Romania Logistics and warehousing Market Outlook to 2029

By Market Structure, By Mode of Transport, By End Users, By Type of Warehousing, By Third-Party Logistics, and By Region

Report Overview

Report Code

TDR0306

Coverage

Europe

Published

September 2025

Pages

80

On This Page

Report Overview

The report titled “Romania Logistics and Warehousing Market Outlook to 2029 - By Market Structure, By Mode of Transport, By End Users, By Type of Warehousing, By Third-Party Logistics, and By Region” provides a comprehensive analysis of the logistics and warehousing market in Romania. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer-level profiling, issues and challenges, and comparative landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the logistics and warehousing industry.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Romania Logistics and Warehousing Market Outlook to 2029 - By Market Structure, By Mode of Transport, By End Users, By Type of Warehousing, By Third-Party Logistics, and By Region” provides a comprehensive analysis of the logistics and warehousing market in Romania. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer-level profiling, issues and challenges, and comparative landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the logistics and warehousing industry. The report concludes with future market projections based on revenue, by market segments, logistics modes, and case studies highlighting the major opportunities and market barriers.

Romania Logistics and Warehousing Market Overview and Size

The Romania logistics and warehousing market reached an estimated value of RON 38 billion in 2023, driven by rising e-commerce penetration, infrastructure modernization, and increasing foreign direct investment in industrial parks. The market is anchored by players such as DHL Romania, DB Schenker, KLG Europe, FM Logistic, and FAN Courier. These companies leverage strategic regional hubs, multimodal logistics solutions, and advanced warehouse management systems to offer competitive supply chain services.

In 2023, FAN Courier announced the expansion of its new fulfillment center near Bucharest to cater to the growing demand from online retailers. Additionally, DB Schenker upgraded its warehousing automation systems to reduce lead time for intra-EU shipments. Bucharest, Cluj-Napoca, and Timișoara are among the key logistics clusters due to their population density, infrastructure, and proximity to major trade routes.

%252C%25202019-2024.png&w=640&q=75)

What Factors are Leading to the Growth of Romania Logistics and Warehousing Market:

Expansion of E-commerce: The Romanian e-commerce sector grew by over 15% YoY in 2023, creating higher demand for last-mile delivery and fulfillment warehousing. Leading players are investing in urban micro-fulfillment centers to meet same-day delivery expectations. Online retail is expected to contribute to over 25% of warehousing demand by 2025.

Infrastructure Development: The Romanian government, in coordination with the EU, has allocated significant funds under the Transport Operational Programme to improve road, rail, and intermodal infrastructure. The completion of major logistics corridors such as A1 and A3 highways has reduced transit times between key industrial cities, boosting regional freight volumes.

Strategic Location in Europe: Romania’s position on the EU’s eastern frontier and its proximity to Black Sea ports like Constanța make it a strategic logistics hub. With increasing nearshoring from Western Europe and supply chain diversification, Romania is emerging as a preferred location for cross-border 3PL and warehousing services.

Which Industry Challenges Have Impacted the Growth of Romania Logistics and Warehousing Market

Infrastructure Bottlenecks: Despite ongoing investments, Romania’s logistics infrastructure still faces challenges such as underdeveloped rural road networks, limited multimodal integration, and congestion in key urban corridors. As of 2023, only 55% of national roads were considered in “good” condition, slowing freight movement and increasing operational costs. These inefficiencies can lead to delays, particularly for time-sensitive sectors such as e-commerce and FMCG.

Labor Shortages and High Attrition: The logistics sector in Romania is struggling with a shortage of skilled labor, especially drivers, warehouse operators, and technicians. Industry data suggests a deficit of over 25,000 logistics workers in 2023, with a 15% attrition rate among warehouse staff. These human resource constraints impact service reliability and limit scalability for logistics providers.

Regulatory Complexity and Compliance Costs: Compliance with EU logistics regulations, including those related to emissions, working hours for drivers, and customs protocols for intra-EU and non-EU shipments, can increase operational complexity. Small and medium-sized logistics firms often cite high administrative overheads and lack of clarity in regulations as barriers to growth.

What are the Regulations and Initiatives Which Have Governed the Market

EU-Aligned Logistics and Emissions Regulations: Romania, as an EU member state, adheres to stringent transportation standards related to emissions (Euro VI norms), vehicle tracking, and electronic freight documents. These initiatives are aimed at harmonizing logistics practices across Europe. In 2023, over 80% of Romania’s trucking fleet met Euro VI standards, reducing the environmental impact of road freight.

National Recovery and Resilience Plan (NRRP): The Romanian government is allocating over €3.9 billion under the NRRP to improve transport and logistics infrastructure by 2026. Projects include the expansion of intermodal terminals, modernization of railway freight lines, and construction of bypass roads to decongest urban logistics routes. These developments are expected to boost logistics efficiency and reduce transit times.

Customs and Digital Trade Facilitation: Romania has implemented the EU Customs Data Model and introduced electronic clearance systems to streamline cross-border trade, especially at eastern borders with Ukraine and Moldova. As of 2023, over 70% of customs declarations were processed electronically, reducing average clearance time by up to 30%.

Romania Logistics and Warehousing Market Segmentation

By Market Structure: The Romanian logistics market is primarily dominated by unorganized or small and mid-sized domestic logistics providers. These firms benefit from deep local knowledge, cost-effective services, and flexibility in operations, making them the preferred choice for regional SMEs. However, the organized sector—comprising multinational 3PLs and integrated service providers—has been rapidly gaining share due to increased demand for end-to-end logistics, real-time tracking, and compliance-driven services. Major players in the organized sector such as DHL, DB Schenker, and KLG Europe are expanding operations through automation and multi-client warehouses.

%252C%25202023.png&w=640&q=75)

By Mode of Transport: Road freight remains the most dominant mode in Romania due to its flexibility, extensive domestic reach, and cost-effectiveness for last-mile delivery. Rail freight is witnessing a revival, supported by EU funding for intermodal development and increasing cross-border trade with Western Europe. Air and maritime modes, while limited in domestic share, play critical roles in international trade—particularly via the Port of Constanța and Bucharest Otopeni Airport, which are key nodes for automotive, machinery, and electronics shipments.

%252C%25202023.png&w=640&q=75)

By Type of Warehousing: Dry warehouses dominate Romania’s warehousing landscape, primarily serving FMCG, retail, and e-commerce sectors. However, demand for cold chain warehousing is increasing due to rising pharmaceutical, agri-food, and dairy exports. Additionally, value-added warehousing services like packaging, labeling, and returns management are gaining traction among 3PLs and large retailers to support omni-channel distribution.

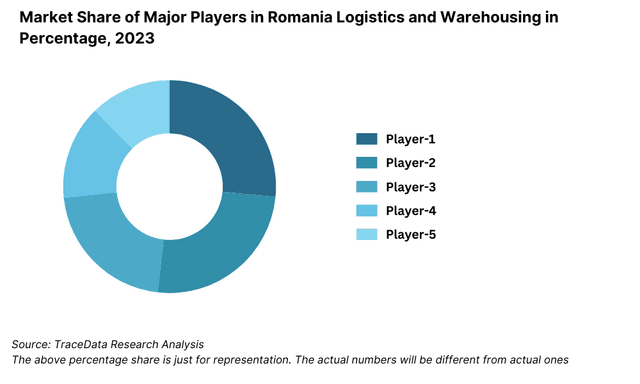

Competitive Landscape in Romania Logistics and Warehousing Market

The Romania logistics and warehousing market is moderately fragmented, with a mix of international 3PLs, domestic logistics providers, and niche warehousing operators. The entrance of global logistics giants, expansion of e-commerce-focused fulfillment providers, and increased investment in automation have significantly diversified the market landscape in recent years.

Company | Establishment Year | Headquarters |

DHL Romania | 1989 | Bucharest, Romania |

DB Schenker | 1872 (Global) | Bucharest, Romania |

FAN Courier | 1998 | Bucharest, Romania |

KLG Europe | 1918 (Global) | Cluj-Napoca, Romania |

FM Logistic | 1967 (Global) | Timișoara, Romania |

Some of the recent competitor trends and key information about competitors include:

DHL Romania: One of the most prominent players in the Romanian logistics landscape, DHL has invested heavily in express delivery, temperature-controlled logistics, and green warehousing. In 2023, DHL opened a new 13,000 sqm logistics hub near Bucharest Airport to support next-day cross-border deliveries across Central and Eastern Europe.

DB Schenker: DB Schenker reported over 10% growth in warehousing demand in Romania in 2023, fueled by rising demand from e-commerce and retail sectors. The company also introduced AI-based warehouse automation systems in its key facilities in Sibiu and Ploiești, improving efficiency and throughput times.

FAN Courier: As Romania’s largest domestic courier and fulfillment company, FAN Courier handles over 70 million parcels annually. In 2023, it launched a 3PL service targeting SMEs and cross-border retailers, offering bundled warehousing, last-mile delivery, and returns management.

KLG Europe: With strategic hubs in Cluj and Arad, KLG Europe focuses on B2B logistics, temperature-controlled transport, and intermodal freight solutions. In 2023, the company expanded its warehouse footprint by 15% to accommodate increasing volumes from the automotive and electronics sectors.

FM Logistic: FM Logistic operates multi-client distribution centers across Western Romania. In 2023, the company introduced value-added warehousing services such as co-packing, delayed differentiation, and e-commerce fulfillment, positioning itself as a flexible partner for omnichannel retail clients.

What Lies Ahead for Romania Logistics and Warehousing Market?

The Romania logistics and warehousing market is projected to witness steady growth through 2029, with a healthy CAGR driven by infrastructure development, rising domestic consumption, and increasing demand for integrated supply chain solutions. Romania’s strategic location in Eastern Europe and its growing role as a regional logistics hub are expected to further strengthen its market position.

Expansion of E-commerce and Last-Mile Infrastructure: As Romania’s e-commerce market continues to expand, logistics providers are expected to invest further in last-mile delivery infrastructure, including urban micro-warehouses and automated parcel lockers. By 2029, last-mile solutions are projected to account for over 30% of total logistics investments, driven by consumer demand for fast, flexible, and low-cost delivery options.

Growth in Cold Chain and Pharma Logistics: The rising demand for temperature-controlled logistics, especially in pharmaceuticals, food, and agriculture, will boost investment in cold storage infrastructure. With Romania emerging as a key distribution hub for Eastern Europe, the cold chain market is expected to grow rapidly, supported by EU funding and private investment.

Increased Automation and Smart Warehousing: Warehouse automation, including robotics, AI-powered inventory systems, and IoT tracking, will become mainstream across new Grade A facilities. These technologies will reduce operational costs, improve order accuracy, and enhance throughput, particularly in high-volume sectors like retail and consumer electronics.

Regional Integration and Cross-Border Freight Growth: Romania’s integration into EU-wide rail and road networks, including the Via Carpathia and Rhine-Danube corridors, will facilitate faster and more cost-effective cross-border freight. By 2029, Romania is expected to handle a significantly larger volume of transit shipments between Western Europe, the Balkans, and Central Asia.

%252C%25202024-2030_ICApfEu.png&w=640&q=75)

Romania Logistics and Warehousing Market Segmentation

• By Market Structure:

o Local Freight Forwarders

o Regional/National 3PL Providers

o Multinational Logistics Companies (4PL)

o Fulfillment and E-commerce Logistics Providers

o Organized Sector

o Unorganized Sector

o Cold Chain Operators

• By Mode of Transport:

o Road Freight

o Rail Freight

o Air Cargo

o Maritime Freight

o Multimodal Transport

• By Type of Warehousing:

o Dry Warehouses

o Cold Storage Facilities

o Bonded Warehouses

o Automated/Smart Warehouses

o Value-Added Warehousing (e.g., packaging, labelling)

• By End-User Industry:

o E-commerce and Retail

o Automotive

o FMCG and Consumer Durables

o Pharmaceuticals and Healthcare

o Agriculture and Food Processing

o Electronics and High-Tech

o Construction and Industrial Goods

• By Region:

o Bucharest-Ilfov

o North-West (Cluj, Bihor)

o West (Timiș, Arad)

o South (Prahova, Giurgiu)

o East (Iași, Suceava)

o South-East (Constanța, Galați)

o Center (Brașov, Sibiu)

Players Mentioned in the Report:

• DHL Romania

• DB Schenker

• FAN Courier

• KLG Europe

• FM Logistic

• CTP Romania

• WDP Romania

• Gebrüder Weiss Romania

• Sameday Courier

• DSV Romania

Key Target Audience:

• 3PL and 4PL Logistics Providers

• E-commerce and Retail Chains

• Real Estate Developers (Logistics Parks, Industrial Warehousing)

• Regulatory Bodies (e.g., Ministry of Transport and Infrastructure, Romanian Customs Authority)

• Cold Chain Service Providers

• Freight Forwarders and Supply Chain Consultants

• Investors and Private Equity Firms

• Research and Development Institutions

Time Period:

• Historical Period: 2018–2023

• Base Year: 2024

• Forecast Period: 2024–2029

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Table of Contents

1. Executive Summary

2. Research Methodology

3. Ecosystem of Key Stakeholders in Romania Logistics and Warehousing Market

4. Value Chain Analysis

4.1. Value Chain Process-Role of Entities, Stakeholders, and Challenges They Face

4.2. Revenue Streams for Romania Logistics and Warehousing Market

4.3. Business Model Canvas for Romania Logistics and Warehousing Market

4.4. Logistics Service Decision-Making Process

4.5. Warehousing and Fulfillment Decision-Making Process

5. Market Structure

5.1. Total Freight Movement in Romania (Million Tons), 2018-2024

5.2. Modal Share (Road, Rail, Air, Sea) of Logistics in Romania, 2018-2024

5.3. Warehousing Capacity and Absorption Trends, 2018-2024

5.4. Number of Logistics Service Providers by Type and Region

6. Market Attractiveness for Romania Logistics and Warehousing Market

7. Supply-Demand Gap Analysis

8. Market Size for Romania Logistics and Warehousing Market Basis

8.1. Revenues, 2018-2024

8.2. Freight Volume (Million Tons), 2018-2024

8.3. Warehousing Stock (Million sq. m.), 2018-2024

9. Market Breakdown for Romania Logistics and Warehousing Market Basis

9.1. By Market Structure (Organized and Unorganized), 2023-2024P

9.2. By Mode of Transport (Road, Rail, Air, Sea), 2023-2024P

9.3. By Type of Warehousing (Dry, Cold, Bonded, Value-Added), 2023-2024P

9.4. By End-User Industry (E-commerce, FMCG, Automotive, etc.), 2023-2024P

9.5. By Region (Bucharest, West, North-West, etc.), 2023-2024P

9.6. By Warehouse Grade (A, B, C), 2023-2024P

10. Demand Side Analysis for Romania Logistics and Warehousing Market

10.1. End-User Landscape and Cohort Analysis

10.2. Customer Journey and Vendor Selection Criteria

10.3. Needs, Preferences, and Pain Point Analysis

10.4. Gap Analysis Framework

11. Industry Analysis

11.1. Trends and Developments in Romania Logistics and Warehousing Market

11.2. Growth Drivers for Romania Logistics and Warehousing Market

11.3. SWOT Analysis for Romania Logistics and Warehousing Market

11.4. Issues and Challenges in Romania Logistics and Warehousing Market

11.5. Government Regulations and Infrastructure Initiatives

12. Snapshot on E-commerce and Retail Fulfillment Market

12.1. Market Size and Growth Potential for E-commerce Fulfillment, 2018-2029

12.2. Business Models and Revenue Streams

12.3. Cross Comparison of Leading Fulfillment Providers (Facility Size, Client Mix, Tech Adoption, etc.)

13. Romania Cold Chain and Temperature-Controlled Logistics Market

13.1. Size and Capacity of Cold Storage Market, 2018-2024

13.2. End-User Demand (Pharma, Food, Agri) and Growth Outlook

13.3. Regulatory Standards and Compliance Environment

13.4. Cold Chain Providers and Market Structure

14. Opportunity Matrix for Romania Logistics and Warehousing Market-Presented with Radar Chart

15. PEAK Matrix Analysis for Romania Logistics and Warehousing Market

16. Competitive Landscape for Romania Logistics and Warehousing Market

16.1. Benchmarking of Key Players: DHL, DB Schenker, FAN Courier, FM Logistic, etc.

16.2. Company Strengths and Weaknesses

16.3. Operating Model Comparison

16.4. Gartner Magic Quadrant Positioning

16.5. Bowman’s Strategic Clock-Competitive Strategy Mapping

17. Future Market Size for Romania Logistics and Warehousing Market Basis

17.1. Revenues, 2025-2029

17.2. Freight Volume (Million Tons), 2025-2029

17.3. Warehousing Stock (Million sq. m.), 2025-2029

18. Market Breakdown for Romania Logistics and Warehousing Market Basis

18.1. By Market Structure (Organized and Unorganized), 2025-2029

18.2. By Mode of Transport (Road, Rail, Air, Sea), 2025-2029

18.3. By Type of Warehousing (Dry, Cold, Bonded, Value-Added), 2025-2029

18.4. By End-User Industry, 2025-2029

18.5. By Region, 2025-2029

18.6. By Warehouse Grade (A, B, C), 2025-2029

18.7. Strategic Recommendations

18.8. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the logistics and warehousing ecosystem and identify all key demand-side (e.g., e-commerce companies, manufacturers, FMCG firms) and supply-side entities (e.g., 3PLs, freight forwarders, warehouse developers) operating in the Romania Logistics and Warehousing Market. Based on this ecosystem, we shortlist 5–6 leading logistics providers in the country based on parameters such as fleet size, warehouse capacity, geographic reach, service offerings, and financial performance.

Sourcing is conducted through industry publications, European logistics databases, Romanian government portals, logistics trade associations, and proprietary secondary sources to gather macro-level market information.

Step 2: Desk Research

An exhaustive desk research process is undertaken using both secondary and proprietary databases. This includes studying market reports, trade articles, investor presentations, company websites, Eurostat logistics datasets, and industry publications to assess the size, segmentation, and key dynamics of the market.

We evaluate company-level data such as revenue, warehouse capacity, freight volumes, and service diversification using public disclosures, press releases, and media coverage. The objective is to establish a foundational understanding of the industry landscape, key operational indicators, regulatory environment, and emerging trends in Romania.

Step 3: Primary Research

A series of structured interviews are conducted with senior executives (CEOs, supply chain heads, logistics managers) and operational stakeholders from key logistics companies, warehouse operators, 3PL users (e-commerce, FMCG, pharma), and industry experts across Romania.

These discussions serve to validate market assumptions, gather granular insights on warehousing practices, freight pricing models, technology adoption, and supply-demand shifts. A bottom-up approach is used to estimate freight volumes, warehouse throughput, and regional share, which is then extrapolated to the national market level.

As part of our triangulation strategy, we also conduct mystery shopping (disguised interviews) with selected 3PL and warehousing service providers to verify operational claims and pricing benchmarks. This helps us validate insights from primary sources against what is observed in practice.

Step 4: Sanity Check

- A combination of top-down and bottom-up modeling is employed to validate market size estimates and cross-check segment-level assumptions. Sensitivity testing is done on key variables such as GDP, e-commerce penetration, warehouse absorption rate, and international trade volumes to assess model robustness. Final outputs are validated against known financial benchmarks and shipment statistics.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Romania logistics and warehousing market is poised for steady expansion, reaching an estimated value of RON 38 billion in 2023. With Romania’s strategic geographic position at the crossroads of Europe, a growing industrial and e-commerce base, and continuous investments in infrastructure and automation, the market is expected to grow significantly through 2029. Additionally, EU-backed transport modernization and rising nearshoring trends are set to enhance Romania’s role as a regional logistics hub.

Key players in the Romania logistics and warehousing space include DHL Romania, DB Schenker, FAN Courier, KLG Europe, and FM Logistic. These companies lead the market due to their integrated service offerings, expansive warehouse networks, adoption technology, and ability to cater to both domestic and international clients. Other notable contributors include CTP Romania and WDP, who are actively developing modern industrial and logistics parks across the country.

The market is being driven by several factors: the rapid rise of e-commerce, government-backed infrastructure upgrades, increasing demand for cold chain and pharma logistics, and the integration of automation in warehousing operations. Romania’s strategic location, access to Black Sea ports, and strong cross-border trade with both EU and non-EU countries further position it for long-term growth.

Despite its growth potential, the market faces several hurdles including infrastructure gaps in rural regions, a shortage of skilled logistics labor, and rising operational costs, especially for energy-intensive warehousing. Additionally, regulatory complexities related to EU customs, emissions standards, and cross-border logistics can increase compliance costs and operational complexity for small and medium providers.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500