Maldives Luxury Apparel Market Outlook to 2030

By Market Structure, By Sales Channel, By Product Category, By Customer Nationality Cluster, By Price Tier, and By Atoll Cluster

Report Overview

Report Code

TDR0347

Coverage

Asia

Published

October 2025

Pages

80

Flexible Purchase Options

Select and purchase only the chapters you need for your strategic decisions

On This Page

Report Overview

The report titled “Maldives Luxury Apparel Market Outlook to 2030 — By Market Structure, By Sales Channel, By Product Category, By Customer Nationality Cluster, By Price Tier, and By Atoll Cluster” provides a comprehensive analysis of luxury apparel retail in the Maldives. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer-level profiling, issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major operators and brands active across resort boutiques, airport duty-free, and marina/village retail.

Report Coverage

Verified Market Sizing

Multi-layer forecasting with historical data and 5–10 year outlook

Deep-Dive Segmentation

Cross-sectional analysis by product type, end user, application and region

Competitive Benchmarking & Positioning

Market share, operating model, pricing and competition matrices

Actionable Insights & Risk Assessment

High-growth white spaces, underserved segments, technology disruptions and demand inflection points

Review Methodology & Data Structure

Preview report structure, data sources and research framework

Executive Summary

The report titled “Maldives Luxury Apparel Market Outlook to 2030 — By Market Structure, By Sales Channel, By Product Category, By Customer Nationality Cluster, By Price Tier, and By Atoll Cluster” provides a comprehensive analysis of luxury apparel retail in the Maldives. The report covers an overview and genesis of the industry, overall market size in terms of revenue, market segmentation; trends and developments, regulatory landscape, customer-level profiling, issues and challenges, and competitive landscape including competition scenario, cross-comparison, opportunities and bottlenecks, and company profiling of major operators and brands active across resort boutiques, airport duty-free, and marina/village retail. The report concludes with future market projections based on tourist arrivals, store counts and formats, product categories, atoll clusters, and channel mix, supported by cause-and-effect relationships and success case studies highlighting the major opportunities and cautions.

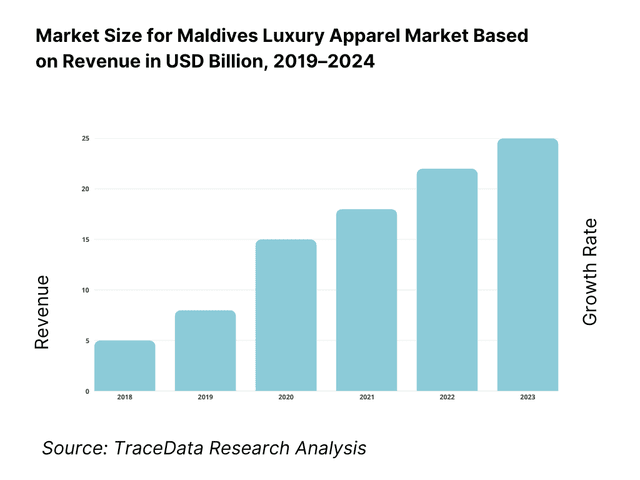

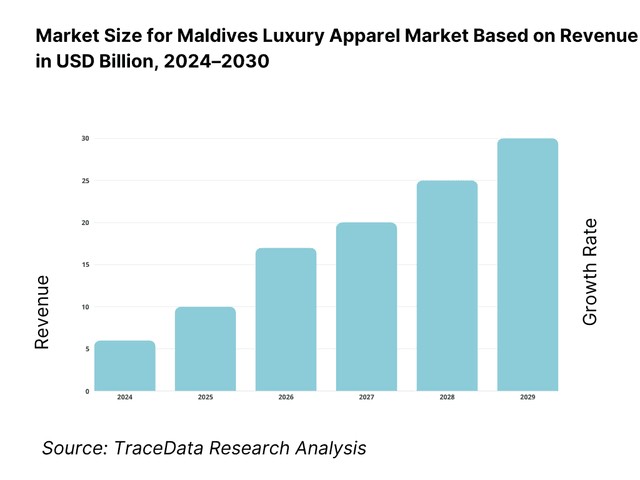

Maldives Luxury Apparel Market Overview and Size

The Maldives luxury apparel market is anchored by travel-retail and resort boutique spend. On a verified basis, airport duty-free sales totaled MVR 609.8 million; the same line rose to MVR 688.7 million subsequently, reflecting throughput and assortment momentum. This duty-free performance rides on record passenger flows and stable conversion—MACL reported total revenue of MVR 7.59 billion, rising to MVR 8.59 billion, within which duty-free is a core non-aeronautical lever.

Demand is concentrated around Velana International Airport/Malé and ultra-luxury resort clusters (Fari Islands, Noonu, Raa). The market’s customer base is fueled by 1,878,543 international arrivals and further acceleration to 2,046,615, with top source markets (India, Russia, UK, Germany, Italy, China) skewing to premium resort stays and high basket sizes for resortwear and accessories—supporting boutique footprints at Fari Marina Village, Cheval Blanc Randheli and Soneva.

What Factors are Leading to the Growth of the Maldives Luxury Apparel Market:

Record international demand funnel energizing resort and travel-retail: The Maldives welcomed 1,878,543 international visitors, rising to 2,046,615 the following year—an all-time high that expands the addressable pool for luxury apparel across resort boutiques, marinas and airside stores. Tourism is the economy’s prime foreign-exchange earner, reflected in services exports of US$4,695,879,775.39 from travel and other services, underscoring spending power circulating through hospitality retail. A solid macro backdrop supports this: national output stood at US$6,975,150,000 with GDP per capita at US$13,215.5, indicating strong purchasing capacity in tourism value chains (airlines, operators, retail concessions). These hard numbers—arrivals, services receipts and macro income—directly translate into higher store traffic, better conversion and premium basket composition for apparel and accessories on the islands.

Expanding bed capacity and resort footprint sustaining on-island purchasing: Retail thrives where guests sleep. Government statistics show average beds in operation at 60,656 (with 61,580 noted a year earlier) across resorts/hotels/guesthouses/safari vessels—ensuring dense, captive demand for apparel edits tailored to climate and occasionwear. Earlier official audits enumerated 168 resorts in the national census frame, while weekly/daily tourism updates track live capacity by class, enabling operators to calibrate assortments and drops to occupancy and island mix. A larger installed base of keys and beds magnifies in-resort footfall and the feasibility of pop-ups, capsule collections and concierge retail, particularly in high-luxury clusters.

Air connectivity and arrivals pipeline underpinned by macro resilience: Tourism inflows are reinforced by healthy system-wide aviation and macro conditions that channel shoppers into airside and resort retail. The monetary authority reports 3.64 billion US$ of imports—much of it consumer and retail goods—moving through the system, indicating robust logistics throughput to stock island outlets. The World Bank notes tourism-led expansion with arrivals at 2.05 million and real growth momentum, while IATA’s country brief highlights aviation’s structural role in jobs and GDP, reinforcing connectivity for high-spend travelers who buy apparel at departure and on-island. Together, these numbers validate a deep funnel for luxury transactions at both the airport and resorts.

Which Industry Challenges Have Impacted the Growth of the Maldives Luxury Apparel Market:

Ultra-dispersed geography complicates inventory, replenishment and cost-to-serve: The Maldives comprises 1,192 coral islands spread over roughly 90,000 km², with only 187 inhabited—an extreme dispersion that raises inter-island freight times for humidity-sensitive apparel and accessories. Store networks must stage inventory across resort-islands while relying on seaplanes and boats; government statistics show the resident base is distributed across atolls while the capital Malé concentrates administration, adding legs to every logistics move. This fragmentation, combined with tourism-plant distribution, demands higher safety stock and climate-controlled storage to prevent shrinkage and mildew—directly affecting sell-through for fashion operators.

External-balance stress tightens import liquidity for fashion supply: Luxury apparel is import-dependent; macro balance sheets matter. The World Bank reports the trade deficit widening to US$3.3 billion with official reserves at US$371.2 million (later US$395.4 million) and usable reserves at US$43.7 million, reducing import cover. MMA data show US$3.64 billion of total imports flowing in the year, underscoring exposure to FX availability for stocking and seasonal drops. Retailers must hedge procurement and shipping cycles against these constraints, prioritize fast-moving SKUs, and plan replenishment windows around reserve and liquidity updates to avoid missed high-season sales.

Seasonality and supply synchronization with accommodation capacity: Tourism bed-nights and arrivals oscillate through the monsoon cycle; official statistics record beds in operation averaging 60,656, with 61,580 the prior year, and monthly arrivals swinging into peak corridors. These numbers mean peak-season shelf availability is critical; late shipments risk stockouts, while off-peak over-allocation inflates holding risk for moisture-sensitive textiles. Operators must align allocations to resort occupancy tables and airlift cadence, staging capsule drops ahead of high-yield weeks and using bonded storage to balance inter-island flows.

What are the Regulations and Initiatives which have Governed the Market:

Indirect tax framework (GST/TGST) that directly affects invoicing, POS integration and pricing displays: The Maldives Inland Revenue Authority sets the general GST at 8% and tourism GST at 16% during the current period, with a legislated step-up of the tourism rate to 17% based on the Seventh Amendment and time-of-supply rules. For luxury apparel sold in resort shops and certain travel-retail contexts, POS systems and room-charge folios must map the correct tax class and rate to remain compliant. Operators planning capsule launches and promotional events should timestamp supplies carefully because rate changes are linked to invoice dates and delivery moments under the “time of supply” provisions.

Duty-free/duty-paid licensing with bonded-warehouse obligations: Duty-free retailing and bonded logistics are tightly codified. The “Regulation Governing Duty Free Business” requires each licensed operator to maintain at least one bonded warehouse, register the facility with Customs, and use serially numbered Customs declarations (multiple copies) when importing, transferring to warehouse, and supplying to the shop floor. Documentation must include commercial invoice, airway bill/bill of lading, packing list and insurance policy, with three-copy procedures when transferring goods to sales areas. These numeric and documentary controls govern fashion merchandise entering airside or designated duty-free zones and shape replenishment timelines.

Traveller allowances and restricted items affecting assortment and customer claims: Customs publishes personal-use concessions and restrictions that retailers and concierges must understand when advising guests on exportability of purchases and inbound items. Tourists aged 18+ may import for personal use up to 200 cigarettes, or 25 cigars, or 250 g of tobacco; separate rules apply to restricted goods such as liquor requiring prior approval. While apparel is generally unrestricted, these numeric thresholds shape mixed baskets (e.g., accessories plus gifts) and inform after-sales support (declarations at exit/entry). Duty-free/tax-free positioning must be balanced with accurate guest guidance on prohibited or restricted items.

Maldives Luxury Apparel Market Segmentation

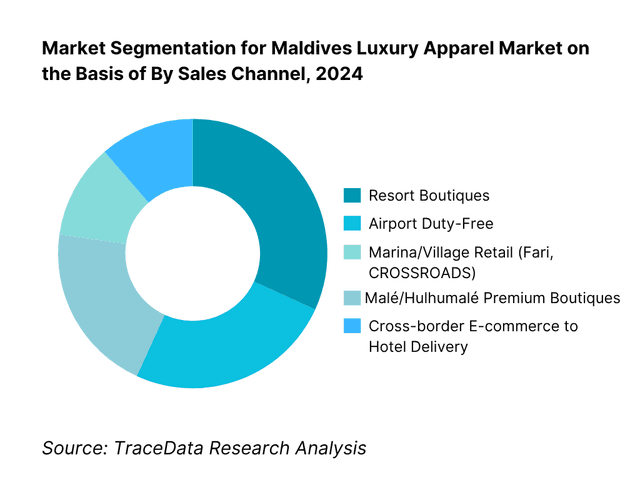

By Sales Channel: The Maldives luxury apparel market is segmented by channel into airport duty-free, resort boutiques, marina/village retail, Malé/Hulhumalé premium boutiques, and cross-border e-commerce to hotel delivery. Recently, resort boutiques hold the largest share because affluent guests spend the majority of their trip on private islands where curated shopping is embedded in the guest journey—think Cheval Blanc Randheli’s Maisons, Soneva’s “So Soneva” sustainable luxury concept, JOALI’s design-led boutique, and Fari Marina’s Rake & Revolution curation. Proximity to villas, personalized styling and capsule drops tailored to resort settings raise conversion and ticket sizes, surpassing airport-only purchases.

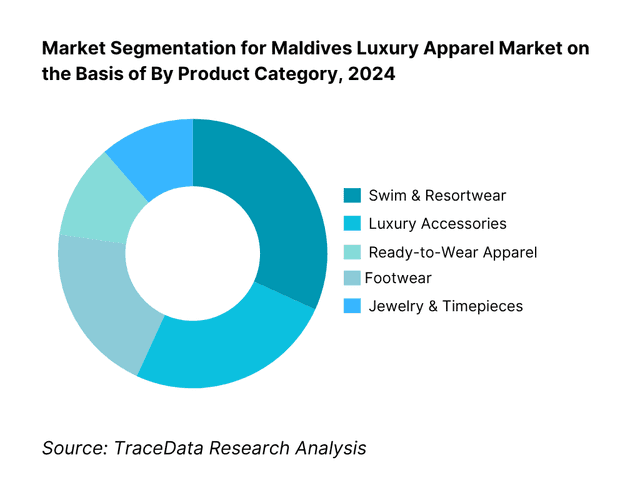

By Product Category: The Maldives luxury apparel market is segmented by product type into swim & resortwear, ready-to-wear apparel, luxury accessories, footwear, and jewelry & timepieces. Recently, swim & resortwear leads share because the destination is inherently leisure-led; guests often buy capsule wardrobes on-site aligned to sun, sand and yacht itineraries. Resort concepts curate edit-specific drops (kaftans, linens, island tailoring) and accessories (straw, raffia, silk scarves) to climate and dress codes, supported by collabs and pop-ups at properties like Ritz-Carlton/Fari Islands and Cheval Blanc Randheli. Purchase urgency (immediate wear), sizes, and omnichannel brand storytelling lift sell-through.

Competitive Landscape in Maldives Luxury Apparel Market

The Maldives luxury apparel market coalesces around a handful of channel anchors: MACL Duty Free at Velana; resort Maisons (Cheval Blanc Randheli; JOALI; Soneva) with curated luxury retail; and integrated marinas/villages (Fari Islands, CROSSROADS) that aggregate designer edits. This concentration gives operators with prime leases and curation capability outsized influence over assortment, pricing power, and experiential merchandising.

Name | Founding Year | Original Headquarters |

Maldives Airports Company Ltd | 2000 | Malé, Maldives |

Cheval Blanc Randheli | 2013 | Noonu Atoll, Maldives |

Soneva – “So Soneva” Boutiques | 1995 | Malé, Maldives |

Fari Marina Village | 2021 | North Malé Atoll, Maldives |

The Marina @ CROSSROADS | 2019 | Emboodhoo Lagoon, Maldives |

JOALI Maldives Boutique | 2018 | Raa Atoll, Maldives |

Patina Maldives (Capella Hotel Group) | 2021 | Fari Islands, Maldives |

Ritz-Carlton Maldives, Fari Islands | 2021 | North Malé Atoll, Maldives |

Island Bazaar | 2015 | Malé, Maldives |

The Rock Shop | 2019 | CROSSROADS, Maldives |

Some of the Recent Competitor Trends and Key Information About Competitors Include:

Maldives Airports Company Ltd – Duty Free Maldives: As the country’s primary airport retail operator, Duty Free Maldives reported a strong rebound in fashion and accessories sales in 2023, driven by increased international passenger arrivals. The operator enhanced assortments in premium accessories and lifestyle categories to capture higher basket values at Velana International Airport.

Cheval Blanc Randheli (LVMH Maisons): Positioned as a luxury fashion and lifestyle anchor within its ultra-premium resort, Cheval Blanc Randheli introduced capsule collections curated for honeymooners and long-stay guests. The Maison also emphasized personalized concierge shopping experiences, boosting conversion rates among high-net-worth travelers.

Soneva – “So Soneva” Boutiques: With a focus on sustainability and experiential retail, Soneva expanded its eco-conscious apparel and accessory lines in 2023, including collaborations with ethical designers. The boutique concept has become a differentiator for guests seeking luxury purchases aligned with sustainability values.

Fari Marina Village (The Rake & Revolution): This curated retail hub gained traction in 2023 with its “fully shoppable vacation” concept, featuring tailored resortwear, luxury watches, and menswear edits. The strategy of linking lifestyle, dining, and shopping has made the marina a prominent retail destination beyond the resorts.

JOALI Maldives Boutique: Known for blending art and fashion, JOALI introduced new limited-edition artisanal collections in 2023, combining local craftsmanship with international designer collaborations. The boutique’s art-immersive positioning has attracted affluent travelers seeking exclusive, collectible fashion items.

What Lies Ahead for Maldives Luxury Apparel Market?

The Maldives luxury apparel market is expected to witness steady growth in the coming years, supported by record tourist arrivals crossing 2.04 million visitors in the most recent year and a resilient GDP per capita of US$13,215.5. The combination of expanding resort bed capacity (60,656 operational beds) and increasing non-aeronautical revenues at Velana International Airport (duty-free sales MVR 688.7 million) provides a robust base for luxury fashion and accessories retail to thrive. Future momentum will be sustained by curated resortwear capsules, experiential shopping concepts, and strengthening air connectivity.

Rise of Resort-Centric Retail Models: The future of luxury apparel in the Maldives will see stronger integration of retail into the resort stay, with flagship boutiques and pop-up activations aligned with the guest journey. With 168 resorts already enumerated, each carrying in-house boutiques or collaborations, the retail experience will increasingly mirror the exclusivity and personalization of accommodation itself.

Focus on Experiential & Sustainable Fashion: Operators are expected to invest in sustainability-driven and experiential offerings, responding to consumer demand for reef-safe materials, artisanal collaborations, and eco-conscious supply chains. With services exports valued at US$4.69 billion, the luxury narrative is moving beyond consumption to responsible storytelling, ensuring apparel complements the Maldives’ positioning as a high-end eco-destination.

Expansion of Marina & Village Concepts: Integrated hubs like Fari Marina Village and CROSSROADS Maldives are set to expand their retail pull, combining dining, leisure, and fashion into lifestyle ecosystems. This clustering strategy is crucial in attracting non-resort traffic and enhancing dwell time, positioning marinas as complementary retail anchors to airport duty-free and resort boutiques.

Leveraging Digital Pre-Order & Concierge Platforms: Digital pre-order portals and concierge-driven delivery will define future retail, with technology enabling guests to shop before arrival and collect items at seaplane lounges or villas. The Maldives’ import channel of US$3.64 billion highlights the scale of merchandise movement; embedding digital tools ensures higher conversion and optimized inventory across dispersed islands.

Maldives Luxury Apparel Market Segmentation

By Sales Channel

Resort boutiques (one-island-one-resort stores)

Airport duty-free fashion & accessories (Velana)

Marina/village retail hubs (Fari Marina Village, CROSSROADS)

Malé/Hulhumalé premium boutiques & concept stores

Pop-ups & beach-club activations

Private/yacht onboard retail & concierge clienteling

Pre-arrival digital pre-order / click-&-collect (seaplane lounges)

By Product Category

Swim & resortwear (kaftans, linen sets, beach couture)

Ready-to-wear apparel (evening/occasion, island tailoring)

Luxury accessories (sunglasses, hats, scarves, SLGs)

Footwear (resort sandals, luxury sneakers)

Jewelry & timepieces (fine & fashion)

Limited capsules/collaborations (resort-exclusive drops)

By Price Tier

Haute/maison luxury

Core luxury

Accessible/contemporary luxury

Premium resort labels

Local premium/artisanal

By Purchase Occasion

Honeymoon & celebrations

Family luxury vacation

Yacht/marina stays & charters

Dive/surf & active leisure

MICE/retreats & elite events

Gifting & last-minute airport purchases

By Geography

Kaafu/Malé area (incl. VIA)

Baa

Noonu

Dhaalu

Raa & others (Lhaviyani, Ari, etc.)

Players Mentioned in the Report:

Dior

Louis Vuitton

Gucci

Prada

Montblanc

Michael Kors

Victoria’s Secret

Joali Boutique

Soneva Boutiques

Velaa Private Island Boutique

Four Seasons Boutique (Landaa/Voavah)

Anantara Kihavah Boutique

Maldives Duty Free (MACL)

The Rock Shop – Hard Rock/CROSSROADS

HLA Maldives

Key Target Audience

Airport retail concessionaires & operators

Resort owners & ultra-luxury GMs

Integrated marina/village developers & landlords

Luxury fashion & accessories brand principals

Logistics & bonded warehousing providers

Payments & fintech processors for travel-retail

Investments and venture capitalist firms

Government & regulatory bodies

Time Period:

Historical Period: 2019-2024

Base Year: 2025

Forecast Period: 2025-2030

Explore Flexible Purchase Options or Have Limited Budget?

Pay only for relevant chapters • Customizable report sections

Table of Contents

Choose individual sections to purchase. Mix and match as you like.

4.1. Delivery Model Analysis for Luxury Apparel in Maldives

4.2. Revenue Streams for Maldives Luxury Apparel Market

4.3. Business Model Canvas for Maldives Luxury Apparel Market

5.1. Resort-Owned Boutiques vs. Franchise/Brand-Owned Stores

5.2. Investment Model in Maldives Luxury Apparel Market (Concession, Franchise, Joint Ventures)

5.3. Comparative Analysis of Apparel Retail Funnel-Airport Duty-Free vs. Resort Boutiques vs. Marina Pop-ups

5.4. Luxury Spend Allocation by Tourist Type & Trip Cohort (Honeymoon, Family, Yacht, MICE)

6.1. Market Size Potential vs. Tourist Arrivals

6.2. Seasonality Impact (peak vs. lean quarters)

6.3. Demand-Supply Equilibrium (resort keys vs. boutique density)

6.4. Competitive Intensity & White-Space Mapping

8.1. Historical Revenues (USD Mn)

8.2. Year-on-Year Growth Rates

8.3. Key Developments & Milestones (new resort openings, luxury marina expansions, brand pop-ups)

9.1. By Market Structure (Resort-owned, Franchise, Concession, Local Multi-brand, Pop-ups)

9.2. By Product Category (Resort-Wear, Swimwear, Occasionwear, Footwear, Accessories)

9.3. By Customer Cluster (China, India, Russia/CIS, GCC, Europe/UK, Rest of World)

9.4. By Purchase Occasion (Honeymoon, Family Luxury Vacation, Yacht Stay, Celebration, MICE/Corporate Retreats)

9.5. By Channel Type (Airport Duty-Free, Marina Boutiques, Resort Concept Stores, On-board Retail, Digital Pre-orders)

9.6. By Price Tier (Haute/Ultra-Luxury, Luxury, Accessible Luxury, Premium Resort Labels, Local Premium Designers)

9.7. By Atoll Cluster (Kaafu/Malé, Baa, Noonu, Dhaalu, Raa & Others)

10.1. Tourist Client Landscape & Cohort Analysis (HNWI, UNWI, repeat vs. first-time visitors)

10.2. Luxury Apparel Purchase Decision-Making Process (concierge/butler influence, pre-arrival vs. impulse)

10.3. Program Effectiveness & ROI (room-charge integration, in-villa try-ons, gift-shop bundling)

10.4. Gap Analysis Framework (supply gaps, assortment mismatches, missed nationalities)

11.1. Trends & Developments (capsule collaborations, resort fashion shows, yacht retail)

11.2. Growth Drivers (airlift expansion, resort pipeline, duty-free upgrades, HNWI travel recovery)

11.3. SWOT Analysis for Maldives Luxury Apparel Market

11.4. Issues & Challenges (customs delays, humidity risk, seasonality, FX exposure)

11.5. Government Regulations (TGST/GST impact, bonded warehouse norms, labeling & HS codes)

12.1. Market Size & Future Potential (pre-order portals, digital clienteling)

12.2. Business Model & Revenue Streams (Click-&-Collect, in-villa ordering, post-stay e-commerce)

12.3. Delivery Models & Digital Channels (seaplane lounge pick-up, resort app integration)

12.4. Cross-Comparison of Leading Digital Initiatives (Pre-order platforms, CRM integration, personalized concierge apps)

15.1. Market Share of Key Players (Resort, Airport, Marina)

15.2. Benchmark of Key Competitors-Company Overview, USP, Business Strategy, Number of Outlets, Revenues, Pricing, Technology Used, Capsule Collections, Strategic Tie-ups, Marketing Initiatives, Major Clientele, Recent Developments

15.3. Operating Model Analysis (Franchise, Concession, Resort-owned)

15.4. Gartner Magic Quadrant for Maldives Luxury Apparel Retailers

15.5. Bowman’s Strategic Clock for Competitive Advantage

16.1. Revenues (USD Mn)

16.2. Forward Projections

16.3. Key Factors Driving Future Growth

17.1. By Market Structure (Resort-owned, Franchise, Concession, Local Multi-brand, Pop-ups)

17.2. By Product Category (Resort-Wear, Swimwear, Occasionwear, Footwear, Accessories)

17.3. By Customer Cluster (China, India, GCC, Russia/CIS, Europe/UK, ROW)

17.4. By Purchase Occasion (Honeymoon, Family, Yacht, Celebration, MICE)

17.5. By Channel Type (Duty-Free, Marina Boutiques, Resort Stores, Pop-ups, Digital Pre-orders)

17.6. By Price Tier (Haute/Ultra-Luxury, Luxury, Accessible Luxury, Premium Resort Labels, Local Premium)

17.7. By Atoll Cluster (Kaafu/Malé, Baa, Noonu, Dhaalu, Raa & Others)

Discuss a Customized Research Scope

Custom research scope • Tailored insights • Industry expertise

Research Methodology

Step 1: Ecosystem Creation

Map the ecosystem and identify all the demand-side and supply-side entities for the Maldives Luxury Apparel Market. Based on this ecosystem, we will shortlist leading 5–6 operators in the country including Maldives Airports Company Ltd – Duty Free Maldives, Cheval Blanc Randheli Boutiques, Soneva “So Soneva” Boutiques, Fari Marina Village (The Rake & Revolution), The Marina @ CROSSROADS, and JOALI Maldives Boutique, selected on the basis of their brand presence, market reach, and client base. Sourcing is conducted through official government portals (Ministry of Tourism, Maldives Inland Revenue Authority, Maldives Customs, Maldives Monetary Authority), SOE financial statements, industry articles, and multiple secondary and proprietary databases to perform desk research around the market and collate industry-level information.

Step 2: Desk Research

Subsequently, we engage in an exhaustive desk research process by referencing diverse secondary and proprietary databases. This approach enables us to conduct a thorough analysis of the market, aggregating industry-level insights. We delve into aspects like the volume of international arrivals (2,046,615 visitors), operational beds (60,656), trade and imports (US$3.64 billion), and non-aeronautical revenues (MVR 688.7 million duty-free sales). We supplement this with detailed examinations of company-level data, relying on sources like annual reports, press releases, government bulletins, and operator announcements. This process aims to construct a foundational understanding of both the market and the entities operating within it.

Step 3: Primary Research

We initiate a series of in-depth interviews with C-level executives and other stakeholders representing various Maldives Luxury Apparel Market operators including resort GMs, retail managers, airport duty-free concessionaires, and marina developers. This interview process serves a multi-faceted purpose: to validate market hypotheses, authenticate statistical data, and extract valuable operational and financial insights from these industry representatives. A bottom-to-top approach is undertaken to evaluate revenue contributions for each player, thereby aggregating to the overall market. As part of our validation strategy, our team executes disguised interviews wherein we approach each company under the guise of potential clients. This approach enables us to validate the operational and financial information shared by company executives, corroborating this data against what is available in secondary databases. These interactions also provide us with a comprehensive understanding of revenue streams, assortment strategies, bonded-warehouse processes, GST/TGST compliance, and inter-island logistics.

Step 4: Sanity Check

A bottom-to-top and top-to-bottom analysis along with market size modeling exercises is undertaken to assess the sanity of the process. Top-down modeling relies on audited duty-free revenues and macroeconomic indicators such as arrivals and bed capacity, while bottom-up modeling consolidates store-level and operator-level data derived from both desk and primary research. The final estimates are validated by reconciling the two approaches and resolving discrepancies through additional data checks and follow-up consultations, ensuring that the final market dataset is accurate, consistent, and reliable.

See What's Inside the Report

Get a preview of key findings, methodology and report coverage

Frequently Asked Questions

The Maldives Luxury Apparel Market holds significant potential, anchored by record-breaking international tourist arrivals of 2,046,615 visitors and an operational bed capacity of 60,656 across resorts, hotels, and guesthouses. The market is strengthened by rising per-capita income at US$13,215.5, which ensures sustained demand for high-value goods within luxury resorts and duty-free outlets. With increasing resort openings, integrated marinas like Fari Islands, and duty-free sales totaling MVR 688.7 million, the Maldives continues to evolve into a hub for experiential luxury shopping alongside its globally recognized hospitality sector.

The Maldives Luxury Apparel Market features several influential operators, including Maldives Airports Company Ltd – Duty Free Maldives, Cheval Blanc Randheli Boutiques, and Soneva “So Soneva” Boutiques. These players dominate the market through their strong retail positioning within ultra-luxury resorts and the primary airport hub. Other notable operators include Fari Marina Village (The Rake & Revolution), The Marina @ CROSSROADS, and JOALI Maldives Boutique, each leveraging unique concepts such as curated collections, experiential shopping, and art-immersive merchandising to capture affluent tourist spending.

Key growth drivers include the sustained rise in international arrivals, with 2.04 million visitors fueling demand for high-end shopping experiences across airport and resort retail. Expanding resort capacity, with over 168 resorts enumerated in the national census, further increases touchpoints for apparel sales through in-house boutiques and branded collaborations. Additionally, macroeconomic resilience, with services exports reaching US$4.69 billion, underpins the spending power of inbound tourists, strengthening the case for curated retail ecosystems such as marinas, village concepts, and premium resortwear boutiques.

The Maldives Luxury Apparel Market faces unique challenges shaped by geography, regulation, and macroeconomic dependencies. The nation’s 1,192 islands, with only 187 inhabited, complicates inter-island logistics, requiring higher safety stock and climate-controlled warehousing to avoid shrinkage. External balance pressures are evident with total imports reaching US$3.64 billion, while usable reserves stood at just US$43.7 million, tightening liquidity for inventory financing. Moreover, regulatory requirements such as GST/TGST compliance at 8% and 16% respectively and duty-free bonded obligations add complexity, raising operating costs for luxury apparel retailers across resort and travel-retail channels.a

License Options

PDF + Excel

Complete report package

$4,000

Excel Only

Data and analytics

$2,500

Custom Sections

Starts from $100

$0