Philippines Industrial Waste Water Treatment Market Outlook to 2029

By Centralized and Decentralized System, By Treatment Technology (Biological, Chemical, Physical, and Advanced), By End-User Industry (Manufacturing, Food & Beverage, Pharmaceuticals, Power Generation, Others), By Treatment Capacity, and By Region

Report Overview

Report Code

TDR0036

Coverage

Asia

Published

September 2024

Pages

80-100

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled "Philippines Industrial Waste Water Treatment Market Outlook to 2029 - By Centralized and Decentralized System, By Treatment Technology (Biological, Chemical, Physical, and Advanced), By End-User Industry (Manufacturing, Food & Beverage, Pharmaceuticals, Power Generation, Others), By Treatment Capacity, and By Region" provides a comprehensive analysis of the industrial wastewater treatment market in the Philippines.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled "Philippines Industrial Waste Water Treatment Market Outlook to 2029 - By Centralized and Decentralized System, By Treatment Technology (Biological, Chemical, Physical, and Advanced), By End-User Industry (Manufacturing, Food & Beverage, Pharmaceuticals, Power Generation, Others), By Treatment Capacity, and By Region" provides a comprehensive analysis of the industrial wastewater treatment market in the Philippines. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer-level profiling, issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities, bottlenecks, and company profiling of major players in the industrial wastewater treatment market. The report concludes with future market projections based on revenue, treatment capacity, treatment technology, end-user industry, region, cause-and-effect relationships, and success case studies highlighting major opportunities and challenges.

Philippines Industrial Waste Water Treatment Market Overview and Size

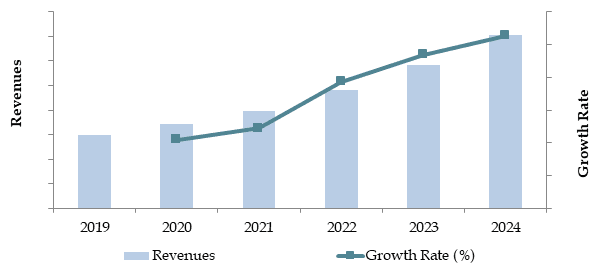

The Philippines industrial wastewater treatment market reached a valuation of PHP 23.5 billion in 2023, driven by rapid industrialization and the enforcement of stringent environmental regulations. The market is expected to grow at a CAGR of 7.8% from 2024 to 2029, fueled by increased investments in infrastructure and the growing focus on sustainable water management. Key players such as Manila Water, Maynilad Water, Veolia Water Philippines, and Ecosafe dominate the market, providing advanced treatment technologies and comprehensive services.

In 2023, Veolia Water Philippines expanded its decentralized treatment systems, which accounted for 15% of the market’s installations, targeting small-to-medium enterprises. Metro Manila and Calabarzon were responsible for 45% of the total market demand due to their high industrial concentration. Furthermore, water reuse practices grew by 10% year-over-year, highlighting a strong shift towards sustainable industrial practices in the region.

Market Size for Philippines Industrial Waste Water Treatment Market on the Basis of Revenue in USD Million, 2018-2024

Source: TraceData Research Analysis

What Factors are Leading to the Growth of the Philippines Industrial Waste Water Treatment Market:

Regulatory Pressure: The enforcement of strict environmental regulations, including the Clean Water Act of the Philippines, has been a primary driver of market growth. In 2023, over 70% of industrial companies in the country were mandated to adopt or upgrade their wastewater treatment facilities to meet new discharge standards, leading to a surge in demand for advanced treatment solutions.

Industrial Expansion: The rapid expansion of industries, especially in sectors such as manufacturing, food processing, and pharmaceuticals, has significantly increased the volume of wastewater generated. In 2023, the industrial wastewater output in the Philippines grew by 8%, creating a heightened need for effective treatment solutions to prevent environmental degradation.

Water Scarcity and Reuse Initiatives: Increasing water scarcity concerns have driven industries to focus on water reuse and recycling. In 2023, approximately 15% of industrial wastewater in the Philippines was treated and reused, a figure projected to grow as companies adopt more sustainable practices to mitigate water shortages and reduce operational costs.

Technological Advancements: The integration of advanced technologies, such as membrane filtration and reverse osmosis, has enhanced the efficiency and effectiveness of wastewater treatment. In 2023, these technologies accounted for 25% of all new installations, providing more robust and scalable solutions for complex industrial wastewater treatment requirements.

Which Industry Challenges Have Impacted the Growth of the Philippines Industrial Waste Water Treatment Market

High Capital Investment: The high upfront cost of establishing industrial wastewater treatment facilities is a significant barrier for many companies. In 2023, approximately 40% of small-to-medium enterprises (SMEs) in the Philippines cited financial constraints as a key challenge, limiting their ability to adopt modern wastewater treatment technologies. This has slowed the adoption of efficient treatment systems, especially among smaller industrial players.

Operational and Maintenance Costs: Industrial wastewater treatment systems require ongoing maintenance and operation, which can be expensive. In 2023, maintenance costs accounted for roughly 20% of the total expenses associated with operating these systems, making it a burden for industries with tight margins, especially in the manufacturing and food processing sectors.

Compliance with Regulations: While regulatory enforcement is driving market growth, compliance with increasingly stringent environmental standards presents a challenge for industries. In 2023, approximately 25% of industrial plants failed to meet the mandatory discharge standards during their first inspection, resulting in penalties and additional costs for system upgrades. This has caused delays in adopting newer technologies and increased operational pressures for companies.

Technological Complexity: The need for specialized technologies to treat diverse wastewater compositions has added complexity to the industry. In 2023, it was reported that 30% of industrial plants faced difficulties in implementing customized treatment solutions due to a lack of technical expertise, further slowing the market’s growth in certain sectors.

What are the Regulations and Initiatives that have Governed the Philippines Industrial Waste Water Treatment Market:

Environmental Compliance Regulations: The Philippines government, under the Clean Water Act (RA 9275), mandates strict discharge standards for industrial wastewater. Industries are required to obtain wastewater discharge permits and comply with the standards set for various contaminants, such as heavy metals and chemical oxygen demand (COD). In 2023, approximately 80% of industrial plants passed compliance inspections, reflecting a growing adherence to these regulations.

Water Reuse and Recycling Incentives: To encourage sustainable water practices, the government has introduced tax incentives and subsidies for industries that implement water reuse and recycling systems. In 2023, around 12% of industrial facilities adopted water recycling initiatives, benefiting from government support programs aimed at reducing the environmental impact of industrial activities.

Industrial Wastewater Management Programs: The Department of Environment and Natural Resources (DENR) has implemented various programs to promote the adoption of advanced wastewater treatment technologies. These programs focus on educating industries about the latest technologies, providing technical assistance, and facilitating partnerships with technology providers. In 2023, numerous companies participated in these programs, leading to an increase in the adoption of membrane filtration and reverse osmosis systems across key sectors.

Philippines Industrial Waste Water Treatment Market Segmentation

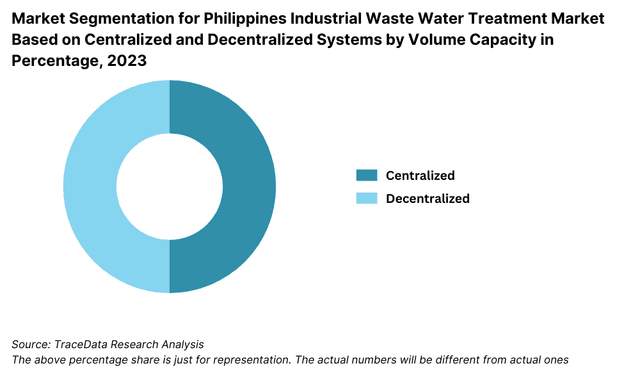

By Market Structure: Centralized treatment plants dominate the market, largely due to their capacity to handle large volumes of wastewater from industrial zones and metropolitan areas. Decentralized systems are growing in popularity, particularly among smaller industries in remote regions. These systems offer flexibility and lower initial capital investments, making them a preferred option for small-to-medium enterprises (SMEs).

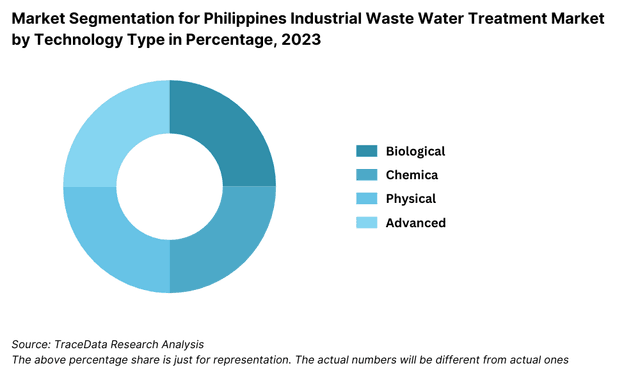

By Treatment Technology: Biological treatment methods are the most widely used, given their effectiveness in treating organic waste in industries such as food processing and manufacturing. Chemical treatments, including coagulation and disinfection, are commonly applied for industries dealing with hazardous chemicals. Advanced treatment technologies, such as membrane filtration and reverse osmosis, are increasingly being adopted, especially in high-tech industries like electronics and pharmaceuticals.

By End-User Industry: The manufacturing sector holds the largest share of the market, driven by the need to comply with stringent effluent regulations. The food & beverage industry is another significant contributor, where wastewater treatment is critical to meeting hygiene and safety standards. Other key sectors include pharmaceuticals, power generation, and textiles, each with specific treatment requirements depending on the nature of their waste.

Competitive Landscape in the Philippines Industrial Waste Water Treatment Market

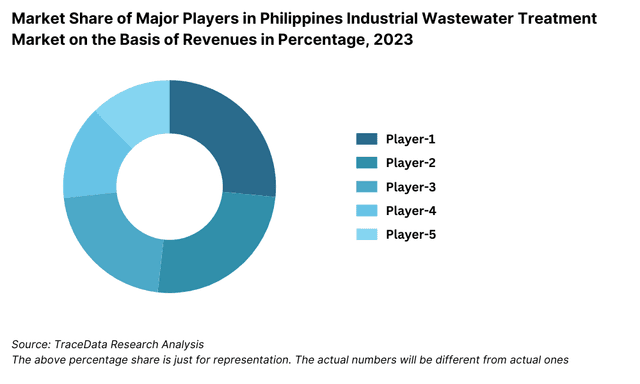

The industrial wastewater treatment market in the Philippines is moderately concentrated, with a mix of large domestic players and international companies competing in the space. Key players such as Manila Water, Maynilad Water, Veolia Water Philippines, and Ecosafe are well-established in the market, but the entry of new firms and increased focus on sustainable water management have diversified the industry, offering industries more specialized solutions.

| Name | Founding Year | Headquarters |

| Manila Water Company, Inc. | 1997 | Quezon City, Philippines |

| Maynilad Water Services, Inc. | 1997 | Pasig City, Philippines |

| Philippine Geothermal Production Co. | 1971 | Makati, Philippines |

| Balibago Waterworks System, Inc. | 1958 | Pampanga, Philippines |

| Veolia Water Philippines, Inc. | 1853 (Global) | Pasig City, Philippines |

| JFE Engineering Corporation (Philippines) | 1912 | Makati, Philippines |

| WATERKONSULT Equipment and Services | 2005 | Quezon City, Philippines |

| Ecolab Philippines | 1923 | Makati, Philippines |

| Envirokonsult Equipment and Services | 2004 | Pasig City, Philippines |

| PrimeWater Infrastructure Corp. | 1989 | Las Piñas, Philippines |

Some of the recent competitor trends and key information about competitors include:

Manila Water: Manila Water, one of the largest wastewater treatment companies in the country, expanded its industrial services division in 2023, securing contracts with major manufacturing companies. The company focuses on providing end-to-end solutions, including design, construction, and operation of treatment plants.

Maynilad Water: In 2023, Maynilad Water reported a 20% increase in revenues from industrial clients, driven by new contracts with food processing plants and manufacturing hubs in Luzon. The company’s expertise in large-scale treatment plants has allowed it to cater to the needs of heavy industries.

Veolia Water Philippines: Veolia recorded a 15% increase in installations of advanced treatment technologies, particularly in the electronics and pharmaceutical sectors. The company’s focus on innovation, such as introducing reverse osmosis systems for high-purity water needs, has solidified its market position.

Ecosafe: Ecosafe, known for its decentralized treatment systems, saw a 12% growth in sales in 2023, mainly driven by small-to-medium enterprises (SMEs). The company’s cost-effective and modular systems have gained popularity in remote industrial zones, where centralized treatment is not feasible.

What Lies Ahead for the Philippines Industrial Waste Water Treatment Market?

The Philippines industrial wastewater treatment market is projected to grow steadily by 2029, exhibiting a healthy CAGR during the forecast period. This growth is expected to be driven by rapid industrialization, tightening environmental regulations, and increasing awareness of sustainable water management practices.

Adoption of Advanced Treatment Technologies: The demand for advanced treatment technologies, such as membrane filtration, reverse osmosis, and biological treatment systems, is anticipated to rise as industries seek more efficient ways to treat complex wastewater streams. This trend will likely be propelled by the need for higher regulatory compliance and sustainability goals.

Expansion of Water Reuse Practices: The growing scarcity of water resources in the Philippines is expected to push more industries towards adopting water reuse and recycling practices. By 2029, a significant percentage of industrial wastewater is projected to be treated and reused, particularly in industries such as food processing, manufacturing, and power generation.

Growth in Decentralized Treatment Systems: With the ongoing expansion of SMEs in remote industrial areas, the demand for decentralized wastewater treatment systems is expected to increase. These systems offer cost-effective solutions for industries operating in locations where centralized treatment infrastructure is not feasible.

Focus on Environmental Sustainability: There is a rising trend towards sustainability in wastewater management, with companies increasingly adopting eco-friendly practices. This includes investments in energy-efficient technologies, water recycling systems, and the reduction of harmful effluents. These initiatives are anticipated to gain traction as industries align with global sustainability standards and consumer expectations.

Government Support and Incentives: Continued government initiatives, including subsidies and incentives for adopting water-efficient technologies and sustainable practices, will play a crucial role in shaping the future of the industrial wastewater treatment market. These programs are expected to further boost market growth and drive innovation across the industry.

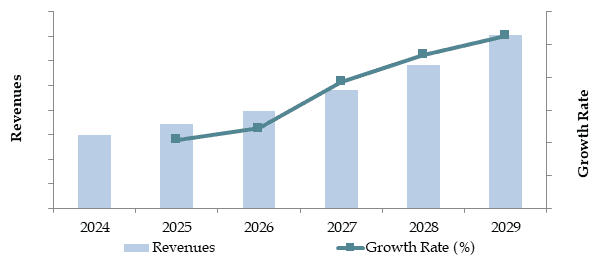

Future Outlook and Projections for Philippines Industrial Wastewater Treatment Market on the Basis of Revenues in USD Million, 2024-2029

Source: TraceData Research Analysis

Philippines Industrial Waste Water Treatment Market Segmentation

- By Market Structure:

- Centralized Treatment Plants

- Decentralized Treatment Systems

- Hybrid Systems

- Commercial Treatment Facilities

- By Treatment Technology:

- Biological Treatment (Aerobic, Anaerobic)

- Chemical Treatment (Coagulation, Disinfection)

- Physical Treatment (Sedimentation, Filtration)

- Advanced Treatment (Membrane Filtration, Reverse Osmosis)

- By End-User Industry:

- Manufacturing

- Food & Beverage

- Pharmaceuticals

- Power Generation

- Mining & Metals

- Textile

- Electronics

- By Treatment Capacity:

- <10,000 m³/day

- 10,000-50,000 m³/day

- 50,000-100,000 m³/day

- 100,000 m³/day

- By Region:

- Metro Manila

- Calabarzon

- Central Luzon

- Visayas

- Mindanao

- By Order intake:

- EPC Contracts

- O&M Contracts

Players Mentioned in the Report:

- Manila Water Company, Inc.

- Maynilad Water Services, Inc.

- Philippine Geothermal Production Co.

- Balibago Waterworks System, Inc.

- Veolia Water Philippines, Inc.

- JFE Engineering Corporation (Philippines)

- WATERKONSULT Equipment and Services

- Ecolab Philippines

- Envirokonsult Equipment and Services

- PrimeWater Infrastructure Corp.

Key Target Audience:

- Industrial Wastewater Treatment Service Providers

- Government Regulatory Bodies (e.g., DENR)

- Technology Providers

- Large Industrial Companies

- Research and Development Institutions

Time Period:

- Historical Period: 2018-2023

- Base Year: 2024

- Forecast Period: 2024-2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-“ Role of Entities, Stakeholders, and Challenges Faced

4.2. Revenue Streams for the Philippines Industrial Wastewater Treatment Market

4.3. Business Model Canvas for the Philippines Industrial Waste Water Treatment Market

4.4. Operating Margin in Philippines Waste Water Treatment System

5.1. Industrial Growth in the Philippines, 2018-2024

5.2. Waste Water Generation by Sector, 2018-2024

5.3. Investment in Waste Water Treatment Infrastructure, 2024

5.4. Number of Treatment Facilities by Location in the Philippines

8.1. Revenues, 2018-2024P

8.2. Wastewater Treatment Volume, 2018-2024P

8.3. Total CAPEX Requirement, 2018-2024P

9.1. By Market Structure (Centralized and Decentralized Systems), 2023-2024P

9.2. By Treatment Technology (Biological, Chemical, Physical, and Advanced), 2023-2024P

9.3. By End-User Industry (Manufacturing, Food & Beverage, Pharmaceuticals, Power Generation, Others), 2023-2024P

9.4. By Treatment Capacity (Small, Medium, Large), 2023-2024P

9.5. By Region (Metro Manila, Calabarzon, Central Luzon, Visayas, Mindanao), 2023-2024P

10.1. Customer Landscape and Cohort Analysis

10.2. Customer Journey and Decision Making

10.3. Needs, Desires, and Pain Points Analysis

10.4. Gap Analysis Framework

11.1. Trends and Developments in the Philippines Industrial Waste Water Treatment Market

11.2. Growth Drivers for the Philippines Industrial Waste Water Treatment Market

11.3. SWOT Analysis for the Philippines Industrial Waste Water Treatment Market

11.4. Issues and Challenges in the Philippines Industrial Waste Water Treatment Market

11.5. Government Regulations Governing the Market

14.1. Technology Used in Philippines Industrial Wastewater Treatment Market

14.2. Technology and Process in Wastewater Treatment Market

15.1. Market Share of Key Players in Philippines Industrial Wastewater Treatment Market Basis Revenues, 2023

15.2. Benchmark of Key Competitors in the Philippines Industrial Waste Water Treatment Market including Company Overview, USP, Business Strategies, Strengths, Weaknesses, Business Model, Treatment Capacity by Volume, Number of Plants, Major Clients, Recent Developments, Sourcing, and Value-Added Services

15.3. Strength and Weakness Comparison

15.4. Operating Model Analysis Framework

15.5. Gartner Magic Quadrant

15.6. Bowmans Strategic Clock for Competitive Advantage

16.1. Revenues, 2025-2029

16.2. Treatment Volume, 2025-2029

17.1. By Market Structure (Centralized and Decentralized Systems), 2025-2029

17.2. By Treatment Technology (Biological, Chemical, Physical, and Advanced), 2025-2029

17.3. By End-User Industry (Manufacturing, Food & Beverage, Pharmaceuticals, Power Generation, Others), 2025-2029

17.4. By Treatment Capacity (Small, Medium, Large), 2025-2029

17.5. By Region (Metro Manila, Calabarzon, Central Luzon, Visayas, Mindanao), 2025-2029

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Mapping the Ecosystem: We map the ecosystem by identifying both demand and supply side entities in the Philippines Industrial Waste Water Treatment Market. This includes treatment technology providers, industrial end-users, and regulatory bodies. Based on this ecosystem, we shortlist the leading 5-6 companies in the country by evaluating their market share, technology adoption, and treatment capacity.

Data Sourcing: Our data sourcing involves gathering information from industry reports, academic publications, proprietary databases, and government documents to ensure a comprehensive understanding of market trends and dynamics.

Step 2: Desk Research

Exhaustive Desk Research: We conduct thorough desk research using secondary sources such as industry articles, company websites, and research databases. This process involves analyzing market size, number of industry players, and demand patterns. Additionally, we examine company-level data through financial reports, press releases, and interviews with industry experts.

Data Aggregation: We aggregate this data to form a detailed understanding of the market structure, regulatory landscape, and emerging technologies in wastewater treatment. This allows us to validate key trends and identify growth opportunities.

Step 3: Primary Research

In-Depth Interviews: We conduct in-depth interviews with C-level executives and operational managers from key industrial wastewater treatment companies in the Philippines. These interviews help validate market assumptions, authenticate data from desk research, and provide insights into company strategies and challenges.

Disguised Interviews: We employ disguised interviews by posing as potential customers to validate company-provided data and gather further insights into pricing, operational efficiency, and technology adoption.

Volume Evaluation: A bottom-to-top approach is used to evaluate treatment volumes for each player, which are then aggregated to form the overall market size.

Step 4: Sanity Check

- Cross-Validation: We perform cross-validation through both top-to-bottom and bottom-to-top market modeling to ensure accuracy. The results are reviewed and adjusted based on feedback from industry insiders and data from secondary sources.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Philippines industrial wastewater treatment market is poised for substantial growth, with a projected CAGR of 7.8% from 2024 to 2029. This growth is driven by factors such as rapid industrialization, stricter environmental regulations, and increasing focus on water reuse and recycling practices across industries.

Key players in the market include Manila Water, Maynilad Water, Veolia Water Philippines, and Ecosafe. These companies lead the market due to their advanced treatment technologies, extensive client base, and ability to meet regulatory standards.

The primary growth drivers include stringent environmental regulations, rapid industrial expansion, and increasing water scarcity. Industries are now more focused on sustainable practices, such as water reuse and advanced treatment technologies, which are boosting market demand.

Major challenges include high capital investments required for setting up wastewater treatment systems, ongoing maintenance costs, and the complexity of treating diverse wastewater compositions across different industries. Additionally, smaller industries often face financial constraints that limit their ability to adopt modern technologies.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0