Malaysia Medical Tourism Market Outlook to 2029

By Market Structure, By Treatments, By Patient Demographics, By Country of Origin, By Revenue Streams, and By Region

Report Overview

Report Code

TDR0093

Coverage

Asia

Published

December 2024

Pages

80-100

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Malaysia Medical Tourism Market Outlook to 2029 - By Market Structure, By Treatments, By Patient Demographics, By Country of Origin, By Revenue Streams, and By Region” provides a comprehensive analysis of the medical tourism market in Malaysia. The report covers a glimpse and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, patient-level profiling, issues and challenges, and comparative landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the Medical Tourism Market.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Malaysia Medical Tourism Market Outlook to 2029 - By Market Structure, By Treatments, By Patient Demographics, By Country of Origin, By Revenue Streams, and By Region” provides a comprehensive analysis of the medical tourism market in Malaysia. The report covers a glimpse and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, patient-level profiling, issues and challenges, and comparative landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major players in the Medical Tourism Market. The report concludes with future market projections based on revenue, patient inflow, region, cause and effect relationship, and success case studies highlighting the major opportunities and cautions.

Overview of Malaysia and Size of its Medical Tourism Market

The Malaysia medical tourism market reached a valuation of MYR 7.5 Billion in the year 2023. This is attributed to the higher inflow of international patients and the strategic support by governments for quality and affordable treatment, among other factors related to Malaysia's established healthcare structure. Major players associated with the market include KPJ Healthcare Berhad, IHH Healthcare Berhad, Prince Court Medical Centre, Gleneagles Hospitals, and Sunway Medical Centre. These are institutions renowned for their state-of-the-art medical facilities, reasonably priced, and patient-oriented services.

Malaysia Healthcare Travel Council introduced an enhanced digital platform in 2023 that would grease the wheels for patients to access medical services and get connected with accredited healthcare providers with much more ease. Kuala Lumpur, Penang, and Johor Bahru are the focus markets because of the dense population of high-class hospitals and accessibility by neighboring countries.

Market Size for Malaysia Medical Tourism Industry on the Basis of Revenues in USD Billion, 2018-2024

Factors contributing to the growth of Malaysia medical tourism market include:

- Cost-Effectiveness: Medical treatment in Malaysia is much cheaper compared to Western countries. Considering cardiac surgery, orthopedic surgery, cosmetic treatments, and other procedures, some patients can save up to 60%-70% of the cost. Savings, together with high value, make Malaysia an impressive destination for medical tourists.

- Advanced Infrastructure for Healthcare: Malaysia has the best, if not one of the finest, complete healthcare systems in Asia, having internationally accredited hospitals with state-of-the-art facilities and skilled doctors. By 2023, Malaysia had more than 70 JCI accredited hospitals contributing to the country's reputation internationally.

- Strategic Location and Connectivity: Strategic location and connectivity in the neighborhood of main markets like Indonesia, China, Singapore, and the Middle East make Malaysia easy to access for tourists to visit medical facilities. It has a Kuala Lumpur International Airport that serves as an important entry point with millions of international visitors' arrival each year.

Which Industry Challenges Have Impacted the Growth of Malaysia Medical Tourism Market?

- Quality of Care and Trust Issues: Issues relating to the quality of treatment and trust in foreign health-care providers have been major growth inhibitors. An industry survey has shown that about 35% of international patients do not travel because they fear misdiagnosis or second-class facilities. These have kept the potential medical tourist wary, thereby possibly holding back patient inflow by up to 18%.

- Regulatory Barriers: Strict visa and travel rules, along with medical licensing restrictions for international patients, create barriers to treatment in Malaysia. In 2013, about 15% of the patients were delayed or canceled due to bureaucratic concern. These often result in impacts on the ease and appeal of Malaysia as a medical tourism destination.

- Competition Intensity: Malaysia faces high competition especially from the hubs in Thailand, Singapore, and India. Similar services have come up in these countries and most of these countries put a lot of effort into marketing and promoting their sector. Malaysia was estimated to capture just 6% share of the total medical tourism market in Southeast Asia due to the competition in the year 2023.

What are the Regulations and Initiatives that Have Governed the Market

- Accreditation and Licensing: In Malaysia, the government strictly follows the standards of providing accreditation and licensing to medical facilities for international patients. The hospitals should address the Ministry of Health requirements and achieve international certifications like Joint Commission International. More than 70 hospitals and clinics gained JCI accreditation in Malaysia during 2023, ensuring compliance with global standards.

- Medical Tourism Visa Policies: To promote the same, the government has a special visa that accommodates the patients and even companions of the patients quickly. In 2023, it is estimated that around 85% availed themselves of the facilitation provided by fast-tracked visa processing, in turn lessening the bureaucracy involved and smoothing the patient's journey.

- Health Travel Council Initiatives: Malaysia Healthcare Travel Council, or MHTC, is the key player that drives the sector. Its major initiatives include developing the "Malaysia Healthcare Brand" and collaboration with airlines, travel agencies, and insurance companies for package deals. In 2023, these initiatives increased patient inflow by 12%, and the council also supported digital transformation for healthcare access.

Malaysia Medical Tourism Market Segmentation

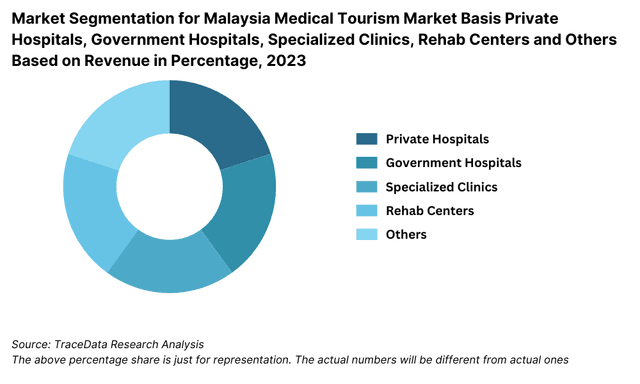

- By Market Structure: The private hospitals dominate the market with their advanced infrastructure, internationally accredited facilities, and patient-centered services. They attract a substantial share of international patients who aim for quality care and waiting times. The government subsidiary hospitals usually complement the private ones, especially for regional medical tourists, through the provision of relatively cheap treatment with experienced medical professionals. Specialized medical centers are also cropping up as major players, targeting niche markets like fertility treatments, cardiology, and orthopedics.

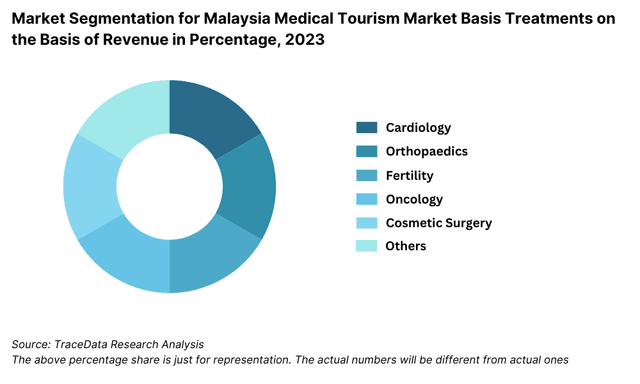

- By Treatment Type: The Malaysian medical tourism market is dominated by cardiology and orthopedics, as Malaysia enjoys a good reputation in these specialties, and also advanced surgical procedures are available at competitive prices. Cosmetic surgery is another significant segment that is driven by the rising demand for aesthetic procedures in markets such as Indonesia, China, and the Middle East. Fertility treatments also represent another growing segment, in part due to the affordable options available in Malaysia, commensurate with success rates from the West.

- By Country of Origin: Geographically, foreign patients come in the biggest chunk from Indonesia because of closeness, cultural affinity, and competitive pricing. Coming next are China and the Middle East, which accounts for Malaysia's good health facilities amalgamated with the country's recognition and status as a '_halal' hub; naturally, this would appeal to many visiting Muslims. European and US patients number fewer but are getting quite significant, given their appreciation for value for money during procedures and mostly merged into leisure travel.

Competitive Landscape in Malaysia Medical Tourism Market

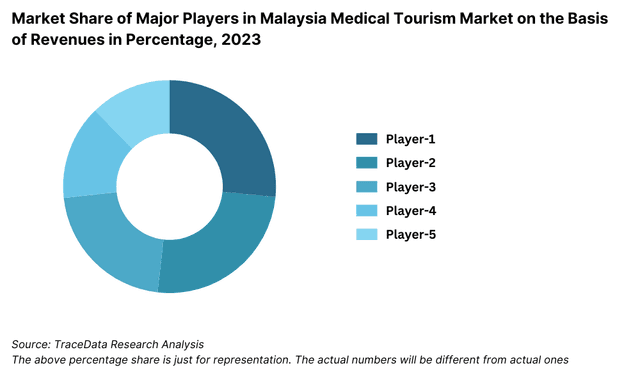

The Malaysia medical tourism market is moderately concentrated, with a few major players leading the industry while several specialized providers and emerging players contribute to the diversity of services. Key players include KPJ Healthcare Berhad, IHH Healthcare Berhad (Parkway Pantai), Prince Court Medical Centre, Gleneagles Hospitals, and Sunway Medical Centre. These institutions are recognized for their international accreditations, advanced facilities, and strong marketing strategies targeting global patients.

Hospital Name | Establishment Year | Location |

|---|---|---|

Prince Court Medical Centre | 2007 | Kuala Lumpur |

Gleneagles Hospital Kuala Lumpur | 1996 | Kuala Lumpur |

Sunway Medical Centre | 1999 | Selangor |

Penang Adventist Hospital | 1924 | Penang |

Island Hospital | 1996 | Penang |

KPJ Healthcare Berhad | 1981 | Kuala Lumpur |

Pantai Hospital Kuala Lumpur | 1974 | Kuala Lumpur |

Mahkota Medical Centre | 1994 | Malacca |

Beverly Wilshire Medical Centre | 2012 | Kuala Lumpur |

Institut Jantung Negara (National Heart Institute) | 1992 | Kuala Lumpur |

Some of the Recent Competitor Trends and Key Information About Competitors Include:

- KPJ Healthcare Berhad: A premier private healthcare provider group in Malaysia, this group reported that there was a 12% increase in international patients in 2023. This medical tourism marketplace has been getting stronger, given that its focus is highly inclined toward patient-centric services, complete treatment packages, and engagement through digitization.

- IHH Healthcare Berhad: IHH Healthcare, under the brand name Parkway Pantai, witnessed a 15% increase in medical tourists hailing from China and the Middle East in the year 2023. Some of the reasons advanced medical technologies and an end-to-end patient experience make it one of the favorites for high-end medical treatments among patients.

- Prince Court Medical Centre: Luxury services and special care related to cardiology and orthopedics, Prince Court succeeded in generating an 18% revenue growth in the year 2023. The improvement in tailored treatment plans and international patient services has further increased its market viability.

- Gleneagles Hospitals: Gleneagle recorded a 14 % increase in visits recorded throughout the year 2023, by these two countries. Indonesia, and Thailand count Gleneagles Hospital for always making progressive improvement in advanced diagnostic tools, backed with the state-of-the-art Hospital and facilities that give rise to a certain reputation from the patient base.

- Sunway Medical Centre: Emphasising 'holistic healthcare', Sunway Medical Centre saw a 20% rise in patients last year for fertility and cosmetic surgery treatments. It has established tie-ups with international travel agencies and conducted strategic digital marketing campaigns for this success.

What's in Store for Malaysia Medical Tourism Market?

The Malaysia medical tourism market will witness steady growth by 2029, recording a CAGR that is respectable considering the forecast period. For the forecast period, some of the factors that might help in the growth would be competitive pricing, highly advanced healthcare facilities, and governmental support for the said segment.

- Increasing Focus on Specialized Treatments: Malaysia is expected to be in high demand, especially for specialized treatments involving fertility services, cardiology, and cosmetic procedures. The niche segments are very much in a state to attract high-value international patients who can contribute majorly to the growth of the market.

- Digital Transformation in Healthcare Services: Further integration of digital health platforms and telemedicine will develop Malaysia as a medical tourism hub. Such technologies will enable pre-consultations, smooth appointment scheduling, and follow-up care, thus making the patient journey seamless and less time-consuming.

- Expansion of Halal-Certified Healthcare Services: This involves increased access to halal accredited health facilities to meet their ever growing demands, which Malaysia might continue by expanding its healthcare services for Muslim tourists visiting Malaysia. This would relate to providing halal medicines and food and other patient care facilities in conformation to the Islamic way of life. As pointed above, this will eventually attract Malaysia as a favorable, reliable option for Muslim customers/patients.

- Emergence of Wellness Tourism: Wellness tourism, in the form of spa treatments, traditional medicine, and holistic therapies, is likely to be part of the Malaysia medical tourism landscape. This will merge healthcare with wellness for Malaysia to attract more health-conscious travelers of demography.

Future Outlook and Projections for Malaysia Medical Tourism Market on the Basis of Revenues in USD Billion, 2024-2029

Malaysia Medical Tourism Market Segmentation

- By Market Structure:

- Private Hospitals

- Government Hospitals

- Specialized Medical Centers

- Wellness Clinics

- Diagnostic Centers

- Dental Clinics

- Rehab Centers

- By Treatment Type:

- Cardiology

- Orthopedics

- Fertility Treatments (e.g., IVF)

- Cosmetic Surgery

- General Surgery

- Oncology

- Dental Procedures

- Wellness and Preventive Care

- By Patient Demographics:

- Indonesia

- China

- Middle East

- Europe

- United States

- Others

- By Revenue Streams:

- Hospital Fees

- Outpatient Services

- Inpatient Services

- Medical Tourism Packages

- Wellness and Alternative Treatments

- Others

- By Region:

- Northern (Penang, Kedah)

- Central (Kuala Lumpur, Selangor)

- Southern (Johor)

- Eastern (Terengganu, Kelantan)

- Western (Perak, Malacca)

Players Mentioned in the Report:

- Prince Court Medical Centre

- Gleneagles Hospital Kuala Lumpur

- Sunway Medical Centre

- Penang Adventist Hospital

- Island Hospital

- KPJ Healthcare Berhad

- Pantai Hospital Kuala Lumpur

- Mahkota Medical Centre

- Beverly Wilshire Medical Centre

- Institut Jantung Negara (National Heart Institute)

Key Target Audience:

- Private Healthcare Providers

- Medical Tourism Facilitators

- International Health Insurance Companies

- Government and Regulatory Bodies (e.g., Ministry of Health Malaysia)

- Research and Development Institutions

Time Period:

- Historical Period: 2018-2023

- Base Year: 2024

- Forecast Period: 2024-2029

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Value Chain Process-Role of Entities, Stakeholders, and Challenges

4.2. Patient Flow in Medical Tourism Market in Malaysia

4.3. Revenue Streams for Malaysia Medical Tourism Market

4.4. Business Model Canvas for Malaysia Medical Tourism Market

4.5. Patient Decision-Making Process

4.6. Medical Tourism Facilitator Role and Process

5.1. Domestic vs. International Patient Inflow in Malaysia, 2018-2024

5.2. Share of Major Medical Tourism Treatments in Malaysia, 2018-2024

5.3. Cost Comparison of Treatments in Malaysia vs. Competitor Countries, 2024

5.4. Number of Accredited Hospitals and Clinics by Region which are focused on Medical Tourism

8.1. Revenues, 2018-2024

8.2. Number of Patients, 2018-2024

9.1. By Market Structure (Private Hospitals, Government Hospitals, Specialized Clinics, Rehab Centers and Others), 2023-2024P

9.2. By Treatments (Cardiology, Orthopaedics, Fertility, Oncology, Cosmetic Surgery and Others), 2023-2024P

9.3. By Country of Origin (Indonesia, China, Middle East, Europe, USA and others), 2023-2024P

9.4. By Revenue Streams (Hospital Fees, Outpatient Services, Wellness Tourism), 2023-2024P

9.5. By Region (Northern, Central, Southern, Eastern, Western), 2023-2024P

10.1. Patient Landscape and Demographics

10.2. Patient Journey and Decision-Making Process

10.3. Needs, Preferences, and Pain Point Analysis

10.4. Gap Analysis Framework

11.1. Trends and Developments in Malaysia Medical Tourism Market

11.2. Growth Drivers for Malaysia Medical Tourism Market

11.3. SWOT Analysis for Malaysia Medical Tourism Market

11.4. Issues and Challenges for Malaysia Medical Tourism Market

11.5. Government Policies and Incentives for Medical Tourism in Malaysia

12.1. Insurance Penetration Rate for Medical Tourists in Malaysia, 2018-2029

12.2. Coverage for Common Medical Procedures and Trends Over Time

12.3. Role of Global Insurance Companies in Facilitating Medical Tourism

12.4. Partnership Models Between Healthcare Providers and Insurance Companies

12.5. Claims and Reimbursement Trends in Medical Tourism Insurance

15.1. Market Share of Key Healthcare Facilities in Malaysia Medical Tourism Market Basis Revenues/Number of Patients, 2023-2024P

15.1.1. Market Share of Key Hospitals, 2023-2024P

15.1.2. Market Share of Key Clinics, 2023-2024P

15.2. Benchmark of Key Competitors in Malaysia Medical Tourism Market Basis Operational and Financial Parameters

15.3. Strength and Weakness Analysis of Major Players

15.4. Business Model and USP Analysis of Competitors

15.5. Global Operations and Partnerships for Major Players

15.6. Recent Developments, Marketing Strategies, and Innovations

15.7. Gartner Magic Quadrant

15.8. Bowmans Strategic Clock for Competitive Advantage

16.1. Revenues, 2025-2029

16.2. Number of Patients, 2025-2029

16. Market Breakdown for Malaysia Medical Tourism Market Basis

16.1. By Market Structure (Private Hospitals, Government Hospitals, Specialized Clinics, Rehab Centers and Others), 2025-2029

16.2. By Treatments (Cardiology, Orthopaedics, Fertility, Oncology, Cosmetic Surgery and Others), 2025-2029

16.3. By Region (Northern, Central, Southern, Eastern, Western), 2025-2029

16.4. By Revenue Streams, 2025-2029

16.5. Recommendations

16.6. Opportunity Analysis

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the Ecosystem: Identify all demand-side and supply-side entities in the Malaysia Medical Tourism Market. This includes hospitals, clinics, medical tourism facilitators, government bodies, and patient demographics. Based on this ecosystem, shortlist the top 5-6 healthcare providers in the country based on financial data, patient volume, and reputation.

Sourcing: Utilize industry articles, secondary research, and proprietary databases to gather information about the medical tourism ecosystem and establish a foundational understanding of market dynamics.

Step 2: Desk Research

Exhaustive Secondary Research: Perform comprehensive desk research using diverse secondary and proprietary databases to analyze the market thoroughly. Collect data on revenue streams, major players, treatment costs, patient inflow, and other variables. Supplement this research with company-level analysis by referencing press releases, annual reports, financial statements, and government publications.

Market Insight Development: Aggregate industry-level insights to construct an overview of Malaysia's medical tourism landscape and the key entities operating within it.

Step 3: Primary Research

Stakeholder Interviews: Conduct in-depth interviews with C-level executives, healthcare providers, and medical tourism facilitators. This validates market hypotheses, authenticates statistical data, and gathers valuable operational insights.

Disguised Interviews: Approach companies under the guise of potential customers to validate information obtained from secondary sources. This method ensures the accuracy of data related to revenue streams, patient volumes, pricing, and value chains.

Bottom-to-Top Approach: Evaluate the patient inflow and revenue for each player to derive the overall market size and segmentation.

Step 4: Sanity Check

- Cross-Verification: Conduct top-to-bottom and bottom-to-top analyses to ensure the reliability of market size modeling. Perform sanity checks using multiple data points from both primary and secondary sources.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Malaysia medical tourism market is poised for significant growth, projected to reach MYR 15 Billion by 2029. This growth is driven by the country’s reputation for affordable, high-quality healthcare, government support, and increasing patient inflow from countries like Indonesia, China, and the Middle East.

Key players include KPJ Healthcare Berhad, IHH Healthcare Berhad, Prince Court Medical Centre, Gleneagles Hospitals, and Sunway Medical Centre. These institutions dominate the market due to their international accreditations, advanced infrastructure, and targeted marketing strategies.

Major growth drivers include Malaysia’s cost-competitive medical procedures, advanced healthcare facilities, and strategic location. Additionally, government initiatives such as fast-track medical visas and partnerships with international insurance companies further bolster market growth.

The market faces challenges such as regulatory hurdles, competition from other medical tourism hubs like Thailand and Singapore, and the need to build greater trust among international patients. Other barriers include logistical challenges, such as visa delays and language barriers, which may impact the overall patient experience.

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0