Ethiopia Cold Chain Market Outlook to 2029

By Market Structure, By Service Type (Cold Storage, Cold Transport), By Temperature Type, By End-User Industries (FMCG, Pharmaceuticals, Agriculture), and By Region

Report Overview

Report Code

TDR0268

Coverage

Africa

Published

September 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Ethiopia Cold Chain Market Outlook to 2029 – By Market Structure, By Service Type (Cold Storage, Cold Transport), By Temperature Type, By End-User Industries (FMCG, Pharmaceuticals, Agriculture), and By Region” provides a comprehensive analysis of the cold chain logistics industry in Ethiopia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the Cold Chain Market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Ethiopia Cold Chain Market Outlook to 2029 – By Market Structure, By Service Type (Cold Storage, Cold Transport), By Temperature Type, By End-User Industries (FMCG, Pharmaceuticals, Agriculture), and By Region” provides a comprehensive analysis of the cold chain logistics industry in Ethiopia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer level profiling, issues and challenges, and comparative landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the Cold Chain Market. The report concludes with future market projections based on revenue, by market segment, temperature range, end-user industries, and success case studies highlighting the major opportunities and cautions.

Ethiopia Cold Chain Market Overview and Size

The Ethiopia cold chain market was valued at USD 240 million in 2023, driven by the rapid expansion of the agriculture and pharmaceutical sectors, rising demand for perishable food items, and increasing focus on healthcare logistics. The market is characterized by key players such as Ethio-Der, East Africa Cold Chain, Tena Cold Logistics, and government-backed warehousing projects under the Ethiopian Agricultural Transformation Agency (ATA). These entities are noted for their growing storage infrastructure, transport fleet enhancements, and service specialization.

In 2023, Ethio-Der introduced a new multi-temperature cold storage facility in Addis Ababa to cater to pharmaceutical and perishable food sectors. This move aligns with national objectives to reduce post-harvest losses and improve food security. Addis Ababa and Dire Dawa remain central hubs owing to their logistical connectivity and commercial demand.

%252C%25202019-2024.png&w=640&q=75)

What Factors are Leading to the Growth of Ethiopia Cold Chain Market:

Agriculture Export Push: Ethiopia’s strong focus on agricultural exports, especially horticulture and livestock, is driving the need for reliable cold chain infrastructure. In 2023, the horticulture sector alone grew by 14%, with refrigerated transport demand increasing accordingly. Cold chain logistics is vital for maintaining product quality during export, especially for flowers, fruits, and meat.

Healthcare and Pharma Demand: The increased demand for vaccine storage, particularly following pandemic-related pressures, and the growth of pharmaceutical imports have necessitated the development of temperature-sensitive logistics. By 2023, the pharmaceutical segment accounted for nearly 28% of cold chain volume movement in Ethiopia.

Infrastructure Investments: The Ethiopian government, in partnership with development organizations such as USAID and the World Bank, is investing in cold chain infrastructure to reduce post-harvest losses. Over USD 50 million was allocated to regional cold storage and rural last-mile connectivity initiatives in 2023.

Which Industry Challenges Have Impacted the Growth for Ethiopia Cold Chain Market

Limited Infrastructure Penetration: A significant challenge is the limited availability of temperature-controlled storage and transport infrastructure across rural and remote areas. As of 2023, over 60% of perishable goods in Ethiopia are transported through non-refrigerated means, leading to spoilage and inefficiencies. This infrastructure gap restricts the reach of cold chain services and limits market scalability, particularly for agricultural exports and pharmaceuticals.

High Operating Costs: The cost of setting up and maintaining cold storage facilities and refrigerated trucks remains prohibitively high due to inconsistent electricity supply and reliance on diesel generators. Energy costs alone contribute to over 40% of cold storage operational expenses. These elevated overheads often deter private sector investment and result in higher service costs for end-users.

Fragmented Supply Chain and Lack of Coordination: The cold chain market in Ethiopia is fragmented, with multiple small-scale operators lacking integration between storage and transportation services. This fragmentation leads to inefficiencies and product loss. In a recent logistics survey, it was found that approximately 35% of post-harvest losses in horticulture were attributable to delays and poor temperature control during transit.

What are the Regulations and Initiatives which have Governed the Market:

Cold Chain Policy Initiatives by Ministry of Agriculture: The Ethiopian Ministry of Agriculture, under the Agricultural Transformation Agenda, has prioritized the development of cold storage facilities and reefer logistics for horticulture and livestock exports. In 2023, the government introduced a national Cold Chain Development Framework aimed at reducing food losses and increasing export revenues.

Food and Drug Administration (EFDA) Guidelines for Pharmaceuticals: The Ethiopian Food and Drug Authority mandates strict storage and transportation regulations for vaccines, biologics, and temperature-sensitive medications. These guidelines require all licensed pharmaceutical distributors to maintain WHO-compliant cold storage and GPS-tracked cold transport vehicles. By 2023, compliance among licensed pharma logistics firms reached 82%.

Tax and Import Duty Exemptions on Cold Chain Equipment: To stimulate private investment, the Ethiopian government offers tax exemptions and import duty waivers on cold chain equipment including refrigeration units, insulated vehicles, and solar-powered systems. This policy, introduced in 2022, led to a 17% increase in cold storage capacity additions by 2023.

Ethiopia Cold Chain Market Segmentation

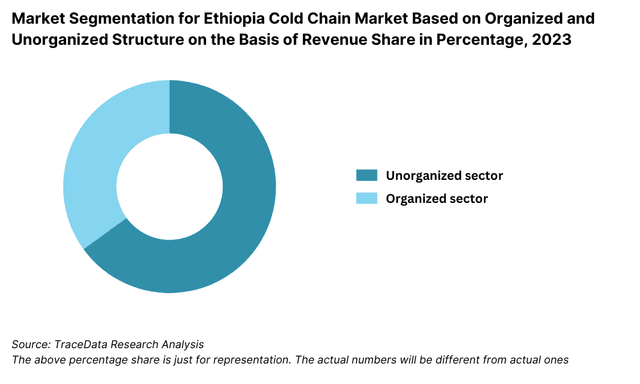

By Market Structure: The Ethiopian cold chain market is predominantly unorganized, comprising small-scale operators and informal players offering basic storage and transport services. These operators cater largely to local agriculture producers and small-scale traders. However, the organized segment is gradually expanding, driven by private sector investment, foreign aid-backed infrastructure projects, and compliance requirements from export-oriented industries. Organized players offer integrated cold logistics services with real-time temperature monitoring, certified storage facilities, and end-to-end logistics solutions.

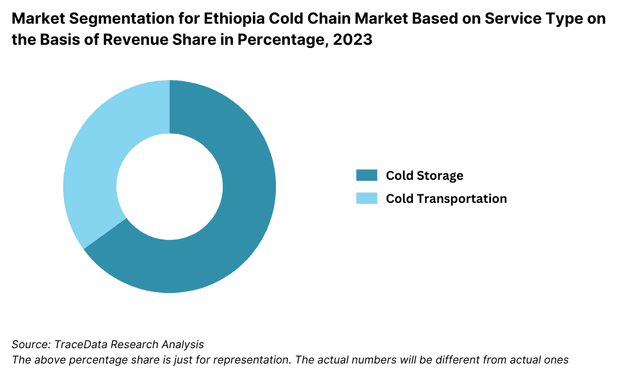

By Service Type (Cold Storage vs. Cold Transportation): Cold storage dominates the Ethiopian cold chain landscape due to high demand from horticulture exporters, dairy cooperatives, and pharmaceutical distributors. These facilities, concentrated in urban hubs like Addis Ababa, focus on multi-temperature warehousing. Cold transportation, while emerging, is still limited due to high operational costs and inadequate reefer truck penetration. Nonetheless, it is seeing increased adoption among large-scale exporters and pharmaceutical logistics providers.

By Temperature Range: The cold chain infrastructure in Ethiopia is primarily geared toward chilled storage (0°C to 8°C), used for dairy, fruits, vegetables, and vaccines. However, frozen storage (-18°C and below), critical for meat exports and certain pharmaceutical products, is gaining traction. Solar-powered and hybrid temperature solutions are being explored in rural zones with poor power access.

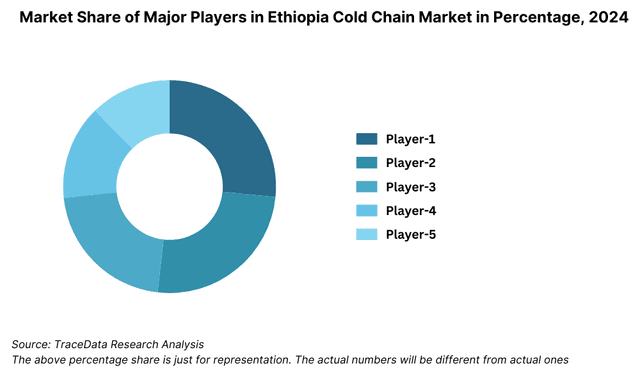

Competitive Landscape in Ethiopia Cold Chain Market

The Ethiopia cold chain market is moderately fragmented, with a mix of government-supported initiatives, local private players, and development-backed logistics providers. The market is witnessing increased participation from international development agencies and private logistics companies, contributing to modernizing cold storage and transport capabilities. Major players include Ethio-Der, Tena Cold Logistics, East Africa Cold Chain, and strategic public-private partnerships such as ATA Cold Chain Project and USAID-backed logistics hubs.

Company Name | Establishment Year | Headquarters |

Ethio-Der Cold Chain | 2012 | Addis Ababa, Ethiopia |

Tena Cold Logistics | 2016 | Addis Ababa, Ethiopia |

East Africa Cold Chain | 2014 | Dire Dawa, Ethiopia |

ATA Cold Chain Initiative | 2019 | Addis Ababa, Ethiopia |

MedTech Logistics | 2021 | Addis Ababa, Ethiopia |

Some of the recent competitor trends and key information about competitors include:

Ethio-Der Cold Chain: A leading cold storage provider in Ethiopia, Ethio-Der expanded its Addis Ababa facility in 2023 to include multi-temperature zones for both pharmaceuticals and perishables. It now services over 120 pharmaceutical distributors and agricultural exporters. The company is known for its solar-powered backup systems, reducing downtime and improving energy efficiency.

Tena Cold Logistics: Focused primarily on cold transportation, Tena Cold Logistics added 20 new refrigerated trucks to its fleet in 2023, enabling expanded services to secondary cities like Mekelle and Bahir Dar. The company specializes in last-mile cold transport for healthcare and food service industries.

East Africa Cold Chain: Operating mainly in eastern Ethiopia, the firm runs a network of cold rooms along major trade corridors. In 2023, it partnered with a Dutch agritech firm to launch Ethiopia’s first blockchain-enabled produce tracking system, improving traceability and compliance with export standards.

ATA Cold Chain Initiative: Backed by the Ethiopian Agricultural Transformation Agency and World Bank, this initiative aims to establish integrated cold hubs in rural farming zones. By 2023, it had operationalized 40 rural aggregation centers with chilled storage and solar-powered mini-grids, significantly reducing post-harvest losses for vegetables and dairy products.

MedTech Logistics: A newcomer specializing in pharma-grade cold chain services, MedTech Logistics operates under EFDA guidelines and serves hospitals, clinics, and importers. In 2023, it secured WHO-GDP certification, enabling it to transport vaccines, insulin, and other critical biologics nationwide.

What Lies Ahead for Ethiopia Cold Chain Market?

The Ethiopia cold chain market is projected to grow steadily through 2029, driven by rapid urbanization, rising demand for processed and perishable foods, growing pharmaceutical imports, and strong support from public and international development agencies. The market is expected to exhibit a healthy CAGR, with expansion opportunities across infrastructure, digitalization, and rural connectivity.

Expansion of Export-Oriented Cold Infrastructure: With Ethiopia’s increasing focus on agricultural exports—especially horticulture, meat, and dairy—there is expected to be substantial investment in export-grade cold storage hubs near major airports and dry ports. Strategic corridors like Addis Ababa–Modjo–Djibouti are likely to see accelerated cold chain expansion, reducing spoilage and enhancing global trade competitiveness.

Growth of Pharmaceutical Cold Chain Logistics: The demand for healthcare-related cold chain solutions is forecasted to rise, driven by increasing imports of temperature-sensitive medicines and vaccines. Ethiopia’s pharmaceutical supply chain is expected to adopt more advanced cold chain compliance technologies and WHO-certified facilities, supported by stricter EFDA enforcement.

Integration of Digital Monitoring and IoT Technologies: The use of digital temperature monitoring, GPS-enabled tracking, and IoT-based cold storage systems is anticipated to gain traction, especially among organized players. These technologies will enhance visibility, minimize losses, and improve regulatory compliance—key drivers for expansion among exporters and large FMCG clients.

Emergence of Solar-Powered Cold Chain Models: With electricity access being a constraint in rural Ethiopia, solar-powered cold storage and hybrid mobile refrigeration units are likely to play a pivotal role. These models, backed by donor programs and PPPs, will be critical for extending cold chain services to remote farming communities and improving last-mile delivery effectiveness.

%252C%25202024-2030.png&w=640&q=75)

Ethiopia Cold Chain Market Segmentation

• By Market Structure:

Public Cold Chain Infrastructure (Government & Development Agency Operated)

Private Cold Chain Providers

Integrated Logistics Players

Rural Aggregation Centers

Standalone Cold Storage Facilities

Reefer Transport Operators

Hybrid (Storage + Transport) Operators

• By Service Type:

Cold Storage

Cold Transportation

Integrated End-to-End Cold Chain Solutions

• By Temperature Range:

Chilled (0°C to 8°C)

Frozen (-18°C and below)

Ambient Controlled (15°C to 25°C – Pharma-specific)

• By End-User Industry:

Agriculture (Fruits, Vegetables, Dairy, Meat)

Pharmaceuticals and Life Sciences

Food Processing and FMCG

Hospitality and HoReCa Sector

Importers & Exporters

Retail Chains and Supermarkets

• By Region:

Addis Ababa (Capital & Commercial Hub)

Oromia (Agricultural Belt)

Amhara (North-Central Zone)

SNNPR (Southern Nations)

Tigray (Northern Corridor)

Dire Dawa & Harar (Eastern Trade Gateways)

Players Mentioned in the Report:

Ethio-Der Cold Chain

Tena Cold Logistics

East Africa Cold Chain

ATA Cold Chain Initiative

MedTech Logistics

USAID Cold Chain Projects

World Bank-Backed Infrastructure Programs

Key Target Audience:

Cold Chain Operators

Exporters and Agro-Processing Units

Pharmaceutical Distributors

Food & Beverage Manufacturers

Government Ministries (e.g., Ministry of Agriculture, EFDA)

Development Agencies and Donor Institutions

Logistics and Infrastructure Investors

Technology Providers (IoT, Monitoring Systems)

Time Period:

Historical Period: 2018–2023

Base Year: 2024

Forecast Period: 2024–2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-“ Role of Entities, Stakeholders, and challenges that they face

4.2. Revenue Streams for Ethiopia Cold Chain Market

4.3. Business Model Canvas for Ethiopia Cold Chain Market

4.4. Service Decision Making Process

4.5. Supply Chain Partner Decision Process

5.1. Cold Storage Facilities by Region and Type (Chilled/Frozen), 2018-“2024

5.2. Reefer Vehicle Penetration by Fleet Size and Ownership, 2018-“2024

5.3. Government & Donor Funding for Cold Chain Infrastructure, 2020-“2024

5.4. Distribution of Cold Chain Operators by Scale and Region

6. Market Attractiveness for Ethiopia Cold Chain Market

8.1. Revenues, 2018-“2024

8.2. Storage Capacity and Reefer Transport Volume, 2018-“2024

9.1. By Market Structure (Organized and Unorganized Market), 2023-“2024P

9.2. By Service Type (Cold Storage vs. Cold Transportation), 2023-“2024P

9.3. By Temperature Range (Chilled, Frozen, Ambient Controlled), 2023-“2024P

9.4. By End-User Industry (Agriculture, Pharmaceuticals, FMCG, etc.), 2023-“2024P

9.5. By Region (Addis Ababa, Oromia, Amhara, SNNPR, etc.), 2023-“2024P

10.1. Customer Landscape and Industry-wise Adoption

10.2. Decision Journey for Cold Chain Logistics Selection

10.3. Service Needs and Pain Points

10.4. Gap Analysis Framework

11.1. Trends and Developments for Ethiopia Cold Chain Market

11.2. Growth Drivers for Ethiopia Cold Chain Market

11.3. SWOT Analysis for Ethiopia Cold Chain Market

11.4. Issues and Challenges for Ethiopia Cold Chain Market

11.5. Government Regulations and Support Policies for Cold Chain Development

12.1. Role of IoT and Remote Monitoring in Ethiopia Cold Chain

12.2. Emerging Technology Startups and Pilot Projects

12.3. Cross Comparison of Cold Chain Tech Vendors in Ethiopia

13.1. Role of Development Finance Institutions (DFIs) and Donor Agencies

13.2. PPP Projects and Capital Allocation Trends

13.3. Private Investment in Cold Chain Infrastructure

13.4. Microfinancing and Cooperative-Based Cold Chain Models

16.1. Benchmark of Key Competitors including Company Overview, Capacity, Technology Adoption, Pricing Models, Region Served, Value-Added Services

16.2. Strength and Weakness

16.3. Operating Model Analysis Framework

16.4. Gartner Magic Quadrant

16.5. Bowmans Strategic Clock for Competitive Advantage

17.1. Revenues, 2025-“2029

17.2. Storage Capacity and Reefer Transport Volume, 2025-“2029

18.1. By Market Structure (Organized and Unorganized Market), 2025-“2029

18.2. By Service Type (Cold Storage vs. Cold Transportation), 2025-“2029

18.3. By Temperature Range (Chilled, Frozen, Ambient Controlled), 2025-“2029

18.4. By End-User Industry (Agriculture, Pharmaceuticals, FMCG, etc.), 2025-“2029

18.5. By Region (Addis Ababa, Oromia, Amhara, SNNPR, etc.), 2025-“2029

18.6. Recommendation

18.7. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand side and supply side entities for Ethiopia Cold Chain Market. Basis this ecosystem, we will shortlist leading 5-6 service providers in the country based upon their financial information, cold storage and transportation capacity/volume.

Sourcing is made through industry articles, multiple secondary, and proprietary databases to perform desk research around the market to collate industry-level information.

Step 2: Desk Research

Subsequently, we engage in an exhaustive desk research process by referencing diverse secondary and proprietary databases. This approach enables us to conduct a thorough analysis of the market, aggregating industry-level insights. We delve into aspects like the revenue size, cold storage and transport capacities, number of market players, price levels, demand by end-user sectors, and other variables. We supplement this with detailed examinations of company-level data, relying on sources like press releases, annual reports, development partner documentation, and similar documents. This process aims to construct a foundational understanding of both the market and the entities operating within it.

Step 3: Primary Research

We initiate a series of in-depth interviews with C-level executives and other stakeholders representing various Ethiopia Cold Chain Market companies and end-users. This interview process serves a multi-faceted purpose: to validate market hypotheses, authenticate statistical data, and extract valuable operational and financial insights from these industry representatives. Bottom to top approach is undertaken to evaluate volume capacities for each player thereby aggregating to the overall market.

As part of our validation strategy, our team executes disguised interviews wherein we approach each company under the guise of potential customers. This approach enables us to validate the operational and financial information shared by company executives, corroborating this data against what is available in secondary databases. These interactions also provide us with a comprehensive understanding of revenue streams, value chain, process, pricing, and other factors.

Step 4: Sanity Check

- Bottom to top and top to bottom analysis along with market size modeling exercises is undertaken to assess sanity check process.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Ethiopia cold chain market is poised for strong growth, reaching a valuation of USD 240 million in 2023. This growth is being fueled by the country’s focus on agricultural exports, the rising demand for temperature-sensitive pharmaceuticals, and the modernization of retail and food service supply chains. Increased investments from both government and international agencies further enhance the market’s long-term potential, particularly in rural and underserved regions.

The Ethiopia Cold Chain Market features several key players, including Ethio-Der, Tena Cold Logistics, and East Africa Cold Chain. These companies are recognized for their specialized service offerings, expanding cold storage infrastructure, and growing regional presence. Other notable players and initiatives include MedTech Logistics and the ATA Cold Chain Project, supported by government and development institutions.

The main growth drivers include the need to reduce post-harvest losses in agriculture, rising pharmaceutical imports requiring cold storage, and the expansion of organized retail and FMCG distribution. Additionally, policy support from the Ethiopian government and multilateral aid for logistics infrastructure is playing a crucial role. The increasing adoption of solar-powered and tech-enabled cold chain solutions is also boosting operational efficiency and scalability.

The Ethiopia Cold Chain Market faces several challenges, including limited cold storage capacity outside of major urban centers, high energy and operational costs, and a shortage of trained personnel in cold chain management. Fragmented supply chains, unreliable electricity, and inadequate integration between storage and transport also pose major hurdles. Despite these challenges, continued investment and innovation are expected to address infrastructure and service delivery gaps in the coming years.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0