Philippines Logistics Market Outlook to 2035

By Service Type, By Mode of Transport, By End-User Industry, By Organization Size, and By Region

Report Overview

Report Code

TDR0502

Coverage

Asia

Published

January 2026

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Philippines Logistics Market Outlook to 2035 – By Service Type, By Mode of Transport, By End-User Industry, By Organization Size, and By Region” provides a comprehensive analysis of the logistics industry in the Philippines. The report covers an overview and genesis of the market, overall market size in terms of value, detailed market segmentation; trends and developments, regulatory and infrastructure landscape, buyer-level demand profiling, key issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the Philippines logistics market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Philippines Logistics Market Outlook to 2035 – By Service Type, By Mode of Transport, By End-User Industry, By Organization Size, and By Region” provides a comprehensive analysis of the logistics industry in the Philippines. The report covers an overview and genesis of the market, overall market size in terms of value, detailed market segmentation; trends and developments, regulatory and infrastructure landscape, buyer-level demand profiling, key issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the Philippines logistics market.

The report concludes with future market projections based on trade and consumption growth, e-commerce penetration, infrastructure modernization programs, port and airport capacity expansion, regional demand drivers, cause-and-effect relationships, and case-based illustrations highlighting the major opportunities and cautions shaping the market through 2035.

Philippines Logistics Market Overview and Size

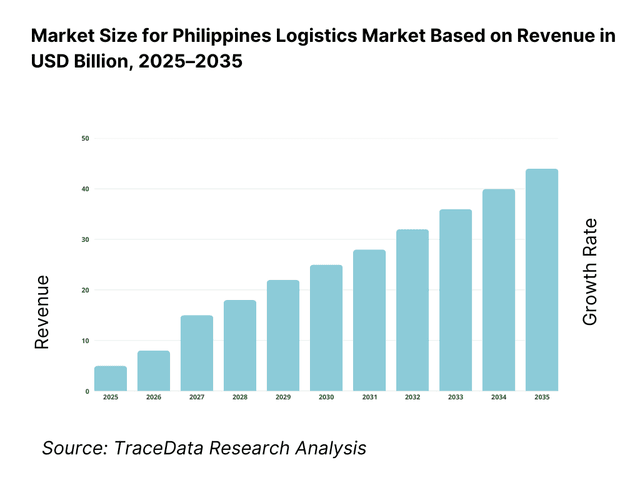

The Philippines logistics market is valued at approximately ~USD ~ billion, representing the total value of services associated with the movement, storage, handling, and distribution of goods across domestic and international supply chains. This includes freight transportation (road, sea, air, and rail where applicable), warehousing and distribution, freight forwarding, express and parcel services, cold chain logistics, and value-added logistics services such as packaging, labeling, and inventory management.

The market is anchored by the Philippines’ role as a consumption-driven economy, rising import dependence for manufactured goods and raw materials, growing export activity in electronics, agribusiness, and processed food, and the rapid expansion of domestic trade across its archipelagic geography. Logistics plays a critical enabling role due to the country’s dispersed island structure, which necessitates multimodal transport integration and strong inter-island shipping networks.

Growth in the logistics sector is further supported by increasing urbanization, the rise of organized retail and e-commerce platforms, and sustained public investment in transport infrastructure under national development programs. Warehousing demand is expanding near major urban centers, ports, and industrial zones as companies seek better inventory positioning, faster delivery cycles, and improved service reliability.

Luzon represents the largest logistics demand center in the Philippines, driven by Metro Manila’s dominance in consumption, manufacturing, and trade activity, as well as the presence of the country’s largest ports, airports, and logistics hubs. The Visayas region benefits from its strategic location for inter-island trade and growing regional distribution centers, while Mindanao is emerging as a high-potential market supported by agribusiness exports, food processing, and improving connectivity infrastructure. Despite strong demand fundamentals, logistics costs in the Philippines remain structurally high due to congestion, fragmented networks, and infrastructure gaps, shaping both pricing and service models across the market.

What Factors are Leading to the Growth of the Philippines Logistics Market:

Expansion of e-commerce, organized retail, and urban consumption strengthens logistics demand: The Philippines is witnessing rapid growth in e-commerce adoption, driven by rising smartphone penetration, digital payments, and a young, urbanizing population. This has significantly increased demand for express delivery, last-mile logistics, urban warehousing, and integrated fulfillment solutions. Retailers and online platforms are investing in distribution centers, sortation hubs, and city-level warehouses to reduce delivery times and manage high order volumes. Logistics service providers are adapting their networks to support same-day and next-day delivery models, particularly in Metro Manila and other Tier-1 cities, reinforcing demand for scalable and technology-enabled logistics services.

Trade growth, import dependence, and export-oriented sectors support freight and forwarding volumes: The Philippine economy remains heavily reliant on imports for consumer goods, intermediate inputs, and capital equipment, while exports such as electronics, semiconductors, agricultural products, and processed food continue to generate outbound freight demand. This trade profile drives steady volumes across international freight forwarding, port handling, customs brokerage, and inland transportation. As companies seek greater supply chain resilience and compliance with global standards, demand for organized logistics providers with end-to-end capabilities, documentation expertise, and multimodal coordination is increasing.

Infrastructure investments and logistics modernization initiatives improve long-term market outlook: Government-led infrastructure development, including port upgrades, airport expansion, road and expressway construction, and logistics park development, is gradually improving connectivity and capacity across the country. These investments are aimed at reducing bottlenecks, lowering logistics costs, and improving the efficiency of cargo movement between islands and economic centers. While execution challenges remain, improved infrastructure is enabling logistics companies to expand service coverage, develop regional hubs, and offer more reliable transit times, supporting long-term market growth.

Which Industry Challenges Have Impacted the Growth of the Philippines Logistics Market:

High logistics costs driven by infrastructure gaps, congestion, and fragmented networks impact service efficiency and competitiveness: The Philippines consistently faces higher logistics costs as a percentage of GDP compared to regional peers, largely due to road congestion in urban centers, limited intermodal integration, port inefficiencies, and the archipelagic nature of the country. Bottlenecks at major gateways such as Metro Manila ports lead to delays, increased dwell times, and higher trucking and demurrage costs. Fragmented logistics networks, especially across inter-island routes, further reduce scale efficiencies and make cost predictability difficult for shippers. These structural challenges limit the ability of logistics providers to offer consistent service levels and constrain margin expansion, particularly for price-sensitive sectors such as FMCG, agriculture, and retail.

Capacity constraints and operational inefficiencies across ports, warehouses, and last-mile delivery create service variability: While demand for logistics services has grown rapidly, capacity expansion across ports, warehousing facilities, and urban distribution infrastructure has not always kept pace. Congestion at ports, limited availability of modern warehousing near consumption centers, and insufficient cold chain capacity create operational bottlenecks. In last-mile delivery, high traffic density, informal addressing systems, and uneven service coverage increase delivery times and costs. These challenges reduce reliability and limit the scalability of express, e-commerce, and time-sensitive logistics services, particularly during peak demand periods.

Regulatory complexity, compliance requirements, and inter-agency coordination challenges increase operational friction: Logistics operations in the Philippines are influenced by multiple regulatory bodies overseeing customs, ports, transport, local government units, and environmental compliance. Variability in local regulations, permitting requirements, and enforcement practices across regions adds complexity for logistics providers operating nationwide networks. Customs clearance procedures, documentation requirements, and inspection protocols can introduce delays, particularly for international freight. Limited coordination across agencies further increases compliance costs and operational uncertainty, impacting overall supply chain efficiency.

What are the Regulations and Initiatives which have Governed the Market:

Transport, trade, and logistics regulations governing freight movement, port operations, and service compliance: The Philippines logistics market operates under a regulatory framework covering domestic and international freight movement, port and terminal operations, customs procedures, and transport safety standards. Regulations influence vessel operations, trucking permits, cargo handling standards, and service licensing for logistics providers. Compliance with these requirements shapes operating models, fleet utilization, and network design, particularly for companies offering multimodal and nationwide services. Regulatory oversight plays a central role in maintaining safety and service standards but can also extend approval timelines and increase documentation requirements.

Customs modernization, trade facilitation initiatives, and digitalization efforts shaping cross-border logistics: Government-led initiatives aimed at improving customs efficiency, enhancing transparency, and digitizing trade processes are influencing the evolution of the logistics market. Efforts to streamline customs clearance, improve risk-based inspections, and adopt electronic documentation systems are designed to reduce dwell times and improve predictability for importers and exporters. While implementation progress varies, these initiatives support long-term improvements in freight forwarding efficiency, cross-border trade facilitation, and international supply chain integration.

Infrastructure development programs and logistics-enabling public investments influencing market capacity: National infrastructure programs focused on ports, airports, roads, expressways, and logistics hubs are central to improving connectivity and reducing logistics costs over the long term. Investments in port modernization, regional airport upgrades, and road networks are intended to support inter-island trade, regional distribution, and export competitiveness. These initiatives influence where logistics providers locate warehouses, distribution centers, and regional hubs, shaping market structure and competitive dynamics. However, project execution timelines, funding constraints, and coordination challenges remain key factors affecting the pace at which regulatory intent translates into operational impact.

Philippines Logistics Market Segmentation

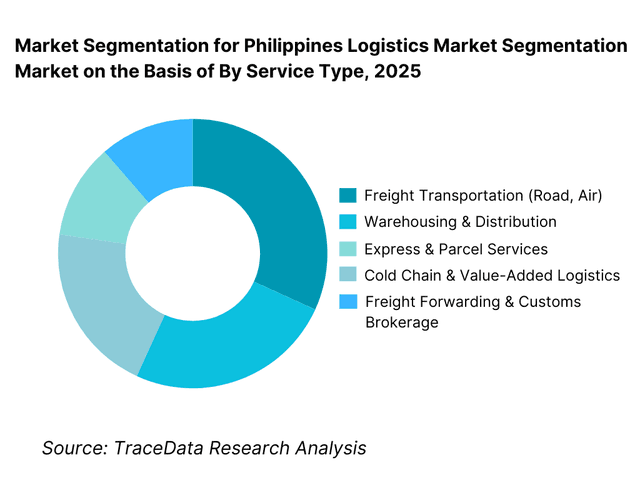

By Service Type: The freight transportation and warehousing segment holds dominance. This is because the Philippines’ logistics demand is fundamentally driven by domestic distribution, import-heavy consumption patterns, and inter-island cargo movement. Road freight, sea freight, and warehousing services form the backbone of supply chains for FMCG, retail, manufacturing, agriculture, and e-commerce players. Warehousing demand continues to expand near ports, urban consumption centers, and industrial zones as companies seek better inventory positioning and responsive delivery. While express, cold chain, and value-added logistics services are growing rapidly, core freight and storage services continue to account for the largest share of market value due to volume intensity and recurring demand.

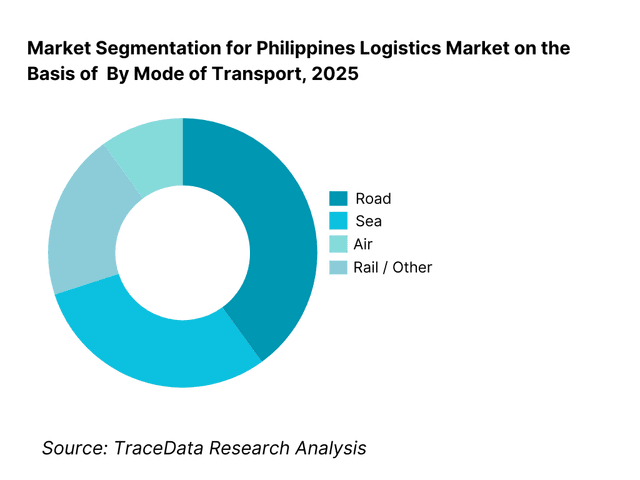

By Mode of Transport: Road and sea transport dominate the Philippines logistics market due to the country’s archipelagic geography and limited rail freight penetration. Road transport remains critical for first mile and last-mile connectivity, particularly in Luzon and major urban centers, while sea freight plays a central role in inter-island trade and bulk cargo movement. Air freight is used selectively for high-value, time-sensitive shipments such as electronics, pharmaceuticals, and perishables but remains limited by cost considerations.

Competitive Landscape in Philippines Logistics Market

The Philippines logistics market is highly fragmented, characterized by a mix of large integrated logistics providers, regional and local transport operators, shipping companies, warehouse owners, and specialized service providers. Market competition is shaped by network coverage, pricing flexibility, service reliability, port and warehouse access, and the ability to manage inter-island complexity. While large players dominate multinational accounts and end-to-end logistics contracts, small and mid-sized operators remain competitive in regional routes, niche services, and cost-sensitive segments.

Market leadership is increasingly influenced by investments in warehousing infrastructure, digital tracking systems, fleet modernization, and integrated service offerings. E-commerce growth has intensified competition in express delivery and last-mile logistics, while international freight forwarding remains driven by relationships, compliance capability, and service reliability.

Name | Founding Year | Original Headquarters |

Integrated Logistics Provider A | 1985 | Philippines |

Domestic Freight & Shipping Operator B | 1978 | Philippines |

International Freight Forwarder C | 1971 | Global |

Express & Parcel Logistics Company D | 2001 | Philippines |

Contract Logistics & Warehousing Provider E | 1994 | Philippines |

Regional Shipping Line F | 1966 | Philippines |

Some of the Recent Competitor Trends and Key Information About Competitors Include:

Integrated logistics providers: Large integrated players are expanding warehouse footprints near major ports and urban consumption hubs while strengthening end-to-end service capabilities. These companies are increasingly targeting long-term contracts with multinational manufacturers, retailers, and e-commerce platforms by offering bundled transportation, warehousing, and value-added services.

Express and last-mile delivery companies: Driven by e-commerce growth, express logistics players are investing in sortation centers, urban hubs, and digital platforms to improve delivery speed and order visibility. Competitive differentiation is increasingly based on delivery reliability, coverage density, and technology integration rather than price alone.

Domestic shipping and inter-island operators: Inter-island shipping companies continue to play a critical role in domestic trade, particularly for bulk cargo and regional distribution. Operators are gradually upgrading fleets and port handling capabilities to improve reliability, though capacity constraints and port congestion remain persistent challenges.

International freight forwarders: Global freight forwarders maintain a strong presence in international trade lanes, serving electronics, industrial goods, and export-oriented sectors. Their competitive positioning is reinforced by customs expertise, global network access, and the ability to manage complex documentation and compliance requirements.

What Lies Ahead for Philippines Logistics Market?

The Philippines logistics market is expected to expand steadily by 2035, supported by long-run consumption growth, rising e-commerce penetration, increasing trade volumes, and ongoing infrastructure modernization across ports, roads, airports, and regional connectivity corridors. Growth momentum is further enhanced by the continued formalization of supply chains, expanding warehousing footprints near key gateways and urban demand centers, and increasing preference for integrated, technology-enabled logistics models among manufacturers, retailers, and e-commerce platforms. As shippers seek improved reliability, visibility, and cost control across fragmented networks, organized logistics providers with scalable nationwide capabilities will strengthen their role across domestic and international cargo flows.

Transition Toward More Integrated, End-to-End Logistics and Contract Logistics Models: The future of the Philippines logistics market will see a continued shift from fragmented point-to-point transportation toward integrated service offerings that combine freight movement, warehousing, fulfillment, and value-added services. Large shippers will increasingly favor contract logistics arrangements to improve inventory positioning, reduce delivery lead times, and manage complexity across multi-island supply chains. Providers capable of offering bundled services with consistent service-level agreements, standardized processes, and nationwide execution will capture a larger share of enterprise accounts.

Growing Emphasis on Inter-Island Network Efficiency, Gateway Decongestion, and Regional Hub Development: A defining theme through 2035 will be the operational push to reduce congestion-related delays and improve cargo flow efficiency by developing stronger regional hubs and alternative gateways. Demand will rise for logistics configurations that reduce dependence on Metro Manila bottlenecks through hub-and-spoke distribution, cross-docking networks, and regional distribution centers in emerging growth corridors. Logistics players that build flexible inter-island routing capabilities and strengthen port-adjacent infrastructure access will be better positioned to deliver predictable transit times and cost performance.

Integration of Digital Tracking, Platform-Based Dispatch, and Visibility as a Competitive Differentiator: Digitalization will become a more central purchasing criterion, with buyers increasingly expecting real-time shipment visibility, electronic proof of delivery, integrated inventory tracking, and analytics-enabled performance reporting. Platform-based dispatch, route optimization, and warehouse management systems will expand across both large players and fast-scaling regional providers. Logistics companies that combine physical network scale with strong digital interfaces will improve customer stickiness and reduce service variability, especially in e-commerce, retail replenishment, and time-sensitive distribution.

Expansion of Cold Chain, Pharma-Grade Logistics, and Specialized Handling Capabilities: As food distribution modernizes and healthcare supply chains grow, demand for temperature-controlled and compliance-driven logistics will expand meaningfully. Cold chain warehousing, reefer transport, and controlled distribution for pharmaceuticals and high-value perishables will increasingly require higher standards of monitoring, packaging integrity, and facility certification. Providers that develop specialized capabilities—such as multi-temperature warehousing zones, last-mile cold delivery, and validated pharma distribution processes—will capture higher-margin segments and differentiate beyond commoditized transport.

Philippines Logistics Market Segmentation

By Service Type

• Freight Transportation (Road, Sea, Air)

• Warehousing & Distribution

• Freight Forwarding & Customs Brokerage

• Express & Parcel Services

• Cold Chain & Value-Added Logistics

By Mode of Transport

• Road

• Sea

• Air

• Rail / Other

By End-User Industry

• Retail, FMCG & E-commerce

• Manufacturing & Industrial

• Agriculture & Food Processing

• Pharmaceuticals & Healthcare

• Others

By Organization Size

• Large Enterprises / Multinationals

• Mid-Sized Enterprises

• Small Businesses / SMEs

By Region

• Luzon

• Visayas

• Mindanao

Players Mentioned in the Report:

• Integrated national logistics providers and contract logistics operators

• International freight forwarders and customs brokerage firms

• Domestic trucking and inter-island shipping operators

• Express delivery and last-mile logistics platforms

• Cold chain warehousing and temperature-controlled transport providers

• Regional warehousing developers and logistics park operators

Key Target Audience

• Logistics service providers (3PL/4PL), freight forwarders, and transport operators

• Warehousing developers, industrial park operators, and cold chain investors

• E-commerce platforms, retailers, and FMCG companies with nationwide distribution needs

• Manufacturers, importers, exporters, and supply chain heads across key industries

• Port, terminal, and inter-island shipping stakeholders

• Government agencies and infrastructure-linked policy stakeholders

• Private equity, infrastructure, and real estate investors tracking logistics capacity expansion

Time Period:

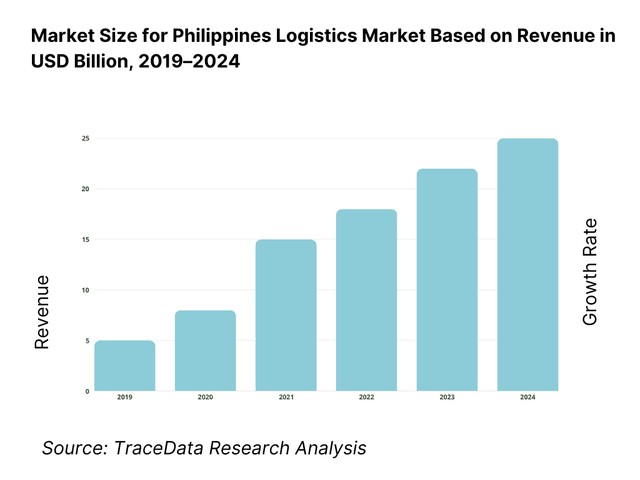

Historical Period: 2019–2024

Base Year: 2025

Forecast Period: 2025–2035

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4. 1 Logistics Service Delivery Model Analysis including asset-heavy logistics providers, asset-light 3PL/4PL models, freight forwarding-led models, express and last-mile delivery platforms, and integrated contract logistics models with margins, preferences, strengths, and weaknesses

4. 2 Revenue Streams for Logistics Market including freight transportation revenues, warehousing and storage revenues, freight forwarding and customs brokerage fees, express and parcel delivery charges, and value-added logistics services

4. 3 Business Model Canvas for Logistics Market covering shippers, logistics service providers, transport operators, warehouse developers, port and terminal operators, technology providers, and regulatory authorities

5. 1 Global Logistics Players vs Regional and Local Players including international 3PLs, regional freight forwarders, domestic trucking operators, inter-island shipping companies, and local warehousing providers

5. 2 Investment Model in Logistics Market including fleet investments, warehouse and logistics park development, technology and digital platform investments, and capacity expansion through partnerships or acquisitions

5. 3 Comparative Analysis of Logistics Service Delivery by Integrated End-to-End Providers versus Specialized Service Providers including transport-only, warehousing-only, and forwarding-focused models

5. 4 Logistics Cost Allocation Analysis comparing transportation, warehousing, handling, last-mile delivery, and administrative or compliance costs with average logistics spend as a percentage of sales

8. 1 Revenues from historical to present period

8. 2 Growth Analysis by service type and by mode of transport

8. 3 Key Market Developments and Milestones including port and airport upgrades, infrastructure projects, regulatory reforms, and major logistics investments

9. 1 By Market Structure including global logistics providers, regional players, and local operators

9. 2 By Service Type including freight transportation, warehousing and distribution, freight forwarding and customs brokerage, express and parcel services, and cold chain logistics

9. 3 By Mode of Transport including road, sea, air, and rail/other

9. 4 By End-User Industry including retail and e-commerce, FMCG, manufacturing, agriculture and food processing, pharmaceuticals and healthcare, and others

9. 5 By Organization Size including large enterprises, mid-sized enterprises, and SMEs

9. 6 By Shipment Type including B2B freight, B2C parcels, and project or bulk cargo

9. 7 By Service Criticality including standard logistics and time-sensitive or express logistics

9. 8 By Region including Luzon, Visayas, and Mindanao

10. 1 Shipper Landscape and Cohort Analysis highlighting enterprise shippers, e-commerce platforms, and SME demand clusters

10. 2 Logistics Service Provider Selection and Purchase Decision Making influenced by cost, service reliability, network coverage, and technology integration

10. 3 Service Utilization and ROI Analysis measuring delivery lead times, damage rates, service-level adherence, and total logistics cost impact

10. 4 Gap Analysis Framework addressing capacity gaps, infrastructure bottlenecks, cost inefficiencies, and service reliability challenges

11. 1 Trends and Developments including growth of e-commerce logistics, contract logistics adoption, cold chain expansion, and digitalization of logistics operations

11. 2 Growth Drivers including consumption growth, trade expansion, infrastructure development, and outsourcing of logistics functions

11. 3 SWOT Analysis comparing integrated logistics scale versus regional flexibility and cost competitiveness

11. 4 Issues and Challenges including congestion, high logistics costs, infrastructure gaps, and regulatory complexity

11. 5 Government Regulations covering customs procedures, transport regulations, port and terminal operations, and logistics-related compliance in the Philippines

12. 1 Market Size and Future Potential of express delivery, parcel logistics, and last-mile services

12. 2 Business Models including platform-based delivery, courier-led models, and hybrid asset-light approaches

12. 3 Delivery Models and Type of Solutions including hub-and-spoke networks, urban micro-fulfillment, and technology-enabled route optimization

15. 2 Benchmark of 15 Key Competitors including integrated logistics providers, international freight forwarders, express delivery companies, domestic transport operators, and cold chain specialists

15. 3 Operating Model Analysis Framework comparing asset-heavy logistics models, asset-light 3PL/4PL models, and platform-driven logistics players

15. 4 Gartner Magic Quadrant positioning global logistics leaders and regional challengers

15. 5 Bowman’s Strategic Clock analyzing competitive advantage through service differentiation versus cost-led logistics strategies

16. 1 Revenues with projections

17. 1 By Market Structure including global, regional, and local logistics providers

17. 2 By Service Type including transportation, warehousing, forwarding, express, and cold chain

17. 3 By Mode of Transport including road, sea, air, and others

17. 4 By End-User Industry including retail/e-commerce, manufacturing, agriculture, and healthcare

17. 5 By Organization Size including large enterprises, mid-sized firms, and SMEs

17. 6 By Shipment Type including B2B, B2C, and bulk/project cargo

17. 7 By Service Criticality including standard and time-sensitive logistics

17. 8 By Region including Luzon, Visayas, and Mindanao

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

We begin by mapping the complete ecosystem of the Philippines Logistics Market across demand-side and supply-side entities. On the demand side, entities include e-commerce platforms, FMCG and retail distributors, manufacturers and industrial shippers, importers and exporters, agribusiness and food processors, pharmaceutical and healthcare distributors, and government-linked procurement and relief supply chains. Demand is further segmented by shipment type (B2B palletized freight vs parcel shipments), service criticality (standard vs time-sensitive), temperature requirement (ambient vs cold chain), and operating geography (urban distribution vs inter-island routing).

On the supply side, the ecosystem includes integrated 3PL/4PL providers, freight forwarding and customs brokerage firms, domestic trucking fleets, inter-island shipping operators, air cargo service providers, warehouse and logistics park developers, express delivery and last-mile platforms, cold chain operators, port/terminal stakeholders, and enabling partners such as WMS/TMS technology providers and packaging/value-added service vendors. From this mapped ecosystem, we shortlist 6–10 leading organized logistics providers and a representative set of regional transport and warehousing operators based on network coverage, gateway access, service portfolio depth, fleet/warehouse scale, reliability reputation, and relevance across key shipper segments. This step establishes how value is created and captured across freight movement, storage, fulfillment, customs clearance, inter-island coordination, and service-level performance delivery.

Step 2: Desk Research

An exhaustive desk research process is undertaken to analyze the Philippines logistics market structure, demand drivers, and segment behavior. This includes reviewing domestic consumption patterns, e-commerce growth, port and airport throughput dynamics, inter-island cargo flow patterns, and infrastructure modernization activity influencing transit times and cost structure. We assess shipper preferences around delivery reliability, total landed logistics cost, visibility and tracking, claims and damage rates, and capacity availability during peak cycles.

Company-level analysis includes review of service portfolios (transportation, warehousing, forwarding, express, cold chain), geographic footprint, asset-light vs asset-heavy models, key customer verticals, and service differentiation through technology and operational processes. We also examine regulatory and compliance dynamics shaping cross-border trade and domestic freight movement, including customs processes, port operations, local permitting, and safety requirements. The outcome of this stage is a comprehensive industry foundation that defines the segmentation logic and creates the assumptions needed for market estimation and future outlook modeling.

Step 3: Primary Research

We conduct structured interviews with integrated logistics providers, freight forwarders, customs brokers, domestic transport operators, inter-island shipping stakeholders, warehouse developers, and enterprise shippers across retail/FMCG, manufacturing, e-commerce, agribusiness, and pharmaceuticals. The objectives are threefold: (a) validate assumptions around demand concentration, routing behavior, and procurement models, (b) authenticate segment splits by service type, transport mode, end-user industry, and regional routing patterns, and (c) gather qualitative insights on pricing behavior, capacity constraints, seasonality, port/terminal bottlenecks, last-mile delivery challenges, and service-level expectations.

A bottom-to-top approach is applied by estimating shipment volumes, average service pricing, and warehousing throughput across key end-use segments and regions, which are aggregated to develop the overall market view. In selected cases, disguised shipper-style interactions are conducted with transport operators and forwarders to validate field-level realities such as rate negotiation behavior, surcharge structures, typical turnaround times, documentation friction points, and service gaps between quoted transit times and real-world delivery performance.

Step 4: Sanity Check

The final stage integrates bottom-to-top and top-to-down approaches to cross-validate the market view, segmentation splits, and forecast assumptions. Demand estimates are reconciled with macro indicators such as trade growth trajectories, consumption expansion, industrial production trends, port and airport throughput shifts, and infrastructure-linked capacity additions. Assumptions around congestion impacts, fuel cost sensitivity, inter-island capacity availability, and warehouse expansion pace are stress-tested to understand their impact on service pricing and adoption of organized logistics providers.

Sensitivity analysis is conducted across key variables including e-commerce growth intensity, infrastructure execution pace, port decongestion effectiveness, cold chain adoption rates, and regulatory efficiency improvements. Market models are refined until alignment is achieved between service provider capacity, gateway throughput realities, and buyer shipment requirements, ensuring internal consistency and robust directional forecasting through 2035.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Philippines Logistics Market holds strong potential, supported by continued growth in consumption, rising e-commerce penetration, increasing trade volumes, and sustained infrastructure modernization across ports, roads, and regional connectivity. Demand for organized logistics is expected to rise as enterprises prioritize reliability, visibility, and nationwide service consistency across complex inter-island supply chains. Expansion in warehousing, last-mile delivery, and cold chain capacity is expected to create additional value capture opportunities through 2035.

The market features a mix of integrated logistics providers, international freight forwarders, domestic trucking and inter-island shipping operators, express delivery platforms, and specialized cold chain providers. Competition is shaped by network coverage, gateway access, service portfolio breadth, technology enablement, and the ability to deliver consistent service-level performance across Luzon, Visayas, and Mindanao. Larger organized players tend to dominate enterprise contracts, while regional operators remain competitive in specific routes and cost-sensitive segments.

Key growth drivers include expansion of e-commerce and last-mile delivery demand, increased reliance on outsourced logistics among retailers and manufacturers, steady import dependence and export flows supporting forwarding volumes, and improving infrastructure enabling broader regional distribution. Additional growth momentum comes from warehousing and fulfillment expansion near major consumption centers, increasing demand for temperature-controlled logistics in food and pharmaceuticals, and rising adoption of digital tracking and platform-based dispatch models.

Challenges include structurally high logistics costs driven by congestion and infrastructure gaps, capacity constraints across ports and modern warehousing, service variability in last-mile delivery, and operational complexity due to multi-island routing requirements. Regulatory and compliance friction, including documentation, inspection processes, and inter-agency coordination challenges, can also impact predictability—particularly for cross-border freight and gateway-linked domestic distribution.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0