UAE Auto Finance Market Outlook to 2029

By Loan Type, By Vehicle Type, By Lender Type, By Tenure Period, By Interest Rate, and By Region

Report Overview

Report Code

TDR0133

Coverage

Middle East

Published

April 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “UAE Auto Finance Market Outlook to 2029 - By Loan Type, By Vehicle Type, By Lender Type, By Tenure Period, By Interest Rate, and By Region” provides a comprehensive analysis of the auto finance market in the UAE. The report covers an overview and genesis of the industry, overall market size in terms of loan disbursement, market segmentation; trends and developments, regulatory landscape, customer profiling, issues and challenges, and competitive landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the auto finance market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “UAE Auto Finance Market Outlook to 2029 - By Loan Type, By Vehicle Type, By Lender Type, By Tenure Period, By Interest Rate, and By Region” provides a comprehensive analysis of the auto finance market in the UAE. The report covers an overview and genesis of the industry, overall market size in terms of loan disbursement, market segmentation; trends and developments, regulatory landscape, customer profiling, issues and challenges, and competitive landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the auto finance market. The report concludes with future market projections based on loan disbursement, by lender type, vehicle type, interest rate, region, and success case studies highlighting the major opportunities and cautions.

The UAE auto finance industry is an essential pillar supporting the broader automotive sector in the region. Given the rising urbanization, increasing disposable incomes, and government-backed economic diversification strategies, the auto finance market has witnessed substantial growth over the past decade. Financial institutions, ranging from traditional banks to fintech-based lending platforms, have played a crucial role in enabling vehicle purchases for both UAE nationals and expatriates. This report highlights the intricacies of the market, providing valuable insights into its evolution, recent developments, and anticipated future trends.

UAE Auto Finance Market Overview and Size

The UAE auto finance market reached a valuation of AED 55 Billion in 2023, driven by increasing demand for vehicle ownership, favorable financing options, and a growing expatriate population. The market is characterized by major players such as Emirates NBD, ADCB, Abu Dhabi Islamic Bank, Dubai Islamic Bank, and HSBC. These financial institutions are recognized for their extensive loan offerings, competitive interest rates, and digital financing solutions.

The rising demand for auto loans in the UAE can be attributed to a variety of factors, including the increasing influx of expatriates seeking financial assistance to purchase vehicles, a strong economic foundation, and the government’s support for digital financial transformation. The automotive sector has remained resilient, even amid economic fluctuations, as banks and financial institutions continue to introduce customer-centric financing products. In 2023, Emirates NBD introduced a digital auto loan approval platform to enhance customer convenience and streamline the application process. This initiative aims to tap into the growing fintech adoption in the UAE and provide a seamless financing experience. Dubai and Abu Dhabi remain the key markets due to their high population density and strong automotive sales.

Market Size for UAE Auto Finance Industry on the Basis of Loan Disbursement on the Basis of USD Billion, 2018-2023

What Factors are Leading to the Growth of UAE Auto Finance Market

Economic Stability: The UAE's strong economic position and steady GDP growth have positively influenced consumer purchasing power, increasing the demand for vehicle financing. Auto loans accounted for approximately 60% of total vehicle purchases in the country in 2023. The nation’s well-developed financial system and banking infrastructure provide a conducive environment for auto financing to thrive.

Rising Vehicle Ownership Among Expatriates: With expatriates comprising around 88% of the total population, the demand for auto loans has surged as banks and financial institutions offer flexible financing solutions tailored to non-residents. This demographic shift has led financial institutions to design specialized lending products that cater to the unique financial situations of expatriates, allowing them easier access to vehicle financing.

Digitalization in Banking Services: Online loan applications and AI-driven credit scoring have transformed the auto finance sector, making loan approvals quicker and more transparent. In 2023, approximately 45% of auto loan applications were processed digitally. The use of machine learning and automated verification processes has significantly reduced the turnaround time for loan approvals, thereby increasing efficiency and accessibility for consumers.

Which Industry Challenges Have Impacted the Growth for UAE Auto Finance Market

High Interest Rates for Non-Residents: Expatriates often face higher interest rates and stricter lending criteria, making it challenging for them to access affordable auto financing options. In 2023, interest rates for non-residents ranged between 3.5% and 6%, compared to 2.5% for UAE nationals. This disparity in rates has led to financial burdens for expatriates and has pushed many towards alternative financing solutions.

Stringent Credit Approval Processes: The Central Bank of the UAE enforces strict credit assessment policies, resulting in high rejection rates, particularly among low-income applicants and those with limited credit history. Many financial institutions require extensive documentation and proof of income, making it difficult for some individuals to qualify for loans.

Impact of Islamic Banking Regulations: Sharia-compliant financing options, while growing in popularity, sometimes involve complex contract structures, leading to extended processing times and higher costs. Islamic banks adhere to principles that prohibit interest-based transactions, which often results in alternative financing models that may not always align with conventional loan structures.

What are the Regulations and Initiatives which have Governed the Market

Central Bank Regulations on Auto Loans: The UAE Central Bank mandates a maximum loan-to-value (LTV) ratio of 80% for auto financing, ensuring financial stability and reducing credit risk. Borrowers must provide a 20% down payment upfront. This regulation aims to safeguard both financial institutions and borrowers by preventing excessive debt accumulation.

Credit Scoring and Debt Burden Ratio (DBR) Requirements: Borrowers must adhere to the Central Bank's 50% DBR rule, meaning monthly debt repayments, including auto loans, cannot exceed 50% of their monthly income. This policy is designed to encourage responsible borrowing and prevent financial distress among consumers.

Government Push for Green Vehicle Financing: To encourage the adoption of electric vehicles (EVs), the UAE government, along with major banks, has introduced low-interest financing schemes for EV purchases. In 2023, EV loans accounted for approximately 8% of total auto finance disbursements, a number expected to grow significantly by 2029. With global emphasis on sustainability, financial institutions are aligning their lending practices with environmentally friendly initiatives to promote cleaner transportation solutions.

Market Segmentation for UAE Auto Finance Market

By Loan Type: Auto finance in the UAE is segmented into conventional loans and Islamic financing. Conventional loans dominate the market due to their flexible repayment options and competitive interest rates. However, Islamic auto financing is gaining traction, accounting for approximately 30% of total auto loan disbursements in 2023, as consumers seek Sharia-compliant options. The increasing demand for ethical banking solutions is expected to further drive the growth of Islamic financing in the coming years.

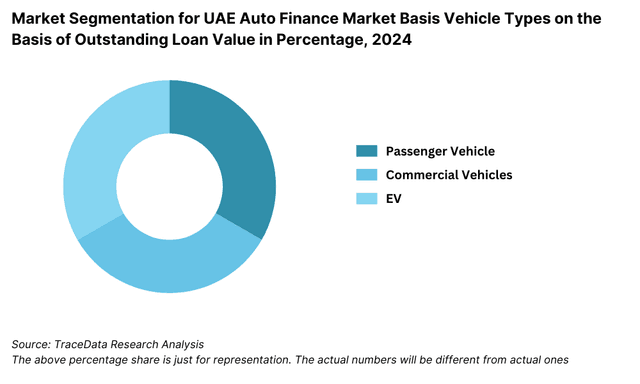

By Vehicle Type: New car financing accounts for around 70% of the total auto finance market in 2023, driven by consumer preference for the latest models and technological advancements. Used car financing makes up the remaining 30%, fueled by affordability and depreciation-conscious buyers. With rising costs of new vehicles, used car financing is expected to witness a surge in demand, particularly among budget-conscious consumers.

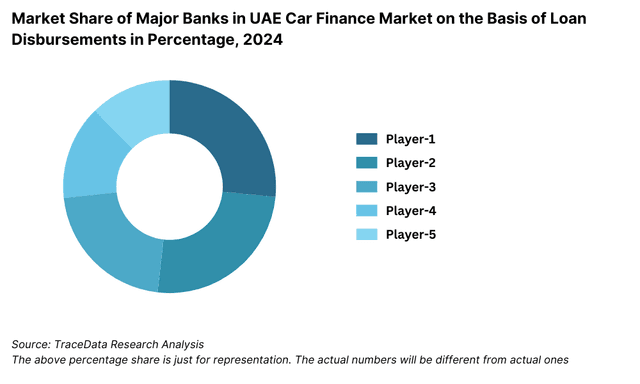

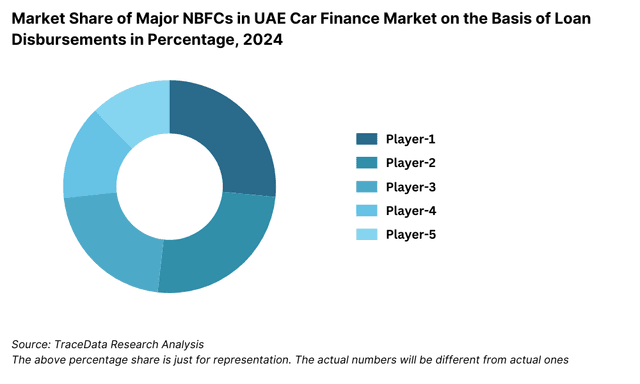

By Lender Type: Banks are the predominant auto finance providers, covering approximately 75% of total loans disbursed in 2023, while non-banking financial institutions (NBFIs) and fintech companies account for the remaining 25%. Fintech-based lenders have grown by 18% year-over-year, leveraging digital platforms to attract customers. The digitalization of lending processes has significantly reduced approval times and improved customer experience, making fintech lenders an increasingly popular choice.

.png&w=640&q=75)

Competitive Landscape in UAE Auto Finance Market

The UAE auto finance market remains highly competitive, with numerous banks and financial institutions providing customized financing solutions. Major players, including Emirates NBD, ADCB, ADIB, Dubai Islamic Bank, and HSBC, dominate the sector by offering attractive interest rates, digital lending services, and innovative financial products tailored to meet the needs of both residents and expatriates.

Name | Founding Year | Original Headquarters |

|---|---|---|

Emirates NBD Auto Loan | 1963 | Dubai, UAE |

Abu Dhabi Commercial Bank (ADCB) Auto Finance | 1985 | Abu Dhabi, UAE |

First Abu Dhabi Bank (FAB) Auto Loan | 2017 | Abu Dhabi, UAE |

Dubai Islamic Bank (DIB) Auto Finance | 1975 | Dubai, UAE |

Mashreq Bank Auto Loan | 1967 | Dubai, UAE |

RAKBANK Auto Finance | 1976 | Ras Al Khaimah, UAE |

Al Hilal Bank Auto Loan | 2008 | Abu Dhabi, UAE |

Noor Bank Auto Finance | 2008 (Merged with DIB) | Dubai, UAE |

HSBC UAE Auto Finance | 1946 | London, UK |

Al-Futtaim Finance Auto Loan | 1985 | Dubai, UAE |

Toyota Financial Services UAE | 1982 | Toyota City, Japan |

Al Jaziri Motors Finance | 1994 | Dubai, UAE |

Al Wifaq Finance | 2006 | Abu Dhabi, UAE |

Some of the recent competitor trends and key information about market players include:

Emirates NBD: A leading financial institution in the UAE, Emirates NBD reported a 12% increase in auto loan disbursements in 2023, driven by their digital lending solutions and partnerships with car dealerships. The bank's innovative approach in digital banking has significantly enhanced the loan application process.

ADCB: Abu Dhabi Commercial Bank has expanded its auto financing segment by offering competitive interest rates and quick approval processes. In 2023, they saw a 9% rise in financed vehicle sales. Their customer-centric approach and personalized loan offerings have strengthened their market position.

ADIB: Abu Dhabi Islamic Bank leads in Sharia-compliant auto financing, with a 20% market share in Islamic car loans. Their Murabaha-based financing model continues to attract customers seeking halal financing options. The bank's continued investment in digital Islamic banking solutions has fueled further growth.

Dubai Islamic Bank: A pioneer in Islamic auto financing, DIB recorded a 15% increase in auto loan applications in 2023, emphasizing its digital platforms and enhanced customer service. The bank has introduced AI-driven loan assessment tools, further improving loan processing efficiency.

HSBC UAE: HSBC remains a significant player in the expatriate auto finance market, focusing on flexible repayment terms and international customer services. Their competitive loan packages tailored for expatriates have contributed to sustained growth in loan disbursements.

What Lies Ahead for UAE Auto Finance Market?

The UAE auto finance market is projected to witness steady growth by 2029, exhibiting a healthy CAGR during the forecast period. This growth is expected to be driven by increasing vehicle ownership, favorable economic conditions, and enhanced digital finance solutions.

Rise of Electric Vehicle Financing: As the UAE government accelerates its push for sustainable mobility through incentives and policies, the demand for electric vehicle (EV) financing is set to grow. Banks and financial institutions are likely to introduce specialized loan products with lower interest rates and extended repayment periods to encourage EV adoption.

Digital Transformation of Financing Services: The adoption of AI, big data analytics, and digital lending platforms is anticipated to revolutionize the auto finance sector. These technologies will enhance credit assessments, reduce approval times, and provide a seamless customer experience.

Focus on Green Financing: With sustainability at the core of UAE’s Vision 2050, banks and financial institutions are expected to roll out green financing initiatives. These will include preferential interest rates and flexible repayment options for environmentally friendly vehicles, appealing to eco-conscious buyers.

Expansion of Fintech Influence: The rise of fintech firms in the UAE’s auto finance market is set to increase competition and innovation. Digital platforms offering quick loan approvals, flexible repayment options, and transparent financial solutions are likely to gain traction, particularly among the region’s younger and digitally savvy consumers

UAE Auto Finance Market Segmentation

- By Loan Type:

- Conventional Loans

- Islamic Financing

- By Vehicle Type:

- New Car Financing

- Used Car Financing

- By Lender Type:

- Banks

- Non-Banking Financial Institutions (NBFIs)

- Fintech Lenders

- By Tenure Period:

- 1-2 Years

- 3-5 Years

- More than 5 Years

- By Interest Rate:

- 2.5% - 4.5% (Conventional Loans)

- 3% - 5% (Islamic Financing)

Players Mentioned in the Report (Banks):

- Emirates NBD

- Dubai Islamic Bank

- First Abu Dhabi Bank (FAB)

- Abu Dhabi Commercial Bank (ADCB)

- Emirates Islamic

- United Arab Bank

- Ajman Bank

- Bank of Baroda UAE

- Mashreqbank

- National Bank of Fujairah (NBF)

- Commercial Bank of Dubai

- RAKBANK

- HSBC UAE

- Arab Bank

- Sharjah Islamic Bank

Players Mentioned in the Report (NBFCs):

- Deem Finance

- Al Futtaim Finance

- Aafaq Islamic Finance

- Mawarid Finance

- Blue Light Automobile Services LLC

- Gulwani Commercial Brokers LLC

- Osool

- Al Wifaq Finance Company

- Al Hilal Auto

- Finance House

- Noor Takaful

- Al Etihad Credit Bureau

Players Mentioned in the Report (Captive):

- Al-Futtaim Finance (Toyota, Lexus, Honda)

- Al Tayer Motors Finance (Ford, Lincoln, Jaguar, Land Rover)

- Gargash Enterprises Finance (Mercedes-Benz)

- Nissan Finance (Arabian Automobiles)

- BMW Financial Services (AGMC)

- Audi Finance (Al Nabooda Automobiles)

- Volkswagen Finance (Al Nabooda Automobiles)

Key Target Audience:

- Banks and Financial Institutions

- Auto Loan Borrowers

- Automotive Dealers and Showrooms

- Fintech and Digital Lending Platforms

- Regulatory Bodies (e.g., UAE Central Bank)

- Research and Development Institutions

Time Period:

- Historical Period: 2018-2023

- Base Year: 2024

- Forecast Period: 2024-2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-Role of Entities, Stakeholders, and challenges they face.

4.2. Relationship and Engagement Model between Banks-Dealers, NBFCs-Dealers and Captive-Dealers-Commission Sharing Model, Flat Fee Model and Revenue streams

4.3. Supply Decision-Making Process

5.1. New Car and Used Car Sales in UAE by type of vehicle, 2018-2024

8.1. Credit Disbursed, 2018-2024

8.2. Outstanding Loan, 2018-2024

9.1. By Market Structure (Bank-Owned, Multi-Finance, and Captive Companies), 2023-2024P

9.2. By Financing Options (Traditional Loans, Leasing, Multi-Finance Loans), 2023-2024P

9.3. By Region, 2023-2024P

9.4. By Type of Vehicle (New, Used, Electric), 2023-2024P

9.5. By Average Loan Tenure (0-2 years, 3-5 years, 6-8 years, above 8 years), 2023-2024P

9.6. By Loan Type (Conventional vs. Islamic), 2023-2024P

10.1. Customer Landscape and Cohort Analysis

10.2. Customer Journey and Decision-Making

10.3. Need, Desire, and Pain Point Analysis

10.4. Gap Analysis Framework

11.1. Trends and Developments for UAE Car Finance Market

11.2. Growth Drivers for UAE Car Finance Market

11.3. SWOT Analysis for UAE Car Finance Market

11.4. Issues and Challenges for UAE Car Finance Market

11.5. Government Regulations for UAE Car Finance Market

12.1. Market Size and Future Potential for Online Car Financing Aggregators, 2018-2029

12.2. Business Model and Revenue Streams

12.3. Cross Comparison of Leading Digital Car Finance Companies Based on Company Overview, Revenue Streams, Loan Disbursements/Number of Leads Generated, Operating Cities, Number of Branches, and Other Variables

13.1. Finance Penetration Rate and Average Down Payment for New and Used Cars, 2018-2029

13.2. How Finance Penetration Rates are Changing Over the Years with Reasons

13.3. Type of Car Segment for which Finance Penetration is Higher

17.1. Market Share of Key Banks in UAE Car Finance Market, 2024

17.2. Market Share of Key NBFCs in UAE Car Finance Market, 2024

17.3. Market Share of Key Captive in UAE Car Finance Market, 2024

17.4. Benchmark of Key Competitors in UAE Car Finance Market, including Variables such as Company Overview, USP, Business Strategies, Strengths, Weaknesses, Business Model, Number of Branches, Product Features, Interest Rate, NPA, Loan Disbursed, Outstanding Loans, Tie-Ups and others

17.5. Strengths and Weaknesses

17.6. Operating Model Analysis Framework

17.7. Gartner Magic Quadrant

17.8. Bowmans Strategic Clock for Competitive Advantage

18.1. Credit Disbursed, 2025-2029

18.2. Outstanding Loan, 2025-2029

19.1. By Market Structure (Bank-Owned, Multi-Finance, and Captive Companies), 2025-2029

19.2. By Financing Options (Traditional Loans, Leasing, Multi-Finance Loans), 2025-2029

19.3. By Region, 2025-2029

19.4. By Type of Vehicle (New, Used, Electric), 2025-2029

19.5. By Average Loan Tenure (0-2 years, 3-5 years, 6-8 years, Above 8 years), 2025-2029

19.6. Recommendation

19.7. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities for the UAE Auto Finance Market. Basis this ecosystem, we will shortlist leading 5-6 financial institutions in the country based upon their financial information, loan disbursement volume, and market share.

Sourcing is made through industry articles, multiple secondary, and proprietary databases to perform desk research around the market to collate industry-level information.

Step 2: Desk Research

Subsequently, we engage in an exhaustive desk research process by referencing diverse secondary and proprietary databases. This approach enables us to conduct a thorough analysis of the market, aggregating industry-level insights. We delve into aspects like total loan disbursements, number of market players, interest rate trends, borrower demand, and other variables. We supplement this with detailed examinations of company-level data, relying on sources like press releases, annual reports, financial statements, and similar documents. This process aims to construct a foundational understanding of both the market and the entities operating within it.

Step 3: Primary Research

We initiate a series of in-depth interviews with C-level executives and other stakeholders representing various UAE Auto Finance Market players and end-users. This interview process serves a multi-faceted purpose: to validate market hypotheses, authenticate statistical data, and extract valuable operational and financial insights from these industry representatives. Bottom-to-top approach is undertaken to evaluate loan disbursement volumes for each player, thereby aggregating to the overall market.

As part of our validation strategy, our team executes disguised interviews wherein we approach each financial institution under the guise of potential customers. This approach enables us to validate the operational and financial information shared by company executives, corroborating this data against what is available in secondary databases. These interactions also provide us with a comprehensive understanding of revenue streams, value chain, process, pricing, and other factors.

Step 4: Sanity Check

- Bottom-to-top and top-to-bottom analysis along with market size modeling exercises is undertaken to assess the sanity check process.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The UAE auto finance market is expected to continue growing, driven by increasing vehicle ownership rates, favorable financing options, and digital innovations. In 2023, the market size reached AED 55 billion, with steady growth projections for the coming years.

Major players in the market include Emirates NBD, ADCB, ADIB, Dubai Islamic Bank, and HSBC UAE. These institutions provide a wide range of auto loan products, leveraging technology and strategic partnerships to expand their market presence.

Key growth factors include strong economic conditions, rising disposable incomes, an increasing expatriate population, and government initiatives promoting digital financial solutions. Additionally, Islamic financing is gaining traction as more consumers seek Sharia-compliant lending options.

Challenges include high interest rates for non-residents, stringent loan approval criteria, and regulatory compliance requirements. Additionally, the increasing competition from fintech lenders and evolving digital financing trends may reshape the traditional lending landscape.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0