Uganda Auto Finance Market Outlook to 2029

By Market Structure, By Lender Type, By Vehicle Type, By Financing Tenure, By Customer Profile, and By Region

Report Overview

Report Code

TDR0158

Coverage

Africa

Published

April 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Uganda Auto Finance Market Outlook to 2029 – By Market Structure, By Lender Type, By Vehicle Type, By Financing Tenure, By Customer Profile, and By Region” provides a comprehensive analysis of the auto finance industry in Uganda. The report covers an overview and genesis of the industry, market size in terms of disbursed loans and number of financed vehicles, detailed segmentation, emerging trends and developments, regulatory framework, customer persona analysis, operational challenges, competitive landscape including profiling of key financial institutions, as well as success stories and potential growth barriers.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Uganda Auto Finance Market Outlook to 2029 – By Market Structure, By Lender Type, By Vehicle Type, By Financing Tenure, By Customer Profile, and By Region” provides a comprehensive analysis of the auto finance industry in Uganda. The report covers an overview and genesis of the industry, market size in terms of disbursed loans and number of financed vehicles, detailed segmentation, emerging trends and developments, regulatory framework, customer persona analysis, operational challenges, competitive landscape including profiling of key financial institutions, as well as success stories and potential growth barriers. The report concludes with future projections, forecasting the evolution of the market through 2029, using cause-effect relationships and growth case studies to highlight opportunities and pitfalls.

Uganda Auto Finance Market Overview and Size

The Uganda auto finance market was valued at approximately UGX 2.3 trillion (~USD 600 million) in 2023, driven by the rising demand for personal mobility, limited public transport infrastructure, and increasing availability of used imported vehicles. Kampala remains the dominant market, accounting for over 45% of the total auto loan disbursement due to its high vehicle penetration, urban density, and access to formal credit infrastructure.

Key players in the market include Stanbic Bank, Centenary Bank, DFCU Bank, AutoSure Africa, and Tugende, among others. These institutions offer vehicle financing solutions for both new and used cars, with tenures ranging between 12 to 60 months. A growing number of fintech-enabled lenders and informal microfinance institutions are also entering the space, particularly in peri-urban and upcountry areas.

In 2023, Tugende expanded its vehicle leasing product line to include boda-boda taxis and small commercial vans, responding to the demand from informal sector entrepreneurs who lack access to traditional bank loans.

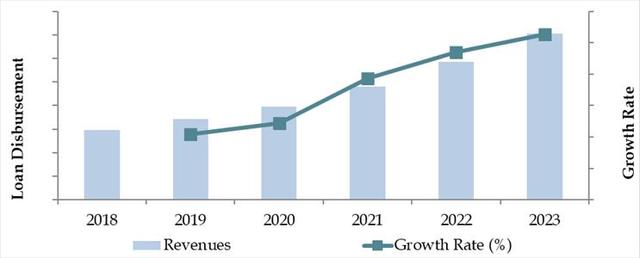

Market Size for Uganda Auto Finance Industry on the Basis of Credit Disbursed in KES Billion, 2018-2023

What Factors are Leading to the Growth of Uganda Auto Finance Market:

Informal Sector-led Demand: A significant portion of vehicle purchases in Uganda, especially boda-bodas and commercial vans, are driven by informal sector workers. As of 2023, over 60% of auto loans originated from microfinance institutions and non-bank financial companies catering to gig economy workers and micro-entrepreneurs. These segments rely heavily on vehicle ownership for income generation.

Import-led Vehicle Market: More than 85% of the vehicles sold in Uganda are used imports from Japan, UAE, and the UK. These vehicles are relatively affordable, and financial institutions have developed specialized loan products to target buyers of used imported vehicles with flexible collateral terms.

Urbanization and Mobility Shifts: Uganda’s urban population has grown at an annual rate of 4.5%, intensifying the demand for personal transportation. This has led to a noticeable uptick in vehicle purchases, particularly in rapidly growing municipalities such as Wakiso, Mukono, and Mbarara, where auto loan penetration has been on the rise.

Which Industry Challenges Have Impacted the Growth for Uganda Auto Finance Market

High Interest Rates and Inflation Pressures: Uganda's auto finance sector has been adversely affected by persistently high interest rates. In 2023, average vehicle loan interest rates ranged between 18%–24%, making vehicle ownership costly for the average consumer. With inflation averaging 8.2% during the year, rising household costs have further squeezed disposable incomes, delaying or reducing loan uptake. Approximately 35% of potential borrowers reported postponing auto loan decisions due to affordability concerns.

Limited Credit History and Informal Economy Dependence: A significant proportion of Uganda’s working population operates in the informal economy, which complicates credit assessments. Over 60% of borrowers in the auto finance sector lack formal income documentation or credit scores, restricting access to financing from traditional banks. This has forced many to rely on non-bank microfinance institutions, which often charge higher fees or require stringent collateral.

Vehicle Quality and Depreciation Risk: Most vehicles financed in Uganda are second-hand imports, typically over 8 years old. As a result, financiers face increased asset risk due to faster depreciation, mechanical failures, and limited resale value. In 2023, over 40% of repossessed vehicles had resale values lower than outstanding loan balances, impacting lender recovery rates and profitability.

What are the Regulations and Initiatives which have Governed the Market:

Minimum Capital and Prudential Guidelines by Bank of Uganda (BoU): All financial institutions engaged in auto lending must comply with capital adequacy and prudential lending guidelines as per the Financial Institutions Act, 2004 (amended 2016). These include strict loan provisioning requirements and loan-to-value ratio ceilings, impacting lending terms and risk appetite.

Import Age Restrictions and Roadworthiness Inspections: Uganda enforces age restrictions on vehicle imports, capping gasoline vehicles at 15 years and diesel vehicles at 10 years. Additionally, all vehicles must pass Uganda National Bureau of Standards (UNBS) inspections before registration. In 2023, over 12,000 vehicles were denied import clearance due to failure in meeting these compliance requirements.

Credit Reference Bureau (CRB) Expansion: The Bank of Uganda has mandated all lenders to report to licensed CRBs. In 2023, the CRB coverage in Uganda expanded to 60% of formal borrowers, aiding lenders in more accurate risk profiling. However, inclusion of informal sector borrowers remains low, limiting the impact in auto finance penetration.

Uganda Auto Finance Market Segmentation

By Market Structure: The auto finance market in Uganda is largely dominated by informal and semi-formal lenders, including SACCOs (Savings and Credit Cooperative Organizations), microfinance institutions (MFIs), and asset-financing companies like Tugende and Asaak. These players cater primarily to low-income and informal sector workers by offering flexible repayment terms and minimal documentation. In contrast, formal financial institutions such as Stanbic Bank, Centenary Bank, and DFCU Bank hold a relatively smaller share, focused mainly on salaried individuals and formal SMEs. Their stricter underwriting processes and collateral requirements limit reach to broader segments.

By Lender Type: Commercial Banks dominate the formal segment by offering vehicle loans primarily to salaried professionals and SMEs. These institutions provide competitive interest rates but require higher documentation and collateral. Non-Banking Financial Institutions (NBFIs) such as microfinance deposit-taking institutions (MDIs) and leasing firms cater to borrowers underserved by banks. These lenders have grown significantly due to their proximity to underserved populations and customized repayment models. Fintech and Digital Lenders have started gaining traction by offering app-based approvals and alternative credit scoring models. These players are more prominent in Kampala and surrounding towns.

By Vehicle Type: Used Vehicles dominate the financed vehicle portfolio in Uganda, accounting for an estimated 85% of total financed units. These include passenger cars, commercial vans, and motorcycles, mostly imported from Japan, UK, or UAE. Their affordability makes them highly appealing to first-time buyers and small business owners. New Vehicles, though a small fraction of the financed market, are typically purchased by corporates, NGOs, and high-income consumers through formal banks or dealer-tied finance arms.

Competitive Landscape in Uganda Auto Finance Market

The Uganda auto finance market is moderately fragmented, with a mix of formal banks, microfinance institutions, and emerging digital lenders. While traditional banks such as Stanbic and DFCU dominate the formal financing landscape, the rise of informal lenders and fintech-based platforms is redefining how credit is accessed and disbursed, especially in peri-urban and rural areas. Players like Tugende, Asaak, and Watu Credit have brought innovation in asset-backed financing, especially for boda-bodas and small commercial vehicles.

| Company Name | Founding Year | Original Headquarters |

| MOGO Uganda | 2012 | Riga, Latvia |

| Tembo Automarket | 2020 | Kampala, Uganda |

| Absa Bank Uganda | 1927 | Johannesburg, South Africa |

| Stanbic Bank Uganda | 1906 | Johannesburg, South Africa |

| Bank of Africa Uganda | 1984 | Bamako, Mali |

| Equity Bank Uganda | 2008 | Nairobi, Kenya |

| UBA Uganda | 1949 | Lagos, Nigeria |

| NCBA Bank Uganda | 1959 | Nairobi, Kenya |

| Bank of India Uganda | 2012 | Mumbai, India |

| I&M Bank Uganda | 2016 | Nairobi, Kenya |

Some of the recent competitor trends and key information about competitors include:

Stanbic Bank: Uganda’s largest commercial bank continues to lead in formal auto finance, primarily catering to salaried professionals and corporates. In 2023, the bank partnered with leading car dealerships to offer bundled vehicle loan + insurance packages, resulting in a 17% YoY increase in auto loan disbursement.

DFCU Bank: Focuses on SME vehicle financing and fleet loans. DFCU reported a 12% rise in vehicle loan uptake among logistics and small construction firms in 2023, driven by post-COVID recovery in SME business activity.

Centenary Bank: Positioned as a pro-agribusiness lender, Centenary has expanded auto financing for agricultural vehicles and small trucks. In 2023, the bank launched a rural outreach initiative in Masaka and Mbarara, enabling loan origination through mobile credit agents.

Tugende: A market leader in lease-to-own financing for boda-boda riders, Tugende has financed over 60,000 two-wheelers since inception. In 2023 alone, the firm financed more than 12,000 motorcycles and introduced digital payment tracking to boost repayment rates.

Asaak: A fintech offering asset-based loans for informal workers, Asaak uses alternative credit scoring (such as mobile money and telecommunication records). In 2023, Asaak launched a product line for second-hand vehicle financing, targeting low-income urban populations.

Watu Credit: Originally launched in Kenya, Watu Credit has rapidly expanded across Uganda, financing two- and three-wheeler vehicles. In 2023, they financed over 18,000 assets and deployed a mobile collections team to improve field repayment efficiency.

Yalelo Microfinance: A new entrant focusing on commercial fishing and trade vehicle loans in Eastern Uganda. The company is experimenting with solar-powered asset financing linked to tuk-tuks and light trucks for lakeside communities.

What Lies Ahead for Uganda Auto Finance Market?

The Uganda auto finance market is projected to witness moderate but steady growth through 2029, supported by ongoing urban expansion, digital credit access, and increasing demand for income-generating vehicles. The industry is expected to expand at a CAGR of 7–9%, primarily driven by informal sector financing, rising entrepreneurship, and improved regulatory oversight.

Expansion of Two-Wheeler and Commercial Vehicle Financing: Given Uganda’s informal economy and strong reliance on mobility for income generation, the demand for financing of boda-bodas, tuk-tuks, and small commercial vehicles will continue to dominate. This segment is expected to account for over 60% of total financed units by 2029.

Digital Lending Ecosystem Maturity: Fintech-led solutions will play a key role in market expansion. Increased adoption of mobile credit scoring, eKYC, and digital repayment platforms will drive financial inclusion. Rural borrowers and first-time buyers are expected to benefit the most as digital lenders scale operations beyond Kampala and Wakiso.

Improved Vehicle Resale and Recovery Infrastructure: Development of structured vehicle resale markets and digitized ownership records will reduce asset recovery risks and encourage more institutions to enter vehicle financing. This will support growth in longer-tenure loans and more competitive interest rates.

Emergence of Green Auto Finance: Although still nascent, financing models for electric motorcycles and hybrid vehicles are expected to emerge in line with Uganda’s National Climate Change Policy. Pilot programs in Kampala may lead to broader adoption by 2027–2028, especially with donor-backed sustainability funds entering the sector.

Future Outlook and Projections for Uganda Car Finance Market Size on the Basis of Loan Disbursements in USD Billion, 2024-2029

Uganda Auto Finance Market Segmentation

By Market Structure:

Formal Financial Institutions (Commercial Banks)

Microfinance Institutions (MFIs, MDIs)

Non-Banking Finance Companies (NBFCs)

Fintech and Digital Lenders

SACCOs and Cooperative Societies

Informal Moneylenders

Vehicle Leasing Companies

By Lender Type:

Commercial Banks

Microfinance Institutions

Digital/Fintech Lenders

Asset-Leasing Firms

Development Finance Institutions (DFIs)

By Vehicle Type:

Used Passenger Cars

Used Commercial Vans

New Passenger Vehicles

Motorcycles/Boda-Bodas

Three-Wheelers (Tuk-Tuks)

Light Trucks

By Loan Tenure:

Up to 12 Months

13–24 Months

25–36 Months

37–48 Months

49–60 Months

By Age of Borrower:

18–24 Years

25–34 Years

35–50 Years

51+ Years

By Region:

Central Region (Kampala, Wakiso, Mukono)

Western Region (Mbarara, Fort Portal)

Eastern Region (Mbale, Jinja)

Northern Region (Gulu, Lira)

West Nile (Arua, Nebbi)

Players Mentioned in the Report (Banks):

- Absa Bank Uganda

- Bank of Africa Uganda

- Bank of Baroda Uganda

- Bank of India Uganda

- Cairo Bank Uganda

- Centenary Rural Development Bank

- Citibank Uganda

- DFCU Bank

- Diamond Trust Bank Uganda

- Ecobank Uganda

- Equity Bank Uganda

- Exim Bank Uganda

- Finance Trust Bank

- Guaranty Trust Bank Uganda

- Housing Finance Bank

- I&M Bank Uganda

- KCB Bank Uganda

- NCBA Bank Uganda

- Stanbic Bank Uganda

- Standard Chartered Bank Uganda

- Tropical Bank

- United Bank for Africa Uganda

- Yako Bank Uganda

Players Mentioned in the Report (NBFCs):

- M-KOPA Uganda

- Tembo Automarket

- JUMO Uganda

- Watu Credit Uganda

- MOGO Uganda

- Mwananchi Credit Uganda

- Berger Financial Services

- Jilead Financial Services

- Prime Image Financial Services

- Makarios Financial Group

- Ecolink Uganda

- Furaha Link Ventures

- Nalico Financial Services

- Ankunda Financial Services

- Real and Known Finance

- Legit Financial Services

Players Mentioned in the Report (Captive):

- Toyota Financial Services Uganda

- Volkswagen Financial Services Uganda

- Mercedes-Benz Financial Services Uganda

- Stellantis Financial Services Uganda

- CFAO Motors Uganda

Key Target Audience:

Commercial and Microfinance Banks

Non-Banking Finance Companies (NBFCs)

Fintech and Digital Lending Startups

Used Vehicle Importers and Dealers

Government & Regulatory Authorities (Bank of Uganda, URA, UNRA)

Auto Leasing and Mobility Platforms

Development Partners and Donor Agencies

Insurance Companies and Underwriting Partners

Time Period:

Historical Period: 2018–2023

Base Year: 2024

Forecast Period: 2024–2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-Role of Entities, Stakeholders, and challenges they face.

4.2. Relationship and Engagement Model between Banks-Dealers, NBFCs-Dealers and Captive-Dealers-Commission Sharing Model, Flat Fee Model and Revenue streams

5.1. New Car and Used Car Sales in Uganda by type of vehicle, 2018-2024

8.1. Credit Disbursed, 2018-2024

8.2. Outstanding Loan, 2018-2024

9.1. By Market Structure (Bank-Owned, Multi-Finance, and Captive Companies), 2023-2024

9.2. By Vehicle Type (Passenger, Commercial and EV), 2023-2024

9.3. By Region, 2023-2024

9.4. By Type of Vehicle (New and Used), 2023-2024

9.5. By Average Loan Tenure (0-2 years, 3-5 years, 6-8 years, above 8 years), 2023-2024

10.1. Customer Landscape and Cohort Analysis

10.2. Customer Journey and Decision-Making

10.3. Need, Desire, and Pain Point Analysis

10.4. Gap Analysis Framework

11.1. Trends and Developments for Uganda Car Finance Market

11.2. Growth Drivers for Uganda Car Finance Market

11.3. SWOT Analysis for Uganda Car Finance Market

11.4. Issues and Challenges for Uganda Car Finance Market

11.5. Government Regulations for Uganda Car Finance Market

12.1. Market Size and Future Potential for Online Car Financing Aggregators, 2018-2029

12.2. Business Model and Revenue Streams

12.3. Cross Comparison of Leading Digital Car Finance Companies Based on Company Overview, Revenue Streams, Loan Disbursements/Number of Leads Generated, Operating Cities, Number of Branches, and Other Variables

13.1. Finance Penetration Rate and Average Down Payment for New and Used Cars, 2018-2029

13.2. How Finance Penetration Rates are Changing Over the Years with Reasons

13.3. Type of Car Segment for which Finance Penetration is Higher

17.1. Market Share of Key Banks in Uganda Car Finance Market, 2024

17.2. Market Share of Key NBFCs in Uganda Car Finance Market, 2024

17.3. Market Share of Key Captive in Uganda Car Finance Market, 2024

17.4. Benchmark of Key Competitors in Uganda Car Finance Market, including Variables such as Company Overview, USP, Business Strategies, Strengths, Weaknesses, Business Model, Number of Branches, Product Features, Interest Rate, NPA, Loan Disbursed, Outstanding Loans, Tie-Ups and others

17.5. Strengths and Weaknesses

17.6. Operating Model Analysis Framework

17.7. Gartner Magic Quadrant

17.8. Bowmans Strategic Clock for Competitive Advantage

18.1. Credit Disbursed, 2025-2029

18.2. Outstanding Loan, 2025-2029

19.1. By Market Structure (Bank-Owned, Multi-Finance, and Captive Companies), 2025-2029

19.2. By Vehicle Type (Passenger, Commercial and EV), 2025-2029

19.3. By Region, 2025-2029

19.4. By Type of Vehicle (New and Used), 2025-2029

19.5. By Average Loan Tenure (0-2 years, 3-5 years, 6-8 years, above 8 years), 2025-2029

19.6. Recommendations

19.7. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand side and supply side entities for Uganda Auto Finance Market. Basis this ecosystem, we will shortlist leading 5-6 financiers in the country based upon their financial information, disbursed loan value/volume, and regional presence.

Sourcing is made through industry articles, multiple secondary, and proprietary databases to perform desk research around the market to collate industry-level information.

Step 2: Desk Research

Subsequently, we engage in an exhaustive desk research process by referencing diverse secondary and proprietary databases. This approach enables us to conduct a thorough analysis of the market, aggregating industry-level insights. We delve into aspects like the disbursed loan values, number of market players, average ticket size, interest rates, demand by region, and other variables. We supplement this with detailed examinations of company-level data, relying on sources like press releases, annual reports, financial statements, and similar documents. This process aims to construct a foundational understanding of both the market and the entities operating within it.

Step 3: Primary Research

We initiate a series of in-depth interviews with C-level executives and other stakeholders representing various Uganda Auto Finance Market companies and end-users. This interview process serves a multi-faceted purpose: to validate market hypotheses, authenticate statistical data, and extract valuable operational and financial insights from these industry representatives. Bottom to top approach is undertaken to evaluate volume disbursed for each player thereby aggregating to the overall market.

As part of our validation strategy, our team executes disguised interviews wherein we approach each company under the guise of potential customers. This approach enables us to validate the operational and financial information shared by company executives, corroborating this data against what is available in secondary databases. These interactions also provide us with a comprehensive understanding of revenue streams, value chain, process, pricing, and other factors.

Step 4: Sanity Check

- Bottom to top and top to bottom analysis along with market size modeling exercises is undertaken to assess sanity check process.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Uganda Auto Finance Market is projected to grow steadily, reaching a market valuation of approximately UGX 4.5 trillion by 2029. This growth is supported by increased demand for income-generating vehicles, expansion of digital credit platforms, and a rising trend of vehicle ownership among urban and peri-urban consumers. The market's long-term potential is strengthened by financial inclusion efforts and the shift toward mobile-based and usage-linked financing solutions.

Key players in the Uganda Auto Finance Market include Stanbic Bank, DFCU Bank, Centenary Bank, Tugende, Asaak, and Watu Credit. These entities dominate various segments of the market, ranging from formal salaried loans to micro-lease financing for informal and gig economy workers. Emerging fintechs and regional MFIs are also entering the space with innovative lending models.

The primary growth drivers include the rising need for affordable personal and commercial mobility, particularly among informal sector workers. The expansion of digital lending ecosystems, greater smartphone and mobile money penetration, and tailored loan products for boda-boda riders and small businesses are also key contributors. Supportive government policies for financial inclusion and infrastructure development further aid market growth.

The Uganda Auto Finance Market faces challenges such as high interest rates, limited credit history among borrowers, and heavy reliance on informal income sources, which restrict access to formal credit. Asset depreciation risk due to the dominance of used vehicle imports, regulatory burdens on vehicle imports, and the lack of a formalized secondary vehicle market also present significant hurdles for financiers.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0