Denmark Logistics and Warehousing Market Outlook to 2029

By Mode of Transport (Road, Rail, Air, Sea), By End User (Retail, FMCG, Healthcare, Automotive, E-Commerce, Others), By Type of Warehousing (General, Cold Storage, Bonded, Others), By Region

Report Overview

Report Code

TDR0265

Coverage

Europe

Published

September 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Denmark Logistics and Warehousing Market Outlook to 2029 – By Mode of Transport (Road, Rail, Air, Sea), By End User (Retail, FMCG, Healthcare, Automotive, E-Commerce, Others), By Type of Warehousing (General, Cold Storage, Bonded, Others), By Region” provides a comprehensive analysis of the logistics and warehousing sector in Denmark. The report covers the genesis and evolution of the industry, overall market size in terms of revenue, segmentation by transport and warehousing type, end-user industries, and regional analysis.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Denmark Logistics and Warehousing Market Outlook to 2029 – By Mode of Transport (Road, Rail, Air, Sea), By End User (Retail, FMCG, Healthcare, Automotive, E-Commerce, Others), By Type of Warehousing (General, Cold Storage, Bonded, Others), By Region” provides a comprehensive analysis of the logistics and warehousing sector in Denmark. The report covers the genesis and evolution of the industry, overall market size in terms of revenue, segmentation by transport and warehousing type, end-user industries, and regional analysis. It further delves into major trends and developments, government regulations, customer profiling, challenges, opportunities, competitive landscape including company profiles and cross comparisons, and concludes with future outlook based on revenue projections and key success case studies.

Denmark Logistics and Warehousing Market Overview and Size

The Denmark logistics and warehousing market was valued at DKK 54 Billion in 2023, supported by the country’s strategic location in Northern Europe, strong trade ties with EU partners, and the high penetration of digital technologies in supply chain operations. Major players such as DSV, PostNord, Blue Water Shipping, Bring, and Frode Laursen are leading the market with comprehensive transport networks, modern warehousing infrastructure, and strong 3PL offerings.

In 2023, DSV expanded its warehousing footprint in Jutland, adding over 80,000 sqm of automated storage facilities to support its FMCG and e-commerce clients. Copenhagen and Aarhus remain the key logistics hubs, owing to their port connectivity, road infrastructure, and proximity to population centers.

%252C%25202019-2024.png&w=640&q=75)

What Factors are Leading to the Growth of Denmark Logistics and Warehousing Market:

E-Commerce and Retail Growth: The sharp rise in online retail, particularly post-2020, has led to increased demand for last-mile logistics and fulfillment centers. In 2023, Denmark saw a 12% YoY increase in e-commerce transactions, resulting in growing investments in micro-fulfillment and urban distribution hubs.

Strategic Location and Trade Facilitation: Positioned as a gateway to Scandinavia and the Baltics, Denmark serves as a transshipment and logistics base for Northern Europe. Trade volumes through Danish ports rose by 7% in 2023, with sea freight and intermodal services contributing significantly to market expansion.

Sustainability and Green Logistics: Denmark’s aggressive climate targets and consumer push for green logistics have driven adoption of electric freight fleets and energy-efficient warehouses. In 2023, over 30% of new logistics vehicles registered were electric or hybrid, and solar-powered warehouses increased by 18% YoY.

Which Industry Challenges Have Impacted the Growth for Denmark Logistics and Warehousing Market

Labor Shortages and Rising Wages: One of the most pressing challenges in Denmark’s logistics sector is the shortage of skilled labor, particularly drivers and warehouse operators. As of 2023, nearly 28% of logistics companies reported unfilled vacancies, with wage inflation increasing operating costs by 6–8% annually. The lack of workforce availability has led to delivery delays and underutilization of logistics infrastructure in some regions.

Space Constraints and High Warehousing Costs: Limited availability of industrial real estate—especially around major hubs such as Copenhagen and Aarhus—has driven up warehousing rental prices. In 2023, prime logistics rents rose by approximately 11% YoY, making it difficult for smaller 3PLs and e-commerce startups to secure affordable storage solutions. This spatial limitation has become a major bottleneck, particularly for temperature-controlled and bonded warehousing.

Fragmented Cold Chain Infrastructure: Despite Denmark’s prominence in pharma and food exports, the cold chain infrastructure remains underdeveloped outside key urban areas. As of 2023, only 17% of Denmark’s total warehouse stock was equipped with temperature-controlled facilities, creating gaps in service continuity and increasing spoilage risks—especially for exports to non-EU markets.

What are the Regulations and Initiatives which have Governed the Market

Green Logistics Mandates and Emission Regulations: Denmark’s National Logistics Strategy mandates emission reductions across all logistics operations in line with the EU Green Deal. From 2023, new regulations have required logistics companies operating fleets larger than 10 vehicles to ensure at least 25% of their fleet is low-emission (electric or hybrid). Compliance has grown to 68% among leading 3PL providers, but smaller operators continue to struggle with conversion costs.

Port Modernization and Intermodal Infrastructure Investments: The Danish Ministry of Transport initiated a DKK 4.2 Billion upgrade program across major ports like Aarhus and Esbjerg, aiming to improve intermodal integration with road and rail by 2026. These upgrades include digitized customs processing, real-time cargo tracking systems, and expanded container handling capacity.

Warehouse Digitalization Incentives: Through the “Smart Industry Denmark” initiative, the government is offering grants and tax deductions for logistics companies investing in automation, AI-driven inventory management, and robotics. In 2023, over 430 warehouses applied for such support, with nearly 38% of them implementing AGVs (automated guided vehicles) or WMS (warehouse management systems) to boost efficiency.

Denmark Logistics and Warehousing Market Segmentation

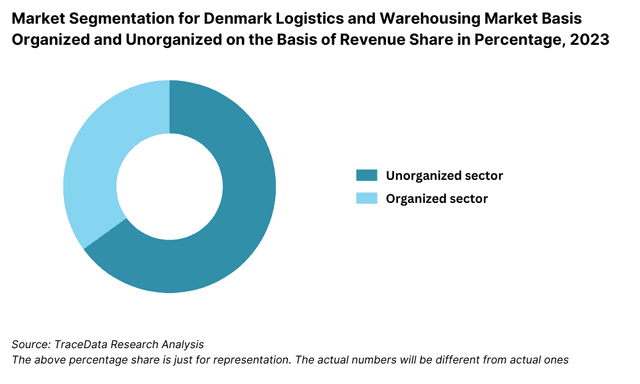

By Market Structure: Organized players dominate the Denmark logistics and warehousing market due to their widespread infrastructure, digital capabilities, and adherence to EU compliance norms. Leading logistics service providers such as DSV, PostNord, and Blue Water Shipping hold significant market share owing to their investment in automated warehouses, green transportation, and last-mile delivery infrastructure. Unorganized or smaller operators, although present, cater primarily to niche or rural markets and lack the scale or technological sophistication to compete on service quality and efficiency.

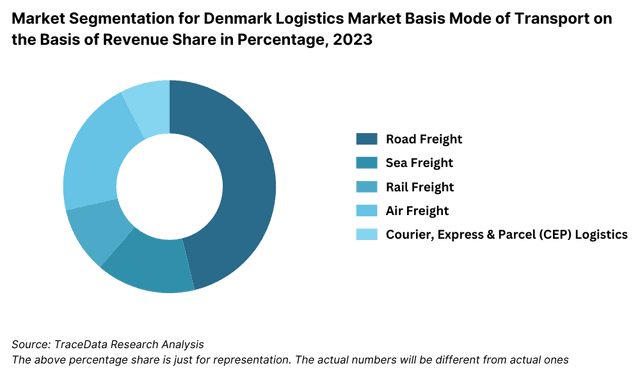

By Mode of Transport: Road transport remains the primary mode due to Denmark’s efficient road infrastructure and connectivity with regional hubs. Sea transport also plays a critical role, leveraging Denmark’s ports such as Aarhus, Esbjerg, and Copenhagen for international trade. Rail freight, though smaller in share, is witnessing increased adoption with growing emphasis on sustainability. Air transport is primarily used for time-sensitive and high-value cargo, especially in pharmaceuticals and electronics.

By Type of Warehousing: General warehousing accounts for the majority of the market share due to its use across sectors including FMCG, industrial goods, and retail. Cold storage warehousing is witnessing growth driven by Denmark’s strong pharmaceutical and food processing sectors. Bonded warehouses are primarily located near ports and are critical for re-export activities and international trade. Smart warehouses with automation and robotics are emerging in the organized segment and are expected to gain momentum in the coming years.

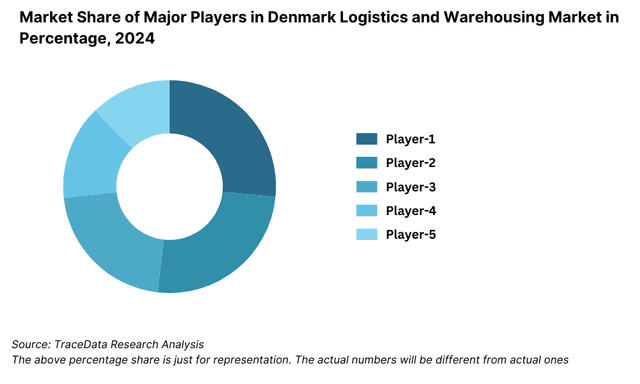

Competitive Landscape in Denmark Logistics and Warehousing Market

The Denmark logistics and warehousing market is moderately concentrated, with a few leading players dominating the organized segment. The presence of global 3PL companies such as DSV and DB Schenker, along with strong regional players like PostNord, Blue Water Shipping, and Frode Laursen, has established a robust and reliable logistics backbone in the country. Additionally, the adoption of digital supply chain solutions and green logistics strategies has become a key differentiator among players in the competitive landscape.

Company | Establishment Year | Headquarters |

DSV | 1976 | Hedehusene, Denmark |

PostNord | 2009 (Merger) | Copenhagen, Denmark |

Blue Water Shipping | 1972 | Esbjerg, Denmark |

Frode Laursen | 1948 | Vitten, Denmark |

Bring | 2002 | Oslo, Norway (operates widely in Denmark) |

Some of the recent competitor trends and key information about competitors include:

DSV: Denmark’s largest logistics company, DSV reported over DKK 190 billion in global revenue in 2023. The company expanded its Danish operations by opening a 150,000 sqm logistics center near Horsens, focused on automation and sustainability, featuring solar-powered operations and EV charging infrastructure.

PostNord: Specializing in mail and parcel logistics, PostNord Denmark processed over 58 million parcels in 2023, a 12% rise from the previous year. The company has invested heavily in last-mile infrastructure, particularly to support growing e-commerce logistics across Copenhagen and surrounding areas.

Blue Water Shipping: A key player in international freight forwarding and port logistics, Blue Water Shipping enhanced its cold chain capabilities in 2023 by launching new temperature-controlled facilities near Aarhus Port to support pharmaceutical exports.

Frode Laursen: Known for its warehousing and retail distribution services, Frode Laursen operates over 700,000 sqm of warehousing across Denmark and the Nordics. In 2023, the company focused on electrifying its transport fleet and automating warehouse operations to reduce environmental impact.

Bring: A Nordic logistics company operating in Denmark, Bring has gained market traction in B2C parcel logistics. It saw a 17% increase in parcel volumes in 2023, especially in suburban and rural areas, supported by investments in AI-driven route optimization and locker-based deliveries.

What Lies Ahead for Denmark Logistics and Warehousing Market?

The Denmark logistics and warehousing market is projected to grow steadily by 2029, demonstrating a healthy CAGR during the forecast period. This growth will be driven by the country’s strategic geographic location, increasing e-commerce penetration, and a strong policy push towards green and digital logistics solutions.

Acceleration of Green Logistics: As Denmark aims to achieve climate neutrality by 2050, the logistics sector is expected to adopt low-emission vehicles, solar-powered warehouses, and carbon-offset delivery solutions at a faster pace. Leading logistics firms are already investing in electric trucks and biofuel alternatives. This momentum is likely to intensify as both government mandates and consumer preferences continue to align with sustainability goals.

Rise of Automated and Smart Warehousing: With labor shortages and cost pressures persisting, companies will increasingly turn to automation technologies, such as warehouse robotics, AI-powered inventory systems, and autonomous mobile robots (AMRs). This will significantly improve warehouse throughput, reduce human error, and optimize space utilization.

Expansion of Cold Chain Infrastructure: The growing demand for temperature-sensitive products—particularly in pharmaceuticals, food exports, and e-grocery segments—is expected to drive investments in cold storage capacity. Regions like Southern Denmark and Greater Copenhagen are anticipated to see the largest cold chain expansion over the next few years.

Integration of Digital Freight Platforms: Digital freight matching platforms and transport management systems (TMS) are anticipated to gain wider adoption, improving vehicle utilization and route planning across domestic and international routes. This integration is expected to streamline operations, reduce empty runs, and provide real-time visibility across the supply chain.

%252C%25202024-2030.png&w=640&q=75)

Denmark Logistics and Warehousing Market Segmentation

• By Market Structure:

o Organized Sector

o Unorganized Sector

o Domestic Logistics Providers

o International 3PL/4PL Providers

o Courier, Express, and Parcel (CEP) Companies

o Contract Logistics Providers

o E-Commerce Fulfillment Centers

• By Mode of Transport:

o Road

o Rail

o Sea

o Air

o Intermodal

• By Type of Warehousing:

o General Warehousing

o Cold Storage Warehousing

o Bonded Warehousing

o Automated/Smart Warehousing

o Temperature-Controlled Storage

o E-Commerce Fulfillment Hubs

• By End User Industry:

o Retail and E-Commerce

o Automotive and Spare Parts

o Pharmaceuticals and Healthcare

o FMCG and Food Processing

o Industrial and Machinery

o Agriculture and Chemicals

• By Region:

o Capital Region (Copenhagen)

o Central Denmark (Aarhus, Herning)

o Southern Denmark (Odense, Kolding)

o North Denmark (Aalborg, Hjørring)

o Zealand Region

Players Mentioned in the Report:

• DSV

• PostNord

• Blue Water Shipping

• Frode Laursen

• Bring

• DB Schenker Denmark

• H. Daugaard A/S

• Danske Fragtmænd

• GLS Denmark

Key Target Audience:

• Logistics Service Providers

• Warehousing Operators

• E-Commerce Platforms

• Manufacturing and Retail Companies

• Real Estate Developers (Logistics Parks)

• Transport Infrastructure Authorities

• Investment and Private Equity Firms

• Regulatory Bodies (e.g., Danish Transport Authority)

Time Period:

• Historical Period: 2018–2023

• Base Year: 2024

• Forecast Period: 2024–2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-“ Role of Entities, Stakeholders, and challenges that they face

4.2. Revenue Streams for Denmark Logistics and Warehousing Market

4.3. Business Model Canvas for Denmark Logistics and Warehousing Market

4.4. Logistics Procurement Decision-Making Process

4.5. Warehousing Location and Outsourcing Decision-Making Process

5.1. Logistics Cost as % of GDP in Denmark, 2018-“2024

5.2. Modal Share of Freight Transport in Denmark (Road, Rail, Sea, Air), 2018-“2024

5.3. Share of Organized vs Unorganized Logistics Providers, 2023

5.4. Warehousing Stock and Rent Trends in Major Cities (Copenhagen, Aarhus, Odense), 2018-“2024

8.1. Revenues, 2018-“2024

8.2. Freight Volume Handled, 2018-“2024

8.3. Warehousing Capacity (in million sq. m), 2018-“2024

9.1. By Market Structure (Organized and Unorganized Market), 2023-“2024P

9.2. By Type of Warehousing (General, Cold Storage, Bonded, Automated), 2023-“2024P

9.3. By Mode of Transport (Road, Rail, Sea, Air, Intermodal), 2023-“2024P

9.4. By Region (Capital Region, Central Denmark, Southern Denmark, North Denmark, Zealand), 2023-“2024P

9.5. By End-User Industry (Retail, Automotive, Pharma, FMCG, Industrial), 2023-“2024P

10.1. Industry-Wise Logistics Spending and Preferences

10.2. Decision-Making Criteria for Logistics Partner Selection

10.3. Need, Pain Point, and Expectation Analysis

10.4. Gap Analysis Framework-“ From Demand to Infrastructure Availability

11.1. Trends and Developments for Denmark Logistics and Warehousing Market

11.2. Growth Drivers for Denmark Logistics and Warehousing Market

11.3. SWOT Analysis for Denmark Logistics and Warehousing Market

11.4. Issues and Challenges for Denmark Logistics and Warehousing Market

11.5. Government Regulations and Green Logistics Policies in Denmark

12.1. Market Size and Growth for B2C Parcel Logistics, 2018-“2029

12.2. Distribution Model for Urban vs Rural Fulfillment

12.3. Comparison of Key E-Commerce Logistics Providers

13.1. Cold Chain Capacity and Coverage in Denmark

13.2. Key Industries Using Cold Storage and Temperature-Controlled Transport

13.3. Investment Trends in Cold Chain Infrastructure, 2018-“2024

13.4. Regulatory Requirements for Pharmaceutical and Food-Grade Storage

16.1. Benchmark of Key Competitors including Company Overview, Service Offerings, Infrastructure Footprint, Strategy, Sustainability Practices, and Technology Adoption

16.2. Strength and Weakness

16.3. Operating Model Analysis Framework

16.4. Gartner Magic Quadrant

16.5. Bowmans Strategic Clock for Competitive Advantage

17.1. Revenues, 2025-“2029

17.2. Freight Volume and Warehousing Capacity, 2025-“2029

18.1. By Market Structure (Organized and Unorganized Market), 2025-“2029

18.2. By Type of Warehousing (General, Cold Storage, Bonded, Automated), 2025-“2029

18.3. By Mode of Transport (Road, Rail, Sea, Air, Intermodal), 2025-“2029

18.4. By Region (Capital Region, Central Denmark, Southern Denmark, North Denmark, Zealand), 2025-“2029

18.5. By End-User Industry (Retail, Automotive, Pharma, FMCG, Industrial), 2025-“2029

18.6. Recommendation

18.7. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand side and supply side entities for Denmark Logistics and Warehousing Market. Basis this ecosystem, we will shortlist leading 5–6 logistics providers and warehousing operators in the country based on their revenue size, operational capacity, and service capabilities.

Sourcing is made through industry articles, multiple secondary, and proprietary databases to perform desk research around the market to collate industry-level information.

Step 2: Desk Research

Subsequently, we engage in an exhaustive desk research process by referencing diverse secondary and proprietary databases. This approach enables us to conduct a thorough analysis of the market, aggregating industry-level insights. We delve into aspects like revenue size, volume of goods handled, warehouse stock, number of logistics players, and modal share by transport type. We supplement this with detailed examinations of company-level data, relying on sources like press releases, annual reports, investor presentations, and government records. This process aims to construct a foundational understanding of both the market and the entities operating within it.

Step 3: Primary Research

We initiate a series of in-depth interviews with C-level executives and other stakeholders representing various Denmark logistics and warehousing companies, as well as large end-user industries such as e-commerce, automotive, FMCG, and pharma. This interview process serves a multi-faceted purpose: to validate market hypotheses, authenticate statistical data, and extract valuable operational and financial insights from these industry representatives. Bottom to top approach is undertaken to evaluate service volumes and warehousing capacity for each player, thereby aggregating to the overall market.

As part of our validation strategy, our team executes disguised interviews wherein we approach each company under the guise of potential customers. This approach enables us to validate the operational and financial information shared by company executives, corroborating this data against what is available in secondary databases. These interactions also provide us with a comprehensive understanding of value chain dynamics, pricing models, digital tools used, automation level, and sustainability initiatives.

Step 4: Sanity Check

- Bottom to top and top to bottom analysis along with market size modeling exercises is undertaken to assess sanity check process. Volume-revenue triangulation, year-on-year consistency checks, and segment-wise validations are conducted to ensure data accuracy.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Denmark logistics and warehousing market is poised for steady growth, reaching a valuation of DKK 54 Billion in 2023. This growth is driven by factors such as the country’s strategic location in Northern Europe, rising e-commerce activity, and government-led infrastructure investments. The market’s potential is further supported by Denmark’s advanced digital readiness and sustainability goals, which are accelerating the adoption of smart and green logistics solutions.

The Denmark logistics and warehousing market features several key players, including DSV, PostNord, Blue Water Shipping, and Frode Laursen. These companies dominate the market due to their strong operational capabilities, national and international coverage, and investments in automation and digital solutions. Other notable players include Bring, DB Schenker Denmark, and Danske Fragtmænd.

Key growth drivers include the rise of e-commerce and digital retail, which is increasing the demand for last-mile delivery and urban warehousing. Additionally, Denmark’s role as a logistics gateway for Northern Europe, supported by efficient sea and road transport networks, is fueling trade volume. The government's push for sustainable logistics practices and investments in cold chain and intermodal infrastructure further contribute to market expansion.

The Denmark logistics and warehousing market faces several challenges, including labor shortages in transport and warehousing operations, rising costs of industrial real estate in key hubs, and underdeveloped cold chain infrastructure in rural regions. Additionally, small and mid-sized logistics firms face difficulties adapting to new emission regulations and digital technologies due to limited resources.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0