Ethiopia Logistics and Warehousing Market Outlook to 2029

- By Market Structure, By Manufacturers, By Types of Warehouses, By Logistics Services, By Regions and By Key Stakeholders

Report Overview

Report Code

TDR0269

Coverage

Africa

Published

September 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Ethiopia Logistics and Warehousing Market Outlook to 2029 - By Market Structure, By Manufacturers, By Types of Warehouses, By Logistics Services, By Regions and By Key Stakeholders” provides a comprehensive analysis of the logistics and warehousing market in Ethiopia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer-level profiling, issues and challenges, and a comparative landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the Logistics and Warehousing Market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Ethiopia Logistics and Warehousing Market Outlook to 2029 - By Market Structure, By Manufacturers, By Types of Warehouses, By Logistics Services, By Regions and By Key Stakeholders” provides a comprehensive analysis of the logistics and warehousing market in Ethiopia. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer-level profiling, issues and challenges, and a comparative landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the Logistics and Warehousing Market. The report concludes with future market projections based on sales revenue, by market, logistics services, region, cause and effect relationships, and success case studies highlighting the major opportunities and cautions.

Ethiopia Logistics and Warehousing Market Overview and Size

The Ethiopia logistics and warehousing market reached a valuation of ETB 35 Billion in 2023, driven by increasing trade activity, infrastructural improvements, and the growing demand for efficient transportation and storage solutions. The market is characterized by key players such as Ethiopian Cargo & Logistics Services, TransEthiopia, and Sky Freight Logistics, among others. These companies have established robust networks to facilitate both domestic and international logistics services.

The Ethiopian government’s investment in infrastructure, including roads, rail, and ports, has significantly contributed to the market’s growth. Notably, the expansion of the Addis Ababa-Djibouti Railway has eased cross-border logistics, creating a more efficient flow of goods to and from the port of Djibouti, Ethiopia's primary gateway for imports and exports.

In 2023, Ethiopian Cargo & Logistics Services further streamlined its operations by implementing new digital solutions, such as online tracking systems and automated warehousing, enhancing operational efficiency and reducing delivery times. The regions surrounding Addis Ababa, such as Oromia and Amhara, are seeing a rapid increase in logistics activity due to improved connectivity and industrialization.

%252C%25202019-2024.png&w=640&q=75)

What Factors are Leading to the Growth of Ethiopia Logistics and Warehousing Market:

Economic Factors: Ethiopia's growing economy, particularly in the manufacturing and agricultural sectors, has increased the demand for logistics and warehousing services. In 2023, logistics services accounted for approximately 40% of the country’s GDP, reflecting the importance of an efficient supply chain. The expansion of industrial parks, such as the Hawassa Industrial Park, has led to a higher demand for both domestic and international logistics solutions.

Infrastructure Development: Significant investments in transportation infrastructure, including roads, railways, and ports, are fostering growth in logistics. The launch of the Addis Ababa-Djibouti Railway has significantly cut down transportation costs, contributing to a more efficient logistics system. The Ethiopian government’s continued efforts to improve infrastructure are expected to further drive market growth.

Digital Transformation: The logistics industry is experiencing a digital transformation, with increasing adoption of technologies like GPS tracking, automated warehousing, and e-commerce logistics solutions. In 2023, around 30% of logistics transactions in Ethiopia were processed digitally, significantly improving service efficiency and customer experience.

Which Industry Challenges Have Impacted the Growth for Ethiopia Logistics and Warehousing Market?

Infrastructure Limitations: Despite significant investments in infrastructure, Ethiopia still faces challenges related to the quality and accessibility of roads, railways, and ports, especially in remote areas. The expansion of the Addis Ababa-Djibouti Railway has alleviated some issues; however, in 2023, nearly 25% of rural areas remained underserved by major logistics networks, limiting the reach of distribution hubs. This lack of infrastructure, particularly in rural regions, impedes the efficient movement of goods.

Regulatory and Bureaucratic Hurdles: The logistics and warehousing industry is hampered by bureaucratic inefficiencies, especially in customs and border control processes. In 2023, around 18% of shipments faced delays due to slow customs clearance procedures, affecting the timely delivery of goods. These regulatory delays can increase costs and reduce the overall competitiveness of Ethiopian logistics services.

Skilled Workforce Shortage: The logistics industry in Ethiopia faces a shortage of skilled labor, including warehousing and supply chain management professionals. This gap affects operational efficiency, particularly in the implementation of advanced technologies like automated warehousing and GPS tracking systems. Approximately 30% of logistics companies in Ethiopia reported difficulties in finding qualified staff, which has led to slower adoption of modern logistics practices.

What are the Regulations and Initiatives Which Have Governed the Market?

Logistics Licensing and Safety Standards: The Ethiopian government mandates that all logistics and warehousing companies must be licensed by the Ministry of Transport and comply with specific safety and environmental standards. These regulations aim to ensure that storage facilities meet the required structural and safety specifications. In 2023, about 80% of warehouses in Ethiopia were compliant with the necessary fire and safety regulations.

Incentives for Logistics Infrastructure Development: To boost the logistics sector, the Ethiopian government has introduced tax incentives and grants for companies investing in logistics infrastructure, including warehousing facilities and cold-storage solutions. In 2023, companies in the logistics sector benefitted from tax exemptions on capital investments in warehouses, encouraging the establishment of modern logistics parks.

E-commerce and Last-Mile Delivery Regulations: As the e-commerce market in Ethiopia grows, the government has begun regulating the last-mile delivery sector, focusing on transportation and delivery speed. In 2023, regulations were introduced that required logistics companies to provide tracking capabilities and set delivery timeframes for e-commerce shipments, ensuring transparency and customer satisfaction.

Ethiopia Logistics and Warehousing Market Segmentation

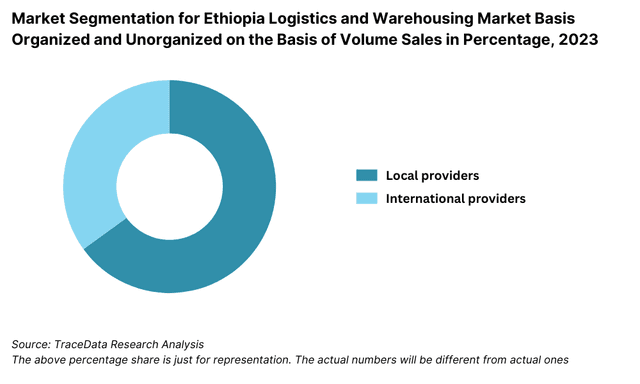

By Market Structure: The Ethiopian logistics and warehousing market is predominantly dominated by local logistics providers due to their deep understanding of local geography, customer needs, and regional supply chain demands. These local players have established networks and offer flexible solutions, especially in urban areas like Addis Ababa. On the other hand, international logistics companies such as DHL and Maersk hold a significant share in the market, offering advanced technologies, global reach, and higher service standards that cater to the needs of multinational companies and large-scale industries.

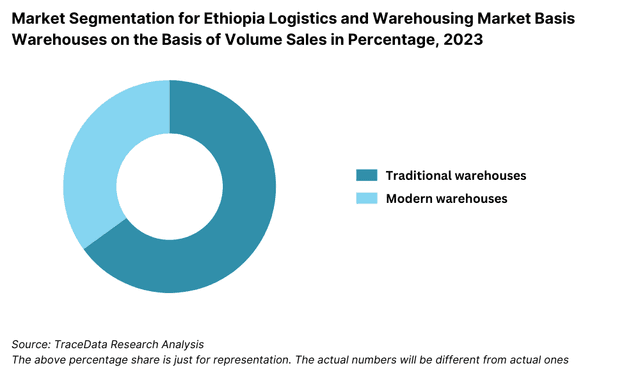

By Type of Warehouses: The warehousing market in Ethiopia is divided into two main categories: traditional warehouses and modern, automated warehouses. Traditional warehouses are primarily used by local businesses for storage, typically located in urban areas. They offer basic storage solutions without advanced technologies. Modern warehouses, on the other hand, are increasingly being adopted by multinational companies and large retailers due to the growing demand for high-efficiency logistics solutions. These warehouses are equipped with automation, inventory management systems, and temperature control facilities, particularly important for industries such as food and pharmaceuticals.

By Logistics Services: In Ethiopia, transportation services dominate the logistics segment, with road transport accounting for a significant portion of the market. The ongoing expansion of the road network, including projects like the Addis Ababa ring road, has bolstered road freight efficiency. Rail transport, primarily through the Addis Ababa-Djibouti Railway, plays a growing role in cross-border logistics. Warehousing services are also seeing an uptick, especially for goods that require specialized storage, such as perishable items or pharmaceuticals.

Competitive Landscape in Ethiopia Logistics and Warehousing Market

The Ethiopian logistics and warehousing market is moderately concentrated, with a few key players leading the industry. However, the growing demand for logistics services and the rise of new digital platforms and e-commerce businesses have diversified the market, offering more choices and services to consumers.

Company | Establishment Year | Headquarters |

Ethiopian Cargo & Logistics Services | 1945 | Addis Ababa, Ethiopia |

TransEthiopia | 2000 | Addis Ababa, Ethiopia |

Sky Freight Logistics | 2005 | Addis Ababa, Ethiopia |

DHL Ethiopia | 2008 | Addis Ababa, Ethiopia |

Maersk Ethiopia | 2010 | Addis Ababa, Ethiopia |

Some of the recent competitor trends and key information about competitors include:

Ethiopian Cargo & Logistics Services: As the state-owned logistics service provider, Ethiopian Cargo & Logistics Services recorded significant growth in 2023, handling over 150,000 metric tons of air cargo. The company is investing in technology to streamline its operations, with a focus on digital tracking systems and automated warehousing. In 2023, the company expanded its reach to 10 new countries in Africa, increasing its market presence.

TransEthiopia: A major player in road freight and warehousing, TransEthiopia reported a 20% increase in sales in 2023. The company is expanding its warehouse capacity in key cities like Addis Ababa, Bahir Dar, and Hawassa. TransEthiopia's investment in training and technology has helped the company maintain a competitive edge, particularly in the growing demand for refrigerated storage and handling.

Sky Freight Logistics: Specializing in international and domestic freight forwarding, Sky Freight Logistics saw a 15% growth in the volume of goods handled in 2023. The company has made significant strides in digitalizing its operations, integrating e-commerce logistics and offering last-mile delivery services, which have been well-received in the growing e-commerce sector in Ethiopia.

DHL Ethiopia: DHL has strengthened its position in Ethiopia with enhanced warehousing and delivery capabilities. In 2023, DHL reported a 30% increase in the volume of parcels handled, primarily driven by e-commerce growth. The company is focused on expanding its distribution network, with plans to add new distribution centers in underserved regions.

Maersk Ethiopia: As a major global logistics provider, Maersk has expanded its services in Ethiopia, focusing on container shipping and port logistics. Maersk has been instrumental in driving the growth of rail freight through the Addis Ababa-Djibouti Railway, and it recorded a 10% increase in its logistics volumes in 2023. The company has also introduced more digital solutions, improving supply chain visibility and tracking for clients in Ethiopia.

What Lies Ahead for Ethiopia Logistics and Warehousing Market?

The Ethiopia logistics and warehousing market is projected to grow steadily by 2029, exhibiting a respectable CAGR during the forecast period. This growth is expected to be fueled by infrastructure development, increasing trade, and rising consumer demand for efficient logistics and warehousing solutions.

Expansion of E-Commerce Logistics: As Ethiopia's e-commerce sector continues to grow, there will be an increasing demand for efficient last-mile delivery and warehousing services. The rise of online shopping, coupled with the expanding middle class, will push the need for more specialized logistics services, including cold-chain logistics and distribution networks in urban and remote areas.

Development of Smart Warehousing: The adoption of smart warehousing technologies, including automation, AI-driven inventory management, and IoT-based tracking, is expected to revolutionize the logistics sector. These technologies will streamline operations, reduce costs, and improve service levels, making Ethiopia's logistics services more competitive in the region.

Government Investments in Infrastructure: The Ethiopian government’s continued investment in transport infrastructure, particularly in roads, rail, and ports, will enhance the efficiency of the logistics and warehousing industry. Projects like the expansion of the Addis Ababa-Djibouti Railway and improvements to the ports of Djibouti will foster smoother cross-border trade, driving growth in both domestic and international logistics services.

Focus on Sustainability: As global supply chains increasingly demand more sustainable practices, the Ethiopian logistics and warehousing market is likely to follow suit. This includes the adoption of eco-friendly vehicles, energy-efficient warehouse designs, and sustainable packaging solutions. The growing consumer preference for environmentally responsible practices will drive companies to adopt green logistics strategies.

%252C%25202024-2030.png&w=640&q=75)

Ethiopia Logistics and Warehousing Market Segmentation

• By Market Structure:

Public Logistics Providers

Private Logistics Providers

International Freight Forwarders

Local Freight Forwarders

Organized Sector

Unorganized Sector

Warehousing Operators (Traditional and Automated)

E-Commerce Logistics Service Providers

• By Logistics Service:

Road Transport

Rail Transport

Air Freight

Sea Freight

Warehousing Services

Cold-Chain Logistics

Last-Mile Delivery Services

Freight Forwarding

• By Type of Warehouses:

Traditional Warehouses

Modern Automated Warehouses

Temperature-Controlled Warehouses (Cold Chain)

E-Commerce Fulfillment Centers

Distribution Centers

• By Region:

Addis Ababa

Oromia

Amhara

Tigray

Southern Nations, Nationalities, and Peoples' Region (SNNPR)

Afar

Harari

Players Mentioned in the Report:

Ethiopian Cargo & Logistics Services

TransEthiopia

Sky Freight Logistics

DHL Ethiopia

Maersk Ethiopia

CMA CGM Ethiopia

FedEx Ethiopia

Key Target Audience:

Logistics Service Providers

Warehousing and Distribution Centers

Freight Forwarders

E-Commerce Companies

Government Agencies (Ministry of Transport, Ethiopian Shipping and Logistics Services Enterprise)

Supply Chain Management Companies

International Trade Bodies

Time Period:

Historical Period: 2018-2023

Base Year: 2024

Forecast Period: 2024-2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-Role of Entities, Stakeholders, and Challenges They Face

4.2. Revenue Streams for Ethiopia Logistics and Warehousing Market

4.3. Business Model Canvas for Ethiopia Logistics and Warehousing Market

4.4. Logistics Decision-Making Process

4.5. Warehousing Decision-Making Process

5.1. Growth of Logistics Infrastructure in Ethiopia, 2018-2024

5.2. Logistics: Organized vs. Unorganized Market, 2018-2024

5.3. Spend on Transportation and Logistics Services in Ethiopia, 2024

5.4. Number of Logistics Providers by Region in Ethiopia

8.1. Revenues, 2018-2024

8.2. Volume of Goods Handled, 2018-2024

9.1. By Market Structure (Organized and Unorganized Market), 2023-2024P

9.2. By Type of Logistics Service (Road, Rail, Air, Sea, Warehousing), 2023-2024P

9.3. By Region, 2023-2024P

9.4. By Type of Warehouses (Traditional vs. Automated), 2023-2024P

9.5. By Warehousing Services (Cold-Chain, General, Specialized), 2023-2024P

10.1. Customer Landscape and Cohort Analysis

10.2. Customer Journey and Decision-Making Process

10.3. Logistics Needs, Desires, and Pain Points

10.4. Gap Analysis Framework

11.1. Trends and Developments for Ethiopia Logistics and Warehousing Market

11.2. Growth Drivers for Ethiopia Logistics and Warehousing Market

11.3. SWOT Analysis for Ethiopia Logistics and Warehousing Market

11.4. Challenges in the Ethiopia Logistics and Warehousing Market

11.5. Government Regulations for Ethiopia Logistics and Warehousing Market

12.1. Market Size and Future Potential for Digital Logistics Services, 2018-2029

12.2. Business Models and Revenue Streams for Online Logistics Providers

12.3. Cross Comparison of Leading Online Logistics and Warehousing Companies

13. Ethiopia Logistics and Warehousing Financing Market

13.1. Finance Penetration Rate and Average Down Payment for Logistics Services, 2018-2029

13.2. Finance Penetration Trends and Their Impact on Market Growth

13.3. Types of Logistics Services with Higher Finance Penetration

13.4. Financing Distribution for Logistics Services (Banks, NBFCs, Private Financing), 2023-2024P

16.1. Benchmark of Key Competitors in Ethiopia Logistics and Warehousing Market

16.2. Strength and Weakness Analysis of Key Competitors

16.3. Operating Model Analysis Framework

16.4. Gartner Magic Quadrant for Logistics and Warehousing Providers

16.5. Bowmans Strategic Clock for Competitive Advantage in Logistics

17.1. Revenues, 2025-2029

17.2. Volume of Goods Handled, 2025-2029

18.1. By Market Structure (Organized and Unorganized Market), 2025-2029

18.2. By Type of Logistics Service (Road, Rail, Air, Sea, Warehousing), 2025-2029

18.3. By Region, 2025-2029

18.4. By Type of Warehouses (Traditional vs. Automated), 2025-2029

18.5. By Warehousing Services (Cold-Chain, General, Specialized), 2025-2029

18.6. By E-Commerce Logistics Services, 2025-2029

18.7. By Financing Options in Logistics, 2025-2029

18.8. Recommendations and Opportunity Analysis for Ethiopia Logistics and Warehousing Market

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities for the Ethiopia Logistics and Warehousing Market. Based on this ecosystem, we will shortlist the leading 5-6 logistics and warehousing providers in the country based on their financial information, service capacity, market share, and technological adoption.

Sourcing is conducted through industry reports, government publications, and proprietary databases to gather market insights and create a comprehensive ecosystem for analysis.

Step 2: Desk Research

We engage in exhaustive desk research by referring to secondary data sources such as government reports, logistics industry publications, and proprietary market intelligence databases. This helps in collecting industry-level data on market size, demand patterns, and trends. Key variables such as market revenues, volume of logistics operations, infrastructure development, and market growth drivers are examined in detail.

Additionally, we analyze company-level data including annual reports, press releases, and other financial statements of major logistics and warehousing companies to gain insights into their operations, capacity, and strategic positioning.

Step 3: Primary Research

We initiate in-depth interviews with senior executives, operations managers, and key stakeholders in the Ethiopia logistics and warehousing industry. This primary research phase validates market hypotheses, ensures the accuracy of secondary data, and provides operational insights. Interviews are conducted with logistics providers, warehousing operators, and key clients such as e-commerce businesses, retail distributors, and manufacturing companies.

In addition, we conduct “disguised interviews,” approaching companies under the guise of potential clients to cross-check the financial and operational information shared by company representatives. This process helps validate pricing models, service offerings, and client satisfaction levels.

Step 4: Sanity Check

- A thorough sanity check is performed through both top-to-bottom and bottom-to-top analyses. Market size models are built to verify the accuracy of assumptions and data collected from primary and secondary research. This involves comparing data points from interviews, company reports, and industry statistics to ensure consistency and validity of findings.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Ethiopia logistics and warehousing market is poised for steady growth, reaching a projected valuation of ETB 70 Billion by 2029. This growth is driven by infrastructure development, the rise of e-commerce, and increased demand for efficient transportation and storage solutions. The expansion of road, rail, and port infrastructure, along with the adoption of smart warehousing technologies, will further accelerate market growth.

Key players in the Ethiopia logistics and warehousing market include Ethiopian Cargo & Logistics Services, TransEthiopia, Sky Freight Logistics, DHL Ethiopia, and Maersk Ethiopia. These companies dominate the market with their extensive service offerings in air freight, road transport, and warehousing. Other notable players include FedEx Ethiopia and CMA CGM Ethiopia.

The primary growth drivers for the Ethiopia logistics and warehousing market include the ongoing improvements in infrastructure, such as the Addis Ababa-Djibouti Railway and the expansion of port facilities. The rise of e-commerce and the growing demand for efficient supply chain solutions also contribute to market growth. Additionally, government incentives for logistics infrastructure development and the increasing adoption of smart warehousing technologies will further stimulate market expansion.

The Ethiopia logistics and warehousing market faces challenges such as inadequate infrastructure in rural areas, leading to inefficiencies in last-mile delivery. Regulatory and bureaucratic hurdles in customs clearance can also result in delays, impacting the efficiency of logistics operations. Furthermore, the shortage of skilled labor in logistics and warehousing operations presents a barrier to the adoption of modern technologies and efficient operational practices.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0