South Korea Car Rental and Leasing Market Outlook to 2030

South Korea Car Rental & Leasing Market, South Korea Car Rental & Leasing Industry

Report Overview

Report Code

TDR0356

Coverage

Asia

Published

October 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “South Korea Car Rental & Leasing Market Outlook to 2030 – By Service Type, By Vehicle Class, By Powertrain, By Booking Channel, By End-User, and By Region” provides a comprehensive analysis of the rental and leasing industry in South Korea. The report covers an overview and genesis of the industry, overall market size in terms of revenue, detailed market segmentation; trends and developments, regulatory and licensing landscape, customer-level profiling, key issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the South Korea car rental & leasing...

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “South Korea Car Rental & Leasing Market Outlook to 2030 – By Service Type, By Vehicle Class, By Powertrain, By Booking Channel, By End-User, and By Region” provides a comprehensive analysis of the rental and leasing industry in South Korea. The report covers an overview and genesis of the industry, overall market size in terms of revenue, detailed market segmentation; trends and developments, regulatory and licensing landscape, customer-level profiling, key issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the South Korea car rental & leasing market. The report concludes with future market projections based on fleet volumes, service types, powertrain adoption, regions, cause-and-effect relationships, and success case studies highlighting the major opportunities and cautions.

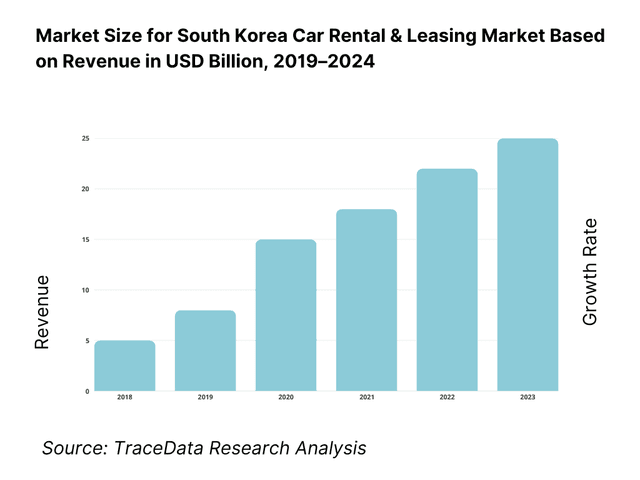

South Korea Car Rental & Leasing Market Overview and Size

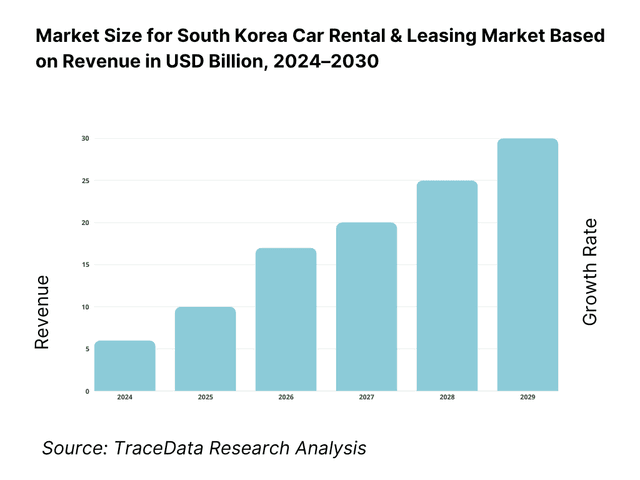

The South Korea car rental market is valued at USD 1,594.1 million (i.e. ~USD 1.59 billion). This reflects the scale of short-term rental services (daily/weekly) and support functions (airport, urban pick-ups). The rental side is bolstered by growth in tourism receipts (inbound travelers) and domestic mobility demand, while leasing (especially long-term and corporate leases) is driven by corporates’ shift to as-a-service models and OEM captive finance arrangements.

Seoul, Busan, and Jeju dominate the South Korea rental & leasing market. Seoul is the business, financial and tourism hub—with the densest demand from both corporate and inbound travelers. Busan acts as a key port and convention city, driving rental usage in the southern region. Jeju, being a major leisure island destination with few public transport alternatives, sees disproportionately high rental demand year-round. The OEM captive finance operations (e.g. Hyundai/Kia) are also headquartered in and around Seoul, further concentrating leasing activity.

What Factors are Leading to the Growth of the South Korea Car Rental & Leasing Market:

Travel demand recovery & air connectivity intensify short-duration rental needs (airport & city stations).: International gate flows are back at scale, supplying steady renter throughput to airport stations and downtown locations. Incheon International Airport handled 70,651,000 passengers in the latest full year, restoring heavy long-haul and regional connectivity that feeds business trips and weekend leisure drives. In parallel, foreign tourist arrivals reached 16,369,629, reflecting a broad-based rebound in inbound demand that supports on-airport counters, chauffeur rentals and self-drive on Jeju/Busan corridors. The size and composition of these flows—multi-city itineraries and tightly scheduled corporate travel—translate into high vehicle turns, strong utilization, and rising attachment of add-ons such as insurance upgrades, GPS, and toll tags.

Large vehicle stock and dense urban mobility patterns sustain replacement, pooling, and corporate leasing cycles.: South Korea operates a registered road fleet of about 26.3 million vehicles, serving a national population of 51,751,065, which underpins continuous renewal of corporate fleets and opportunities for operating leases, subscription plans and medium-term rentals. Within Seoul’s multi-modal core, Line 2 alone carried 1,964,128 passengers per day, exceeding the combined daily ridership of other metropolitan systems nationwide. This density boosts demand for “first/last-mile” rentals, weekend escapes and intercity trips where car access complements transit. Fleet owners capitalize by rotating high-mileage units into rental channels and structuring leases that optimize utilization between corporate workdays and leisure peaks.

Electrification push and charging build-out open premium rental & green corporate-lease lanes.: Policy momentum is visible in budgets and hardware: the government set KRW 618.7 billion for EV charging facilities, up sharply from the prior year, while 305,309 public chargers supported 565,154 registered EVs at the last annual checkpoint. Coupled with safety enhancements and certification measures for batteries, this infrastructure enables rental/leasing firms to introduce electric-only classes, bundle workplace charging services, and sell “carbon-lite” TCO propositions to procurement teams. The result is a viable electrified segment with clear operational anchors—dense urban charging and growing intercity fast-charge corridors.

Which Industry Challenges Have Impacted the Growth of the South Korea Car Rental & Leasing Market:

Demographic headwinds reshape demand mix toward shorter contracts and off-peak utilization.: Korea’s population stood at 51,751,065, with rapid aging altering travel and commuting behavior in core cities. An expanding elderly cohort and rising shares of single-person elderly households can dampen multi-year corporate lease appetites while lifting ad-hoc rentals for medical, caregiving, and suburban errands. For fleet managers, aging translates into lower average annual mileage and more weekday daytime availability, pressuring yield unless pricing and product are adapted. Mobility packages for seniors, flexible insurance deductibles, and concierge pick-ups are increasingly needed to counteract these structural shifts.

Currency volatility raises imported-vehicle and financing exposure for lease portfolios.: Leasing residuals, parts costs and interest servicing are sensitive to foreign exchange volatility. The average KRW per US$ in 2024 was 1,363.4381, and the won touched 1,448.9 per US$ during a late-year trough, amplifying exposure for fleets heavy in imported models and dollar-linked components such as tires and electronics. Funding costs are also policy-driven, as the central bank’s base-rate path and communications keep capital-market spreads in flux. Rental and leasing operators hedge with staggered procurement and mixed-origin fleets, but volatility still impacts pricing cadence and residual-value setting.

Public-transport dominance compresses weekday self-drive demand in urban cores.: Seoul’s high-capacity rail network diverts daily trips from private car usage, concentrating car rental demand into weekends and airport traffic. Seoul Metro Line 2 carried 1,964,128 passengers per day, and combined secondary systems handled nearly 1.91 million daily passengers, indicating deep transit preference for commuting. For car rental and leasing, that means skewed utilization curves—peaks around holidays and late Fridays—requiring yield-management, one-way flexibility, and suburban station placement. Operators increasingly pivot toward B2B leasing outside core CBDs and short-haul leisure offerings aligned with rail nodes.

What are the Regulations and Initiatives which have Governed the Market:

Passenger Transport Service Act (platform & rental-with-driver boundaries).: The Passenger Transport Service Act (Act No. 19387) sets market boundaries between taxi services, platform intermediation, and rental-with-driver operations. Amendments introduced structured categories for app-based services and clarified limitations on chauffeured rentals, such as minimum-time and specific pickup rules that restrict “ride-hailing via rental vans.” For rental/leasing firms, compliance dictates how chauffeur options are marketed for tourist charters and airport transfers, and influences the placement of rental stations near airports and seaports to meet lawful pickup criteria.

Personal Information Protection Act (PIPA) – strict data handling for telematics & renter privacy.: Fleet telematics, dashcams, and app-based rentals fall under the Personal Information Protection Act, which imposes rigorous standards for collection, processing, and cross-border transfer of data. Enforcement has included financial sanctions above KRW 21 billion for unlawful collection and misuse of sensitive information. Rental and leasing providers must ensure explicit consent flows, minimize video/audio data capture in vehicles, and maintain robust compliance for connected-car analytics used in damage adjudication and usage-based billing.

Compulsory motor liability insurance – binding operating prerequisite & cost pass-through.: Operating rental vehicles and leasing fleets requires continuous insurance coverage under Korea’s mandatory automobile liability framework. Non-life insurance premium inflows totaled KRW 61.3 trillion in the first half of the latest year, underscoring both the market’s scale and the regulator’s close oversight. For rental and leasing operators, compliance translates into standardized insurance offerings at counters and in corporate contracts, such as CDW/LDW, enhanced liability, and uninsured-motorist coverage. These policies ensure fleet safety while passing costs into rental yields and leasing terms.

South Korea Car Rental & Leasing Market Segmentation

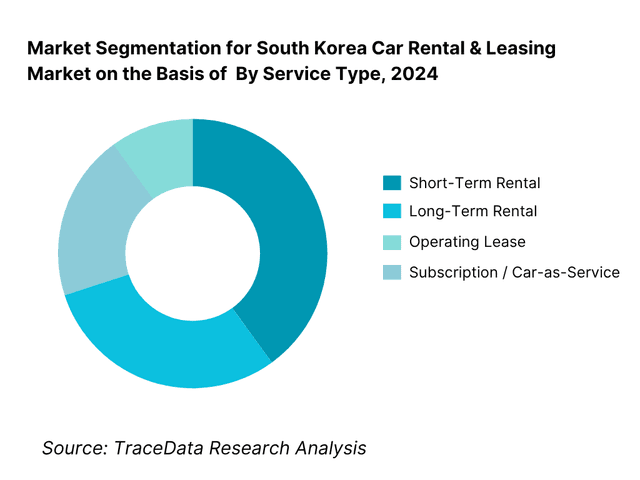

By Service Type: The short-term rental holds dominance. This is because daily/weekly rentals serve both tourists and domestic travelers who require flexible mobility without ownership commitment. The airport-based and app booking infrastructure is mature, and the frequency of turn-over of vehicles allows higher yield. Many users (foreign tourists, intra-city users) prefer short durations, driving volume. The fixed overhead of branches and fleet utilization benefits short-term volume. Meanwhile, leasing and subscription are growing but remain investment-heavy and slower to scale.

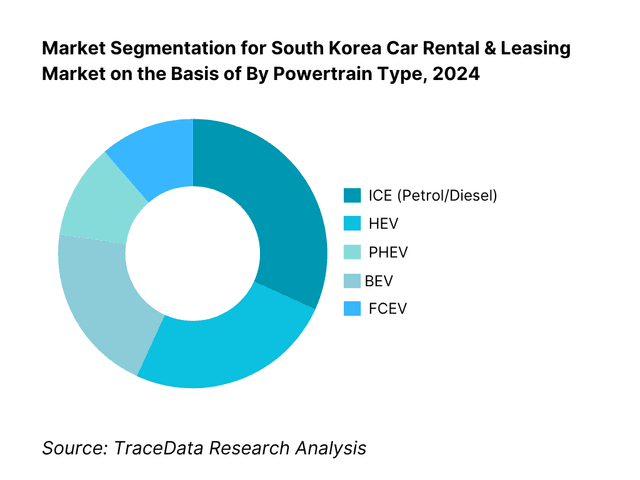

By Powertrain Type: The ICE (petrol/diesel) segment remains dominant because legacy fleet replacement cycles still favor internal combustion vehicles. The existing maintenance, fueling infrastructure, lower capex, and residual value certainty support ICE fleet prevalence. The transition to hybrid/BEV is underway, but battery leasing, charging infrastructure constraints, and residual risk slow mass adoption. BEV uptake is strongest in premium segments and in captives, but not yet large enough to overtake ICE in 2024.

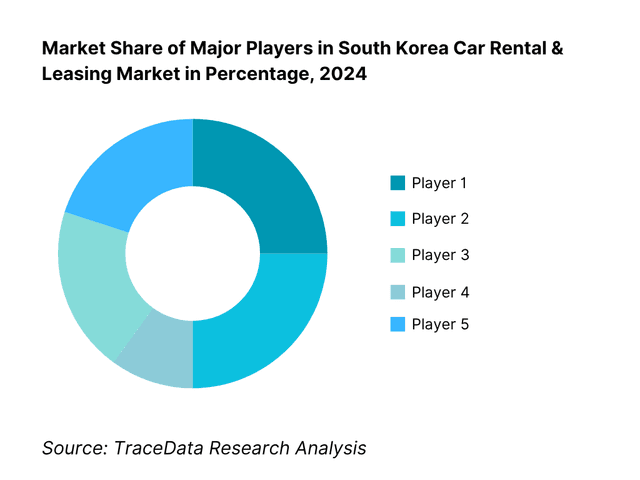

Competitive Landscape in South Korea Car Rental & Leasing Market

The South Korea rental & leasing market exhibits moderate concentration, led by a combination of national captives and independent operators. Key players leverage fleet scale, OEM partnerships, digital booking platforms, and airport counter networks.

Name | Founding Year | Original Headquarters |

LOTTE Rental (LOTTE Rent-a-Car) | 1989 | Seoul, South Korea |

SK Rent-a-Car (orig. AJ Rent-a-Car) | 1988 | Seoul, South Korea |

Hyundai Capital (Auto Lease) | 1993 | Seoul, South Korea |

KB Capital (Auto Lease) | 1990 | Seoul, South Korea |

Hana Capital (Auto Lease) | 2007 | Seoul, South Korea |

Shinhan Capital (Auto Lease) | 1991 | Seoul, South Korea |

NH NongHyup Capital (Auto Lease) | 2007 | Seoul, South Korea |

SOCAR (car-sharing/subscription) | 2011 | Seoul, South Korea |

GreenCar (car-sharing) | 2011 | Seoul, South Korea |

Avis Budget Group Korea | 1946 | Parsippany, New Jersey, USA |

Hertz Korea | 1918 | Estero, Florida, USA |

Sixt Rent a Car Korea | 1912 | Munich, Germany |

K Car (subscription) | 1997 | Seoul, South Korea |

AJ Networks / AJ Rent-a-Car | 2000 | Seoul, South Korea |

Jeju Rent-a-Car | 2004 | Jeju City, South Korea |

Some of the Recent Competitor Trends and Key Information About Competitors Include:

LOTTE Rental: As South Korea’s largest rental operator, LOTTE Rental expanded its electric vehicle fleet in 2024 by adding over 2,000 BEVs across Seoul and Jeju branches. The company has also launched digital enhancements to its mobile app, enabling contactless booking, AI-based fleet allocation, and real-time vehicle condition checks.

SK Rent-a-Car: nown for its strong airport presence, SK Rent-a-Car signed new partnerships in 2024 with major airlines to offer bundled car rental packages. It has also invested in expanding its premium vehicle segment, catering to rising demand from business travelers and inbound tourists in Seoul and Busan.

Hyundai Capital Auto Lease: Leveraging its OEM captive advantage, Hyundai Capital increased the penetration of long-term EV leases in 2024. It introduced bundled offerings that combine vehicle financing, battery leasing, and charging solutions, positioning itself as a leader in corporate green mobility.

SOCAR: As a pioneer in South Korea’s car-sharing and subscription space, SOCAR launched AI-driven dynamic pricing in 2024, adjusting rates based on demand fluctuations and vehicle availability. The platform also rolled out new ESG initiatives, including discounted rates for EV car-sharing in metropolitan hubs.

K Car: Focused on subscription and used-car leasing, K Car expanded its subscription user base by double digits in 2024. The company strengthened its digital ecosystem by integrating predictive analytics for vehicle demand forecasting and broadening partnerships with fintech players for flexible payment solutions.

What Lies Ahead for South Korea Car Rental & Leasing Market?

The South Korea Car Rental & Leasing Market is expected to expand steadily by 2030, supported by rising inbound tourism, corporate fleet outsourcing, and the government’s strong emphasis on green mobility adoption. Growth momentum is further enhanced by Seoul’s role as a global business hub, the heavy tourist influx into Jeju, and increasing corporate reliance on operating leases and subscription-based mobility. Supportive transport infrastructure, policy-driven EV incentives, and digital distribution channels are shaping the next phase of market evolution.

Rise of Hybrid Mobility Models: The future of South Korea’s rental and leasing market will likely see the expansion of hybrid mobility models, where short-term rentals, long-term leases, car-sharing, and subscription services converge. Customers increasingly value flexibility—switching between a daily rental, a monthly lease, or a car-share depending on travel purpose. Operators are blending these models to maximize fleet utilization while addressing both leisure tourists and corporate clients with variable mobility needs.

Focus on Sustainable & Green Fleet Leasing: As companies and government bodies in South Korea prioritize sustainability and carbon reduction, there will be a sharper focus on EV and hybrid leasing solutions. Operators are expanding their green fleets, backed by more than 305,000 public charging stations nationwide and financial incentives that encourage eco-friendly adoption. Corporate contracts increasingly demand EV-based fleets to align with ESG targets, making green leasing a central growth area in the years ahead.

Expansion of Sector-Specific Leasing Solutions: There is growing demand for sector-specific leasing programs in industries such as logistics, technology, and government institutions. Logistics companies are leveraging long-term leases for light commercial vehicles to optimize delivery networks, while corporates in IT and finance demand premium fleet solutions for employee mobility. Regional tourism hubs like Jeju are witnessing tailored rental products for inbound travelers, highlighting how sector- and region-specific mobility needs are reshaping fleet composition.

Leveraging AI, Telematics & Analytics: The adoption of AI and telematics-based analytics is expected to increase, enhancing fleet management and user experience. Operators are integrating predictive analytics to optimize pricing, route efficiency, and vehicle maintenance. For customers, personalized booking recommendations, app-based loyalty programs, and digital identity verification streamline the rental process. On the corporate side, analytics-driven reporting ensures better tracking of leasing ROI, residual values, and sustainability metrics—ultimately driving higher transparency and efficiency across the ecosystem.

South Korea Car Rental & Leasing Market Segmentation

By Service Type

Short-Term Rental (daily / weekly)

Long-Term Rental (multi-month)

Operating Lease

Finance Lease

Subscription / Car-as-a-Service

Chauffeur / Driver Services

By Vehicle Class

Mini / Compact Cars

Midsize Cars

Full-Size Cars

SUV / MPV

Premium / Luxury Cars

Light Commercial Vehicles (LCVs)

By Powertrain

ICE (Petrol)

ICE (Diesel)

Hybrid Electric Vehicles (HEV)

Plug-in Hybrid Electric Vehicles (PHEV)

Battery Electric Vehicles (BEV)

Fuel Cell Electric Vehicles (FCEV)

By Booking Channel

On-Airport Counters

City / Off-Airport Branches

Direct Online (Company App / Website)

OTA / Aggregators (e.g., global platforms)

Corporate Contracts

By End-User / Client Type

Corporate Clients (Large Enterprises)

SMEs (Small & Medium Enterprises)

Government / Public Institutions

Individual Domestic Travelers

Inbound Tourists

Players Mentioned in the Report:

LOTTE Rental

SK Rent-a-Car

Hyundai Capital Auto Lease

KB Capital Auto Lease

Hana Capital Auto Lease

Shinhan Capital Auto Lease

NH NongHyup Capital Auto Lease

SOCAR (subscription / sharing)

GreenCar (sharing)

Avis Budget Korea

Hertz Korea

Sixt Korea

K Car Subscription

AJ Networks / AJ Rent-a-Car

Jeju Rent-a-Car operators / regional aggregators

Key Target Audience

Entities that are likely buyers/users of this market report include:

Fleet investment funds / private equity & venture capital firms (mobility and automotive)

OEM captive finance divisions (Hyundai, Kia, BMW Korea)

Bank / auto finance arms evaluating leasing portfolios

Large corporate mobility & procurement divisions (Samsung, LG, SK, POSCO)

Airport authorities / airport concession planners

Tourism promotion agencies (Visit Korea, Korea Tourism Organization)

Charging infrastructure providers / EV infrastructure developers

Government & regulatory bodies

Time Period:

Historical Period: 2019-2024

Base Year: 2025

Forecast Period: 2025-2030

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Delivery Model Analysis for Car Rental & Leasing (Short-Term, Long-Term, Operating Lease, Subscription, Chauffeur)-Margins, Preference, Strength & Weakness

4.2. Revenue Streams for South Korea Car Rental & Leasing Market (Daily Rental Fees, Lease Payments, Add-Ons, Insurance Sales, Subscription Packages, Ancillary Services)

4.3. Business Model Canvas for South Korea Car Rental & Leasing Market

5.1. Independent Operators vs Captive/Finance-Backed Leasing Players

5.2. Investment Model in South Korea Car Rental & Leasing Market (Fleet Capex, Buyback Agreements, Charging Infra Investment, Airport Concessions)

5.3. Comparative Analysis of Funneling Process by Local vs International Operators (Airport/OTA vs Direct Corporate Contracts)

5.4. Corporate Rental/Leasing Budget Allocation by Company Size

8.1. Revenues (KRW Tn, USD Bn)

9.1. By Market Structure (Short-Term Rental, Long-Term Rental, Operating Lease, Subscription, Chauffeur)

9.2. By Vehicle Class (Mini/Compact, Midsize, SUV/MPV, Premium/Luxury, LCV)

9.3. By Industry Verticals (Corporate, Government, Retail, Tourism, Logistics/Delivery)

9.4. By Company Size (Large Corporates, SMEs, Public Sector, Individuals)

9.5. By Customer Type (Inbound Tourist, Domestic Leisure, Corporate Travelers, Replacement/Insurance Users)

9.6. By Mode of Booking (Direct App/Web, OTA/Aggregator, Corporate Contracts, Walk-in Branches)

9.7. By Powertrain (ICE Petrol/Diesel, HEV, PHEV, BEV, FCEV)

9.8. By Region (Seoul Capital Area, Busan-Ulsan-Gyeongnam, Daegu-Gyeongbuk, Daejeon-Chungcheong, Gwangju-Jeolla, Gangwon, Jeju)

10.1. Corporate Client Landscape and Cohort Analysis

10.2. Rental & Leasing Decision-Making Process (Pricing, Availability, Digital Channel Preference)

10.3. ROI Analysis for Leasing Contracts (Residual Value, Maintenance Cost Savings, Tax Benefits)

10.4. Gap Analysis Framework

11.1. Trends and Developments (Telematics, Contactless Pickup, Dynamic Yield Management, EV Fleet Penetration, Subscription Models)

11.2. Growth Drivers (Domestic Tourism, EV Subsidies, Airport Passenger Growth, Corporate Mobility)

11.3. SWOT Analysis

11.4. Issues and Challenges (Depreciation, Insurance Costs, Charging Infra Gaps, High Concession Fees)

11.5. Government Regulations (Motor Vehicle Management Act, PIPA, EV/FCEV Subsidy Rules, Insurance Mandates)

12.1. Market Size and Future Potential of Online/OTA Channels in South Korea

12.2. Business Models & Revenue Streams (Direct Apps, Aggregator Partnerships, Corporate Portals)

12.3. Digital Delivery Models and Customer UX (App Integration, Telematics, E-KYC, Loyalty Programs)

15.1. Market Share of Key Players (Fleet Size, Utilization %, Revenues, Lease O/S)

15.2. Benchmark of Key Competitors (Company Overview, USP, Business Model, Branch/Counter Count, Fleet Mix, EV Share, Pricing Basis, Technology Stack, Major Clients, Strategic Tie-Ups, Recent Developments)

15.3. Operating Model Analysis Framework

15.4. Gartner Magic Quadrant-Positioning of Rental & Leasing Players

15.5. Bowman’s Strategic Clock-Competitive Advantage Mapping

16.1. Revenues (KRW Tn, USD Bn)

17.1. By Market Structure (Short-Term, Long-Term, Operating Lease, Subscription, Chauffeur)

17.2. By Vehicle Class (Mini, Midsize, SUV/MPV, Luxury, LCV)

17.3. By Industry Verticals (Corporate, Government, Tourism, Retail, Logistics/Delivery)

17.4. By Company Size (Large Corporates, SMEs, Individuals)

17.5. By Customer Type (Tourist, Domestic, Corporate, Insurance Replacement)

17.6. By Mode of Booking (Direct, OTA, Aggregators, Contracts)

17.7. By Powertrain (ICE, HEV, PHEV, BEV, FCEV)

17.8. By Region (Seoul, Busan, Daegu, Daejeon, Gwangju, Gangwon, Jeju)

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

We begin by mapping the complete ecosystem of the South Korea Car Rental & Leasing Market. On the demand side, entities include domestic travelers, inbound tourists, corporate mobility accounts, SMEs leasing fleets, and government institutions procuring long-term leases. On the supply side, we include rental operators, leasing captives, OEM-backed finance arms, car-sharing platforms, OTA aggregators, insurers, and charging infrastructure providers. From this mapped ecosystem, we shortlist 5–6 leading operators (such as LOTTE Rental, SK Rent-a-Car, Hyundai Capital, SOCAR, K Car, and AJ Networks) based on available fleet data, financial disclosures, and client base strength. Sourcing for this step leverages industry articles, operator disclosures, and multiple secondary and proprietary databases to collate industry-level information.

Step 2: Desk Research

An exhaustive desk research process is undertaken using diverse secondary and proprietary databases to analyze the South Korea market. This involves reviewing industry-level metrics such as fleet sizes, utilization percentages, branch networks, and inbound tourism numbers. We also examine company-level disclosures, including press releases, financial statements, annual reports, and regulatory filings. This desk research aims to build a foundational understanding of revenue distribution across short-term rental, long-term leasing, subscription, and chauffeur services. OTA booking trends, average daily rental rates, and utilization data are integrated to identify structural patterns. The outcome of this stage is a comprehensive industry overview that details both market aggregates and granular company-level insights.

Step 3: Primary Research

We conduct structured in-depth interviews with C-level executives and operational managers from rental operators, leasing captives, airport concession managers, OTA platforms, and insurers active in the South Korea Car Rental & Leasing Market. The objectives are threefold: (a) validate market hypotheses, (b) authenticate statistical data collected in desk research, and (c) extract financial and operational insights around fleet procurement, utilization, residual values, insurance claims, and digital booking adoption. A bottom-to-top approach is applied to estimate revenue contributions from each player, which are then aggregated to the overall market. Disguised interviews are occasionally used, wherein our team engages as potential corporate clients to validate pricing structures, value-added services, and corporate contract terms. These interactions offer deeper understanding of operational processes, yield management strategies, and cost structures across the ecosystem.

Step 4: Sanity Check

The final stage integrates a bottom-to-top and top-to-bottom analysis to cross-validate market size and segmentation findings. Fleet-level utilization and average daily rate calculations are benchmarked against aggregated tourism flows, airport passenger data, and vehicle registration trends. Sensitivity testing is applied across multiple variables—fleet procurement costs, utilization ranges, and EV penetration—to ensure robustness. Market size modeling exercises are repeated iteratively until alignment is reached between operator-level financials and industry-wide metrics, thereby ensuring the accuracy and sanity of the final estimates.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The South Korea Car Rental & Leasing Market holds strong potential, anchored by robust domestic travel activity, a growing inbound tourism base, and expanding corporate mobility solutions. Incheon International Airport alone handled 70.6 million passengers in 2023, supporting heavy rental throughput at airport counters, while total registered vehicles in the country stood at 26.3 million, reflecting a deep pool for leasing and fleet services. With Seoul, Busan, and Jeju emerging as major demand hubs, the market is well positioned to grow further as electrification and subscription-based services gain traction.

The South Korea Car Rental & Leasing Market features leading operators such as LOTTE Rental, SK Rent-a-Car, Hyundai Capital Auto Lease, SOCAR, and K Car. These companies dominate due to their extensive branch networks, large vehicle fleets, and integration with digital booking channels. Other significant players include GreenCar, AJ Networks, Avis Budget Korea, Hertz Korea, and Sixt Korea, along with banking-backed finance arms like KB Capital, Hana Capital, Shinhan Capital, and NH NongHyup Capital. Collectively, these entities shape both the short-term rental and long-term leasing landscapes.

Key growth drivers include rising mobility demand linked to South Korea’s strong travel flows, with 16.3 million foreign visitors recorded in 2023, fueling rental demand in Jeju and major cities. Corporate leasing expansion is another driver, supported by an economy with a GDP of USD 1.67 trillion and high business density in Seoul, which encourages fleet leasing and long-term contracts. Government EV policies, backed by 305,309 public chargers and subsidies for battery-powered cars, also enhance opportunities for rental and leasing companies to diversify into eco-friendly fleets.

Challenges include demographic and structural headwinds, as South Korea’s population declined to 51.75 million in 2023 with rapid aging, reshaping demand patterns for rental and leasing products. High urban transit penetration, with Seoul Metro Line 2 alone carrying 1.96 million passengers daily, reduces weekday demand for rentals in core business districts. Additionally, financial risks linked to imported fleet procurement are magnified by currency volatility, with the won trading at an average of KRW 1,363 per USD, pressuring operators on depreciation and financing costs.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0