Colombia Cold Chain Market Outlook to 2029

By Market Structure, By Temperature Range, By Products Stored, By End User Industry, By Ownership and By Region

Report Overview

Report Code

TDR0262

Coverage

Central and South America

Published

September 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Colombia Cold Chain Market Outlook to 2029 – By Market Structure, By Temperature Range, By Products Stored, By End User Industry, By Ownership and By Region” provides a comprehensive analysis of the cold chain logistics market in Colombia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation, trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the Colombia Cold Chain Market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Colombia Cold Chain Market Outlook to 2029 – By Market Structure, By Temperature Range, By Products Stored, By End User Industry, By Ownership and By Region” provides a comprehensive analysis of the cold chain logistics market in Colombia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation, trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross comparison, opportunities and bottlenecks, and company profiling of major players in the Colombia Cold Chain Market. The report concludes with future market projections based on revenue, by product type, storage type, region, cause and effect relationships, and success case studies highlighting the major opportunities and cautions.

Colombia Cold Chain Market Overview and Size

The Colombia cold chain market reached a valuation of COP 3.4 Trillion in 2023, driven by the rising demand for temperature-controlled storage in pharmaceuticals, dairy, and fresh produce industries, as well as growing exports of perishable goods. The market is characterized by players such as Servientrega, Logyca, Cold Logistic, Frioport, and DHL Supply Chain, which are recognized for their integrated warehousing and transport services, advanced refrigeration technology, and regulatory compliance.

In 2023, Frioport expanded its cold storage footprint in Bogotá, launching a new multi-temperature warehouse to support the rising demand for processed and frozen foods. Bogotá and Medellín are considered key hubs due to their infrastructure, distribution connectivity, and industrial activity.

%252C%25202019-2024.png&w=640&q=75)

What Factors are Leading to the Growth of Colombia Cold Chain Market:

Export Growth of Perishables: Colombia’s exports of perishables like flowers, avocados, and berries increased by over 8% CAGR from 2018–2023. This has necessitated investment in reefer trucks, cold rooms, and airport-based cold storage facilities.

Pharmaceutical and Vaccine Logistics: With rising healthcare access and public-private immunization programs, pharma cold chain demand surged. In 2023, over 30% of cold storage utilization was from healthcare, especially post-COVID vaccine distribution needs.

Retail and E-commerce Expansion: Major retail and food chains like Éxito, Olímpica, and Rappi are expanding their fresh and frozen product categories, necessitating robust last-mile cold logistics. As of 2023, 26% of cold chain revenue came from urban grocery and food delivery.

Which Industry Challenges Have Impacted the Growth for Colombia Cold Chain Market

Infrastructure Gaps in Rural and Secondary Cities: A significant challenge remains the lack of cold storage infrastructure in Tier 2 and Tier 3 cities. Over 45% of Colombia’s perishable agricultural output comes from regions with limited cold chain access. As a result, nearly 30% of perishable goods experience post-harvest losses due to inadequate cold storage or inefficient transport.

High Operating and Energy Costs: Cold chain operations in Colombia face high electricity costs, especially in urban centers like Bogotá and Medellín. In 2023, energy accounted for 25–30% of operational expenses for cold storage warehouses, limiting the profitability and scalability of smaller players.

Fragmented Logistics Ecosystem: The cold chain sector is highly fragmented, with many small and medium-sized operators lacking end-to-end capabilities. This leads to inefficiencies such as temperature deviations during intermodal transfers. A study in 2023 showed that 18% of cold chain failures were due to coordination lapses between transporters and warehouse operators.

What are the Regulations and Initiatives which have Governed the Market:

INVIMA Temperature Control Regulations: The Colombian National Food and Drug Surveillance Institute (INVIMA) mandates strict temperature controls for pharmaceutical and food logistics. In 2023, compliance audits increased by 15%, with fines imposed on operators lacking calibrated monitoring equipment or deviation records.

Subsidies for Cold Storage Infrastructure: The government, through the Ministry of Agriculture, launched a subsidy program in 2022 offering up to 40% cost support for establishing cold storage units in high-production zones. This has led to over 120 new cold rooms being set up in regions like Cundinamarca and Antioquia by 2023.

Trade Facilitation for Agri-exports: Colombia’s National Development Plan (PND) emphasizes modernization of agro-logistics to support exports. In 2023, special clearance zones with cold holding areas were created at major airports (e.g., El Dorado in Bogotá), reducing customs processing time for perishables by 22%.

Colombia Cold Chain Market Segmentation

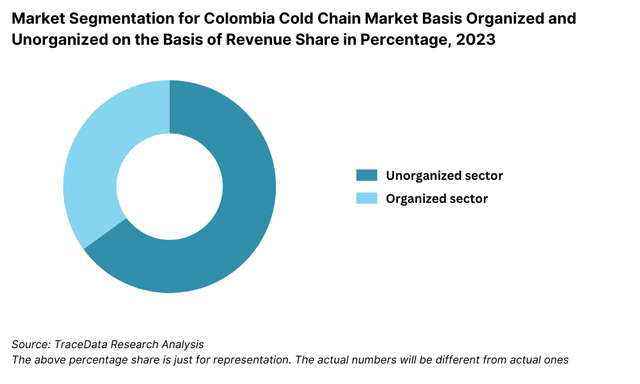

By Market Structure: The unorganized sector currently dominates the Colombian cold chain market, primarily composed of small-scale operators, local transporters, and facility owners with limited technology integration. These players cater mainly to short-haul and regional distribution due to their cost-effective pricing and proximity to farms and local food processors.

The organized sector, however, is growing rapidly, driven by international 3PLs, pharma logistics providers, and retail supply chain operators offering end-to-end temperature-controlled logistics. These players are adopting advanced tracking technologies, automation, and centralized distribution hubs to improve service reliability and regulatory compliance.

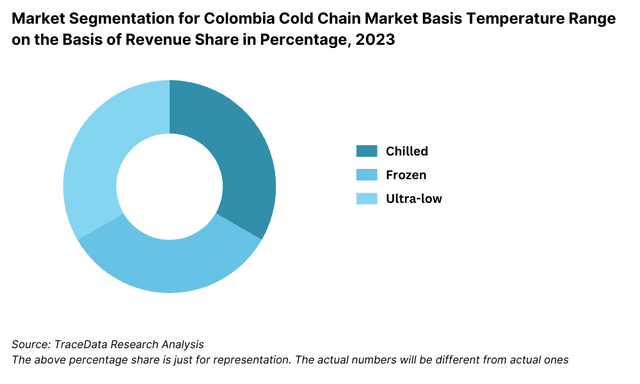

By Temperature Range: The market is segmented into Chilled (0°C to 10°C) and Frozen (-18°C and below) categories. Chilled storage is dominant due to high domestic movement of fresh produce, dairy, and beverages. Frozen storage is critical for meat, seafood, and processed food exports, which account for a significant share of Colombia’s cold exports. A smaller portion of the market also includes Ultra-low temperature storage (for vaccines and biotech), which is gaining relevance due to rising pharma investments.

By Product Category: Fruits and vegetables lead the market due to Colombia’s strong agricultural base and export focus. Meat and seafood follow closely, especially from coastal regions, requiring deep frozen logistics. Pharmaceuticals and dairy products are emerging segments with growing cold storage requirements, driven by urban consumption and health regulations.

Competitive Landscape in Colombia Cold Chain Market

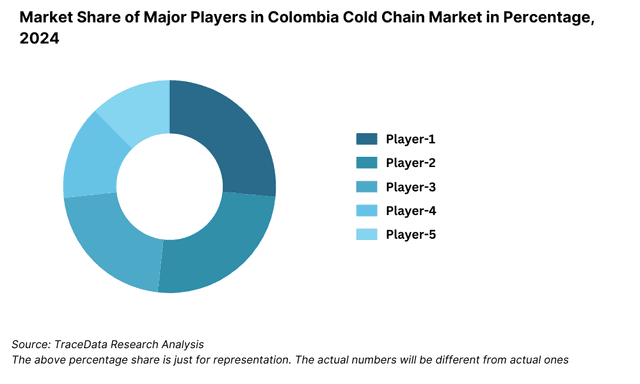

The Colombia cold chain market is moderately fragmented, with a mix of established logistics providers, regional cold storage operators, and emerging digital logistics platforms. The entry of global 3PLs and the expansion of cold infrastructure by domestic firms like Servientrega, Logyca, and Frioport have intensified competition, while technology-driven players are disrupting traditional models through real-time monitoring and integrated services.

Company | Establishment Year | Headquarters |

Servientrega | 1982 | Bogotá, Colombia |

Logyca | 2004 | Bogotá, Colombia |

Frioport | 2011 | Barranquilla, Colombia |

DHL Supply Chain | 1969 (Colombia: 1996) | Bogotá, Colombia |

Cold Logistic S.A. | 2010 | Medellín, Colombia |

Some of the recent competitor trends and key information about competitors include:

Servientrega: A major logistics player in Colombia, Servientrega expanded its cold chain services in 2023 by adding refrigerated delivery capabilities to its urban last-mile network. The firm reported a 22% YoY growth in its cold logistics division, driven by e-commerce demand for frozen and fresh food.

Logyca: Known for its supply chain optimization and warehousing services, Logyca introduced a blockchain-based temperature traceability solution in 2023 for pharmaceutical clients. The technology has improved audit compliance and reduced temperature excursion incidents by 18%.

Frioport: A leading cold storage operator in Colombia’s Atlantic region, Frioport opened a new 25,000-pallet capacity facility in Barranquilla port in 2023. This expansion aims to support rising export volumes of frozen meat and seafood to the U.S. and Europe.

DHL Supply Chain: Leveraging its global expertise, DHL expanded its temperature-controlled pharma logistics capacity in Bogotá and Cali. In 2023, DHL handled over 3.2 million temperature-sensitive packages across Colombia with an on-time delivery rate exceeding 97%.

Cold Logistic S.A.: A regional cold chain operator, Cold Logistic upgraded its Medellín warehouse with IoT-based real-time temperature monitoring in 2023. The company also signed long-term contracts with dairy and beverage clients, boosting its annual revenue by 14%.

What Lies Ahead for Colombia Cold Chain Market?

The Colombia cold chain market is projected to experience robust growth through 2029, with a strong CAGR driven by rising demand from the agri-exports, pharmaceutical, and food retail sectors. Infrastructure development, regulatory support, and digital transformation are expected to play key roles in shaping the market’s future.

Expansion of Agri-Export-Oriented Cold Chain Infrastructure: With Colombia aiming to increase exports of perishables like avocados, flowers, and berries, significant investment is expected in port-based cold storage, reefer trucks, and packhouses. Government-backed export promotion programs and trade agreements with North America and Europe will further fuel this trend.

Pharmaceutical Cold Chain Modernization: As Colombia becomes a key distribution hub for vaccines and biologics in Latin America, the demand for ultra-low temperature storage and compliant cold transport will rise. Strategic partnerships between logistics companies and pharma manufacturers are anticipated to grow significantly.

Adoption of IoT and Automation: The use of IoT sensors, cloud-based monitoring, and AI for predictive maintenance is projected to increase across cold warehouses and vehicles. These technologies will reduce spoilage, improve fuel efficiency, and support real-time visibility across the supply chain, attracting international clients.

Growth in Urban Last-Mile Cold Logistics: With increasing consumer preference for online grocery and meal delivery platforms like Rappi and Éxito, the demand for efficient last-mile cold chain logistics in urban centers will surge. Companies are likely to invest in smaller, decentralized cold storage hubs and electric reefer vehicles for same-day deliveries.

%252C%25202024-2030.png&w=640&q=75)

Colombia Cold Chain Market Segmentation

- By Market Structure:

o Organized Sector

o Unorganized Sector

o Integrated 3PL Cold Chain Providers

o Standalone Cold Storage Operators

o Temperature-Controlled Transporters

o Regional Logistics Providers - By Temperature Range:

o Chilled (0°C to 10°C)

o Frozen (-18°C and below)

o Ambient Controlled

o Ultra-Low Temperature (-80°C and below – mainly for pharmaceuticals) - By Product Category:

o Fruits and Vegetables

o Meat and Seafood

o Dairy Products

o Pharmaceuticals and Vaccines

o Baked Goods and Confectionery

o Beverages - By End User Industry:

o Food & Beverage

o Agriculture & Horticulture

o Pharmaceuticals & Life Sciences

o Retail and E-Commerce

o Hospitality & Food Service - By Ownership:

o Private Logistics Providers

o Government-Supported Facilities

o Cooperative-Owned Cold Chains

o Retailer-Owned Infrastructure - By Region:

o Bogotá Capital District

o Antioquia (Medellín and surrounding areas)

o Valle del Cauca (Cali and surrounding areas)

o Atlántico and Caribbean Coast

o Cundinamarca and Central Region

o Eje Cafetero and Southwestern Region

Players Mentioned in the Report:

- Servientrega

- Logyca

- Frioport

- DHL Supply Chain

- Cold Logistic S.A.

- Kuehne + Nagel Colombia

- RappiLogística

- Colombiana de Comercio Refrigerado

Key Target Audience:

- Cold Chain Logistics Providers

- Food & Pharma Exporters

- Agricultural Cooperatives

- Supermarkets and Retail Chains

- Pharmaceutical Manufacturers and Distributors

- Regulatory Authorities (e.g., INVIMA, ICA)

- Technology and Cold Storage Equipment Suppliers

- Investment and Infrastructure Development Agencies

Time Period:

- Historical Period: 2018–2023

- Base Year: 2024

- Forecast Period: 2024–2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-“ Role of Entities, Stakeholders, and Challenges

4.2. Revenue Streams for Colombia Cold Chain Market

4.3. Business Model Canvas for Colombia Cold Chain Market

4.4. Cold Chain Decision Making Process-“ Exporters and Distributors

4.5. Supply Chain Flow from Farm/Factory to Retail

5.1. Overview of Cold Chain Industry in Colombia

5.2. Cold Chain Infrastructure Gap Analysis

5.3. Number of Cold Storage Facilities by Region

5.4. Reefer Truck and Container Availability in Colombia

8.1. Revenues, 2018-“2024

8.2. Storage Capacity (Pallet Positions / Cubic Meters), 2018-“2024

8.3. Reefer Truck Capacity (Fleet Size), 2018-“2024

9.1. By Market Structure (Organized and Unorganized), 2023-“2024P

9.2. By Temperature Range (Chilled, Frozen, Ultra-Low), 2023-“2024P

9.3. By Product Category (Fruits, Dairy, Meat, Pharma, Others), 2023-“2024P

9.4. By End-User Industry (F&B, Pharma, Retail, Agriculture), 2023-“2024P

9.5. By Ownership Type (Private, Cooperative, Government-Aided), 2023-“2024P

9.6. By Region (Bogotá, Antioquia, Valle del Cauca, etc.), 2023-“2024P

10.1. Client Profile-“ Food Exporters, Distributors, Pharma Firms

10.2. User Needs and Preferences in Cold Storage and Logistics

10.3. Challenges Faced by End Users

10.4. Pain Point and Opportunity Mapping

11.1. Trends and Developments in Colombia Cold Chain Market

11.2. Growth Drivers for Colombia Cold Chain Market

11.3. SWOT Analysis

11.4. Issues and Challenges in the Cold Chain Value Chain

11.5. Government Regulations and Incentives

12.1. Market Size and Forecast of Cold E-Grocery Delivery, 2018-“2029

12.2. Revenue Streams in B2B and B2C Cold Delivery

12.3. Cross Comparison of Key Cold Chain Players by Reach, Tech Adoption, and Sector Served

13.1. Government Grants, Subsidies, and Programs (MinAgri, MinSalud)

13.2. Private Investment and PE/VC Activity in Cold Chain Startups

13.3. Financing Barriers and Infrastructure Gaps

16.1. Benchmarking of Key Competitors-“ Overview, Strength, USP, Services

16.2. Strengths and Weaknesses of Major Players

16.3. Operating Model Analysis Framework

16.4. Gartner Magic Quadrant Style Positioning

16.5. Bowmans Strategic Clock for Competitive Advantage

17.1. Revenues, 2025-“2029

17.2. Storage and Transport Capacity, 2025-“2029

18.1. By Market Structure (Organized and Unorganized), 2025-“2029

18.2. By Temperature Range, 2025-“2029

18.3. By Product Category, 2025-“2029

18.4. By Region, 2025-“2029

18.5. By End-User Industry, 2025-“2029

18.6. By Ownership Type, 2025-“2029

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities for the Colombia Cold Chain Market. Based on this ecosystem, we shortlist the leading 5–6 players in the country based on their infrastructure capacity, service footprint, client base, and technological capabilities.

Sourcing is conducted through industry journals, trade associations, regulatory databases (e.g., INVIMA, ICA), and multiple proprietary and open-access databases to perform desk research and gather industry-level information.

Step 2: Desk Research

We proceed with comprehensive desk research by referencing a wide array of secondary and proprietary databases. This enables an in-depth analysis of the cold chain market, compiling data points such as revenue estimates, warehousing capacities, regional distribution patterns, pricing benchmarks, and regulatory compliance levels.

In addition, company-level insights are gathered using sources like annual reports, press releases, investor presentations, tenders, infrastructure announcements, and logistics sector reports. This process helps build a baseline understanding of both market dynamics and player positioning.

Step 3: Primary Research

A series of detailed interviews are conducted with C-level executives, operations heads, facility managers, and logistics planners representing Colombia Cold Chain companies and their major clients across food, agriculture, and pharmaceutical sectors. These discussions help validate market assumptions, understand growth drivers and bottlenecks, and collect financial and operational insights.

Our team also executes disguised interviews, approaching companies as potential clients to validate the claims made by the company representatives. This cross-verification approach enables us to assess accuracy in warehouse utilization rates, transport capacities, temperature compliance, pricing models, and value-added services offered.

Step 4: Sanity Check

- Both bottom-up and top-down market estimation techniques are applied to triangulate and validate the total market size. Sensitivity analysis is also conducted based on warehouse capacity, reefer fleet size, product perishability profiles, and trade data to ensure robustness of forecasts.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Colombia cold chain market holds strong growth potential, reaching a valuation of COP 3.4 Trillion in 2023. Its expansion is driven by increasing demand for temperature-sensitive logistics in the agri-export, pharmaceutical, and retail sectors. With rising exports of perishables and stricter regulations in food and drug safety, the market is expected to grow steadily through 2029, supported by infrastructure investments and digital transformation.

Key players in the Colombia Cold Chain Market include Servientrega, Logyca, Frioport, DHL Supply Chain, and Cold Logistic S.A. These companies are recognized for their extensive warehousing networks, compliance capabilities, and adoption of IoT-enabled cold chain solutions. Other emerging players like RappiLogística and Colombiana de Comercio Refrigerado are also gaining traction in the last-mile and regional cold logistics segments.

The market's growth is propelled by increasing agri-export volumes, rising pharmaceutical cold storage requirements, growing urban demand for perishable goods, and supportive government initiatives. The adoption of technology such as IoT monitoring, temperature tracking, and WMS solutions is also playing a pivotal role in improving efficiency and traceability, thereby enhancing market attractiveness.

Key challenges include limited cold storage infrastructure in rural areas, high operating and energy costs, fragmented logistics networks, and compliance difficulties with changing regulatory standards. Small and medium operators often lack the capacity to invest in advanced technology, leading to inefficiencies and service limitations. These constraints must be addressed to unlock the full market potential.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0