South Korea Logistics and Warehousing Market Outlook to 2029

By Type of Services (Freight Forwarding, Warehousing, Courier and Parcel, and Others), By Mode of Transport (Road, Rail, Air, and Sea), By End-User Industry, and By Region

Report Overview

Report Code

TDR0178

Coverage

Asia

Published

May 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “South Korea Logistics and Warehousing Market Outlook to 2029 –By Type of Services (Freight Forwarding, Warehousing, Courier and Parcel, and Others), By Mode of Transport (Road, Rail, Air, and Sea), By End-User Industry, and By Region” provides a comprehensive analysis of the logistics and warehousing market in South Korea. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in...

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “South Korea Logistics and Warehousing Market Outlook to 2029 –By Type of Services (Freight Forwarding, Warehousing, Courier and Parcel, and Others), By Mode of Transport (Road, Rail, Air, and Sea), By End-User Industry, and By Region” provides a comprehensive analysis of the logistics and warehousing market in South Korea. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the logistics and warehousing market. The report concludes with future market projections based on revenue, by service segment, transport type, region, and success case studies highlighting the major opportunities and challenges in the South Korean logistics space.

South Korea Logistics and Warehousing Market Overview and Size

The South Korea logistics and warehousing market was valued at KRW 48 trillion in 2023, driven by the country’s robust manufacturing base, increasing e-commerce penetration, and advancements in smart logistics infrastructure. The market is dominated by key players such as CJ Logistics, Hanjin Transportation, Lotte Global Logistics, Korea Post, and Pantos Logistics. These companies are known for their integrated logistics networks, strong warehousing capacity, and technology-enabled services.

In 2023, CJ Logistics expanded its smart logistics centers equipped with AI and robotics for automated sorting and inventory management, addressing rising demand from both domestic and cross-border e-commerce. Major logistics hubs such as Seoul-Incheon, Busan, and Daegu continue to serve as pivotal regions owing to their industrial density, port access, and infrastructural readiness.

Market Size for South Korea Logistics and Warehousing Industry on the Basis of Revenue in USD Billion, 2018-2024

What Factors are Leading to the Growth of South Korea Logistics and Warehousing Market:

E-Commerce Expansion: The rapid growth of e-commerce in South Korea has significantly boosted demand for last-mile delivery and warehousing solutions. In 2023, e-commerce accounted for over 30% of total retail sales, prompting logistics players to invest in fulfillment centers and smart warehousing infrastructure. This trend is expected to continue, driven by consumer expectations for same-day or next-day delivery.

Government Investment in Smart Logistics: The South Korean government has actively promoted smart logistics through infrastructure investments, subsidies for automation, and the development of smart logistics complexes. The “Smart Logistics Development Strategy,” initiated in 2021, aims to increase logistics productivity by 30% by 2030. This policy push is accelerating the adoption of AI, IoT, and robotics in the sector.

Export-Driven Manufacturing Sector: South Korea’s position as a global hub for electronics, automobiles, and machinery has led to consistent demand for large-scale freight forwarding and warehousing services. In 2023, exports accounted for approximately 40% of the country’s GDP, reinforcing the need for a robust and efficient logistics backbone that supports outbound cargo handling and international trade.

Which Industry Challenges Have Impacted the Growth for South Korea Logistics and Warehousing Market:

Urban Congestion and Delivery Constraints: High urban population density, particularly in Seoul and Incheon, has led to logistical challenges including delivery delays and increased last-mile costs. Approximately 25% of logistics costs are attributed to inefficiencies in urban delivery, limiting profitability and scalability for courier and parcel service providers.

Labor Shortage in Logistics Sector: South Korea is facing a shortage of skilled and semi-skilled labor in the logistics industry, especially in warehousing and truck driving. The logistics workforce declined by 6% between 2019 and 2023, leading to increased labor costs and operational disruptions, especially during peak seasons.

Land Availability and Real Estate Costs: The scarcity of land for large-scale warehousing projects near major cities has significantly driven up costs. In regions like Gyeonggi Province, industrial land prices have surged by over 20% since 2020, making it challenging for new entrants and small players to establish warehousing infrastructure.

What are the Regulations and Initiatives which have Governed the Market:

Smart Logistics Industry Promotion Act: The South Korean government enacted the Smart Logistics Industry Promotion Act to support digital transformation across the logistics sector. The regulation mandates the adoption of smart technologies such as AI, robotics, and big data analytics in logistics operations. By the end of 2023, over 20% of logistics centers nationwide had adopted some form of automation or smart warehousing solution in compliance with the act.

Warehouse Safety and Fire Regulation: In response to a series of warehouse fires, South Korea tightened safety protocols under the Industrial Safety and Health Act. Warehousing operators are now required to implement fire prevention systems, conduct regular safety drills, and ensure real-time temperature and smoke monitoring systems. In 2023, compliance checks rose by 30%, particularly targeting cold chain and hazardous material storage facilities.

Eco-Friendly Freight Transport Policy: The Ministry of Land, Infrastructure and Transport (MOLIT) has introduced initiatives aimed at decarbonizing freight logistics. This includes subsidies for the purchase of LNG and electric trucks, as well as incentives for companies adopting rail and sea transport over road freight. In 2023, eco-friendly freight options represented 12% of total inland cargo movement, a figure targeted to reach 25% by 2029.

Zoning and Land Use Regulations for Logistics Parks: Local governments have enforced stricter zoning regulations for the development of large logistics hubs, particularly in proximity to urban centers. Developers are now required to comply with land-use impact assessments, environmental clearance, and infrastructure compatibility standards. In 2023, seven new logistics complexes were approved under these regulations, concentrated in regions like Gyeonggi-do and Chungcheong.

South Korea Logistics and Warehousing Market Segmentation

By Market Structure: The organized logistics sector dominates the South Korean market, driven by large corporations with advanced infrastructure, compliance protocols, and technology integration. These include firms such as CJ Logistics, Lotte Global Logistics, and Hanjin Transportation. Their established national networks, end-to-end service offerings, and investment in smart logistics centers give them a competitive edge. The unorganized segment comprises small and mid-sized logistics providers offering last-mile, courier, and local freight services. These companies are more agile and price-competitive but face scalability and compliance challenges.

By Mode of Transport: Road transport leads the market due to South Korea’s extensive expressway infrastructure and the flexibility it provides for domestic freight and parcel services. Sea freight follows, supported by major ports like Busan and Incheon that handle international cargo. Air freight, though a smaller segment by volume, is critical for high-value, time-sensitive goods. Rail transport is growing slowly, used primarily for bulk and industrial goods over long distances.

By Type of Service: Freight forwarding constitutes the largest share due to high trade volumes and export dependence. Warehousing services are rapidly growing with the rise in e-commerce and retail distribution networks. Courier and parcel services are witnessing significant growth as consumer delivery expectations rise. Cold chain and specialized logistics are also emerging segments, particularly in pharmaceuticals and fresh food sectors.

Competitive Landscape in South Korea Logistics and Warehousing Market

The South Korea logistics and warehousing market is moderately consolidated, with a few dominant players leading the industry and several mid-sized firms and new entrants expanding into specialized logistics services. The rise of e-commerce and demand for automation has also given way to the emergence of tech-driven logistics startups. Key players include CJ Logistics, Hanjin Transportation, Lotte Global Logistics, Korea Post, Pantos Logistics, LogisAll, and eCourier Korea, each offering varying capabilities in freight forwarding, warehousing, and last-mile delivery.

| Company Name | Founding Year | Original Headquarters |

| CJ Logistics Corporation | 1930 | Seoul, South Korea |

| Hyundai Glovis Co., Ltd. | 2001 | Seoul, South Korea |

| Hanjin Transportation Co., Ltd. | 1945 | Seoul, South Korea |

| LX Pantos (formerly Pantos Logistics) | 1977 | Seoul, South Korea |

| Logen Co., Ltd. | 1996 | Seoul, South Korea |

| Korchina Logistics Holdings | 1994 | Seoul, South Korea |

| Daesin Logistics Co., Ltd. | 1991 | Seoul, South Korea |

| Dongbu Express Co., Ltd. | 1969 | Seoul, South Korea |

| Hansol Logistics Co., Ltd. | 1991 | Seoul, South Korea |

| Sunjin Logistics Co., Ltd. | 1990 | Incheon, South Korea |

| Seino Korea Co., Ltd. | 1993 | Seoul, South Korea |

| DHL Supply Chain Korea | 1969 (Korea: ~1970s) | Bonn, Germany |

| DB Schenker Korea Ltd. | 1872 (Korea: 1980s) | Essen, Germany |

| Kuehne + Nagel Korea Ltd. | 1890 (Korea: ~1980s) | Schindellegi, Switzerland |

Some of the recent competitor trends and key information about competitors include:

CJ Logistics: The market leader in South Korea, CJ Logistics operates an extensive domestic and international logistics network. In 2023, the company expanded its Smart Hub Terminal in Gunpo, integrating automated sorting systems and AI-based route optimization, which increased delivery capacity by 22% year-over-year.

Hanjin Transportation: Known for its strong presence in freight forwarding and parcel services, Hanjin reported 15% YoY growth in its e-commerce logistics segment in 2023. The company has invested in EV delivery fleets to meet sustainability goals and address urban delivery challenges.

Lotte Global Logistics: Leveraging synergies from the Lotte Group, the firm focuses heavily on FMCG and retail logistics. In 2023, Lotte launched a new temperature-controlled warehouse facility in Icheon, targeting pharmaceutical and food industries. This expansion increased their cold chain capacity by 30%.

Korea Post: As the state-owned postal and logistics provider, Korea Post continues to be a key player in last-mile delivery. In 2023, it processed over 3.5 billion parcels, supported by its extensive nationwide network. It has also begun pilots using drones for rural delivery routes.

Pantos Logistics: A key global logistics subsidiary of LG Group, Pantos focuses on high-tech, electronics, and heavy industries. In 2023, the company opened a new logistics center near Incheon Airport, dedicated to handling air freight for semiconductors and electronics exports.

LogisAll: Specializing in pallet pooling and logistics IT services, LogisAll introduced a blockchain-enabled inventory tracking system in 2023. The initiative is aimed at improving transparency and reducing shrinkage across distribution networks.

eCourier Korea: A rising player in urban logistics and B2C deliveries, eCourier Korea gained traction with same-day delivery services in Seoul and Busan. In 2023, the company expanded its smart locker infrastructure, adding over 1,200 new locations to support contactless delivery demand.

What Lies Ahead for South Korea Logistics and Warehousing Market?

The South Korea logistics and warehousing market is projected to witness sustained growth through 2029, with a strong CAGR supported by technological innovation, rising e-commerce activity, and government-backed infrastructure investments. As businesses continue to optimize their supply chains and consumers demand faster delivery, the industry is set for continued transformation.

Expansion of Smart Warehousing and Automation: The adoption of robotics, AI-driven warehouse management systems (WMS), and IoT sensors is expected to accelerate. By 2029, a significant share of large-scale logistics hubs in metropolitan areas will be fully automated, enabling greater accuracy, speed, and cost-efficiency in warehousing operations.

Rising Role of Cold Chain and Healthcare Logistics: With increased demand for pharmaceuticals, biotechnology products, and fresh food, South Korea’s cold chain logistics segment is projected to grow rapidly. New investments in temperature-controlled warehouses and real-time tracking technologies will become essential to meet strict compliance and safety standards.

Sustainability and Green Logistics: Environmental concerns are driving logistics companies to invest in eco-friendly practices such as electric delivery vehicles, solar-powered warehouses, and optimized route planning to reduce carbon emissions. By 2029, over 35% of last-mile deliveries in urban centers are expected to be made using electric or low-emission vehicles.

Integration of Multimodal Transport Networks: To overcome land constraints and improve efficiency, logistics providers will increasingly leverage integrated rail, sea, and road networks. Government plans to expand inland rail terminals and enhance port connectivity will play a key role in boosting multimodal logistics volumes.

Future Outlook and Projections for South Korea Logistics and Warehousing Market on the Basis of Revenues in USD Billion, 2024-2029

South Korea Logistics and Warehousing Market Segmentation

- By Market Structure:

o Organized Sector

o Unorganized Sector

o Public Sector Logistics Providers

o Private 3PL Providers

o In-house Logistics Units

o Asset-Light Logistics Companies - By Type of Service:

o Freight Forwarding

o Warehousing

o Courier and Parcel

o Cold Chain Logistics

o Reverse Logistics

o Value-Added Services (Labeling, Packaging, Assembly) - By Mode of Transport:

o Road

o Rail

o Air

o Sea

o Multimodal - By End-User Industry:

o E-commerce and Retail

o Manufacturing

o Pharmaceuticals and Healthcare

o Food and Beverage

o Automotive

o Electronics and High-Tech

o FMCG - By Region:

o Seoul Capital Area (Seoul, Incheon, Gyeonggi)

o Chungcheong Region

o Gyeongsang Region (Busan, Daegu, Ulsan)

o Jeolla Region

o Gangwon Region

o Jeju Island

Players Mentioned in the Report:

Freight Forwarding Companies

- CJ Logistics

- LX Pantos

- Nippon Express Korea

- Yusen Logistics Korea

- DSV Korea

- Dimerco Express Korea

- JAS Korea

- AIT Worldwide Logistics Korea

- Crane Worldwide Logistics Korea

- Air Tiger Express Korea

- Omni Logistics Korea

Warehousing Companies

- Rhenus Logistics Korea

- Nippon Express Korea

- Alps Logistics Korea

- Omni Logistics Korea

- Allcargo Logistics Korea

- Hyundai Glovis

- Hansol Logistics

- AJ Networks

- EMRO Incorporated

E-Commerce Logistics Companies

- Coupang

- CJ Logistics

- FedEx Korea

- DHL Korea

- SF Express Korea

- Lotte Global Logistics

- MeshKorea

- WEKEEP

- Techtaka (ARGO)

- KOISRA

- Cainiao Korea

Express Logistics Companies

CJ Logistics

Korea Post

DHL Express Korea

FedEx Korea

Aramex Korea

OCS Korea

SF Express Korea

Lotte Global Logistics

DB Schenker Korea

Key Target Audience:

- 3PL and 4PL Logistics Providers

- E-commerce and Retail Companies

- Cold Chain Logistics Operators

- Industrial Park and Warehouse Developers

- Port and Freight Terminal Operators

- Government Bodies (e.g., MOLIT – Ministry of Land, Infrastructure and Transport)

- Industry Associations (e.g., Korea Integrated Logistics Association)

- Research and Consulting Firms

Time Period:

- Historical Period: 2018–2023

- Base Year: 2024

- Forecast Period: 2024–2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Macroeconomic Framework for South Korea Including GDP, GDP Growth and GDP Contribution by Sector

4.2. Logistics Sector Contribution to GDP and How the Contribution Has Been Changing in the Historical Assessment

4.3. Ease of Doing Business in South Korea

4.4. LPI Index of South Korea and Improvements in the Last Decade

4.5. Customs Procedures and Customs Charges in South Korea Logistics Market

5.1. Landscape of Industrial Parks, Logistics Parks and Free Economic Zones in South Korea (Location, Sector Focus and Incentives)

5.2. Current Scenario for Logistics Infrastructure in South Korea

5.3. Road Infrastructure in South Korea Including Road Network, Toll Charges and Toll Network, Major Goods Traded through Road, Major Flow Corridors for Road

5.4. Air Infrastructure in South Korea Including Total Volume Handled, FTK for Air Freight, Major Inbound and Outbound Flow Corridors, Major Goods Traded through Air, Number of Commercial and Passenger Airports, Air Freight Volume by Airports and Other Parameters (South Korea Air Cargo Structure)

5.5. Sea Infrastructure in South Korea Including Total Volume Handled, FTK for Sea Freight, Major Inbound and Outbound Flow Corridors, Major Goods Traded through Sea, Number of Ports for Coastal and Ocean Freight, Number of Vessels, Sea Freight Volume by Ports and Other Parameters (Container and Bulk Shipping in South Korea)

5.6. Rail Infrastructure in South Korea Including Total Volume Handled, FTK for Rail Freight, Major Inbound and Outbound Flow Corridors, Major Goods Traded through Rail and Other Parameters (Intermodal and Bulk Rail in South Korea)

6.1. Basis Revenues, 2018-2024P

7.1. By Segment (Freight Forwarding, Warehousing, CEP and Value-Added Services)

7.2. By End User Industries

8.1. Market Overview and Genesis

8.2. South Korea Freight Forwarding Market Size by Revenues

8.3. South Korea 3PL Freight Forwarding Market Segmentation

8.3.1. By Mode of Freight Transport (Road, Sea, Air and Rail)

8.3.1.1. Price per FTK for Road, Air, Sea and Rail in South Korea

8.3.1.2. Road Freight in South Korea (Domestic Volume, FTK and Revenue; Number of Registered Commercial Freight Vehicles)

8.3.1.3. Road Freight Domestic Corridors in South Korea (Seoul-Busan, Capital Region-Southeast Industrial Belt and Other Key Corridors)

8.3.1.4. Ocean Freight in South Korea (Domestic and International Volume, FTK and Revenue; Volume by Commodity; Key Container and Bulk Port Statistics)

8.3.1.5. Air Freight in South Korea (Domestic and International Volume, FTK and Revenue; High-value and Time-sensitive Cargo Mix)

8.3.1.6. Rail Freight in South Korea (Volume, FTK and Revenue; Volume by Commodity and Region; Intermodal Connectivity with Ports and ICDs)

8.3.1.7. Export-Import Scenario for South Korea

8.3.2. By Intercity Road Freight Corridors

8.3.3. By International Freight Corridors

8.3.4. By End User

8.4. Snapshot of Freight Truck Aggregators and Digital Freight Platforms in South Korea Including Company Overview, USP, Business Strategies, Future Plans, Business Model, Number of Fleets, Margins/Commission, Number of Bookings, Major Clients, Average Booking Amount, Major Routes and Other Parameters

8.5. Competitive Landscape in South Korea Freight Forwarding Market

8.5.1. Heat Map of Major Players in South Korea Freight Forwarding on the Basis of Service Offering (Mode Coverage, Sector Focus and Value-added Services)

8.5.2. Market Share of Major Players in South Korea Freight Forwarding Market

8.5.3. Cross Comparison of Major Players in South Korea Freight Forwarding Companies on the Basis of Parameters

8.5.3.1. Total Freight Forwarding Revenue in South Korea

8.5.3.2. Volume Handled by Mode (Road, Sea, Air and Rail) in South Korea

8.5.3.3. Number and Location of Logistics Facilities and Warehouses in South Korea

8.5.3.4. Fleet Size and Composition (Owned and Subcontracted Trucks, Specialized Equipment) in South Korea

8.5.3.5. Coverage of International Trade Lanes (China, Japan, USA, Europe and ASEAN) from South Korea

8.5.3.6. Degree of Technology Adoption (WMS/TMS Integration, Tracking, Digital Platforms and Automation) in South Korea

8.5.3.7. Sector Specialization (Automotive, Electronics, Retail, Pharma, Cold Chain and Project Cargo) in South Korea

8.5.3.8. Service Quality and Performance Metrics (On-time Delivery, Damage Ratio, Customer Base and Contract Tenure in South Korea)

8.5.4. Profiles of Major Freight Forwarding and Integrated Logistics Companies in South Korea (Company Overview, Service Portfolio and Strategic Positioning)

8.6. South Korea Freight Forwarding Future Market Size by Revenues

8.7. South Korea Freight Forwarding Market Future Segmentation

8.7.1. Future Market Segmentation by Mode of Freight Transport (Road, Sea, Air and Rail)

8.7.2. Future Market Segmentation by International Freight Corridors

8.7.3. Future Market Segmentation by End User

9.1. Market Overview and Genesis

9.2. Value Chain Analysis in South Korea Warehousing Market Including Entities, Margins, Role of Each Entity, Process Flow, Challenges and Other Aspects

9.3. South Korea Warehousing Market Size on the Basis of Revenues and Warehousing Space (Historical Period for South Korea Warehousing)

9.4. South Korea Warehousing Market Segmentation

9.4.1. South Korea Warehousing Revenue by Business Model

9.4.2. South Korea Warehousing by Type of Warehouse

9.4.3. South Korea Warehousing Revenue by End User

9.4.4. 3PL Warehousing Space by Region

9.5. Competitive Landscape in South Korea Warehousing Market (Key Operators and Asset Owners in South Korea)

9.5.1. Market Share of Top Companies in South Korea Warehousing Market

9.5.2. Cross Comparison of Top Warehousing Companies on the Basis of Parameters Including Company Overview, USP, Business Strategy, Future Plans, Technology, Revenues from Warehousing, Number of Warehouses, Warehousing Space, Location of Warehouses, Type of Warehouses, Occupancy Rate, Rental Rates, Clients and Other Metrics (South Korea Warehousing Competitive Matrix)

9.6. South Korea Warehousing Future Market Size on the Basis of Revenues

9.7. South Korea Warehousing Market Future Segmentation

9.7.1. South Korea Warehousing Revenue by Business Model

9.7.2. South Korea Warehousing Revenue by Type of Warehouse

9.7.3. South Korea Warehousing Revenue by End User

10.1. Market Overview and Genesis

10.2. Value Chain Analysis in South Korea CEP Market Including Entities, Margins, Role of Each Entity, Process Flow, Challenges and Other Aspects

10.3. Revenue Composition and Contribution Between First Mile/Mid Mile and Last Mile Delivery-Analysis for Domestic and International Shipments

10.4. South Korea CEP Market Size on the Basis of Revenues and Shipments

10.5. South Korea CEP Market Segmentation

10.5.1. Segmentation by Mails and Documents, E-commerce Shipments and Express Cargo (Product Mix in South Korea CEP)

10.5.2. Segmentation by International and Domestic Express

10.5.3. Segmentation by B2B, B2C and C2C

10.5.4. Segmentation by Period of Delivery

10.6. Competitive Landscape in South Korea CEP Market

10.6.1. Overview and Genesis, Market Nature, Market Stage and Major Competing Parameters (Coverage, Speed, Price and Technology in South Korea CEP)

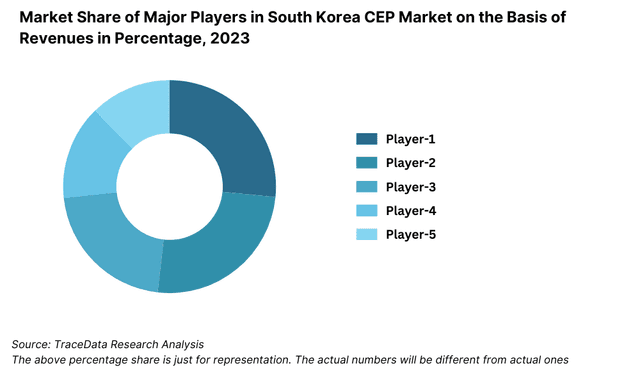

10.6.2. Market Share of Companies in South Korea CEP Market on the Basis of Revenues/Number of Shipments (Base Year CEP Market Shares in South Korea)

10.6.3. Market Share of Top Companies in South Korea E-commerce Shipment Market on the Basis of Revenues/Number of Shipments

10.6.4. Cross Comparison of Top South Korea CEP Companies on the Basis of Parameters Including Company Overview, USP, Business Strategy, Future Plans, Technology, Number of Last Mile Delivery Shipments, Revenues, Major Clients, Number of Fleets, Number of Employees, Number of Riders, Number of Service Points/Areas Covered, Major Service Offering and Other Metrics

10.7. South Korea CEP Market Size on the Basis of Revenues and Shipments

10.8. South Korea CEP Market Future Segmentation

10.8.1. Segmentation by Mails and Documents, E-commerce Shipments and Express Cargo

10.8.2. Segmentation by International and Domestic Express

10.8.3. Segmentation by B2B, B2C and C2C

10.8.4. Segmentation by Period of Delivery

11.1. Customer Cohort Analysis and End User Paradigm for Different Industry Verticals under Logistics Sector

11.2. Understanding of Logistics Spend by End User

11.3. End User Preferences in Terms of In-house or Outsourcing Logistics Services and Reason for Selection; Segregation by Size of Company on the Basis of Revenues

11.4. Major Logistics Companies Specialized in Serving Each Type of End User

11.5. Detailed Landscape of Each End User across Parameters Including Major Products Manufactured and Traded, Emerging Products, Type of Services Required and Outsourced, Major Companies, Contract Duration, Likelihood to Recommend, Market Orientation, Major Clusters, Type of Sourcing Preference, Pain Points, Facilities/Services Required, Future Outlook and Market Size for End User Industry Verticals with Growth Rate (South Korea End User Profiles)

12.1. Basis Revenues, 2025-2029

13.1. By Segment (Freight Forwarding, Warehousing, CEP and Value-Added Services)

13.2. By End User Industries

13.3. Market Analysts’ Recommendations

13.4. Opportunity Analysis

6.1. Basis Revenues

12.1. Basis Revenues

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities within the South Korea Logistics and Warehousing Market. This includes 3PL/4PL service providers, freight forwarders, warehouse developers, cold chain operators, e-commerce logistics players, and key end-user industries (e.g., retail, manufacturing, pharma, etc.).

Basis this ecosystem, we shortlist leading 6–8 logistics providers in the country based on parameters such as revenue, warehouse capacity (sq. meters), fleet size, and service coverage.

Sourcing is conducted through industry whitepapers, trade association reports, government publications, and proprietary subscription-based databases to perform an initial desk review.

Step 2: Desk Research

An exhaustive secondary research process is carried out by referencing public data sources, company reports, industry journals, and proprietary intelligence platforms.

This process includes mapping historical trends, revenue estimations, service-line segmentation (freight forwarding, courier, warehousing), warehousing capacity trends, and identifying key infrastructure developments (e.g., smart logistics complexes, port expansions).

Company-specific data (such as press releases, investment announcements, fleet modernization plans, and operational metrics) is aggregated to analyze strategic positioning and future outlooks.

Step 3: Primary Research

A targeted primary research campaign is executed through telephonic and virtual interviews with top-level executives (e.g., CEOs, Head of Logistics, Regional Directors) and operational leads from logistics firms and end-user companies (e.g., e-commerce, FMCG, automotive).

These interviews help validate market hypotheses, confirm key trends (e.g., automation, cold chain growth), and gather pricing benchmarks and operational KPIs.

A bottom-to-top approach is used to estimate logistics volume handled (in tons or TEUs), warehouse occupancy, and revenue per sqm, which is then aggregated to arrive at the overall market size.

Additionally, disguised interviews are conducted posing as prospective customers to verify pricing models, delivery lead times, service SLAs, and warehouse availability.

Step 4: Sanity Check

Both bottom-up and top-down modeling frameworks are applied to perform a triangulated market size assessment.

A comparative assessment is conducted against benchmarks such as GDP contribution by logistics, logistics cost as % of GDP, average parcel volumes, warehouse sq.m. per capita, and more.

- The model is stress-tested for different growth scenarios (e.g., high-growth e-commerce vs. moderate industry recovery) to ensure data accuracy and consistency.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The South Korea logistics and warehousing market is poised for steady expansion, reaching an estimated valuation of KRW 48 Trillion in 2023. This potential is underpinned by the country’s strong export-driven economy, rapid growth of e-commerce, and increasing investments in smart logistics infrastructure. With supportive government policies and technology adoption, the sector is expected to maintain a healthy growth trajectory through 2029.

Major players in the South Korean logistics market include CJ Logistics, Hanjin Transportation, Lotte Global Logistics, Korea Post, and Pantos Logistics. These companies have wide domestic and international networks, robust warehousing infrastructure, and are investing heavily in digital logistics solutions. Emerging players such as LogisAll and eCourier Korea are also gaining traction in niche segments like urban delivery and pallet pooling.

Key growth drivers include the rise of e-commerce, which has increased demand for last-mile delivery and fulfillment services; government-led smart logistics initiatives to digitize supply chains; and expanding international trade, which drives freight forwarding and port logistics. Additionally, the shift toward cold chain logistics and sustainable delivery models is unlocking new growth opportunities.

The market faces challenges such as urban congestion and high last-mile delivery costs, especially in densely populated cities like Seoul. Rising industrial land prices and limited land availability pose barriers for new warehousing projects. Labor shortages in warehousing and trucking, along with fragmentation among small logistics providers, further limit operational efficiency and scalability. Regulatory compliance, particularly around safety and environmental norms, also increases the cost burden on smaller players.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0