demand for both short-duration rentals and medium-term leasing solutions, especially among young professionals, expatriates, and small businesses.

Which Industry Challenges Have Impacted the Growth of the Philippines Car Rental and Leasing Market:

Fleet acquisition costs, vehicle price inflation, and residual value uncertainty impact profitability and expansion planning: Car rental and leasing operators in the Philippines remain exposed to fluctuations in vehicle acquisition costs driven by import duties, currency movements, OEM pricing revisions, and supply constraints for specific models. Sudden increases in vehicle prices or limited availability of preferred models can delay fleet expansion decisions and compress margins, particularly for operators offering fixed-rate long-term leases. In addition, uncertainty around resale values and used vehicle demand affects lifecycle cost modeling, making it more challenging for less mature operators to accurately forecast depreciation and fleet replacement cycles.

Operational complexity, maintenance consistency, and service quality variability constrain scalability: While the rental and leasing model benefits from centralized fleet ownership, execution on the ground requires disciplined maintenance practices, availability of service networks, vehicle downtime management, and consistent customer service delivery. Smaller and regional operators often face challenges in maintaining uniform service standards across locations, particularly outside major urban centers. Variability in workshop quality, spare part availability, and driver availability for chauffeur-driven services can impact customer satisfaction and fleet utilization, limiting the ability of operators to scale operations efficiently.

Traffic congestion, infrastructure gaps, and regulatory inconsistencies affect utilization and customer experience: Severe traffic congestion in Metro Manila and other urban centers increases vehicle wear-and-tear, fuel consumption, and operating costs while reducing effective daily utilization. In some tourist and secondary regions, road quality, signage, and limited parking infrastructure constrain the attractiveness of self-drive rental options. Additionally, regulatory interpretation related to commercial vehicle usage, local permits, and enforcement practices can vary by municipality, creating compliance uncertainty for operators operating across multiple regions.

What are the Regulations and Initiatives which have Governed the Market:

Land transportation regulations and vehicle registration requirements governing commercial fleet operations: Car rental and leasing fleets must comply with national land transportation regulations covering vehicle registration, roadworthiness, insurance, and safety standards. Requirements related to periodic inspections, emission compliance, and commercial vehicle documentation directly affect operating costs and fleet availability. Operators offering chauffeur-driven services must also comply with driver licensing, employment, and accreditation norms, requiring ongoing monitoring and administrative coordination to maintain compliance across expanding fleets.

Taxation structures, import duties, and incentives shaping fleet acquisition economics: The Philippines’ vehicle taxation framework—including excise taxes, value-added tax, and import duties—plays a significant role in determining fleet acquisition costs and pricing competitiveness. Changes in tax slabs or incentives for specific vehicle categories can influence fleet composition decisions, such as the adoption of fuel-efficient or alternative powertrain vehicles. While incentives for electric and low-emission vehicles are emerging, infrastructure readiness and cost considerations continue to influence the pace of adoption within rental and leasing fleets.

Tourism promotion initiatives, infrastructure programs, and public-private mobility partnerships supporting demand creation: Government-led tourism promotion, airport expansion projects, and regional infrastructure development initiatives indirectly support growth in the car rental and leasing market by increasing travel volumes and improving inter-city connectivity. Public-private partnerships related to transport modernization, smart mobility initiatives, and regional development programs enhance the addressable market for organized rental and leasing operators. These initiatives encourage greater formalization of services, improved service standards, and increased participation of organized players in both tourist-driven and corporate mobility demand.

Philippines Car Rental and Leasing Market Segmentation

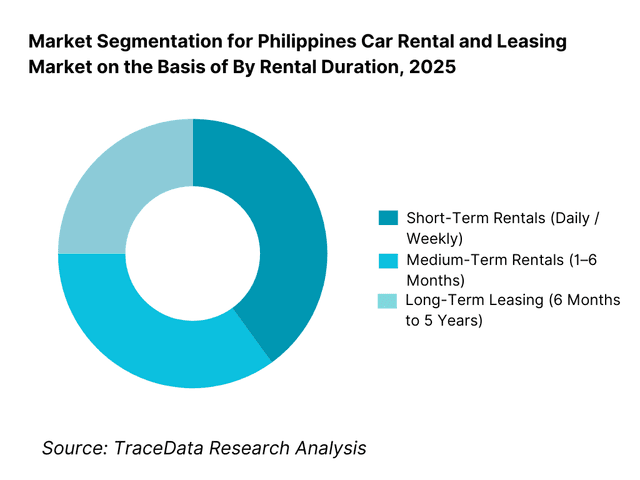

By Rental Duration: The short-term rental segment holds dominance in the Philippines car rental and leasing market. This is primarily driven by tourism activity, airport-based rentals, domestic leisure travel, and short-duration business trips. Short-term rentals align strongly with the needs of inbound tourists and domestic travelers who prioritize flexibility, convenience, and point-to-point mobility, particularly in regions with limited public transport connectivity. While long-term leasing is expanding steadily among corporate and institutional clients, short-term rentals continue to account for higher transaction volumes and fleet rotation frequency.

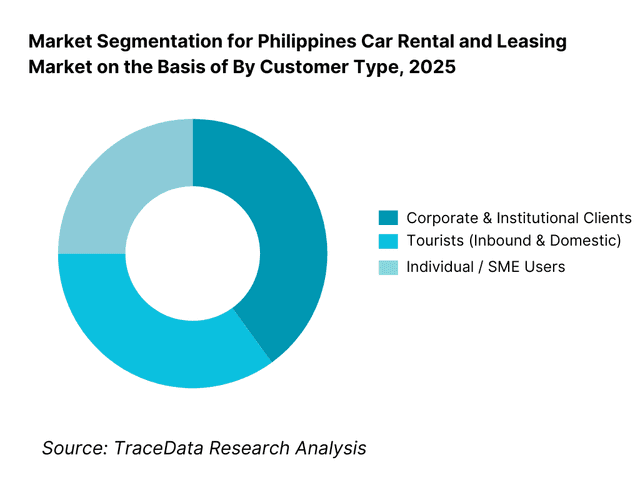

By Customer Type: Corporate and institutional customers dominate value-based demand in the Philippines car rental and leasing market, driven by long-term fleet leasing contracts, chauffeur-driven services, and centralized mobility outsourcing. These buyers prioritize reliability, service consistency, predictable costs, and nationwide coverage. Individual and tourist customers, while higher in volume, contribute a comparatively lower share of total market value due to shorter rental durations and price sensitivity.

Competitive Landscape in Philippines Car Rental and Leasing Market

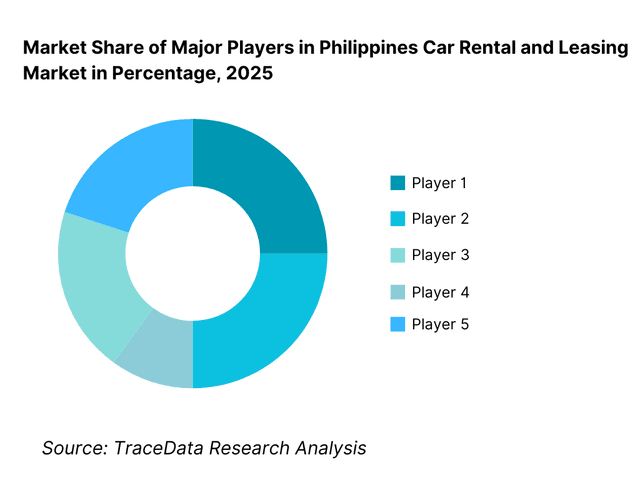

The Philippines car rental and leasing market exhibits moderate fragmentation, characterized by a mix of international brands, established national operators, and a large base of regional and local rental companies. Market competitiveness is shaped by fleet size, airport presence, corporate contracting capability, service reliability, pricing transparency, and digital booking integration. While international brands dominate airport locations and multinational corporate accounts, local players remain highly competitive in regional markets through localized knowledge, flexible pricing, and relationship-driven sales.

Large, organized players benefit from standardized processes, fleet renewal discipline, and centralized booking systems, whereas smaller operators compete on customization, regional availability, and cost competitiveness. The leasing segment shows higher consolidation relative to short-term rentals due to capital requirements, fleet management expertise, and long-term contract orientation.

Name | Founding Year | Original Headquarters |

Avis Philippines | 1946 | Manila, Philippines |

Hertz Philippines | 1918 | Manila, Philippines |

Budget Car Rental Philippines | 1958 | Manila, Philippines |

Diamond Rent-a-Car | 1992 | Manila, Philippines |

Europcar Philippines | 1949 | Manila, Philippines |

SafeRide Car Rental | 2003 | Cebu, Philippines |

Alpha Car Hire Philippines | 2010 | Manila, Philippines |

Enterprise Rent-A-Car Philippines | 1957 | Manila, Philippines |

Some of the Recent Competitor Trends and Key Information About Competitors Include:

Avis Philippines: Avis continues to leverage its global brand positioning and corporate relationships to secure long-term leasing and chauffeur-driven contracts, particularly among multinational corporations and institutional clients. Its competitive strength lies in standardized service delivery, airport presence, and fleet renewal discipline, making it a preferred partner for business travel and corporate mobility programs.

Hertz Philippines: Hertz maintains strong positioning in airport-based rentals and premium service offerings, benefiting from brand recognition among international travelers. The company emphasizes reliability, vehicle quality, and digital booking convenience, supporting steady demand from both inbound tourists and corporate travelers.

Budget Car Rental Philippines: Budget competes primarily on cost efficiency and value-driven offerings, targeting price-sensitive tourists and domestic travelers. Its simplified pricing structure and broad vehicle availability make it competitive in high-volume rental locations, particularly airports and urban centers.

Diamond Rent-a-Car: Diamond Rent-a-Car has built a strong local presence through diversified offerings across self-drive rentals, chauffeur-driven services, and corporate leasing. The company benefits from local market knowledge and flexible service models that cater to both individual and enterprise customers.

Europcar Philippines: Europcar focuses on serving international tourists and corporate accounts, emphasizing standardized service quality and fleet consistency. Its positioning is strongest in airport locations and major business hubs, where brand familiarity and service predictability influence customer choice.

What Lies Ahead for Philippines Car Rental and Leasing Market?

The Philippines car rental and leasing market is expected to expand steadily through 2035, supported by sustained growth in domestic and inbound tourism, increasing corporate fleet outsourcing, and evolving urban mobility preferences. As travel volumes recover and expand beyond traditional metro-centric patterns, demand for flexible, point-to-point mobility solutions is expected to remain strong. Long-term growth is further supported by infrastructure development, airport expansion, regional connectivity improvements, and the continued shift among businesses toward asset-light operating models. Car rental and leasing services are expected to remain a core mobility solution for tourists, corporates, and institutional users seeking cost predictability, operational flexibility, and service reliability.

Transition Toward Structured Corporate Leasing and Integrated Mobility Solutions: The future of the Philippines car rental and leasing market will see a gradual shift from transactional rentals toward more structured, long-term leasing and managed mobility solutions. Corporates are increasingly seeking bundled offerings that include vehicle supply, maintenance, insurance, replacement vehicles, driver management, and reporting under single contracts. This transition favors organized leasing players with fleet management expertise, financial strength, and nationwide service capability. As enterprises expand operations across multiple cities, standardized fleet programs with centralized procurement and service-level agreements will gain importance, strengthening the role of established leasing providers.

Growing Emphasis on Service Reliability, Fleet Quality, and Lifecycle Cost Optimization: As competition intensifies, customer decision-making will increasingly move beyond headline pricing toward total cost of use, uptime reliability, and service consistency. Fleet age, maintenance discipline, replacement response time, and customer support will become critical differentiators, particularly for corporate and institutional clients. Operators that invest in disciplined fleet renewal cycles, preventive maintenance systems, and data-driven utilization management will be better positioned to retain long-term clients and protect margins through economic cycles.

Increased Adoption of Digital Booking, Fleet Management, and Data-Driven Operations: Digitalization will play a central role in shaping the market through 2035. Online reservations, mobile applications, automated billing, GPS-based fleet tracking, and telematics-enabled maintenance planning will become standard expectations rather than value-added features. Corporate clients will increasingly demand usage analytics, cost transparency, and reporting dashboards to manage fleet efficiency and compliance. Operators that integrate customer-facing platforms with back-end fleet management systems will improve utilization, reduce downtime, and enhance scalability across regions.

Gradual Integration of Fuel-Efficient and Alternative Powertrain Vehicles into Rental Fleets: Rising fuel costs, environmental considerations, and emerging regulatory incentives will encourage gradual integration of fuel-efficient and alternative powertrain vehicles into rental and leasing fleets. While large-scale electric vehicle adoption may remain limited in the near term due to infrastructure constraints, hybrid and fuel-efficient models are expected to gain traction in urban and corporate fleets. Operators that proactively pilot and scale suitable vehicle types will benefit from lower operating costs and improved alignment with sustainability objectives of multinational and institutional clients.

Philippines Car Rental and Leasing Market Segmentation

By Rental Duration

• Short-Term Rentals (Daily / Weekly)

• Medium-Term Rentals (1–6 Months)

• Long-Term Leasing (6 Months to 5 Years)

By Customer Type

• Corporate & Institutional Clients

• Tourists (Inbound & Domestic)

• Individual / SME Users

By Vehicle Segment

• Economy & Compact Cars

• Sedans & Mid-Size Vehicles

• SUVs & MPVs

• Vans & Light Commercial Vehicles

• Premium & Luxury Vehicles

By Service Model

• Self-Drive Rentals

• Chauffeur-Driven Rentals

• Operating Lease / Fleet Leasing

• Managed Mobility & Corporate Transport Solutions

By Region

• Metro Manila

• Luzon (Excluding Metro Manila)

• Visayas

• Mindanao

Players Mentioned in the Report:

• Avis Philippines

• Hertz Philippines

• Budget Car Rental Philippines

• Diamond Rent-a-Car

• Europcar Philippines

• Regional car rental operators, corporate fleet leasing providers, and airport-based rental companies

Key Target Audience

• Car rental and fleet leasing companies

• Corporate fleet managers and procurement teams

• Tourism operators and travel service providers

• Airport authorities and transport infrastructure planners

• Multinational companies and BPO operators

• Government agencies and public sector institutions

• Mobility technology providers and fleet management solution vendors

• Private equity and mobility-focused investors

Time Period:

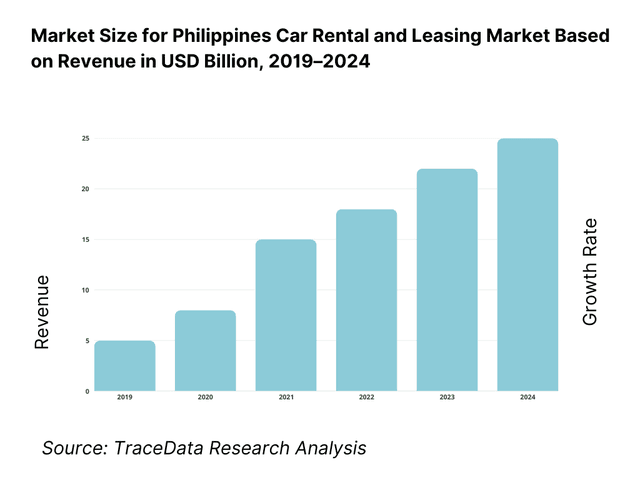

Historical Period: 2019–2024

Base Year: 2025

Forecast Period: 2025–2035

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4. 1 Delivery Model Analysis for Car Rental and Leasing including self-drive rentals, chauffeur-driven rentals, short-term rentals, long-term operating leases, and managed corporate mobility services with margins, preferences, strengths, and weaknesses

4. 2 Revenue Streams for Car Rental and Leasing Market including daily and weekly rental revenues, long-term lease contracts, chauffeur services, fleet management fees, and ancillary services

4. 3 Business Model Canvas for Car Rental and Leasing Market covering fleet owners, rental operators, leasing companies, corporate clients, travel partners, insurance providers, and maintenance partners

5. 1 International Car Rental Brands vs Regional and Local Players including global brands, national operators, airport-based rental companies, and regional or city-level players

5. 2 Investment Model in Car Rental and Leasing Market including fleet acquisition models, leasing versus ownership strategies, financing structures, and asset lifecycle management

5. 3 Comparative Analysis of Car Rental and Leasing Distribution by Direct Booking, Corporate Contracts, Travel Aggregators, and Airport or Hotel Partnerships

5. 4 Consumer Transportation Budget Allocation comparing car rentals and leasing versus ride-hailing, public transport, taxis, and private vehicle ownership with average spend per user per month

8. 1 Revenues from historical to present period

8. 2 Growth Analysis by rental duration, vehicle segment, and service model

8. 3 Key Market Developments and Milestones including airport expansions, tourism recovery initiatives, corporate leasing adoption, and regulatory updates

9. 1 By Market Structure including international brands, national operators, and local rental players

9. 2 By Rental Duration including short-term rentals, medium-term rentals, and long-term leasing

9. 3 By Service Model including self-drive rentals, chauffeur-driven rentals, and managed fleet services

9. 4 By Customer Type including corporate clients, tourists, and individual or SME users

9. 5 By Vehicle Segment including economy cars, sedans, SUVs and MPVs, vans and light commercial vehicles, and premium vehicles

9. 6 By Booking Channel including direct bookings, online travel platforms, corporate contracts, and airport or hotel counters

9. 7 By Usage Type including business travel, leisure tourism, employee transportation, and project-based mobility

9. 8 By Region including Metro Manila, Luzon (excluding Metro Manila), Visayas, and Mindanao

10. 1 Customer Landscape and Cohort Analysis highlighting tourists, corporate users, and urban mobility users

10. 2 Rental and Leasing Provider Selection and Purchase Decision Making influenced by pricing, vehicle availability, service reliability, and booking convenience

10. 3 Utilization and ROI Analysis measuring fleet utilization rates, average rental duration, and contract profitability

10. 4 Gap Analysis Framework addressing fleet mix gaps, service quality variations, and regional availability constraints

11. 1 Trends and Developments including growth of corporate leasing, digital booking platforms, and chauffeur-driven services

11. 2 Growth Drivers including tourism expansion, corporate outsourcing of fleets, and infrastructure development

11. 3 SWOT Analysis comparing international brand strength versus local market agility and cost competitiveness

11. 4 Issues and Challenges including fleet acquisition costs, traffic congestion, maintenance consistency, and regulatory variability

11. 5 Government Regulations covering vehicle registration, taxation, insurance requirements, and commercial transport regulations in the Philippines

12. 1 Market Size and Future Potential of long-term leasing and managed fleet services

12. 2 Business Models including operating leases, full-service leasing, and bundled mobility solutions

12. 3 Delivery Models and Type of Solutions including fleet management systems, telematics, and driver management services

15. 1 Market Share of Key Players by revenues and by fleet size

15. 2 Benchmark of 15 Key Competitors including international car rental brands, national leasing companies, airport-focused operators, and regional rental players

15. 3 Operating Model Analysis Framework comparing international franchise models, national fleet operators, and regional relationship-driven players

15. 4 Gartner Magic Quadrant positioning global mobility service providers and regional challengers in car rental and leasing

15. 5 Bowman’s Strategic Clock analyzing competitive advantage through service differentiation versus price-led mass rental strategies

16. 1 Revenues with projections

17. 1 By Market Structure including international, national, and local players

17. 2 By Rental Duration including short-term, medium-term, and long-term leasing

17. 3 By Service Model including self-drive, chauffeur-driven, and managed fleet services

17. 4 By Customer Type including corporate, tourist, and individual users

17. 5 By Vehicle Segment including economy, mid-size, SUVs, vans, and premium vehicles

17. 6 By Booking Channel including direct, online platforms, and corporate contracts

17. 7 By Usage Type including business, leisure, and employee transportation

17. 8 By Region including Metro Manila, Luzon, Visayas, and Mindanao

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

We begin by mapping the complete ecosystem of the Philippines Car Rental and Leasing Market across demand-side and supply-side entities. On the demand side, entities include inbound and domestic tourists, corporate enterprises, BPO operators, government agencies, SMEs, expatriates, and project-based users requiring short-term or long-term mobility solutions. Demand is further segmented by usage type (leisure travel, business travel, employee transportation, project deployment), rental duration (short-term, medium-term, long-term leasing), vehicle category, and service model (self-drive, chauffeur-driven, managed fleet services).

On the supply side, the ecosystem includes international car rental brands, national rental and leasing companies, regional and local operators, fleet leasing specialists, vehicle OEMs and distributors, financing and leasing partners, insurance providers, maintenance and service workshops, driver service providers, digital booking platforms, and regulatory authorities overseeing vehicle registration and commercial transport operations. From this mapped ecosystem, we shortlist 8–12 leading rental and leasing operators and a representative set of regional players based on fleet size, geographic coverage, airport presence, corporate contract penetration, service capability, and fleet renewal practices. This step establishes how value is created and captured across fleet acquisition, deployment, utilization, maintenance, customer service, and vehicle disposal.

Step 2: Desk Research

An exhaustive desk research process is undertaken to analyze the structure and evolution of the Philippines car rental and leasing market. This includes reviewing tourism arrival trends, domestic travel patterns, airport traffic growth, corporate mobility practices, urbanization dynamics, and infrastructure development programs. We assess customer preferences around flexibility, pricing transparency, service reliability, and vehicle availability across regions.

Company-level analysis includes review of operator fleet composition, service offerings, pricing structures, booking channels, airport concessions, and corporate leasing models. Regulatory and operating environments are examined, including vehicle taxation, registration norms, insurance requirements, and employment regulations impacting chauffeur-driven services. The outcome of this stage is a comprehensive industry foundation that defines segmentation logic and establishes base assumptions for market sizing, demand modeling, and long-term outlook development.

Step 3: Primary Research

We conduct structured interviews with car rental operators, fleet leasing companies, corporate fleet managers, travel management companies, tourism stakeholders, and vehicle service providers. The objectives are threefold: (a) validate assumptions around demand concentration, customer mix, and regional adoption patterns, (b) authenticate segment splits by rental duration, vehicle type, customer category, and service model, and (c) gather qualitative insights on pricing behavior, fleet utilization, maintenance challenges, driver availability, and customer expectations.

A bottom-to-top approach is applied by estimating fleet size, average utilization rates, rental yields, and contract values across key segments and regions, which are aggregated to develop the overall market view. In selected cases, disguised buyer-style interactions are conducted with rental operators to validate field-level realities such as booking lead times, pricing flexibility, service inclusions, vehicle condition standards, and replacement responsiveness.

Step 4: Sanity Check

The final stage integrates bottom-to-top and top-to-down approaches to cross-validate the overall market view, segmentation splits, and forecast assumptions. Demand estimates are reconciled with macro indicators such as tourism growth trajectories, corporate employment expansion, infrastructure investments, and vehicle sales trends. Assumptions around fleet growth, vehicle replacement cycles, utilization rates, and pricing sensitivity are stress-tested to assess their impact on market growth.

Sensitivity analysis is conducted across key variables including tourism recovery pace, corporate leasing adoption intensity, fuel cost volatility, regulatory changes, and regional infrastructure development. Market models are refined until alignment is achieved between operator fleet capacity, utilization potential, and customer demand patterns, ensuring internal consistency and robust directional forecasting through 2035.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Philippines car rental and leasing market holds strong long-term potential, supported by sustained growth in domestic and inbound tourism, increasing reliance on flexible mobility solutions, and rising adoption of fleet outsourcing among corporates and institutions. As infrastructure connectivity improves and travel patterns diversify beyond major urban centers, demand for both short-term rentals and long-term leasing is expected to expand steadily through 2035.

The market features a mix of international rental brands, established national operators, and a large base of regional and local players. Competition is shaped by fleet size, airport presence, corporate contracting capability, service reliability, pricing transparency, and digital booking integration. Organized operators with strong fleet management practices and nationwide coverage are increasingly gaining share, particularly in corporate leasing and airport-based rentals.

Key growth drivers include expansion of tourism and air connectivity, increasing business travel, rising preference for asset-light mobility models among corporates, and improving road and airport infrastructure. Additional momentum comes from digital booking adoption, centralized corporate fleet management, and growing demand for chauffeur-driven and managed mobility solutions across business and institutional users.

Challenges include high fleet acquisition costs, residual value uncertainty, traffic congestion in major cities, maintenance consistency across regions, and regulatory variability at local levels. Price-sensitive demand in the short-term rental segment can compress margins, while infrastructure gaps and enforcement inconsistencies can impact utilization and service quality. Managing fleet efficiency and service reliability across diverse geographies remains a key operational challenge.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0