Singapore Beauty & Personal Care Market Outlook to 2030

By Product Category, By Price Tier, By Distribution Channel, By Consumer Demographics, and By Product Claims/Attributes

Report Overview

Report Code

TDR0353

Coverage

Asia

Published

October 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Singapore Beauty & Personal Care Market Outlook to 2030 – By Product Category, By Price Tier, By Distribution Channel, By Consumer Demographics, and By Product Claims/Attributes” provides a comprehensive analysis of the beauty and personal care market in Singapore. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the beauty and personal care market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Singapore Beauty & Personal Care Market Outlook to 2030 – By Product Category, By Price Tier, By Distribution Channel, By Consumer Demographics, and By Product Claims/Attributes” provides a comprehensive analysis of the beauty and personal care market in Singapore. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the beauty and personal care market. The report concludes with future market projections based on product categories, price tiers, distribution channels, consumer groups, attributes, cause-and-effect relationships, and success case studies highlighting the major opportunities and cautions.

Singapore Beauty & Personal Care Market Overview and Size

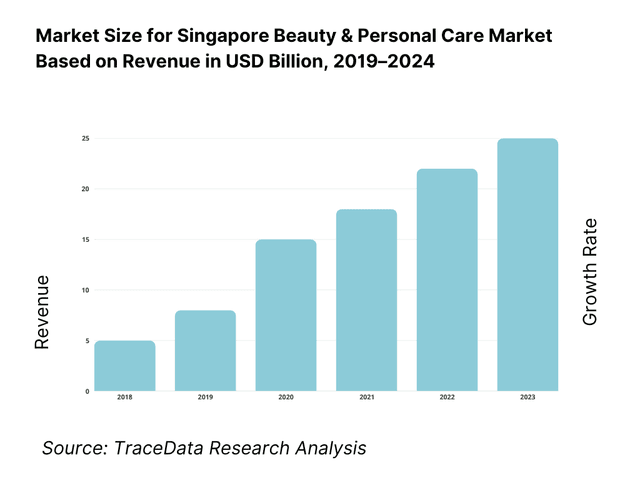

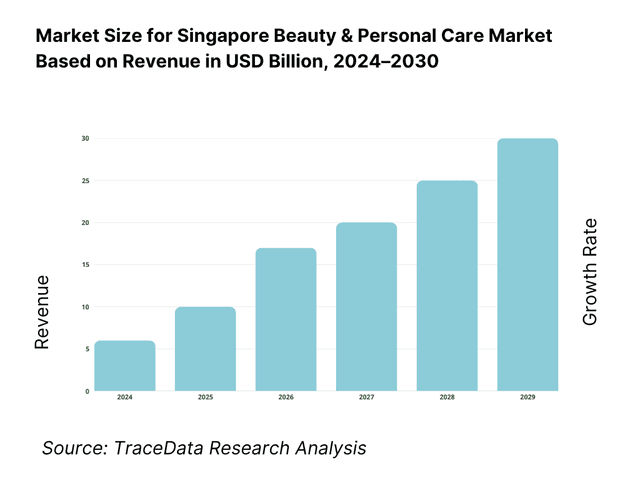

The Singapore Beauty & Personal Care market is valued at USD 1,245 million, based on a five-year historical analysis, and the latest official reference indicates USD 1,244 million for the most recent period. This scale is underpinned by high-spend consumers, dense retail (Watsons, Guardian, Sephora) and resilient online demand, while tourism-linked travel retail and cross-border e-commerce add incremental receipts. The 1.24–1.25 billion band is corroborated by a U.S. International Trade Administration brief (citing Statista) and a market sizing report focused on Singapore.

Within the city-state, Orchard Road/CBD–Marina Bay luxury corridors and Changi Airport travel-retail are dominant due to premium footfall, tourist conversion and mono-brand flagships, while digital sales concentrate on Shopee, Lazada, Qoo10, Amazon and TikTok Shop. On the supply side, country-of-origin influence is led by France (fragrance, prestige), Japan/Korea (derma, K-/J-beauty), and the United States (mass/premium portfolios), reflecting brand depth, marketing firepower and distribution partnerships in Singapore.

What Factors are Leading to the Growth of the Singapore Beauty & Personal Care Market:

Tourism and airport throughput translate directly into premium beauty sell–through: Singapore’s visitor pipeline and airport capacity materially lift beauty retail and gifting. International Visitor Arrivals reached 16,500,000, while tourism receipts totaled S$29,800,000,000—a record tied to strong spending in retail-linked categories. Aviation supply-side capacity has normalised, with >41,000,000 seats at Changi reported alongside the visitor rebound, sustaining traffic for travel-retail counters and mono-brand boutiques. The combined scale of 16.5 million inbound travellers and S$29.8 billion in receipts underpins high-velocity launches and replenishment in terminals and downtown flagships, reinforcing Singapore’s role as a regional showcase for prestige skincare, fragrance and derma lines.

High-income, compact consumer base with deep consumption outlays: Beauty trading-up is supported by macro spending power and dense urban demand. The World Bank reports GDP per capita of US$90,674.10 for Singapore, with population at approximately 6,000,000, creating a concentrated pool of premium shoppers reachable through a short store network and same-day logistics. Household spending depth is visible in national accounts: Household Final Consumption Expenditure of US$172,365,448,241 provides the absolute base from which beauty baskets draw, particularly in skincare and fragrance. This combination of US$90,674.10 income per person, ~6.077 million residents and US$172,365,448,241 of household outlays sustains premiumization and frequent replenishment.

Digital commerce rails and live-commerce funnels accelerate discovery and replenishment: Online infrastructure and platform scale convert beauty demand into transactions. A U.S. government country guide records 3,510,000 e-commerce users in Singapore, a meaningful base for beauty marketplaces and brand.com. At the retail ledger level, SingStat shows S$1,000,000,000 of online retail sales value in December, underscoring the absolute volumes digital channels process in peak months (promotions, gifting). These hard numbers—3,510,000 digital shoppers and S$1,000,000,000 online turnover in a single month—explain why Sephora, Watsons and prestige brands stage digital-first drops, sampling and creator-led live streams that lift serums, sunscreens and fragrance coffrets.

Which Industry Challenges Have Impacted the Growth of the Singapore Beauty & Personal Care Market:

Stringent enforcement against illegal or non-compliant products raises operational risk: HSA’s enforcement footprint is sizeable: its annual summary reported 1,120,000 illegal health-product units seized and 55 prosecutions over 2021–2023, demonstrating active action across online and physical channels. Penalty ceilings are high; the Ministry of Health states fines of up to S$100,000 and/or 3 years’ imprisonment under the Health Products Act for illegal products. For cosmetics specifically, supplying a product without prior notification is an offence carrying up to S$20,000 fine and/or 12 months’ imprisonment under the Cosmetic Products—ACD Regulations. These figures compel robust compliance systems, ingredient screening and recall readiness.

Channel shifts intensify competition for shelf space and promo budgets: Digital consolidation absorbs large absolute spend, tightening offline sell-through for slower categories. Statistics Singapore recorded S$1,000,000,000 in online retail sales in December, a cash-value reminder of the promotional gravity of digital months. At the same time, beauty’s physical network must serve a compact domestic base of about 6,077,000 residents, constraining store-led volume outside tourism and commuter flows. Brands must budget for concurrent presence across marketplaces, pharmacies and specialty beauty, managing duplication and returns while protecting price ladders when S$1.0 billion monthly online volume concentrates price discovery and discounting.

Rising compliance costs tied to notification fees and quality systems: Regulatory fees are explicit cash items in a beauty P&L. HSA lists cosmetic notification fees of S$28 for around-eyes/lips, oral/dental and specific hair dyes (first 3 variants), S$8 for each subsequent variant in that class, and S$13 for other cosmetic products (first 3 variants). Quality recognition also carries cost: a local cosmetic GMP certificate application is S$4,440, with S$220 per additional certificate without further assessment. When multiplied across multi-SKU catalogues (shades/variants), these S$28 / S$13 / S$8 notifications and S$4,440 quality certifications become material operating line items for Singapore portfolios.

What are the Regulations and Initiatives which have Governed the Market:

Health Products (Cosmetic Products—ASEAN Cosmetic Directive) Regulations: pre-market notification & offences: Before supply, a cosmetic must be notified; failure is an offence liable to S$20,000 fine and/or 12 months’ imprisonment. Dealers must maintain a Product Information File and ensure ingredient, claims and labelling compliance. HSA sets specific fees: S$28 for higher-risk classes (eyes/lips, certain dyes, oral/dental; first 3 variants), S$8 for each further variant, and S$13 for other cosmetics (first 3 variants). These numeric obligations (fines and fee schedule) drive structured go-live plans, variant rationalisation and budgeting for annual re-notifications.

Health Products Act: penalties for illegal health products & evidence of enforcement: The Ministry of Health states penalties of up to S$100,000 and/or 3 years’ imprisonment for the sale of illegal health products under the Health Products Act. HSA’s enforcement data logs 1,120,000 seized units and 55 prosecutions over 2021–2023, confirming active monitoring of online channels where cosmetics circulate alongside other health products. These numerical thresholds and outcomes necessitate robust supplier due diligence, vigilant marketplace policing and clear adverse-event reporting SOPs within Singapore entities and regional distributors.

ASEAN Cosmetic Directive ingredient annexes & quality recognition costs: Singapore implements the ACD ingredient annexes (prohibited, restricted and permitted lists) and updates them via HSA. Operationally, compliance includes tracking annex revisions published by HSA and retaining a PIF for audits, while quality credentials strengthen tenders and retailer onboarding. For manufacturers seeking formal recognition, HSA lists a GMP certificate application fee of S$4,440 and S$220 for each additional certificate without further assessment—numbers that directly inform budgeting for audits and certifications tied to Singapore operations.

Singapore Beauty & Personal Care Market Segmentation

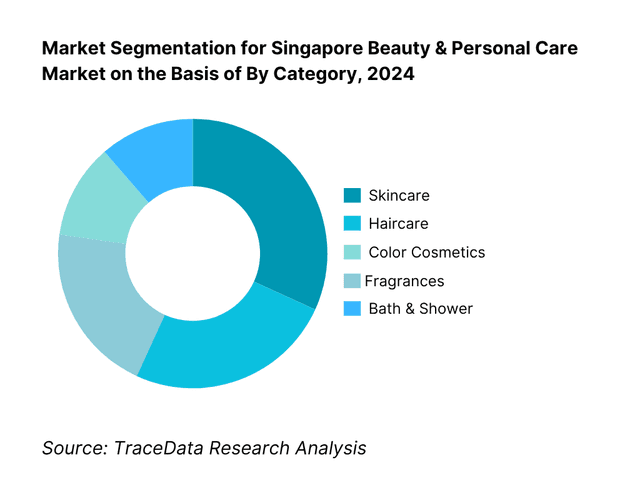

By Category: Singapore Beauty & Personal Care market is segmented by product category into skincare, haircare, color cosmetics, fragrances, bath & shower, men’s grooming and oral care. Recently, skincare has a dominant market share in Singapore under the segmentation by product category; it is driven by hot-humid climate needs (sun protection, oil control, sensitive-skin routines), high acceptance of derma-cosmetics and device-linked “skintellect” regimens, and the strength of K-/J-beauty plus French derm brands across Sephora/Watsons/Guardian and marketplaces.

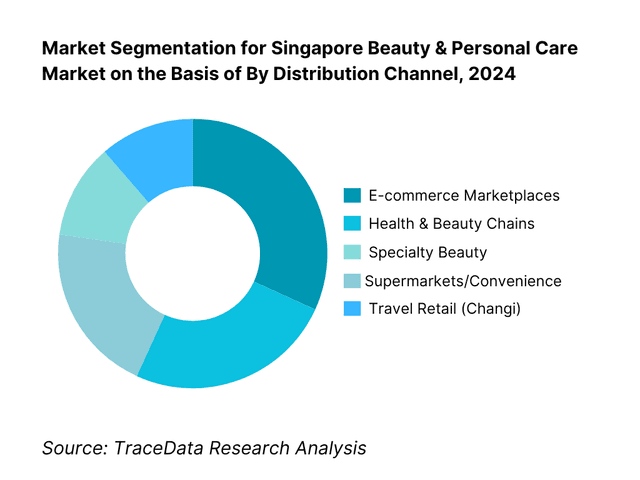

By Distribution Channel: Singapore Beauty & Personal Care market is segmented by distribution into health & beauty chains, specialty beauty, e-commerce marketplaces, supermarkets/convenience, travel retail and clinics/med-spas. Recently, e-commerce marketplaces hold a dominant market share in Singapore under the distribution segmentation; this stems from high digital penetration, aggressive promotions, same-day/next-day logistics, and cross-border assortment breadth (especially Korean, Japanese and niche brands) that exceed offline shelf space.

Competitive Landscape in Singapore Beauty & Personal Care Market

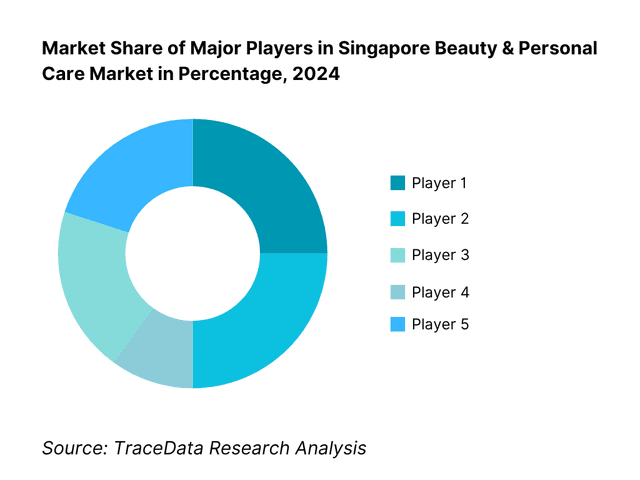

The Singapore Beauty & Personal Care market is anchored by multinational portfolios and a handful of strong local innovators, led by L’Oréal, Estée Lauder, Shiseido, Unilever/P&G-linked brands and Coty, alongside Amorepacific, Kao, Beiersdorf and Kenvue in mass/derma. Distribution power sits with Watsons, Guardian and Sephora, while online discovery and conversion increasingly concentrate on Shopee, Lazada and TikTok Shop. This consolidation underscores the influence of global R&D pipelines and marketing scale, while local brands (e.g., Allies of Skin, Skin Inc) carve out premium derm niches via clinic partnerships and D2C.

Name | Founding Year | Original Headquarters |

L’Oréal | 1909 | Clichy, France |

Estée Lauder | 1946 | New York, USA |

Shiseido | 1872 | Tokyo, Japan |

Procter & Gamble (P&G) | 1837 | Cincinnati, USA |

Unilever | 1929 | London, UK |

Beiersdorf | 1882 | Hamburg, Germany |

Kenvue (ex-J&J Consumer Health) | 2023 | New Jersey, USA |

Coty | 1904 | Paris, France |

Amorepacific | 1945 | Seoul, South Korea |

Kao Corporation | 1887 | Tokyo, Japan |

LG Household & Health Care | 1947 | Seoul, South Korea |

Clarins | 1954 | Paris, France |

Chanel (Fragrance & Beauty) | 1910 | Paris, France |

Allies of Skin | 2016 | Singapore |

Skin Inc | 2008 | Singapore |

Some of the Recent Competitor Trends and Key Information About Competitors Include:

L’Oréal: As one of the largest players in Singapore’s beauty market, L’Oréal has strengthened its derma-cosmetics portfolio through Vichy and La Roche-Posay in pharmacies, while also expanding refillable packaging pilots across premium lines such as Lancôme and Kiehl’s. Travel-retail activations at Changi Airport remain a key revenue driver.

Estée Lauder: With a strong prestige positioning, Estée Lauder has introduced advanced serums under Estée Lauder and Clinique brands in Singapore, supported by digital-first launches on Sephora and Lazada. The group has also increased its reliance on DFS/Changi travel-retail to capture tourist flows.

Shiseido: The Japanese major has expanded its Anessa sunscreen and Elixir derma lines in Singapore, aligning with climate-specific skincare needs. Shiseido has also integrated eco-packaging across multiple SKUs and leveraged Sephora tie-ups for J-beauty category growth.

Unilever/Kenvue: Mass and masstige portfolios like Dove, Lux, Aveeno and Neutrogena have deepened their presence in Watsons and Guardian, with Kenvue boosting Aveeno’s sensitive-skin lines. Sustainability moves such as PCR plastics have been rolled out to enhance consumer loyalty.

Amorepacific: Laneige and Sulwhasoo have continued strong Sephora traction, with Water Bank moisturizers and anti-ageing serums leading sales. Innisfree has piloted refill stations in Singapore, showcasing sustainability leadership within K-beauty.

What Lies Ahead for Singapore Beauty & Personal Care Market?

The Singapore Beauty & Personal Care market is projected to expand steadily by 2030, supported by strong tourism receipts, sustained consumer affluence, and continued digital adoption across retail channels. Growth will be fueled by the rebound of travel-retail at Changi Airport, rising derma-cosmetic adoption, and government-backed policies encouraging sustainability and product safety through regulatory frameworks.

Premiumization & Derma Expansion: The future of Singapore’s beauty market will be shaped by consumers trading up to derma-focused skincare and premium fragrances, with rising demand for functional claims like anti-ageing, brightening, and sensitive-skin solutions. Pharmacies, clinics, and med-spas will become important distribution nodes.

Sustainable & Refillable Formats: As consumers become environmentally conscious, refillable packaging, PCR plastics, and recycling schemes will gain traction. Brands investing in eco-driven innovation will benefit from stronger loyalty and retailer preference, especially in Sephora and Watsons.

Rise of Digital-First & Live Commerce: Digital-first launches and live-commerce campaigns via Shopee, Lazada, and TikTok Shop will increasingly dominate discovery and replenishment, allowing brands to reach the city-state’s 3.5 million e-commerce users with interactive formats and influencer engagement.

Travel Retail Rebound & Gifting: Changi Airport will remain a global showcase for prestige brands, with premium gift sets and miniatures in demand from international travellers. This channel will play a critical role in sustaining fragrance and luxury skincare volumes.

Personalization through AI & Beauty Tech: The use of AI-driven diagnostics, AR try-ons, and personalized skincare routines will continue to expand, helping brands deliver more tailored consumer experiences, boost engagement, and enhance conversion both online and offline.

Singapore Beauty & Personal Care Market Segmentation

By Product Category (In Value %)

Skincare

Haircare

Color Cosmetics

Fragrances

Bath & Shower

Men’s Grooming

Oral Care

Baby & Mother Care

By Price Tier (In Value %)

Mass

Masstige

Premium

Luxury

Derma/Clinic Grade

By Distribution Channel (In Value %)

Health & Beauty Chains (Watsons, Guardian)

Specialty Beauty (Sephora, Mono-brand Boutiques)

E-commerce Marketplaces (Shopee, Lazada, Qoo10, Amazon, TikTok Shop)

Supermarkets & Convenience Stores

Travel Retail (Changi Airport & downtown duty-free)

Clinics & Med-Spas

By Consumer Demographics (In Value %)

Gen Z

Working Professionals

Families

Seniors

Expatriates

By Product Claims / Attributes (In Value %)

Halal-certified

Clean / “Free-from”

Dermatologist-tested / Sensitive Skin

Vegan / Cruelty-free

Sun Protection (SPF)

Whitening / Brightening

Anti-ageing / Firming

Players Mentioned in the Report:

L’Oréal (Singapore) Pte Ltd

Estée Lauder Cosmetics (Singapore) Pte Ltd

Shiseido (Singapore) Co. Pte Ltd

Procter & Gamble (Singapore) Pte Ltd

Unilever Asia Pte Ltd

Beiersdorf Singapore Pte Ltd

Kenvue (Singapore) Pte Ltd

Coty Asia Pte Ltd

Amorepacific Singapore Pte Ltd

Kao Singapore Pte Ltd

LG Household & Health Care (Singapore)

Clarins Pte Ltd

Chanel (Singapore) Pte Ltd — Fragrance & Beauty

Allies of Skin Pte Ltd

Skin Inc Global Pte Ltd

Key Target Audience

Brand owners & regional general managers (MNC and regional portfolios)

Retail chains (Watsons, Guardian, Sephora; supermarkets/convenience)

E-commerce marketplaces (Shopee, Lazada, Qoo10, Amazon, TikTok Shop)

Clinics, dermatology groups & med-spas (treatment-linked retail)

Packaging & sustainability partners (refill/PCR ecosystem)

Investments and venture capitalist firms (beauty tech/indie brand growth)

Government & regulatory bodies (Health Sciences Authority (HSA); Enterprise Singapore; Changi Airport Group for travel-retail facilitation)

Logistics & cold-chain/temperature-controlled distributors

Time Period:

Historical Period: 2019-2024

Base Year: 2025

Forecast Period: 2025-2030

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Delivery Model Analysis-Offline Retail, E-Commerce, Travel Retail, Clinics/Med-Spas [Margins, Consumer Preference, Strengths & Weaknesses]

4.2. Revenue Streams for Singapore Beauty & Personal Care Market [Retail Sales, Cross-Border E-Commerce, Subscription Boxes, Professional Treatments, Licensing]

4.3. Business Model Canvas for Singapore Beauty & Personal Care Market [Mass, Premium, Luxury, Clinic-Grade]

5.1. Freelance Makeup Artists / Beauty Professionals vs Full-Time Salon & Clinic Staff

5.2. Investment Models in Singapore Beauty & Personal Care Market [Flagship Stores, Pop-Ups, Digital-First D2C]

5.3. Comparative Analysis of Sales Funnel-Retail Chains vs E-Commerce Platforms vs Clinics

5.4. Beauty & Personal Care Budget Allocation by Household Income Segment

8.1. Revenues (In USD Bn, Historic Analysis)

9.1. By Market Structure (Mass, Masstige, Premium, Luxury, Derma), Current Analysis

9.2. By Product Category (Skincare, Haircare, Color Cosmetics, Fragrances, Bath & Shower, Men’s Grooming, Oral Care, Baby & Mother Care)

9.3. By Consumer Demographic (Gen Z, Professionals, Families, Seniors, Expatriates)

9.4. By Company Size (MNCs, Regional Players, SMEs, Indie Labels)

9.5. By Mode of Purchase (Offline Retail, Online Marketplaces, Live-Commerce, Direct-to-Consumer)

9.6. By Customized vs Standardized Programs (Personalized vs Mass-Market Products)

9.7. By Region (Central, East, West, North, South Singapore)

10.1. Consumer Client Landscape & Cohort Analysis

10.2. Beauty & Personal Care Needs & Purchase Decision-Making Process

10.3. Product Effectiveness & ROI (Repurchase Intent, Loyalty Metrics)

10.4. Gap Analysis Framework

11.1. Trends & Developments for Singapore Beauty & Personal Care Market [K-/J-/C-Beauty, Clean Labels, Refillables, Hybrid Makeup-Skincare, Scalp Care]

11.2. Growth Drivers for Singapore Beauty & Personal Care Market [Affluent Urban Base, Tourism & Travel Retail, Humidity/Climate Needs, Cross-Border E-Commerce, Social Commerce Influence]

11.3. SWOT Analysis for Singapore Beauty & Personal Care Market

11.4. Issues & Challenges for Singapore Beauty & Personal Care Market [High Regulatory Scrutiny, Counterfeits, Shelf-Space Competition, Brand Saturation]

11.5. Government Regulations for Singapore Beauty & Personal Care Market [Health Products Act, ACD Alignment, Safety Standards, Labelling Rules]

12.1. Market Size & Future Potential for Online Beauty & Personal Care Industry in Singapore

12.2. Business Models & Revenue Streams [Subscription, D2C, Cross-Border]

12.3. Delivery Models & Product Range Offered

15.1. Market Share of Key Players (By Revenues / Category Contribution)

15.2. Benchmark of Key Competitors-Variables: Company Overview, USP, Business Strategies, Business Model, No. of SKUs, Revenues, Pricing, Technology Used, Best-Selling Products, Strategic Tie-Ups, Marketing Strategy, Recent Developments

15.3. Operating Model Analysis Framework

15.4. Gartner Magic Quadrant

15.5. Bowman’s Strategic Clock for Competitive Advantage

16.1. Revenues (Projections, In USD Bn)

17.1. By Market Structure (Mass, Masstige, Premium, Luxury, Derma)

17.2. By Product Category (Skincare, Haircare, Color Cosmetics, Fragrances, Men’s Grooming, Oral Care, Bath & Shower, Baby Care)

17.3. By Consumer Demographic (Gen Z, Families, Professionals, Seniors, Expatriates)

17.4. By Company Size (MNCs, Regional, SMEs, Indie Labels)

17.5. By Mode of Purchase (Offline, Online, Live-Commerce, D2C)

17.6. By Customized vs Standardized Programs (Personalized vs Mass-Market)

17.7. By Region (Central, East, West, North, South Singapore)

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

We begin by mapping the ecosystem of the Singapore Beauty & Personal Care Market, identifying all demand-side and supply-side entities. On the supply side, this includes multinational brand owners, local indie labels, distributors, health & beauty chains, specialty beauty retailers, e-commerce platforms, and clinics/med-spas. On the demand side, it covers consumer cohorts such as Gen Z, working professionals, families, seniors, and expatriates. Based on this mapping, we shortlist 5–6 leading beauty companies active in Singapore by evaluating their financial disclosures, category breadth, retail penetration, and client/consumer base. Sourcing is performed through industry articles, company filings, regulator notices, and proprietary databases, ensuring comprehensive desk research inputs.

Step 2: Desk Research

An exhaustive desk research process is conducted by referencing diverse secondary and proprietary databases. This involves gathering insights on category revenues, distribution splits, product introductions, pricing ladders, and e-commerce performance. We supplement this with detailed examinations of company-level data—press releases, annual reports, financial statements, sustainability reports, and retailer listings—to build a foundational understanding of both the market and its participants. The desk research also explores Singapore-specific factors such as regulatory compliance under HSA/ASEAN Cosmetic Directive, travel-retail throughput at Changi Airport, and online retail values reported by SingStat. Together, these sources create a robust baseline for category and channel dynamics.

Step 3: Primary Research

To validate hypotheses and refine desk findings, we conduct in-depth interviews with brand managers, retailers, distributors, and clinic operators within the Singapore Beauty & Personal Care Market. These discussions serve to confirm statistical estimates, enrich qualitative insights, and extract operational and financial details. A bottom-up approach is applied to estimate brand contributions by category and channel, which are then aggregated to the overall market structure. As part of our strategy, we occasionally conduct disguised interviews under the guise of potential clients, allowing us to validate operational claims such as SKU counts, distribution contracts, and promotional strategies. These interactions provide deeper visibility into revenue streams, pricing, marketing cadences, and value-chain processes.

Step 4: Sanity Check

Finally, a top-down and bottom-up triangulation is undertaken to ensure alignment between macro-level indicators (household consumption expenditure, retail sales values, tourism receipts) and micro-level company/channel performance. This involves market size modeling exercises that reconcile regulatory disclosures, retailer sell-out data, and e-commerce sales reports with primary research estimates. The result is a sanity-checked market view that balances official macroeconomic statistics with company-level operating realities, ensuring accuracy and reliability in our final outputs for the Singapore Beauty & Personal Care Market.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Singapore Beauty & Personal Care Market is poised for sustained expansion, valued at USD 1,245 million in 2023. This potential is anchored by strong consumer spending power, with GDP per capita at USD 90,674.10, and significant inbound tourism receipts of S$29.8 billion. The combination of affluent residents, dense urban retail infrastructure, and robust e-commerce rails creates fertile ground for growth. Furthermore, the city’s status as a regional beauty hub attracts multinational brands and innovation launches, reinforcing long-term opportunity.

The Singapore Beauty & Personal Care Market features several key players, including L’Oréal, Estée Lauder, Shiseido, Procter & Gamble, and Unilever, which dominate with their extensive portfolios and global marketing power. Other notable players such as Beiersdorf, Coty, Kenvue, Amorepacific, and Kao have entrenched presence in skincare, fragrance, and haircare segments. Local innovators like Allies of Skin and Skin Inc also hold relevance in the premium derma and personalized skincare space, adding diversity and innovation to the market landscape.

Key growth drivers include tourism and travel-retail flows, as Singapore welcomed 16.5 million international visitors in the latest cycle, sustaining high fragrance and luxury skincare turnover. The city’s affluent consumer base, with household final consumption expenditure of US$172,365,448,24, enables premiumization and frequent replenishment of beauty baskets. Digital infrastructure also acts as a major catalyst, with 3.51 million e-commerce users and S$1.0 billion in online retail sales in December alone, ensuring beauty products gain scale through online campaigns, live-commerce, and cross-border shopping.

Challenges include stringent regulation, as failure to notify a cosmetic before supply can attract fines up to S$20,000 and/or 12 months’ imprisonment. Market saturation in a compact consumer base of ~6.077 million people also heightens competitive intensity, forcing brands to differentiate through innovation and loyalty programs. Additionally, operational costs rise with compliance fees—cosmetic notification costs range from S$8 to S$28 per variant, and GMP certification costs S$4,440, creating financial barriers for SMEs and indie brands seeking scale.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0