Spain Auto Finance Market Outlook to 2029

By Vehicle Type (New and Used), By Lender Type (Banks, NBFCs, OEM Captives), By Loan Tenure, By Interest Rate Type, By Consumer Age Group, and By Region

Report Overview

Report Code

TDR0170

Coverage

Europe

Published

May 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Spain Auto Finance Market Outlook to 2029 – By Vehicle Type (New and Used), By Lender Type (Banks, NBFCs, OEM Captives), By Loan Tenure, By Interest Rate Type, By Consumer Age Group, and By Region” provides a comprehensive analysis of the auto finance industry in Spain. The report covers an overview and genesis of the industry, overall market size in terms of revenue and loan disbursals, market segmentation; trends and developments, regulatory landscape, customer-level profiling, key challenges and issues, and competitive landscape including the market share of major players, cross-comparison, and company profiling of leading auto finance...

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Spain Auto Finance Market Outlook to 2029 – By Vehicle Type (New and Used), By Lender Type (Banks, NBFCs, OEM Captives), By Loan Tenure, By Interest Rate Type, By Consumer Age Group, and By Region” provides a comprehensive analysis of the auto finance industry in Spain. The report covers an overview and genesis of the industry, overall market size in terms of revenue and loan disbursals, market segmentation; trends and developments, regulatory landscape, customer-level profiling, key challenges and issues, and competitive landscape including the market share of major players, cross-comparison, and company profiling of leading auto finance providers in Spain. The report concludes with future market projections based on disbursals and revenue, by market segment, loan product type, geography, consumer demographics, as well as success stories and strategic imperatives for market participants.

Spain Auto Finance Market Overview and Size

The Spain Auto Finance Market reached a valuation of EUR 18.7 Billion in 2023, driven by a rebound in vehicle sales post-pandemic, increasing digitalization in loan disbursal processes, and favorable interest rates. The market is dominated by players such as BBVA Auto, Santander Consumer Finance, CaixaBank Payments & Consumer, Cetelem, and ALD Automotive. These institutions offer competitive loan terms, flexible repayment options, and bundled insurance-financing products aimed at enhancing customer acquisition and retention.

In 2023, Santander Consumer Finance rolled out a fully digital auto loan journey, allowing consumers to complete loan applications, approvals, and disbursals entirely online. This move was aimed at capturing the growing segment of tech-savvy consumers and streamlining operational costs. Madrid, Catalonia, and Andalusia emerged as high-demand regions, thanks to higher vehicle ownership rates and better financing infrastructure.

Market Size for Spain Auto Finance Industry on the Basis of Loan Disbursed, 2018–2023

What Factors are Leading to the Growth of Spain Auto Finance Market:

Post-COVID Recovery & Pent-Up Demand: Following the economic downturn of 2020–21, Spain witnessed a surge in both new and used vehicle demand, largely driven by deferred purchases and a renewed interest in private vehicle ownership. In 2023, auto loan disbursals increased by 11.2% YoY, driven by higher disposable incomes and improved consumer confidence.

Attractive Financing Terms: Historically low interest rates in Spain (ranging between 4.5% to 6.8%) have made vehicle loans more affordable for the mass market. Lenders are also offering zero-down-payment schemes, longer loan tenures (up to 84 months), and bundled deals with maintenance and insurance to drive conversions.

Used Car Financing Growth: A major shift towards used vehicles is evident, especially among young and cost-conscious buyers. In 2023, used car finance accounted for 44% of the overall auto finance disbursals, up from 36% in 2020. Financing used vehicles is now more streamlined with digital verification processes and vehicle history reports.

Which Industry Challenges Have Impacted the Growth for Spain Auto Finance Market

High Interest Rates and Inflationary Pressure: In recent years, Spain has experienced economic volatility, with inflation and interest rates impacting consumer purchasing power. In 2024, the average auto loan interest rate rose to 8.2%, up from 6.5% in 2022. This increase has led to reduced affordability for auto loans, particularly among younger and lower-income consumers, discouraging many from financing vehicle purchases.

Stringent Credit Assessment Criteria: Spanish banks and lenders have maintained conservative credit assessment practices, particularly after the COVID-19 pandemic. As of 2023, approximately 36% of loan applications for used vehicles were rejected due to insufficient credit scores or unstable income documentation. This restricts access for a considerable segment of the population, particularly gig economy workers and first-time buyers.

Limited Penetration of Used Car Financing: While financing for new cars is well-established, used car financing remains underpenetrated. Data from 2023 shows that only 42% of used car purchases in Spain were financed through formal lending institutions, compared to over 70% for new vehicles. This is partly due to a lack of tailored financial products for older vehicles and limited awareness among consumers.

What are the Regulations and Initiatives Which Have Governed the Market

EU Emissions Standards and Scrappage Policies: Spain, as part of the European Union, adheres to stringent emissions regulations. Older vehicles with high CO₂ output face higher taxes and restrictions in urban zones. In 2023, Spain expanded its Low Emission Zones (LEZs) in major cities like Madrid and Barcelona, indirectly influencing auto finance by promoting loans for newer, greener vehicles.

Plan MOVES III Subsidy Program: The Spanish government continues to support the “Plan MOVES III” scheme, which provides subsidies for electric vehicles (EVs) and plug-in hybrids. Under this initiative, buyers can receive up to €7,000 in subsidies when scrapping an old vehicle and financing a new EV. As of 2023, more than 68,000 buyers benefited from the program, boosting demand for auto loans tied to EVs.

Digital Finance and Open Banking Regulations: The introduction of open banking under the EU’s PSD2 directive has begun reshaping the lending landscape in Spain. Consumers now have better access to comparative loan offers and faster approval processes. In 2023, over 25% of auto loans were facilitated through digital platforms, driven by fintech adoption and regulatory support for online lending innovation.

Spain Auto Finance Market Segmentation

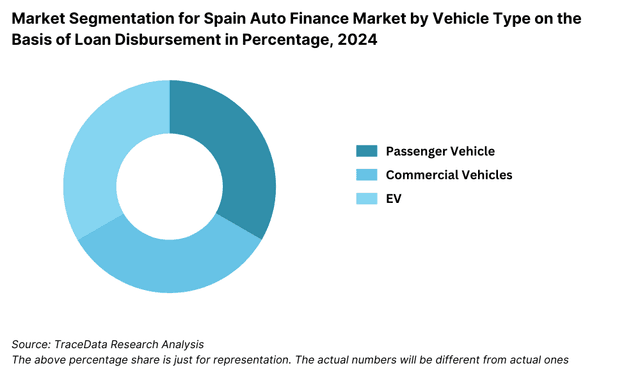

By Vehicle Type: New vehicles dominate the auto finance market due to widespread promotional financing schemes offered by OEMs and banks, especially for low-emission models. These deals often feature lower interest rates, zero down payment options, and extended repayment terms. However, financing for used vehicles is steadily gaining ground, as more consumers seek affordable ownership solutions amidst rising new car prices. Used vehicle financing accounted for a growing share in 2023, particularly among millennials and price-sensitive segments.

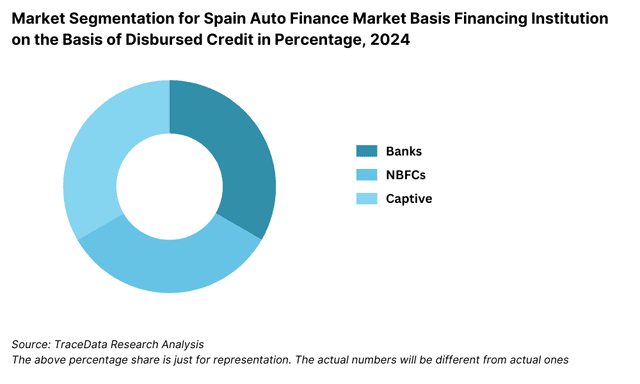

By Lender Type: Banks lead the market due to their vast branch network, competitive interest rates, and strong brand credibility. OEM Captive Finance arms like Volkswagen Financial Services and Toyota Kreditbank hold a significant share, particularly for new cars, offering bundled incentives such as extended warranties and loyalty discounts. Non-Banking Financial Companies (NBFCs) and fintech players are emerging in the used car finance segment, offering quick approvals and flexible repayment structures tailored for underserved segments.

By Loan Tenure: The most common loan tenure in Spain ranges between 48 to 60 months, offering a balance between manageable EMIs and total interest outgo. Shorter tenures (24-36 months) are preferred by high-income buyers or for used vehicles, where faster repayment is desirable. Longer tenures (above 60 months) are more common in EV financing, supported by government incentives and lower upfront payments.

Competitive Landscape in Spain Auto Finance Market

The Spain auto finance market is moderately concentrated, with a combination of traditional banks, OEM captive finance arms, and emerging fintech lenders shaping the competitive environment. While major players like Santander Consumer Finance, BBVA, and CaixaBank dominate, the rise of digital platforms and auto-specific lenders like Cetelem, ALD Automotive, and Younited Credit is creating greater diversification and accessibility in the market.

| Company Name | Founding Year | Original Headquarters |

| Santander Consumer Finance | 1987 | Madrid, Spain |

| BBVA Autorenting | 2001 | Bilbao, Spain |

| CaixaBank Payments & Consumer | 2011 | Barcelona, Spain |

| Mobilize Financial Services | 1974 | Paris, France |

| CA Auto Bank | 1925 | Turin, Italy |

| LeasePlan Spain (Ayvens) | 1963 | Amsterdam, Netherlands |

| Deutsche Leasing Iberica | 1962 | Bad Homburg, Germany |

| Lendrock | 2016 | Madrid, Spain |

| Unicaja Banco | 1991 | Málaga, Spain |

| Amovens | 2013 | Madrid, Spain |

Some of the recent competitor trends and key information about competitors include:

Santander Consumer Finance: As the leading auto finance provider in Spain, Santander CF financed over 500,000 vehicles in 2023. The bank's comprehensive digital onboarding, flexible repayment plans, and partnerships with car dealers have solidified its position in both new and used car financing segments.

BBVA Auto Finance: Known for its strong customer base and digital loan processing, BBVA introduced real-time credit scoring and pre-approved offers in 2023, helping reduce loan approval time by 30%. The bank has seen notable growth in financing electric and hybrid vehicles, aligned with national green mobility goals.

CaixaBank Payments & Consumer: CaixaBank's auto lending division witnessed an 18% year-on-year growth in loan disbursals in 2023. Their collaboration with local dealerships and strategic EV finance packages contributed significantly to this performance.

Cetelem Spain: A specialist in consumer credit, Cetelem grew its auto loan portfolio by 22% in 2023, focusing on used car financing and offering competitive fixed-rate products. Its fully online application process and rapid disbursal model have been key differentiators.

ALD Automotive: A leader in auto leasing and fleet management, ALD is expanding its footprint in retail auto finance. In 2023, it launched a vehicle subscription model in Spain, appealing to younger, urban consumers seeking flexible ownership alternatives.

Younited Credit: This European fintech lender continues to disrupt the Spanish market with AI-driven risk assessments and seamless digital platforms. In 2023, Younited financed over €150 million in auto loans in Spain, primarily targeting tech-savvy millennials through app-based loan approvals.

What Lies Ahead for Spain Auto Finance Market?

The Spain auto finance market is projected to witness steady growth through 2029, with a moderate but consistent CAGR driven by economic recovery, digital adoption, and increasing preference for flexible ownership models. As mobility patterns evolve and financial innovation continues, auto financing is expected to play a central role in vehicle accessibility across demographics.

Rise of Electric Vehicle Financing: With Spain’s firm commitment to sustainability and the EU’s push toward carbon neutrality, the auto finance sector is expected to see a significant uptick in financing for electric vehicles (EVs). Government-backed incentives under programs like Plan MOVES III will continue to encourage both lenders and consumers to favor EVs over traditional internal combustion engine vehicles.

Expansion of Digital Lending Platforms: The ongoing shift towards online financial services will further revolutionize the auto finance process. By 2029, a majority of auto loans in Spain are expected to be initiated and processed digitally, with instant credit checks, personalized loan offers, and AI-powered decision-making becoming industry norms. This digital convenience will enhance loan accessibility for younger, tech-savvy consumers.

Growing Popularity of Subscription and Leasing Models: Alternative vehicle ownership models such as car subscriptions and flexible leasing plans are set to gain momentum, especially among urban dwellers and Gen Z consumers. These options often come bundled with finance elements, providing a hybrid model that bridges traditional loans and modern usage-based access to vehicles.

Increased Focus on Financial Inclusion: By 2029, there will be a greater emphasis on creating inclusive financial products, particularly for gig economy workers, self-employed individuals, and immigrants who often struggle with credit eligibility under traditional systems. Fintechs and NBFCs are expected to lead this transformation by leveraging alternative data for credit scoring.

Future Outlook and Projections for Spain Car Finance Market Size on the Basis of Loan Disbursements in USD Billion, 2024-2029

Spain Auto Finance Market Segmentation

• By Vehicle Type:

o New Vehicles

o Used Vehicles

• By Lender Type:

o Banks

o OEM Captive Finance Companies

o Non-Banking Financial Companies (NBFCs)

o Fintech/Digital Lending Platforms

• By Loan Tenure:

o Less than 24 Months

o 24–36 Months

o 37–48 Months

o 49–60 Months

o More than 60 Months

• By Interest Rate Type:

o Fixed Interest Rate

o Variable Interest Rate

• By Consumer Age Group:

o 18–24 Years

o 25–34 Years

o 35–44 Years

o 45–54 Years

o 55+ Years

• By Region:

o Madrid

o Catalonia

o Andalusia

o Valencia

o Basque Country

o Other Regions

Players Mentioned in the Report (Banks):

- Banco Santander

- BBVA

- CaixaBank

- Banco Sabadell

- Bankinter

- Unicaja Banco

- Abanca

- Kutxabank

- Ibercaja Banco

- Cajamar Caja Rural

Players Mentioned in the Report (NBFCs):

- Lendrock

- Fintonic

- Boopos

- ID Finance

- SeQura

- Twinco Capital

- Pagantis

- Grupo BC

- TEKNIKA BEREZIAK SL (MRDCars

Players Mentioned in the Report (Captive):

- Santander Consumer Finance

- Stellantis Financial Services

- Volkswagen Financial Services Spain

- Toyota Financial Services Spain

- BMW Financial Services Spain

- Mercedes-Benz Financial Services Spain

- Nissan Finance Spain

- Ford Credit Spain

- Hyundai Capital Spain

- CA Auto Bank

Key Target Audience:

• Auto Finance Companies

• Commercial and Retail Banks

• OEMs and Captive Finance Arms

• Digital Lending Platforms and Fintechs

• Government Agencies (e.g., Dirección General de Tráfico, Ministry for the Ecological Transition)

• Automotive Dealerships

• Investment and Research Institutions

Time Period:

• Historical Period: 2018–2023

• Base Year: 2024

• Forecast Period: 2024–2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-Role of Entities, Stakeholders, and challenges they face.

4.2. Relationship and Engagement Model between Banks-Dealers, NBFCs-Dealers and Captive-Dealers-Commission Sharing Model, Flat Fee Model and Revenue streams

5.1. New Car and Used Car Sales in Spain by type of vehicle, 2018-2024

8.1. Credit Disbursed, 2018-2024

8.2. Outstanding Loan, 2018-2024

9.1. By Market Structure (Bank-Owned, Multi-Finance, and Captive Companies), 2023-2024

9.2. By Vehicle Type (Passenger, Commercial and EV), 2023-2024

9.3. By Region, 2023-2024

9.4. By Type of Vehicle (New and Used), 2023-2024

9.5. By Average Loan Tenure (0-2 years, 3-5 years, 6-8 years, above 8 years), 2023-2024

10.1. Customer Landscape and Cohort Analysis

10.2. Customer Journey and Decision-Making

10.3. Need, Desire, and Pain Point Analysis

10.4. Gap Analysis Framework

11.1. Trends and Developments for Spain Car Finance Market

11.2. Growth Drivers for Spain Car Finance Market

11.3. SWOT Analysis for Spain Car Finance Market

11.4. Issues and Challenges for Spain Car Finance Market

11.5. Government Regulations for Spain Car Finance Market

12.1. Market Size and Future Potential for Online Car Financing Aggregators, 2018-2029

12.2. Business Model and Revenue Streams

12.3. Cross Comparison of Leading Digital Car Finance Companies Based on Company Overview, Revenue Streams, Loan Disbursements/Number of Leads Generated, Operating Cities, Number of Branches, and Other Variables

13.1. Finance Penetration Rate and Average Down Payment for New and Used Cars, 2018-2029

13.2. How Finance Penetration Rates are Changing Over the Years with Reasons

13.3. Type of Car Segment for which Finance Penetration is Higher

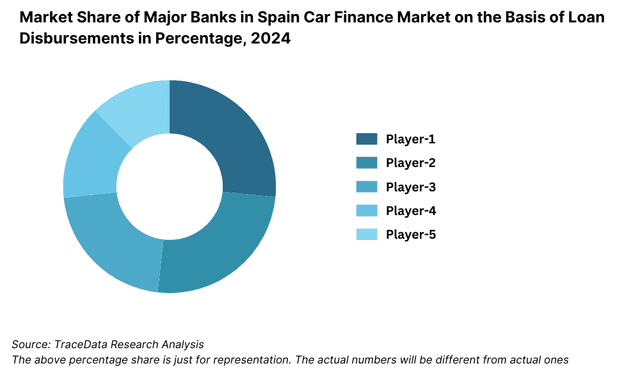

17.1. Market Share of Key Banks in Spain Car Finance Market, 2024

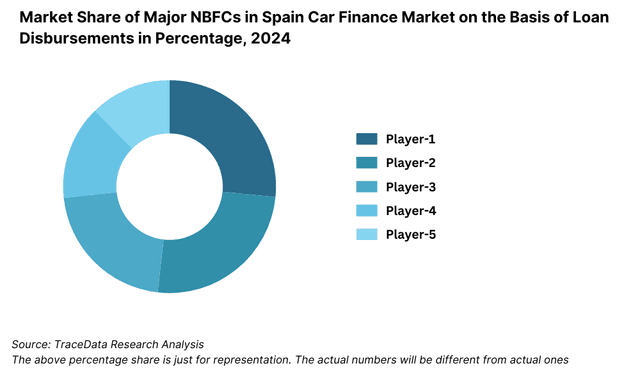

17.2. Market Share of Key NBFCs in Spain Car Finance Market, 2024

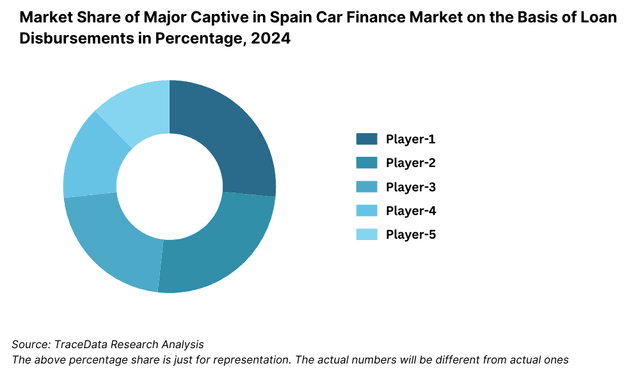

17.3. Market Share of Key Captive in Spain Car Finance Market, 2024

17.4. Benchmark of Key Competitors in Spain Car Finance Market, including Variables such as Company Overview, USP, Business Strategies, Strengths, Weaknesses, Business Model, Number of Branches, Product Features, Interest Rate, NPA, Loan Disbursed, Outstanding Loans, Tie-Ups and others

17.5. Strengths and Weaknesses

17.6. Operating Model Analysis Framework

17.7. Gartner Magic Quadrant

17.8. Bowmans Strategic Clock for Competitive Advantage

18.1. Credit Disbursed, 2025-2029

18.2. Outstanding Loan, 2025-2029

19.1. By Market Structure (Bank-Owned, Multi-Finance, and Captive Companies), 2025-2029

19.2. By Vehicle Type (Passenger, Commercial and EV), 2025-2029

19.3. By Region, 2025-2029

19.4. By Type of Vehicle (New and Used), 2025-2029

19.5. By Average Loan Tenure (0-2 years, 3-5 years, 6-8 years, above 8 years), 2025-2029

19.6. Recommendations

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities within the Spain Auto Finance Market. Based on this ecosystem, we shortlist 5–6 leading lenders and fintech companies in the country using parameters such as total loan disbursals, market reach, interest rate competitiveness, and digital presence.

Sourcing is conducted through a combination of industry reports, news articles, government publications, financial portals, and proprietary databases to gather relevant desk research material and build an understanding of the market landscape.

Step 2: Desk Research

An in-depth desk research process is carried out using secondary and proprietary data sources. This includes examining macroeconomic data, interest rate trends, vehicle ownership ratios, and auto loan penetration across regions in Spain.

We also analyze company-level financials and strategies by reviewing annual reports, investor presentations, earnings calls, press releases, and product brochures. The objective is to build a strong base of market intelligence on loan volumes, average interest rates, tenure preferences, and borrower demographics.

Step 3: Primary Research

A series of structured interviews is conducted with stakeholders including executives from banks, NBFCs, OEM captive finance arms, and digital lending platforms, as well as auto dealers and consumers. These interviews serve to validate secondary data, test hypotheses, and collect qualitative insights on trends, challenges, and innovations in auto finance.

Disguised interviews are also executed, in which our researchers engage players under the guise of prospective customers. This helps cross-check real-world operational metrics, loan processes, turnaround time, pricing models, and customer experience — and compare them against secondary findings.

The primary research also includes bottom-up estimation of loan disbursals by major players, which is then aggregated to calculate total market size.

Step 4: Sanity Check

- A top-down and bottom-up triangulation model is used to verify the accuracy of findings. Market sizing, CAGR projections, and segmentation shares are evaluated for internal consistency, while expert inputs are used to finalize assumptions and build robust financial models.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Spain auto finance market holds strong growth potential, projected to expand steadily through 2029. In 2023, the market showed robust activity, driven by rising vehicle ownership, supportive government EV incentives, and increasing digital adoption in loan processing. The sector is poised to benefit from the growing demand for electric and used vehicles, along with the expansion of online lending platforms, which are improving accessibility and loan processing speeds.

The Spain Auto Finance Market is led by key players such as Santander Consumer Finance, BBVA Auto Finance, and CaixaBank Payments & Consumer. These institutions dominate due to their expansive branch networks, competitive loan products, and partnerships with auto dealerships. Emerging players like Cetelem, ALD Automotive, and Younited Credit are gaining traction, especially in used car and digital lending segments.

Growth is fueled by multiple factors, including rising consumer preference for vehicle ownership, availability of low-interest financing for EVs, and supportive national policies such as Plan MOVES III. The increased penetration of fintech lenders offering digital, fast-track loan approvals has broadened access to credit. Additionally, urbanization and growing demand for flexible vehicle ownership models are driving the need for diverse financing options.

The market faces several challenges such as rising interest rates, stringent credit checks, and limited financing penetration in the used car segment. Traditional lenders are often cautious with self-employed and gig economy applicants, leading to credit access issues. Regulatory pressures around emissions and environmental compliance also affect vehicle selection and financing eligibility, particularly for older or diesel-powered vehicles.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0