Taiwan Cold Chain Market Outlook to 2029

By Storage and Transportation Type, By End Users (Food, Pharmaceuticals, Chemicals), By Temperature Range, By Ownership Model, and By Region

Report Overview

Report Code

TDR0192

Coverage

Asia

Published

May 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Taiwan Cold Chain Market Outlook to 2029 - By Storage and Transportation Type, By End Users (Food, Pharmaceuticals, Chemicals), By Temperature Range, By Ownership Model, and By Region” provides a comprehensive analysis of the cold chain logistics industry in Taiwan. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the Taiwan Cold Chain Market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Taiwan Cold Chain Market Outlook to 2029 - By Storage and Transportation Type, By End Users (Food, Pharmaceuticals, Chemicals), By Temperature Range, By Ownership Model, and By Region” provides a comprehensive analysis of the cold chain logistics industry in Taiwan. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the Taiwan Cold Chain Market. The report concludes with future market projections based on market revenue, by segment, service type, end-user industry, and case studies highlighting major growth enablers and key cautionary areas.

Taiwan Cold Chain Market Overview and Size

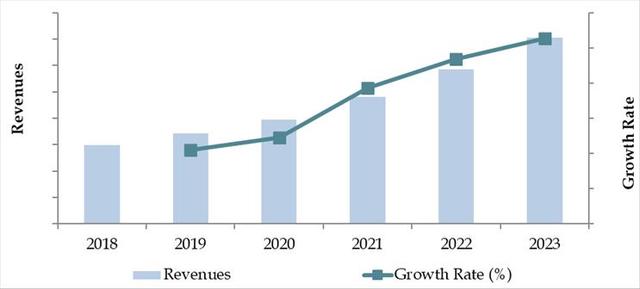

The Taiwan cold chain market reached a valuation of TWD 40 Billion in 2023, fueled by increasing demand for temperature-sensitive logistics, particularly in the food and pharmaceutical sectors. Rising consumer awareness around food safety, stringent government regulations, and the growing export market for fresh produce and biopharma products have contributed to robust market expansion. Major players operating in the space include Great Wall Cold Chain, THT Logistics, Kerry TJ Logistics, DHL Supply Chain Taiwan, and Yusen Logistics.

In 2023, Kerry TJ Logistics expanded its cold storage infrastructure in Taoyuan to support rising demand for temperature-controlled warehousing, especially for vaccine storage. The urban centers of Taipei, Kaohsiung, and Taichung are major hubs owing to high population density and proximity to port facilities and distribution centers.

Market Size for Taiwan Cold Chain Industry on the Basis of Revenues in USD Million, 2018-2024

What Factors are Leading to the Growth of Taiwan Cold Chain Market:

Rising Pharmaceutical and Biotech Exports: Taiwan's position as a major regional biotech hub has led to a surge in demand for temperature-controlled logistics. Biopharmaceutical exports grew by 11.3% in 2023, increasing the requirement for reliable cold chain services.

Shift in Food Consumption Trends: A significant increase in demand for fresh, frozen, and processed foods—particularly seafood, fruits, and meat—has led to the development of more cold storage infrastructure. E-commerce grocery sales saw a 17% YoY growth, further accelerating demand for cold chain capabilities.

Government Regulations and Food Safety Standards: Regulatory mandates such as Taiwan’s Act Governing Food Safety and Sanitation are pushing stakeholders to adopt reliable cold chain practices across the food supply chain to maintain compliance and product quality.

Which Industry Challenges Have Impacted the Growth for Taiwan Cold Chain Market

Infrastructure Bottlenecks: Limited availability of advanced temperature-controlled storage facilities and outdated transportation infrastructure continue to hinder cold chain efficiency in Taiwan. Industry estimates suggest that nearly 30% of perishable goods experience minor spoilage due to inconsistent temperature control during transportation, particularly in rural areas.

High Operational Costs: The cost of maintaining cold storage and temperature-controlled logistics is considerably high due to energy-intensive equipment and rising electricity prices. As per 2023 data, cold chain logistics costs are estimated to be 18–22% higher than standard logistics services, affecting the profitability margins for small-scale operators.

Workforce Skill Gap: A shortage of trained personnel to manage and operate cold storage systems and refrigerated logistics poses a significant operational challenge. Surveys indicate that more than 40% of logistics providers face difficulties in hiring skilled technicians, which often results in inefficient cold chain handling and higher product loss.

What are the Regulations and Initiatives which have Governed the Market:

Cold Chain Certification and Monitoring Standards: The Taiwanese government enforces stringent certification requirements for cold storage and transport service providers under the Food Safety and Sanitation Act and Pharmaceutical Affairs Law. In 2023, over 85% of certified cold chain facilities underwent regular compliance checks, ensuring quality and safety throughout the logistics process.

Temperature Monitoring Mandate for Pharmaceuticals: The Taiwan Food and Drug Administration (TFDA) requires real-time temperature tracking and GPS-enabled monitoring systems for all pharmaceutical cold chain logistics. This mandate has driven tech adoption, with nearly 60% of pharmaceutical logistics fleets upgraded with IoT-based cold monitoring by 2023.

Government Support for Green Cold Chain Solutions: Taiwan’s Ministry of Economic Affairs has introduced incentives to promote energy-efficient and eco-friendly refrigeration systems. Subsidies of up to TWD 2 million are available for retrofitting cold storage with solar-powered systems or smart temperature controls, aiming to reduce the carbon footprint of cold logistics. Adoption of green cold chain practices has grown by 13% YoY since the program's launch in 2021.

Taiwan Cold Chain Market Segmentation

By Market Structure: The organized sector is rapidly gaining traction in Taiwan's cold chain market, led by large logistics providers and 3PL companies offering integrated cold storage and transportation solutions. These firms leverage automation, digital monitoring, and compliance certifications to serve key sectors such as pharmaceuticals and processed food. The unorganized sector, comprising smaller local players, still holds a substantial share, especially in the fresh produce and seafood segments, due to their agility and hyperlocal reach, though they often face challenges in meeting standardized safety and temperature protocols.

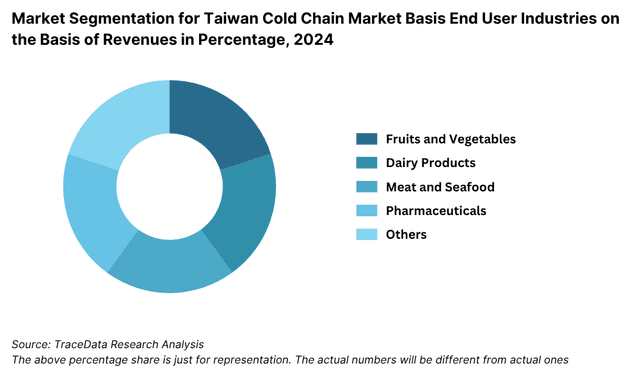

By End-Use Industry: The food and beverage industry is the dominant consumer of cold chain services in Taiwan, driven by demand from supermarkets, convenience stores, and e-commerce grocery platforms. This includes frozen foods, dairy, and fresh produce. The pharmaceutical industry represents the second-largest segment due to strict temperature control requirements for vaccines, biologics, and specialty drugs. The chemical sector, while smaller, utilizes cold logistics primarily for temperature-sensitive industrial chemicals and lab reagents.

By Temperature Range: The chilled segment (0°C to 8°C) is the largest by revenue share, catering mainly to dairy, fresh produce, and ready-to-eat meals. The frozen segment (below -18°C) follows, largely used for meat, seafood, and ice cream. An emerging segment is ultra-cold storage (below -70°C), primarily driven by demand for mRNA vaccines and specialty pharmaceuticals.

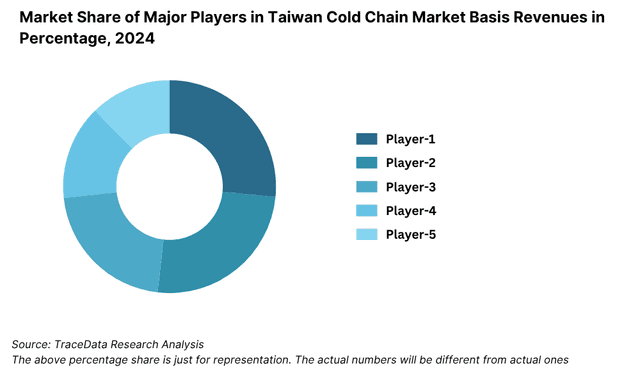

Competitive Landscape in Taiwan Cold Chain Market

The Taiwan cold chain logistics market is moderately consolidated, with a mix of established logistics firms and specialized cold chain operators. The growth of pharmaceutical cold storage demand and rising food e-commerce deliveries have also led to the emergence of digital-first and niche service providers. Major players in the market include Kerry TJ Logistics, Yamato Transport, President Transnet, Chi Mei Logistics, and Evergreen Logistics, among others.

| Company Name | Founding Year | Original Headquarters |

| President Transnet Corp. | 2000 | Taipei, Taiwan |

| Taiwan Pelican Express Co., Ltd. | 2000 | Taipei, Taiwan |

| Kerry TJ Logistics (Cold Chain Division) | 1930 (as Taiwan Jiun) | Taipei, Taiwan |

| HCT Logistics Co., Ltd. | 1938 | Taipei, Taiwan |

| Yuan Shun Logistics Co., Ltd. | 1993 | Kaohsiung, Taiwan |

| Tze Shin International Logistics | 1986 | Taichung, Taiwan |

| King Cold Logistics Co., Ltd. | 2003 | Taoyuan, Taiwan |

| Uni-President Enterprises Corp. (Cold Chain Logistics Unit) | 1967 | Tainan, Taiwan |

| DHL Supply Chain Taiwan (Cold Chain Services) | 1969 (Taiwan: ~1980s) | Bonn, Germany |

| DB Schenker Taiwan Ltd. (Cold Chain Division) | 1872 (Taiwan: ~1990s) | Essen, Germany |

| Kuehne + Nagel Taiwan (Pharma & Perishables) | 1890 (Taiwan: ~1990s) | Schindellegi, Switzerland |

| Maersk Taiwan Ltd. (Cold Chain Services) | 1904 (Taiwan: ~2000s) | Copenhagen, Denmark |

| FedEx Taiwan (Refrigerated Express) | 1971 (Taiwan: ~1990s) | Memphis, USA |

| UPS Taiwan (Temperature-sensitive logistics) | 1907 (Taiwan: ~1988) | Atlanta, USA |

| Yusen Logistics Taiwan (Cold Chain Services) | 1955 (Taiwan: ~1990s) | Tokyo, Japan |

| Nippon Express Taiwan (Refrigerated Cargo Division) | 1937 (Taiwan: ~1970s) | Tokyo, Japan |

Some of the recent competitor trends and key information about competitors include:

Kerry TJ Logistics: One of Taiwan’s leading cold chain service providers, Kerry expanded its pharmaceutical-grade cold warehouses in 2023, adding over 10,000 pallet positions across northern and central Taiwan. The company also partnered with hospitals and vaccine manufacturers to ensure end-to-end cold chain integrity.

Yamato Transport (Taiwan): Known for its temperature-controlled last-mile delivery service, Yamato introduced smart refrigerated lockers in Taipei in 2023 to cater to the booming demand for chilled grocery and meal kit deliveries. The move resulted in a 17% increase in urban cold parcel volumes.

President Transnet: A key player in food and beverage logistics, the company has recently upgraded its fleet with IoT-based temperature and humidity sensors to enhance traceability. It reported a 22% increase in cold shipments in 2023 driven by rising consumer demand for ready-to-eat meals.

Chi Mei Logistics: Specializing in cold chain for chemicals and dairy products, Chi Mei launched energy-efficient cooling systems across its southern Taiwan depots. The initiative helped cut refrigeration energy costs by 15% YoY, improving sustainability metrics and operational profitability.

Evergreen Logistics: With a strong presence in frozen seafood logistics, Evergreen invested in cross-docking facilities and reefer container solutions in 2023 to optimize supply chain flow. The company also signed a strategic agreement with a major seafood exporter, boosting its international cold chain capabilities.

What Lies Ahead for Taiwan Cold Chain Market?

The Taiwan cold chain market is expected to witness steady growth through 2029, supported by the rising demand for temperature-sensitive logistics in food, pharmaceuticals, and biotechnology. The sector is anticipated to grow at a healthy CAGR, driven by infrastructure modernization, technological adoption, and regulatory support for quality assurance in cold chain handling.

Expansion of Pharmaceutical and Biotech Cold Storage Needs: With Taiwan emerging as a key player in regional pharmaceutical production and clinical research, the demand for ultra-cold and precision-controlled storage is expected to grow significantly. This includes increasing storage needs for biologics, vaccines, and mRNA-based therapies, pushing logistics providers to upgrade their capabilities.

Rise of E-Grocery and Meal Kit Deliveries: As consumer behavior shifts towards online grocery shopping and ready-to-cook meal kits, the demand for last-mile chilled and frozen logistics is projected to rise. By 2029, the e-grocery segment alone is expected to account for over 25% of cold chain delivery volumes in urban Taiwan.

Adoption of IoT and Real-Time Monitoring: The market is expected to see increased deployment of IoT-based solutions for real-time temperature and humidity tracking. These systems will improve traceability, minimize spoilage, and ensure regulatory compliance, particularly for pharmaceutical and high-value food logistics.

Government Push for Sustainable Cold Chain Infrastructure: Taiwan’s Ministry of Economic Affairs is expected to continue offering incentives for energy-efficient cold storage units and eco-friendly refrigerants. Green cold chain practices, such as solar-powered warehouses and electric refrigerated transport, will become increasingly important, helping companies meet ESG targets and reduce operational costs.

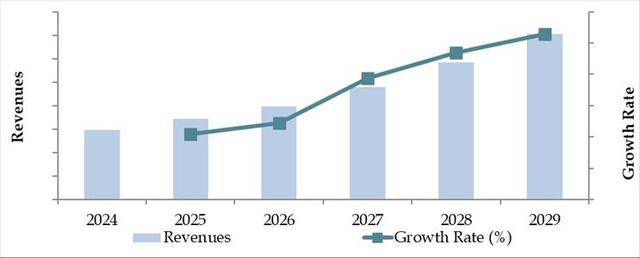

Future Outlook and Projections for Taiwan Cold Chain Market on the Basis of Revenues in USD Million, 2024-2029

Taiwan Cold Chain Market Segmentation

By Market Structure:

Organized Logistics Providers

Third-Party Logistics (3PL) Cold Chain Operators

Captive In-house Cold Chain Facilities

Local Refrigerated Transporters

Temperature-Controlled Warehousing Companies

Urban Last-Mile Cold Chain Delivery Firms

By End-Use Industry:

Food & Beverage (Frozen Foods, Dairy, Seafood, Fresh Produce)

Pharmaceuticals (Vaccines, Biologics, Clinical Trial Samples)

Chemicals (Temperature-Sensitive Lab Chemicals, Reagents)

E-Commerce Grocery Platforms

Food Service & Meal Kit Providers

By Temperature Range:

Chilled (0°C to 8°C)

Frozen (Below -18°C)

Ultra-Cold (Below -70°C)

Ambient-Controlled (15°C to 25°C)

By Ownership Model:

Third-Party Operated

Captive (Owned by Food/Pharma Companies)

Hybrid (Collaborative Logistics Networks)

By Region:

Northern Taiwan (Taipei, New Taipei, Keelung)

Central Taiwan (Taichung, Changhua)

Southern Taiwan (Kaohsiung, Tainan, Pingtung)

Eastern Taiwan (Hualien, Taitung)

Offshore Islands (Kinmen, Penghu)

Players Mentioned in the Report:

- Taiwan Cold Chain Logistics Company (TCCLC)

- Yusen Logistics Taiwan

- UPS Healthcare Taiwan

- DHL Taiwan

- YES Logistics

- Kerry TJ Logistics

- CTW Logistics

- Choice E-Logistics

- Logistic Republic

- MENQ Logistics

- HCT Logistics

- Centurion Logistics Services

- Transworld Express

- Best Logistics Taiwan

- Omni Logistics Taiwan

- GEODIS Taiwan

- Maersk Taiwan

- Dimerco Express Group

- SunFresh Cold Chain Logistics

- Gallant Ocean Group

Key Target Audience:

Cold Chain Logistics Companies

Food Manufacturing & Processing Firms

Pharmaceutical and Biotech Companies

Government and Regulatory Bodies (e.g., TFDA, Ministry of Economic Affairs)

Technology Solution Providers (IoT, Cold Monitoring Systems)

Warehousing & Transport Infrastructure Investors

Market Research and Consulting Firms

Time Period:

Historical Period: 2018–2023

Base Year: 2024

Forecast Period: 2024–2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

6.1. Revenues, 2018-2024P

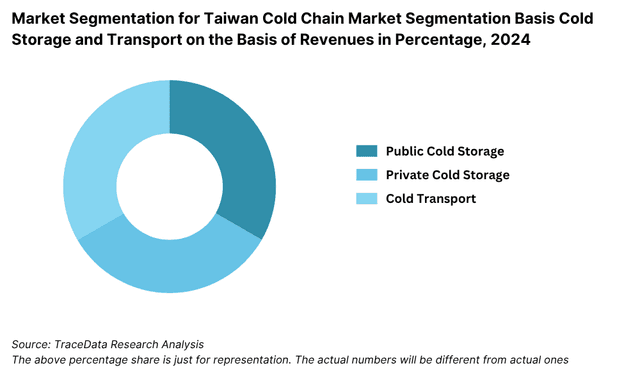

7.1. By Cold Storage and Cold Transport, 2023-2024P

7.2. By End-User Application (Dairy Products, Meat and Seafood, Pharmaceuticals, Fruits and Vegetables and Others), 2023-2024P

7.3. By Ownership (Owned and 3PL Cold Chain Facilities), 2023-2024P

10.1. Taiwan Cold Storage Market Size

10.1.1. By Revenue, 2018-2024P

10.1.2. By Number of Pallets, 2018-2024P

10.2. Taiwan Cold Storage Market Segmentation

10.2.1. By Temperature Range (Ambient, Chilled and Frozen), 2023-2024P

10.2.2. By End-User Application (Dairy Products, Meat and Seafood, Pharmaceuticals, Fruits and Vegetables and Others), 2023-2024P

10.2.3. By Major Cities (Manila, Quezon, Cebu and others), 2023-2024P

10.3. Taiwan Cold Storage Market Future Outlook and Projections, 2025-2029

10.3.1. By Temperature Range (Ambient, Chilled and Frozen), 2025-2029

11.1. Taiwan Cold Transport Market Size (By Revenue and Number of Reefer Trucks), 2018-2024P

11.2. Taiwan Cold Transport Market Segmentation

11.2.1. By Mode of Transportation (Land, Sea and Air), 2023-2024P

11.2.2. By Location (Domestic and International), 2023-2024P

11.3. Taiwan Cold Transport Market Future Outlook and Projections, 2025-2029

11.3.1. By Mode of Transport (Land, Sea and Air), 2025-2029

11.3.2. By Location (Domestic and International), 2025-2029

12.1. Trends and Developments in Taiwan Cold Chain Market

12.2. Issues and Challenges in Taiwan Cold Chain Market

12.3. Decision Making Parameters for End Users in Taiwan Cold Chain Market

12.4. SWOT Analysis of Taiwan Cold Chain Industry

12.5. Government Regulations and Associations in Taiwan Cold Chain Market

12.6. Macroeconomic Factors Impacting Taiwan Cold Chain Market

13.1. Parameters to be covered for Each End Users to Determine Business Potential:

13.1.1. Production Clusters

13.1.2. Market Demand, Major Products Stored, Cold Storage Companies in Guwahati catering to End Users

13.1.3. Location Preference for Each End User and their Production Plants, Preferences for Outsourcing and Captive Facility, Services Required, Facility Preferences, Decision Making Parameters

13.1.4. Cross comparison of leading end users/companies based on Headquarters, Manufacturing Plants, Products Stored, Major Products, Total Production, Cold Chain Partner, Facility Outsourced/Captive, Pallets Owned/Hired, Contact Person, Address and others

16.1. Competitive Landscape in Taiwan Cold Chain Market

16.2. Competition Scenario in Taiwan Cold Chain Market (Competition Stage, Major Players, Competing Parameters)

16.3. Key Metrics (Temperature Range, Pallet Position, Prices Charged, Occupancy Rate, Revenue (2023) and Employee Base) for Major Players in Taiwan Cold Chain Market

16.4. Company Profiles of Major Companies in Taiwan Cold Chain Market (Year of Establishment, Company Overview, Service Offered, USP, Warehousing Facilities, Warehousing Price, Cold Storage by location, Occupancy Rate, Major Clientele, Industries Catered, Employee Base, Temperature Range, Topline OPEX*, Revenue, Recent Developments, Future Strategies)

16.5. Strength and Weakness

16.6. Operating Model Analysis Framework

16.7. Gartner Magic Quadrant

16.8. Bowmans Strategic Clock for Competitive Advantage

17.1. Revenues, 2025-2029

18.1. By Cold Storage and Cold Transport, 2025-2029

18.2. By End-User Application (Dairy Products, Meat and Seafood, Pharmaceuticals, Fruits and Vegetables and Others), 2025-2029

18.3. By Ownership (Owned and 3PL Cold Chain Facilities), 2025-2029

18.4. Recommendation

18.5. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities for the Taiwan Cold Chain Market. Based on this ecosystem, we shortlist leading 5–6 companies in the country, considering factors such as operational capacity (cold storage space, fleet size), service coverage (regions and industries served), and financial information.

Sourcing is conducted through industry reports, government bulletins, and multiple secondary and proprietary databases to perform desk research and collate industry-level intelligence.

Step 2: Desk Research

We subsequently engage in an exhaustive desk research process, referencing a wide range of proprietary and public data sources. This enables a comprehensive market analysis, covering sales revenues, number of logistics players, temperature-controlled warehousing capacity, technology adoption, and demand-side segmentation.

This is supplemented with company-level data reviews using press releases, annual filings, investor presentations, and cold chain audit reports. This process helps establish a detailed understanding of the market dynamics, investment trends, and supply chain infrastructure.

Step 3: Primary Research

We initiate a series of in-depth interviews with C-level executives and operational heads of logistics providers, warehousing firms, pharmaceutical companies, food producers, and regulatory bodies in the Taiwan Cold Chain Market. The objective is to validate secondary findings, quantify market volumes, and understand operational best practices, pricing, and process flows.

As part of our validation methodology, disguised interviews are conducted by approaching companies as potential clients. This dual-source validation helps cross-check company statements with field insights and ensures data accuracy regarding storage capacity, throughput, service models, and client engagement strategies.

Step 4: Sanity Check

- A comprehensive bottom-up and top-down triangulation approach is deployed to validate total market size and segment-wise estimates. This includes modeling based on cold storage capacity utilization, volume of goods moved under temperature-controlled conditions, and average revenue per unit, ensuring robust and reliable outputs.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Taiwan Cold Chain Market is poised for robust expansion, projected to surpass TWD 60 Billion by 2029. This growth is driven by increasing demand from the pharmaceutical and processed food sectors, a rise in e-grocery adoption, and heightened regulatory focus on temperature-controlled logistics. Technological advancements and government incentives for cold chain modernization further strengthen the market's long-term potential.

Key players in the Taiwan Cold Chain Market include Kerry TJ Logistics, Yamato Transport (Taiwan), President Transnet, Chi Mei Logistics, and Evergreen Logistics. These companies dominate the market with their nationwide cold storage networks, temperature-controlled fleets, and integrated service offerings across food and pharma supply chains.

Primary growth drivers include the increasing demand for pharmaceutical cold storage, growing popularity of e-commerce grocery platforms, and the expansion of Taiwan’s food processing and export industry. Additionally, the adoption of IoT-enabled monitoring systems and support for green cold chain infrastructure through government subsidies are catalyzing market development.

The market faces several challenges, including high operational costs due to energy consumption, limited cold storage capacity in rural and offshore regions, and a shortage of skilled labor for cold chain management. Regulatory compliance for temperature-sensitive goods and the need for infrastructure upgrades also pose significant hurdles for smaller and mid-tier players.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0